You might also like

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- BB SIR QUESTION BANK DT May 22Document216 pagesBB SIR QUESTION BANK DT May 22Srushti AgarwalNo ratings yet

- The Payment of The Bonus Act 1965Document28 pagesThe Payment of The Bonus Act 1965Arpita Acharjya100% (1)

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- 1 - Income Tax IntroductionDocument14 pages1 - Income Tax IntroductionAkshitNo ratings yet

- Taxation - Direct & Indirect JUNE 2022Document10 pagesTaxation - Direct & Indirect JUNE 2022Rajni KumariNo ratings yet

- Karanam 14b PDFDocument101 pagesKaranam 14b PDFGovind BharathwajNo ratings yet

- Paper14b PDFDocument101 pagesPaper14b PDFGovind BharathwajNo ratings yet

- GR - III: Paper 14: Indirect and Direct Tax Management December 2011 Direct TaxationDocument101 pagesGR - III: Paper 14: Indirect and Direct Tax Management December 2011 Direct TaxationGovind BharathwajNo ratings yet

- Karanam 14b PDFDocument101 pagesKaranam 14b PDFGovind BharathwajNo ratings yet

- Submitted BY: A) DefinationsDocument35 pagesSubmitted BY: A) Definationsnitin0010No ratings yet

- 7th Term - Legal Frameworks of ConstructionDocument79 pages7th Term - Legal Frameworks of ConstructionShreedharNo ratings yet

- Deductions U/S 80C TO 80U: By: Sumit BediDocument69 pagesDeductions U/S 80C TO 80U: By: Sumit BediKittu NemaniNo ratings yet

- Project BBA 4th Semister FinanceDocument15 pagesProject BBA 4th Semister FinanceKunal Hire-PatilNo ratings yet

- Business Taxation 5445Document9 pagesBusiness Taxation 5445Muhammad Saleem MushtaqNo ratings yet

- 8 Salary11Document119 pages8 Salary11Pranav kumar PandeyNo ratings yet

- NMIMS Global Access School For Continuing Education (NGA-SCE) Course: Taxation-Direct and Indirect Internal Assignment Applicable For June 2020 ExaminationDocument10 pagesNMIMS Global Access School For Continuing Education (NGA-SCE) Course: Taxation-Direct and Indirect Internal Assignment Applicable For June 2020 ExaminationAnkit SharmaNo ratings yet

- Income From SalaryDocument21 pagesIncome From SalaryAditya Avasare60% (10)

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Payment of Bonus ActDocument9 pagesPayment of Bonus ActPradnya Ram PNo ratings yet

- Aditya Sharma - II Mid Term Paper Shikha MamDocument9 pagesAditya Sharma - II Mid Term Paper Shikha MamAditya SharmaNo ratings yet

- Extra Reading Time: 15 Minutes Writing Time: 03 Hours Maximum Marks: 100 Roll No.Document4 pagesExtra Reading Time: 15 Minutes Writing Time: 03 Hours Maximum Marks: 100 Roll No.Dj BravoNo ratings yet

- CSDocument26 pagesCSAnjuElsaNo ratings yet

- Aditya Sharma - MBA Dual - CTMDocument10 pagesAditya Sharma - MBA Dual - CTMAditya SharmaNo ratings yet

- 1 - Income Tax Introduction With Lecture NotesDocument13 pages1 - Income Tax Introduction With Lecture NotesRhea SharmaNo ratings yet

- Tax Credit 1Document18 pagesTax Credit 1Hani ShehzadiNo ratings yet

- Tax Rebate Claim Form-2019Document2 pagesTax Rebate Claim Form-2019Muhammad Hanif SuchwaniNo ratings yet

- 19279comp Sugans Finalold DT cp1Document7 pages19279comp Sugans Finalold DT cp1Nitin DaduNo ratings yet

- Chapter - 5 - TaxDocument15 pagesChapter - 5 - TaxAshek AHmedNo ratings yet

- Taxation - Direct and Indirect 2022Document10 pagesTaxation - Direct and Indirect 2022Sagar JindalNo ratings yet

- A Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingDocument12 pagesA Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingSipoy SatishNo ratings yet

