You might also like

- PRELIM Chapter 9 10 11Document37 pagesPRELIM Chapter 9 10 11Bisag AsaNo ratings yet

- BAM031 - P2 - Q2 - Introduction To Gross Income, Inclusions and Exclusions - AnswersDocument8 pagesBAM031 - P2 - Q2 - Introduction To Gross Income, Inclusions and Exclusions - AnswersShane QuintoNo ratings yet

- Chapter 10 Tabag - Serrano NotesDocument5 pagesChapter 10 Tabag - Serrano NotesNatalie SerranoNo ratings yet

- Franco FM Taxation 7Document4 pagesFranco FM Taxation 7Kim FloresNo ratings yet

- Chapter 13 B&C Quiz ReviewDocument23 pagesChapter 13 B&C Quiz Reviewdianne caballeroNo ratings yet

- Income Taxation Preliminary Examination Income Tax On Individuals Multiple ChoicesDocument3 pagesIncome Taxation Preliminary Examination Income Tax On Individuals Multiple ChoicesJoel RagosNo ratings yet

- Chapter 4 EXERCISES - Estates and TrustsDocument9 pagesChapter 4 EXERCISES - Estates and TrustscathyydumpNo ratings yet

- Chapter 13 Part 1Document11 pagesChapter 13 Part 1Danielle Angel MalanaNo ratings yet

- Deductions and Exclusions for Individual and Corporate TaxpayersDocument4 pagesDeductions and Exclusions for Individual and Corporate TaxpayersIvan AnaboNo ratings yet

- Mantuano DeducDocument28 pagesMantuano DeducDonita MantuanoNo ratings yet

- INCOMETAX M45 ReviewerDocument15 pagesINCOMETAX M45 ReviewerCaryl Isabel Francisco100% (1)

- AssesmentDocument12 pagesAssesmentMaya Keizel A.No ratings yet

- Foreign Tax CreditDocument2 pagesForeign Tax CreditSophiaFrancescaEspinosaNo ratings yet

- Lesson 6 Business TaxesDocument9 pagesLesson 6 Business TaxesReino CabitacNo ratings yet

- W7-Module Concept of Income-Part 2Document21 pagesW7-Module Concept of Income-Part 2Danica VetuzNo ratings yet

- Statement of Changes in EquityDocument8 pagesStatement of Changes in EquityGonzalo Jr. RualesNo ratings yet

- Intro To Regular Income TaxationDocument2 pagesIntro To Regular Income TaxationhotgirlsummerNo ratings yet

- Chap. 6 8Document44 pagesChap. 6 82vpsrsmg7jNo ratings yet

- Solution Manual Chapter 13 B MC Problems 1Document3 pagesSolution Manual Chapter 13 B MC Problems 1Mallet S. GacadNo ratings yet

- Coffee Klatch Ratios BreakdownDocument21 pagesCoffee Klatch Ratios BreakdownJonalyn TaboNo ratings yet

- Chapter 9 TaxDocument27 pagesChapter 9 TaxJason MalikNo ratings yet

- Friendship CoDocument3 pagesFriendship CoKeahlyn BoticarioNo ratings yet

- Quiz - Chapter 4 - Partnership Liquidation - 2021 EditionDocument7 pagesQuiz - Chapter 4 - Partnership Liquidation - 2021 EditionYam SondayNo ratings yet

- TRUE OR FALSE (p.179,180)Document2 pagesTRUE OR FALSE (p.179,180)Aberin GalenzogaNo ratings yet

- Income Taxation Banggawan 2019 Ed Solution ManualDocument40 pagesIncome Taxation Banggawan 2019 Ed Solution ManualJesse100% (1)

- Income tax calculations for non-resident citizens and aliensDocument3 pagesIncome tax calculations for non-resident citizens and aliensRosemarie CruzNo ratings yet

- Chapter 6 Income Tax by BanggawanDocument11 pagesChapter 6 Income Tax by BanggawanEarth PirapatNo ratings yet

- Tax Reviewer PDFDocument2 pagesTax Reviewer PDFwhin LimboNo ratings yet

- Chapter 6 Capital Gains TaxationDocument4 pagesChapter 6 Capital Gains TaxationBisag AsaNo ratings yet

- DocxDocument5 pagesDocxJohn Vincent CruzNo ratings yet

- Diana May Company IssuedDocument1 pageDiana May Company IssuedQueen ValleNo ratings yet

