You might also like

- Lesson 1 Business TaxesDocument6 pagesLesson 1 Business Taxesman ibeNo ratings yet

- Direct & Indirect Tax QuestionsDocument6 pagesDirect & Indirect Tax QuestionsSaiful FaisalNo ratings yet

- Requirements For Summary List of Sales and PurchasesDocument2 pagesRequirements For Summary List of Sales and PurchasesMary Joy Villanueva100% (2)

- F3FFA Chapter 5 Day Book PDFDocument40 pagesF3FFA Chapter 5 Day Book PDFMd Enayetur RahmanNo ratings yet

- OVERVIEW 2020 Printed Edition (iBOOK Version)Document21 pagesOVERVIEW 2020 Printed Edition (iBOOK Version)Quinciano MorilloNo ratings yet

- 43677RMO 3-2009 - Suspension GroundsDocument29 pages43677RMO 3-2009 - Suspension GroundsAnonymous OyhbxcjNo ratings yet

- Rmo 3-2009Document29 pagesRmo 3-2009sheena100% (2)

- VAT 404 - Guide For Vendors - External GuideDocument110 pagesVAT 404 - Guide For Vendors - External Guidesimphiwe8043No ratings yet

- Assignment From Victor QuiahDocument20 pagesAssignment From Victor QuiahSamah ShenhaNo ratings yet

- 25 Part II Finance Operations Information and Procedures HandbookDocument15 pages25 Part II Finance Operations Information and Procedures HandbookVijay MadhvanNo ratings yet

- IAS 12 TaxationDocument30 pagesIAS 12 Taxationwakemeup143No ratings yet

- 07 - Excise For Dealers PDFDocument57 pages07 - Excise For Dealers PDFsanku guptaNo ratings yet

- Transfer and Business Taxation: Module WritersDocument129 pagesTransfer and Business Taxation: Module WritersPaulita GomezNo ratings yet

- Vat Summary Notes Business TaxationDocument34 pagesVat Summary Notes Business TaxationNinNo ratings yet

- Kvat RulesDocument56 pagesKvat RulesShreyas IyengarNo ratings yet

- Procedure To Be Followed For Delhi Value Added TaxDocument6 pagesProcedure To Be Followed For Delhi Value Added TaxChirag MalhotraNo ratings yet

- TaxationDocument5 pagesTaxationWindylyn LalasNo ratings yet

- 2015 11 01 VAT Guidance On Invoices Sales Receipts Credit Notes and Debit NotesDocument26 pages2015 11 01 VAT Guidance On Invoices Sales Receipts Credit Notes and Debit NotesRoseNo ratings yet

- Details of VAT Form 240Document23 pagesDetails of VAT Form 240yoga_tptNo ratings yet

- Part I: Concept of Tax AdministrationDocument22 pagesPart I: Concept of Tax AdministrationShiela Marie Sta AnaNo ratings yet

- RSM Ashvir VAT Guide KenyaDocument29 pagesRSM Ashvir VAT Guide KenyaslowcouchNo ratings yet

- Excise Tax Returns User GuideDocument89 pagesExcise Tax Returns User GuideNoori Zahoor KhanNo ratings yet

- "VAT, VAT Audit and Statutory Role of Cost Accountant": Name - Richard D'silva Roll No - 09Document12 pages"VAT, VAT Audit and Statutory Role of Cost Accountant": Name - Richard D'silva Roll No - 09Richard DsilvaNo ratings yet

- TAX LAW and ADMINISTRATIONDocument11 pagesTAX LAW and ADMINISTRATIONReStyleNo ratings yet

- CPAR VAT (Batch 92) - HandoutDocument38 pagesCPAR VAT (Batch 92) - HandoutVan DahuyagNo ratings yet

- Income Tax - Ii: Semester - VIDocument154 pagesIncome Tax - Ii: Semester - VIiya100% (1)

- Accounting Technician Level 3 Module 3 Part 1Document29 pagesAccounting Technician Level 3 Module 3 Part 1Rona Amor MundaNo ratings yet

- Bir Ruling 044-10Document4 pagesBir Ruling 044-10Jason CertezaNo ratings yet

- VAT, Other Percentage Tax, Excise Tax and Documentary Stamp TaxDocument5 pagesVAT, Other Percentage Tax, Excise Tax and Documentary Stamp TaxJune Romeo ObiasNo ratings yet

- PM Reyes Notes On Taxation 2 Remedies Working Draft Updated 3 Mar 2013Document31 pagesPM Reyes Notes On Taxation 2 Remedies Working Draft Updated 3 Mar 2013Mycor Castillo OpsimaNo ratings yet