- Incom TaxDocument54 pagesIncom TaxRamesh AlathurNo ratings yet

- Taxation Direct and IndirectDocument9 pagesTaxation Direct and Indirectdivyakashyapbharat1No ratings yet

- What Is TaxDocument5 pagesWhat Is TaxVenkatesh YerramsettiNo ratings yet

- AssignmentDocument19 pagesAssignmentAyesha ParveenNo ratings yet

- IncomeTax MaterialDocument91 pagesIncomeTax MaterialSandeep JaiswalNo ratings yet

- Notes On SalariesDocument18 pagesNotes On SalariesParul KansariaNo ratings yet

- Section Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionDocument32 pagesSection Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionanilpeddamalliNo ratings yet

- Income Tax in IndiaDocument19 pagesIncome Tax in IndiaConcepts TreeNo ratings yet

- Income Tax, IndiaDocument11 pagesIncome Tax, Indiahimanshu_mathur88No ratings yet

- Taxation Theory QuestionsDocument7 pagesTaxation Theory QuestionsPrince kumarNo ratings yet

- Army Institute of Law: Concept of Income and Total IncomeDocument17 pagesArmy Institute of Law: Concept of Income and Total IncomeMehr MunjalNo ratings yet

- SYBAF SEM IV TAXATION Unit IDocument5 pagesSYBAF SEM IV TAXATION Unit ISam RockerNo ratings yet

- Income From SalaryDocument103 pagesIncome From SalaryNAVEEN ROYNo ratings yet

- Topic 4 To 6Document9 pagesTopic 4 To 6srocky2000No ratings yet

- Final MF0003 2nd AssigDocument6 pagesFinal MF0003 2nd Assignigistwold5192No ratings yet

- Tax PlanningDocument28 pagesTax PlanningDishaNo ratings yet

- IFRS - 2017 - Solved QPDocument15 pagesIFRS - 2017 - Solved QPSharan ReddyNo ratings yet

- MockDocument18 pagesMockSmarty ShivamNo ratings yet

- Income Tax Test 1 & 2Document6 pagesIncome Tax Test 1 & 2Shital PujaraNo ratings yet

- Tax Planning in Respect of Employee's Remuneration ProjrctDocument15 pagesTax Planning in Respect of Employee's Remuneration ProjrctPreyNo ratings yet

- TrustDocument36 pagesTrustpremsuwaatiiNo ratings yet

- Exemptions Under Various Sections of The Income Tax, India: 1) Section 80 C (Limit: Rs. 1,00,000)Document5 pagesExemptions Under Various Sections of The Income Tax, India: 1) Section 80 C (Limit: Rs. 1,00,000)Ramakoteswar NampalliNo ratings yet

- GIT - Total Income Exam QP - 18-3-2020Document18 pagesGIT - Total Income Exam QP - 18-3-2020geddadaarunNo ratings yet

- 523247Document30 pages523247AgyeiNo ratings yet

- TAXATION - Various ConceptsDocument19 pagesTAXATION - Various Conceptslc17358No ratings yet

- Revised - DeductionsDocument29 pagesRevised - Deductionsdevkinger1212No ratings yet

- Decision ScienceDocument8 pagesDecision Sciencedivyakashyapbharat1No ratings yet

- Cost and Management AccountingDocument8 pagesCost and Management Accountingdivyakashyapbharat1No ratings yet

- Business LawDocument9 pagesBusiness Lawdivyakashyapbharat1No ratings yet

- Corporate FinanceDocument8 pagesCorporate Financedivyakashyapbharat1No ratings yet

- Business CommunicationDocument8 pagesBusiness Communicationdivyakashyapbharat1No ratings yet

- Business Ethics Governance and RiskDocument36 pagesBusiness Ethics Governance and Riskdivyakashyapbharat1No ratings yet

- Incentives and Benefits Available To Ssi Entrepreneurs 1Document8 pagesIncentives and Benefits Available To Ssi Entrepreneurs 1veenagadennavarNo ratings yet

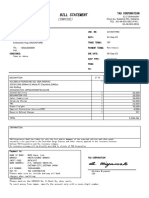

- Bill Statement: (Invoice)Document1 pageBill Statement: (Invoice)Terrence LimNo ratings yet

