You might also like

- Ejercicio Portafolio Óptimo A (DESARROLLO)Document5 pagesEjercicio Portafolio Óptimo A (DESARROLLO)Valeria MaldonadoNo ratings yet

- Portfolio Optimization ResultsDocument229 pagesPortfolio Optimization ResultsvaskoreNo ratings yet

- Vanguard Index Fund Performance and California REIT ReturnsDocument5 pagesVanguard Index Fund Performance and California REIT ReturnsMuhammad IlyasNo ratings yet

- Ta2 1-3Document12 pagesTa2 1-3Marcelo DelgadilloNo ratings yet

- Sumativa 1 Exp 2 FinDocument14 pagesSumativa 1 Exp 2 FinRoger Danilo Lujan ArmasNo ratings yet

- S&P 500 and Bancolombia stock performance and correlation from 2015-2020Document4 pagesS&P 500 and Bancolombia stock performance and correlation from 2015-2020anonimo centenarioNo ratings yet

- Prueba Largo Plazo A.KDocument13 pagesPrueba Largo Plazo A.KAngelica ReyNo ratings yet

- Average Monthly Returns: Date S&P 500 3 Month T-Bill RJR HasbroDocument16 pagesAverage Monthly Returns: Date S&P 500 3 Month T-Bill RJR HasbroKing CheungNo ratings yet

- Share Price Data Saved AsDocument15 pagesShare Price Data Saved AsMaithri Vidana KariyakaranageNo ratings yet

- Alex Sharpe 1Document4 pagesAlex Sharpe 1Twisha Priya100% (1)

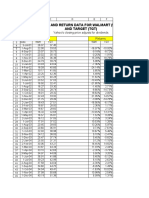

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument13 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsArisha KhanNo ratings yet

- Alex Case StudyDocument4 pagesAlex Case StudyPratiksha GhosalNo ratings yet

- Weekly DataDocument22 pagesWeekly DataAshishNo ratings yet

- 3) LabS 03 2023 First Part - RIFATTADocument11 pages3) LabS 03 2023 First Part - RIFATTAgiovanni lazzeriNo ratings yet

- Date S&P500 Aapl MSFT BAC XOM PFE Month TDocument17 pagesDate S&P500 Aapl MSFT BAC XOM PFE Month TZeynep DerinözNo ratings yet

- Beta Management CorpDocument11 pagesBeta Management CorpKaneez FatimaNo ratings yet

- Potfolio ManagementDocument3 pagesPotfolio Managementsomya guptaNo ratings yet

- Date S&P500 Aapl MSFT BAC XOM PFE Correlation MatrixDocument14 pagesDate S&P500 Aapl MSFT BAC XOM PFE Correlation MatrixZeynep DerinözNo ratings yet

- HC Investimentos - HedgeDocument11 pagesHC Investimentos - HedgeFabiano MorattiNo ratings yet

- Solución: Rentabilidad Esperada Volatilidad Coeficiente de Variación Varianza Covarianza Beta 1.98 1.2Document6 pagesSolución: Rentabilidad Esperada Volatilidad Coeficiente de Variación Varianza Covarianza Beta 1.98 1.2Yessica MacedaNo ratings yet

- EJERICICIO 3 - Valor en Riesgo (VAR) - SEMANA 12Document299 pagesEJERICICIO 3 - Valor en Riesgo (VAR) - SEMANA 12aidaNo ratings yet

- Topicos Lucastorres UssDocument10 pagesTopicos Lucastorres UssCaslu MontanaNo ratings yet

- Efficient Frontier: Month HDFC TCS % Return TCS % Return HDFC HDFC TCS RP S.D Portfolio Mix (W)Document1 pageEfficient Frontier: Month HDFC TCS % Return TCS % Return HDFC HDFC TCS RP S.D Portfolio Mix (W)Rajarshi DaharwalNo ratings yet

- Alex Sharpe CaseDocument17 pagesAlex Sharpe Casemusunna galibNo ratings yet

- Monthly and quarterly KPI trackingDocument30 pagesMonthly and quarterly KPI trackingPaulo Victor PinheiroNo ratings yet

- CFin I CAPM AutomobilesDocument8 pagesCFin I CAPM Automobilessumeet kumarNo ratings yet

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Portofolio Correlation - Kaunang, MarioDocument3 pagesPortofolio Correlation - Kaunang, Mariomario kaunangNo ratings yet