- Chapter 3 SolmanDocument23 pagesChapter 3 SolmanUchayyaNo ratings yet

- Ampongan SolmanDocument25 pagesAmpongan SolmanNikolina100% (2)

- Intermediate Accounting 1 Solution Manual: Chapter 15 - Property, Plant and Equipment To Chapter 17 - Depletion of Mineral ResourcesDocument20 pagesIntermediate Accounting 1 Solution Manual: Chapter 15 - Property, Plant and Equipment To Chapter 17 - Depletion of Mineral ResourcesMckenzieNo ratings yet

- Strategic Tax Management - Week 5Document37 pagesStrategic Tax Management - Week 5Arman DalisayNo ratings yet

- Income Taxation Quiz2Document3 pagesIncome Taxation Quiz2Printing PandaNo ratings yet

- Exercises Budgeting and Responsibility Problems W - Solutions 1Document10 pagesExercises Budgeting and Responsibility Problems W - Solutions 1Kristine NunagNo ratings yet

- Output TaxDocument15 pagesOutput TaxAmie Jane MirandaNo ratings yet

- I Can Make It Corp financial performance 2020 vs 2019Document3 pagesI Can Make It Corp financial performance 2020 vs 2019Evan MiñozaNo ratings yet

- VAT (Chapter 8 Compilation of Summary)Document36 pagesVAT (Chapter 8 Compilation of Summary)Dianne LontacNo ratings yet

- Statement of Changes in Comprehensive IncomeDocument33 pagesStatement of Changes in Comprehensive Incomeellyzamae quiraoNo ratings yet

- INCOTAX - Multiple Choices - Problems Part 1Document3 pagesINCOTAX - Multiple Choices - Problems Part 1Harvey100% (1)

- H04 - Final Income TaxationDocument6 pagesH04 - Final Income Taxationnona galidoNo ratings yet

- NAME Chapter7Document10 pagesNAME Chapter7Shawn VerzalesNo ratings yet

- Exclusions and Inclusions - MANTUANODocument8 pagesExclusions and Inclusions - MANTUANODonita MantuanoNo ratings yet

- Joey, A non-VAT Taxpayer Purchased Merchandise Worth P11,200, VATDocument10 pagesJoey, A non-VAT Taxpayer Purchased Merchandise Worth P11,200, VATLeah Isabelle Nodalo DandoyNo ratings yet

- Cfas (Pas 16)Document7 pagesCfas (Pas 16)Niña Mae VerzosaNo ratings yet

- Regular Income Tax Chapter on Exclusions from Gross IncomeDocument15 pagesRegular Income Tax Chapter on Exclusions from Gross IncomeJolina AynganNo ratings yet

- October To September Sales Report Movies by GenreDocument3 pagesOctober To September Sales Report Movies by GenreAngelica Austria-MantalNo ratings yet

- Group 1 - Chapter 16Document8 pagesGroup 1 - Chapter 16Cherie Soriano AnanayoNo ratings yet

- Employee Benefits Exercises-ANSWERSDocument12 pagesEmployee Benefits Exercises-ANSWERSfaye pantiNo ratings yet

- TaxiDocument12 pagesTaxiKaiden AmaruNo ratings yet

- Chap. 13A 15BDocument72 pagesChap. 13A 15B2vpsrsmg7jNo ratings yet

- Excise TaxDocument15 pagesExcise TaxDaniella MananghayaNo ratings yet

- Database Management Systems ExplainedDocument7 pagesDatabase Management Systems ExplainedKrisshaNo ratings yet

- MixDocument32 pagesMixUnnecessary BuyingNo ratings yet

- Cost of Goods Manufactured for Christian CompanyDocument10 pagesCost of Goods Manufactured for Christian CompanyAira Santos VibarNo ratings yet

- EX EX EX EX: Regular Income TaxDocument7 pagesEX EX EX EX: Regular Income TaxMary Leigh TenezaNo ratings yet

- CHAPTER 9 To CHAPTER 15 ANSWERSDocument38 pagesCHAPTER 9 To CHAPTER 15 ANSWERSryanmartintaanNo ratings yet

- True or FalseDocument76 pagesTrue or FalsepangytpangytNo ratings yet

- FINALDocument30 pagesFINALaskmeeNo ratings yet

- MA HR Issues Around The WorldDocument96 pagesMA HR Issues Around The WorldpensiontalkNo ratings yet