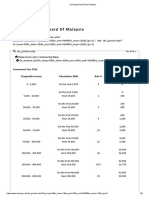

- Inland Revenue Board of Malaysia: Eng MalDocument6 pagesInland Revenue Board of Malaysia: Eng Malathirah jamaludinNo ratings yet

- (DHT) Core CriteriaDocument3 pages(DHT) Core CriteriaKeith McCannNo ratings yet

- Final Exam Moodle 1100 - 2019 BersDocument8 pagesFinal Exam Moodle 1100 - 2019 BersShawaz HusainNo ratings yet

- Econ 12 ReviewerDocument10 pagesEcon 12 Reviewerashyanna juarezNo ratings yet

- Assignment 1 PDFDocument8 pagesAssignment 1 PDFRose Aubrey A CordovaNo ratings yet

- Landmark Facility SolutionsDocument25 pagesLandmark Facility SolutionsGaurav Gupta8% (13)

- Annual Report 2022 23Document116 pagesAnnual Report 2022 23robertphilNo ratings yet

- Midterm Test AnswersDocument4 pagesMidterm Test AnswersSelly Cahya CamilaNo ratings yet

- Thesis On Unemployment in GhanaDocument6 pagesThesis On Unemployment in GhanaWhereCanIFindSomeoneToWriteMyCollegePaperUK100% (1)

- Financial Justification of ProjectsDocument5 pagesFinancial Justification of ProjectsDilippndtNo ratings yet

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 14Document28 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 14jasperkennedy091% (11)

- Economic Potential Tourism Post Covid19Document44 pagesEconomic Potential Tourism Post Covid19Shingo TadaNo ratings yet

- E PSDA Assignment For Project Management (BBA 302) Date of Submission: 13 April 2020Document12 pagesE PSDA Assignment For Project Management (BBA 302) Date of Submission: 13 April 2020Naman SethNo ratings yet

- Ramanujam - Chennai Metro WaterDocument1 pageRamanujam - Chennai Metro WaterlkjdfkallNo ratings yet

- The 2022 Mckinsey Global Payments ReportDocument53 pagesThe 2022 Mckinsey Global Payments ReportIrene SkorlifeNo ratings yet

- Barómetro Omt Del TurismoDocument18 pagesBarómetro Omt Del TurismoMara Villasanti PortilloNo ratings yet

- Five Year Plans: Presented By:Mr - Robin J Bhatti MSN-2 YearDocument36 pagesFive Year Plans: Presented By:Mr - Robin J Bhatti MSN-2 YearAsta LavistaNo ratings yet

- De Guzman, Nhevia - Written ReportDocument3 pagesDe Guzman, Nhevia - Written ReportNhevia de GuzmanNo ratings yet

- Cpec A Threat or A Game Changer For PakistanDocument3 pagesCpec A Threat or A Game Changer For PakistanAyesha FakharNo ratings yet

- 0469 MihamaDocument1 page0469 Mihamasaurav royNo ratings yet

- Internship Report F (Aaron Lopes)Document66 pagesInternship Report F (Aaron Lopes)Aarxn LopesNo ratings yet

- AbstractDocument45 pagesAbstractMelvin BrionesNo ratings yet

- Penawaran BerthaDocument2 pagesPenawaran BerthaTito AdiNo ratings yet

- Unit 2Document8 pagesUnit 2Tatiana DortaNo ratings yet

- CB Insights - Tech MA Report Q3 2023Document40 pagesCB Insights - Tech MA Report Q3 2023Ishrak ZamanNo ratings yet

- RGF Salary Watch 2020 - VIETNAM PDFDocument37 pagesRGF Salary Watch 2020 - VIETNAM PDFcuongtieubinh100% (1)

- E: G, I I: Mployment Rowth Nformalisation AND Other SsuesDocument23 pagesE: G, I I: Mployment Rowth Nformalisation AND Other SsuesHarpreetNo ratings yet

- Accountancy - Bills of Exchange - 230929 - 081107Document21 pagesAccountancy - Bills of Exchange - 230929 - 081107Amritha VNo ratings yet