- Stock Price Performance and Correlation AnalysisDocument3 pagesStock Price Performance and Correlation Analysismario kaunangNo ratings yet

- Varianza y CovarianzaDocument4 pagesVarianza y CovarianzaWendy SequeirosNo ratings yet

- Date Alcargo Logistics Share Price Alcargo Change % Annualized Allcargo Nifty 50 Nifty Change %Document17 pagesDate Alcargo Logistics Share Price Alcargo Change % Annualized Allcargo Nifty 50 Nifty Change %Deepak KshirsagarNo ratings yet

- Fin RatiosDocument7 pagesFin Ratiosakankshag_13No ratings yet

- 02.09 Frontera EficienteDocument11 pages02.09 Frontera Eficientelaila89No ratings yet

- BreakdownDocument103 pagesBreakdownhandiNo ratings yet

- Fin 213 Assignment ExcelDocument47 pagesFin 213 Assignment ExcelMICHEALA JANICE JOSEPHNo ratings yet

- S&P 500 y BancosDocument5 pagesS&P 500 y BancosJavier D'cNo ratings yet

- Excel Lecture 3a - SolvedDocument22 pagesExcel Lecture 3a - SolvedRimpy SondhNo ratings yet

- Mercado Bursatil BrasilDocument18 pagesMercado Bursatil BrasilLina AlvarezNo ratings yet

- % Var - Mastercard: Gráfico de BetaDocument16 pages% Var - Mastercard: Gráfico de BetaMario RefNo ratings yet

- Plan Vs ActDocument1 pagePlan Vs Actsyednehal21No ratings yet

- MES Mead Corp. (%) Boise Cascade (%) Nike Inc. (%)Document4 pagesMES Mead Corp. (%) Boise Cascade (%) Nike Inc. (%)Enrique de Jesús Ramos CastelanNo ratings yet

- var_RINDocument2 pagesvar_RINRaul Ronaldo Romero TolaNo ratings yet

- Alex Sharpe S PortfolioDocument3 pagesAlex Sharpe S Portfolionishnath satyaNo ratings yet

- Assignment Regression Beta 03Document5 pagesAssignment Regression Beta 03John DummiNo ratings yet

- Beta CalculationDocument2 pagesBeta CalculationvarunsardaindoreNo ratings yet

- Portofolio Efficient Frontier - Kaunang, MarioDocument3 pagesPortofolio Efficient Frontier - Kaunang, Mariomario kaunangNo ratings yet

- S&P 500, Reynolds, Hasbro stock returns & analysisDocument3 pagesS&P 500, Reynolds, Hasbro stock returns & analysisSiona Maria NathanielNo ratings yet

- Alex Sharp's PortfolioDocument6 pagesAlex Sharp's PortfolioFurqanTariqNo ratings yet

- Performance MeasurementDocument14 pagesPerformance Measurementamirabbas mollaeiNo ratings yet

- IV PortDocument19 pagesIV PortAchilles AkhilNo ratings yet

- Fecha S&P 500 LN S&P 500 ABT LN Abt Valor NasvDocument12 pagesFecha S&P 500 LN S&P 500 ABT LN Abt Valor NasvKaren Xiomara Galeano ContrerasNo ratings yet

- AnnexuresDocument23 pagesAnnexuresMohit AnandNo ratings yet

- Date Adj Close CCR CCR Adj Close CCR CCR CCRDocument17 pagesDate Adj Close CCR CCR Adj Close CCR CCR CCRRanjith KumarNo ratings yet

- ColoviviDocument8 pagesColoviviBENNo ratings yet

- Bitcoin Price HistoryDocument2 pagesBitcoin Price HistoryLemuel Kim TabinasNo ratings yet

- EvoviviDocument8 pagesEvoviviBENNo ratings yet

- Midterm - Invest & Port MGTDocument11 pagesMidterm - Invest & Port MGTMohamed HelmyNo ratings yet

- HC Investimentos - Como Calcular A Correlação Entre InvestimentosDocument7 pagesHC Investimentos - Como Calcular A Correlação Entre InvestimentosMario Sergio GouveaNo ratings yet

- 3.2.2b Tính Beta Và Chi Phi Von ChuDocument10 pages3.2.2b Tính Beta Và Chi Phi Von ChuLê TiếnNo ratings yet

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Deen Dayal Upadhyaya Gorakhpur University, Gorakhpur: FORM NO. 20213390011Document2 pagesDeen Dayal Upadhyaya Gorakhpur University, Gorakhpur: FORM NO. 20213390011Aditya ChaurasiaNo ratings yet

