You might also like

- Wharton Consulting Club Case Book 2019Document201 pagesWharton Consulting Club Case Book 2019guilhermetrinco62% (13)

- NWC Financial ForecastDocument9 pagesNWC Financial ForecastTimNo ratings yet

- Cases in Finance 3rd Edition Demello Solutions ManualDocument11 pagesCases in Finance 3rd Edition Demello Solutions ManualJanice Kahalehoe100% (36)

- Mini Case CH 3 SolutionsDocument14 pagesMini Case CH 3 SolutionsTimeka CarterNo ratings yet

- Case Study - Track SoftwareDocument6 pagesCase Study - Track SoftwareRey-Anne Paynter100% (14)

- Import invoice and bill of lading for wooden furniture shipmentDocument1 pageImport invoice and bill of lading for wooden furniture shipmentrifablackNo ratings yet

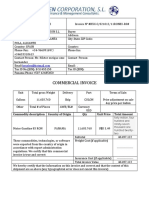

- Commercial Invoice: Commodity Description Country of Origin Qty Unit Price Total AmountDocument2 pagesCommercial Invoice: Commodity Description Country of Origin Qty Unit Price Total AmountOswaldo Montana0% (1)

- Apple 10-K AnalysisDocument8 pagesApple 10-K AnalysisRyanNo ratings yet

- Apple Financial Ratios AnalysisDocument6 pagesApple Financial Ratios AnalysisEdward AwiNo ratings yet

- AssignmentDocument7 pagesAssignmentGrace MwendeNo ratings yet

- Module 1: Analyze Amazon & Walmart FinancialsDocument10 pagesModule 1: Analyze Amazon & Walmart FinancialsDEENo ratings yet

- MINI CASE Ch 9Document7 pagesMINI CASE Ch 9Samara SharinNo ratings yet

- Corporate Finances Problems Solutions Ch.18Document9 pagesCorporate Finances Problems Solutions Ch.18Egzona FidaNo ratings yet

- Operating Margin RatioDocument9 pagesOperating Margin RatiorideralfiNo ratings yet

- Income StatementDocument20 pagesIncome StatementkasoziNo ratings yet

- Ratio AnalysisDocument16 pagesRatio AnalysisAbdul RehmanNo ratings yet

- Nestle AnanlysisDocument18 pagesNestle AnanlysisSLUG GAMINGNo ratings yet

- Comparative Study of Financial Statement Ratios Between Dell and EpsonDocument7 pagesComparative Study of Financial Statement Ratios Between Dell and EpsonMacharia NgunjiriNo ratings yet

- 3-Ifn3 031210073 Assignment1Document6 pages3-Ifn3 031210073 Assignment1May MsNo ratings yet

- SABIC (Detailed Analysis)Document17 pagesSABIC (Detailed Analysis)Mirza Zain Ul AbideenNo ratings yet

- Financial Accounting And The Financial StatementsDocument10 pagesFinancial Accounting And The Financial StatementsRajiv RankawatNo ratings yet

- Gross Profit Margin and Net Profit Margin Analysis of VCFDocument7 pagesGross Profit Margin and Net Profit Margin Analysis of VCFthai hoangNo ratings yet

- Project 2Document11 pagesProject 2api-545675901No ratings yet

- Econ 3073 Assignment - 1 and 2 CompleteDocument12 pagesEcon 3073 Assignment - 1 and 2 CompleteMudassar Gul Bin AshrafNo ratings yet

- Apple's Foreign Exchange Risk ManagementDocument17 pagesApple's Foreign Exchange Risk Managementamirul asyrafNo ratings yet

- 03 CH03Document41 pages03 CH03Walid Mohamed AnwarNo ratings yet

- Chapter 4 Sample BankDocument18 pagesChapter 4 Sample BankWillyNoBrainsNo ratings yet

- Apple Financial Analysis V2Document9 pagesApple Financial Analysis V2HaniNo ratings yet

- Aetna Financial Analysis Reveals Strategic Investments for Future GrowthDocument11 pagesAetna Financial Analysis Reveals Strategic Investments for Future GrowthKimberlyHerringNo ratings yet

- Financial Accounting - Starbucks CaseDocument14 pagesFinancial Accounting - Starbucks CaseHạnh TrầnNo ratings yet

- Problem BankDocument10 pagesProblem BankSimona NistorNo ratings yet

- Du PontDocument8 pagesDu PontTên Hay ThếNo ratings yet

- Accounting in Organization and SocietyDocument13 pagesAccounting in Organization and SocietyHải BìnhNo ratings yet

- A. Ratios Caculation. 1. Current Ratio For Fiscal Years 2017 and 2018Document6 pagesA. Ratios Caculation. 1. Current Ratio For Fiscal Years 2017 and 2018Phạm Thu HuyềnNo ratings yet

- Collier 1ce Solutions Ch13Document14 pagesCollier 1ce Solutions Ch13Oluwasola OluwafemiNo ratings yet