- AT - T COMMUNICATIONS SERVICES PHILIPPINES, INC., Vs CIR G.R. No. 182364 August 3, 2010Document4 pagesAT - T COMMUNICATIONS SERVICES PHILIPPINES, INC., Vs CIR G.R. No. 182364 August 3, 2010Francise Mae Montilla MordenoNo ratings yet

- Draft RR Registration EOPT - For Public ConsultationDocument18 pagesDraft RR Registration EOPT - For Public ConsultationGennelyn OdulioNo ratings yet

- 28689ipcc ST Vol1 cp7 PDFDocument0 pages28689ipcc ST Vol1 cp7 PDFGautam PradhanNo ratings yet

- Indirect Taxes: Excise, VAT and GSTDocument19 pagesIndirect Taxes: Excise, VAT and GSTmanikaNo ratings yet

- Taxation Law - 2013 Dimaampao Lecture Notes PDFDocument90 pagesTaxation Law - 2013 Dimaampao Lecture Notes PDFPaul Joseph MercadoNo ratings yet

- CPAR VAT (Batch 93) - HandoutDocument38 pagesCPAR VAT (Batch 93) - HandoutJuan Miguel UngsodNo ratings yet

- FORM - 704 Audit Report Under Section 61 of The Maharashtra Value Added Tax Act, 2002, Part - 1 Audit and Certification (See Rule 65)Document55 pagesFORM - 704 Audit Report Under Section 61 of The Maharashtra Value Added Tax Act, 2002, Part - 1 Audit and Certification (See Rule 65)maahi7No ratings yet

- Mail To Sana SB - Final QuerriesDocument2 pagesMail To Sana SB - Final QuerriesMuhammad Ammar KhanNo ratings yet

- Local Body TaxDocument13 pagesLocal Body Taxj787100% (1)

- BAF 306 BAF 3 - Registration and DeregistrationDocument18 pagesBAF 306 BAF 3 - Registration and Deregistrationyudamwambafula30No ratings yet

- VAT Booklet F.Y.2012-13Document20 pagesVAT Booklet F.Y.2012-13ankur2706No ratings yet

- How To Comply With Summary Lists of Sales and Purchases - Tax and Accounting Center, IncDocument8 pagesHow To Comply With Summary Lists of Sales and Purchases - Tax and Accounting Center, IncJames SusukiNo ratings yet

- Inome Tax April 15Document2 pagesInome Tax April 15brainNo ratings yet

- 4 Applied Indirect TaxationDocument316 pages4 Applied Indirect TaxationSanjay VanjayNo ratings yet

- Applied Indirect TaxationDocument349 pagesApplied Indirect TaxationVijetha K Murthy100% (1)

- Module 7 Business TaxationDocument6 pagesModule 7 Business Taxationfranz mallari0% (1)

- A Overview of Maharashtra Value Added Tax: IndexDocument10 pagesA Overview of Maharashtra Value Added Tax: IndexAdnan ParkarNo ratings yet

- Income Taxation Handout No. 1-02 Complete TextDocument21 pagesIncome Taxation Handout No. 1-02 Complete TextTong WilsonNo ratings yet

- VAT EXEMPTION UNDER SPECIAL LAWS - CONTEX CORPORATION vs. CIRDocument3 pagesVAT EXEMPTION UNDER SPECIAL LAWS - CONTEX CORPORATION vs. CIRChristine Gel MadrilejoNo ratings yet

- GST 21 Important QuestionsDocument2 pagesGST 21 Important QuestionsAngela PalNo ratings yet

- Taxation 1 Mod 4Document48 pagesTaxation 1 Mod 4Harui Hani-31No ratings yet

- Tax AdministrationDocument93 pagesTax AdministrationRobin LiuNo ratings yet

- Concept Note Sales Tax On ServicesDocument7 pagesConcept Note Sales Tax On ServicesAhmed RehanNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Wiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsFrom EverandWiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsNo ratings yet

- Balance SheetDocument2 pagesBalance SheetLabib ShahNo ratings yet

- Donald Chapter 1Document53 pagesDonald Chapter 1Labib ShahNo ratings yet

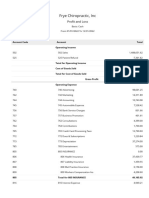

- Profit and LossDocument3 pagesProfit and LossLabib ShahNo ratings yet

- Lecture 04Document36 pagesLecture 04Labib ShahNo ratings yet

- Lecture 03Document30 pagesLecture 03Labib ShahNo ratings yet

- Behavioral Classification of CostDocument22 pagesBehavioral Classification of CostLabib ShahNo ratings yet

- 7 E's in Management AccountingDocument18 pages7 E's in Management AccountingLabib Shah100% (2)

- Semester Spring 2013 Investment Analysis & Portfolio Management-FIN730Document2 pagesSemester Spring 2013 Investment Analysis & Portfolio Management-FIN730Labib ShahNo ratings yet