- Valuation With The Moving Average Price: Problems With Stock CoverageDocument6 pagesValuation With The Moving Average Price: Problems With Stock CoverageUday HawaldarNo ratings yet

- CHAPTER 4 - Job Order Costing: Learning ObjectivesDocument3 pagesCHAPTER 4 - Job Order Costing: Learning Objectivesyes yesnoNo ratings yet

- Ross12e Chapter05 TBDocument19 pagesRoss12e Chapter05 TBHải YếnNo ratings yet

- Lane County Holiday Farm Fire Response - Fee WaiversDocument19 pagesLane County Holiday Farm Fire Response - Fee WaiversSinclair Broadcast Group - EugeneNo ratings yet

- ShellEnergy Bill 119130235Document6 pagesShellEnergy Bill 119130235Madalina Gr100% (1)

- Module 7 8 Contemporary World College Contemporary World 2Document6 pagesModule 7 8 Contemporary World College Contemporary World 2Ian Nick NaldaNo ratings yet

- NEGOTIN FINAL EXAM QuestionDocument1 pageNEGOTIN FINAL EXAM Questionjan bert0% (1)

- Solution Manual For Introduction To Finance 17th Edition Ronald W MelicherDocument24 pagesSolution Manual For Introduction To Finance 17th Edition Ronald W MelicherCrystalPhamfcgz95% (41)

- Ipsos Primary Consumer Sentiment IndexDocument3 pagesIpsos Primary Consumer Sentiment IndexAgie RifanggiNo ratings yet

- CICPA Contract Report SampleDocument1 pageCICPA Contract Report SampleRhea RamirezNo ratings yet

- ARCHITECTURAL DESIGN SITE PLANNINGDocument5 pagesARCHITECTURAL DESIGN SITE PLANNINGMarnie Shane GamezNo ratings yet

- Profitability SamsungDocument5 pagesProfitability SamsungDACLUB IBSbNo ratings yet

- IIT TenderDocument10 pagesIIT TenderB DroidanNo ratings yet

- NEW PRICE LISTDocument7 pagesNEW PRICE LISTmed b nasrNo ratings yet

- IMFDocument21 pagesIMFPrem Chand ThakuriNo ratings yet

- Global Free Trade Has Done More Harm Than GoodDocument1 pageGlobal Free Trade Has Done More Harm Than GoodZea SantosNo ratings yet

- MSTM 5030 C - Group Assignment - Anjali and SumeetDocument11 pagesMSTM 5030 C - Group Assignment - Anjali and SumeetANJALI ARORANo ratings yet

- Lani Nuraini MakmurDocument39 pagesLani Nuraini MakmurIlham PandjuNo ratings yet

- Pfaff Performance 2054 Service ManualDocument110 pagesPfaff Performance 2054 Service ManualiliiexpugnansNo ratings yet

- Synchro-Cog HT: Synchronous Drive BeltDocument32 pagesSynchro-Cog HT: Synchronous Drive BeltDavid BaylissNo ratings yet

- Form MGT 7 01032021 SignedDocument14 pagesForm MGT 7 01032021 SignedMohak GuptaNo ratings yet

- This Study Resource WasDocument3 pagesThis Study Resource WasCHAU Nguyen Ngoc BaoNo ratings yet

- Chapter 3 In-Class QuestionsDocument8 pagesChapter 3 In-Class Questionsbharath_No ratings yet

- Cañon EodDocument58 pagesCañon EodJonatan AlmeidaNo ratings yet

- Question 6 Write Short Notes On A) Economic Environment B) Public Accountability C) Industrial Policy of 1956Document5 pagesQuestion 6 Write Short Notes On A) Economic Environment B) Public Accountability C) Industrial Policy of 1956HozefadahodNo ratings yet

- B-BBMD001 - Gantt Chart - Business Plan 2023Document5 pagesB-BBMD001 - Gantt Chart - Business Plan 2023Anthony PrincipioNo ratings yet

- Assignment 2 BNP 30402 AnswerDocument7 pagesAssignment 2 BNP 30402 AnswerbndrprdnaNo ratings yet

- Plate No: EM8635: Official ReceiptDocument1 pagePlate No: EM8635: Official ReceiptRomie Opeda67% (3)

- Thesis Topics International EconomicsDocument8 pagesThesis Topics International Economicsnikkismithmilwaukee100% (2)