- SER Memo 11 27 17Document8 pagesSER Memo 11 27 17Adam BelzNo ratings yet

- Landing - Jobs - Tech Careers Report PT v1.2Document46 pagesLanding - Jobs - Tech Careers Report PT v1.2favaoNo ratings yet

- Compensation ManagementDocument64 pagesCompensation ManagementNagireddy KalluriNo ratings yet

- Taxable Salary IncomeDocument253 pagesTaxable Salary IncomedjbbuzzzNo ratings yet

- Nascon Offer LetterDocument5 pagesNascon Offer LetterMarcus AntoniusNo ratings yet

- Form No. 16: Part ADocument7 pagesForm No. 16: Part AFuture ArtistNo ratings yet

- Lovely Professional University Academic Task-1 Mittal School of BusinessDocument9 pagesLovely Professional University Academic Task-1 Mittal School of BusinessPankaj MahantaNo ratings yet

- Usaid70 02Document5 pagesUsaid70 02api-304173542No ratings yet

- PLS Taxation QA FinalDocument24 pagesPLS Taxation QA FinalTAU MU OFFICIALNo ratings yet

- Case Analysis On Welcome Aboard Group 8Document7 pagesCase Analysis On Welcome Aboard Group 8Aishwarya SolankiNo ratings yet

- Taxation of Individuals 6th Edition Spilker Solutions Manual 1Document47 pagesTaxation of Individuals 6th Edition Spilker Solutions Manual 1robert100% (39)

- Jordan, Reynier I - Mba - SMBP - Final OutputDocument11 pagesJordan, Reynier I - Mba - SMBP - Final OutputEnergy Trading QUEZELCO 1No ratings yet

- Wage and Salary AdministrationDocument27 pagesWage and Salary AdministrationVipin Cool100% (1)

- Arun Kumar v. Union of India, (2007) 1 SCC 732Document32 pagesArun Kumar v. Union of India, (2007) 1 SCC 732Modassir Husain KhanNo ratings yet

- Class DiagramDocument2 pagesClass DiagramJongNo ratings yet

- Supreme Court upholds Christmas bonus under 1972 CBA despite 13th month pay lawDocument3 pagesSupreme Court upholds Christmas bonus under 1972 CBA despite 13th month pay lawChristelle Ayn BaldosNo ratings yet

- Kanga & Palkhivala IT Act 10th Ed Vol II CH 12G-14Document208 pagesKanga & Palkhivala IT Act 10th Ed Vol II CH 12G-14lokeshNo ratings yet

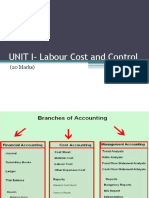

- Labour Cost and ControlDocument65 pagesLabour Cost and Controlaishwarya raikarNo ratings yet

- Government Withholding Tax GuideDocument9 pagesGovernment Withholding Tax GuideChristian AnresNo ratings yet

- Chapter 4 Income From SalariesDocument106 pagesChapter 4 Income From SalariesYogesh Sahani50% (2)

- CARE GBV - Concept Note Summary Budget TDocument10 pagesCARE GBV - Concept Note Summary Budget TtawandaeltonNo ratings yet

- IncomeTax Ordinance, 1984 (English)Document277 pagesIncomeTax Ordinance, 1984 (English)enamulNo ratings yet

- Buckwold 20ce sm04Document68 pagesBuckwold 20ce sm04Kailash Kumar100% (1)

- Employee Transportation Benefits Are Good For BusinessDocument5 pagesEmployee Transportation Benefits Are Good For BusinessahmedtaniNo ratings yet

- GST & BAS Detailed HandbookDocument60 pagesGST & BAS Detailed Handbooktestnation100% (1)

- CFP Mock Test Tax PlanningDocument8 pagesCFP Mock Test Tax PlanningDeep Shikha67% (3)

- HR E-BookDocument8 pagesHR E-BookAttila G.No ratings yet

- Times Review Classifieds: Aug. 27, 2015Document8 pagesTimes Review Classifieds: Aug. 27, 2015TimesreviewNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Tax Savvy for Small Business: A Complete Tax Strategy GuideFrom EverandTax Savvy for Small Business: A Complete Tax Strategy GuideRating: 5 out of 5 stars5/5 (1)

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- Freight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesFrom EverandFreight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesRating: 5 out of 5 stars5/5 (1)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)