- Semester Spring 2013 Investment Analysis & Portfolio Management-FIN730Document3 pagesSemester Spring 2013 Investment Analysis & Portfolio Management-FIN730Labib ShahNo ratings yet

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document1 pageIncome Tax Department: Computerized Payment Receipt (CPR - It)Labib ShahNo ratings yet

- Secretary of Finance v. Lazatin, G.R. No. 210588, November 29, 2016Document16 pagesSecretary of Finance v. Lazatin, G.R. No. 210588, November 29, 2016Christopher ArellanoNo ratings yet

- TAX-501 (Excise Taxes - Part 1)Document4 pagesTAX-501 (Excise Taxes - Part 1)lyndon delfinNo ratings yet

- Sec of Finance Purisima Vs Philippine Tobacco Institute IncDocument2 pagesSec of Finance Purisima Vs Philippine Tobacco Institute IncCharlotte100% (1)

- Public Finance and Taxation Strathmore University Notes and Revision Kit - Watermark PDFDocument340 pagesPublic Finance and Taxation Strathmore University Notes and Revision Kit - Watermark PDFAudrey OnyangoNo ratings yet

- Ceylon Tobacco Company Initiation ReportDocument32 pagesCeylon Tobacco Company Initiation ReportMurtaza JafferjeeNo ratings yet

- RL 4Document9 pagesRL 4surekha chandranNo ratings yet

- GST Notes For Sem 4Document7 pagesGST Notes For Sem 4prakhar100% (2)

- DTREDocument37 pagesDTREWYNBAD100% (2)

- Central Excise Vizag08022021Document35 pagesCentral Excise Vizag08022021do or dieNo ratings yet

- Iii. Trade Policies and Practices by Measure (1) I: Mauritius WT/TPR/S/198/Rev.1Document38 pagesIii. Trade Policies and Practices by Measure (1) I: Mauritius WT/TPR/S/198/Rev.1Nanda MunisamyNo ratings yet

- Application Form For Introduction of AFD-I Category ItemsDocument7 pagesApplication Form For Introduction of AFD-I Category ItemssukritgoelNo ratings yet

- Central Road Fund Act2000Document7 pagesCentral Road Fund Act2000Latest Laws TeamNo ratings yet

- TRIST Manual: Using Examples From TRIST NigeriaDocument90 pagesTRIST Manual: Using Examples From TRIST NigeriaseydianNo ratings yet

- Idt Notes June Dec 22Document232 pagesIdt Notes June Dec 22Sam SamNo ratings yet

- Taxation Direct and IndirectDocument304 pagesTaxation Direct and IndirectJagat Patel100% (1)

- Gar-7 Accounting Code of Excise DutiesDocument1 pageGar-7 Accounting Code of Excise Dutiesshiv_bhargava9368No ratings yet

- Tutorial 5Document5 pagesTutorial 5Lê Thiên Giang 2KT-19No ratings yet

- SUMMER TRAINING REPORT - CameyDocument99 pagesSUMMER TRAINING REPORT - CameycameyNo ratings yet

- 064&076-Association of Customs Brokers, Inc. v. The Municipal Board, 93 Phil. 103Document3 pages064&076-Association of Customs Brokers, Inc. v. The Municipal Board, 93 Phil. 103Jopan SJNo ratings yet

- Tax Cases 2Document146 pagesTax Cases 2Sylver JanNo ratings yet

- Tax AssignmentDocument5 pagesTax AssignmentdevNo ratings yet

- HB04102 Third Reading Sent To Senate ApprovedDocument3 pagesHB04102 Third Reading Sent To Senate ApprovedGladys Eleonor SaulonNo ratings yet

- Gems and JewelleryDocument10 pagesGems and JewelleryAakash ChadhaNo ratings yet

- Chart of Accounts For Government AccountingDocument10 pagesChart of Accounts For Government AccountingNeil ArmstrongNo ratings yet

- Solutions For GST Question BankDocument55 pagesSolutions For GST Question BankVarun VardhanNo ratings yet

- Critical Appraisal of The Nigeria Tax Laws As Administered by The Enugu State GovernmentDocument134 pagesCritical Appraisal of The Nigeria Tax Laws As Administered by The Enugu State GovernmentEmmanuel KingsNo ratings yet

- Center and State RelationsDocument21 pagesCenter and State RelationsPadma CheelaNo ratings yet

- Export Import Procedures: Name: Pratik Patil Class: Sybms A Roll No: 3243Document10 pagesExport Import Procedures: Name: Pratik Patil Class: Sybms A Roll No: 3243Alisha PimentaNo ratings yet

- Marketing Research On ArevaDocument94 pagesMarketing Research On ArevakmanilamNo ratings yet

- Sap MM Config Document Real Life Project PDFDocument182 pagesSap MM Config Document Real Life Project PDFmilosmartin100% (1)