- Annual Report Project For Apple Inc.Document12 pagesAnnual Report Project For Apple Inc.daynachristianmarie11No ratings yet

- Bob's dilemma: debt vs equity financing for expansionDocument11 pagesBob's dilemma: debt vs equity financing for expansionfarisa.oeNo ratings yet

- Ma2 Examiner's Report S21-A22Document7 pagesMa2 Examiner's Report S21-A22tashiNo ratings yet

- Financial Forecasting and Planning Tut - 1Document2 pagesFinancial Forecasting and Planning Tut - 1Sohad ElnagarNo ratings yet

- ACC 404 RatiosDocument11 pagesACC 404 RatiosMahmud TuhinNo ratings yet

- Financial Statement AnalysisDocument59 pagesFinancial Statement AnalysisJeymar YraNo ratings yet

- Plagiarism Declaration Form (T-DF)Document24 pagesPlagiarism Declaration Form (T-DF)Nur HidayahNo ratings yet

- Bob's Dilemma: Should Symonds Electronic Raise Capital Through Debt or EquityDocument7 pagesBob's Dilemma: Should Symonds Electronic Raise Capital Through Debt or EquityRaffin AdarshNo ratings yet

- Maria FinalDocument8 pagesMaria FinalrideralfiNo ratings yet

- Apple Inc.-Final Case StudyDocument9 pagesApple Inc.-Final Case StudyPan TurkNo ratings yet

- Revison Lecture - Q1 Q2Document28 pagesRevison Lecture - Q1 Q2pes60804No ratings yet

- Lessons From Apple For African EntrepreneursDocument5 pagesLessons From Apple For African EntrepreneursAdebayo AlongeNo ratings yet

- Inventories With Lower Cost, Without Sacrificing Its QualityDocument4 pagesInventories With Lower Cost, Without Sacrificing Its QualityMark Lyndon YmataNo ratings yet

- Ratio Analysis and Valuation of Apple Inc. and Olympic IndustriesDocument21 pagesRatio Analysis and Valuation of Apple Inc. and Olympic IndustriesAnikaNo ratings yet

- Mid-Term Test Preparation QuestionsDocument5 pagesMid-Term Test Preparation QuestionsDurjoy SharmaNo ratings yet

- Snisbury's Ratio AnalysisDocument8 pagesSnisbury's Ratio Analysis99 Nazmul AlamNo ratings yet

- FAUE InterpretationDocument4 pagesFAUE InterpretationAnkit PatidarNo ratings yet

- Financial Aspect of Apple Inc. by Dr. Zayar NaingDocument8 pagesFinancial Aspect of Apple Inc. by Dr. Zayar Naingzayarnmb_66334156No ratings yet

- Tutorial 7 - (Solution) Analysis of Financial StatementsDocument4 pagesTutorial 7 - (Solution) Analysis of Financial StatementsSamer LaabidiNo ratings yet

- BV BrouillonDocument3 pagesBV BrouillonemocittolamNo ratings yet

- Tutorial 3 AnswersDocument5 pagesTutorial 3 Answers杰克 l孙No ratings yet

- BNL Stores' Declining ProfitabilityDocument16 pagesBNL Stores' Declining ProfitabilityAMBWANI NAREN MAHESHNo ratings yet

- Acct 602-Discussion 4Document2 pagesAcct 602-Discussion 4Michael LipphardtNo ratings yet

- Finance AssignmentDocument3 pagesFinance AssignmentMelanie SamarooNo ratings yet

- Accm506 Ca1Document10 pagesAccm506 Ca1Shay ShayNo ratings yet

- Part C: Figure 1:astrazeneca Financial Position 2021Document11 pagesPart C: Figure 1:astrazeneca Financial Position 2021Unzillah AzharNo ratings yet

- Singapore's Development Shaped by Science and TechnologyDocument7 pagesSingapore's Development Shaped by Science and TechnologyAlexandra GarciaNo ratings yet

- PPBL Savings Account Statement for 28 March 2022 to 27 June 2022Document43 pagesPPBL Savings Account Statement for 28 March 2022 to 27 June 2022Maha RajaNo ratings yet

- Return and Risk From All Investment DecisionsDocument4 pagesReturn and Risk From All Investment DecisionsAchmad ArdanuNo ratings yet

- Chapter 1. L1.4 Nature of Securities and Risks InvolvedDocument3 pagesChapter 1. L1.4 Nature of Securities and Risks InvolvedvibhuNo ratings yet

- Akuntansi Is Easy: Nama - Nama Perkiraan (Akun) Dan Istilah Dalam Bahasa InggrisDocument9 pagesAkuntansi Is Easy: Nama - Nama Perkiraan (Akun) Dan Istilah Dalam Bahasa InggrisDwan ZNo ratings yet

- Import and Export DocumentsDocument28 pagesImport and Export DocumentsVenkata BalajiNo ratings yet

- GlobalizationDocument19 pagesGlobalizationNguyen Ngoc Yen VyNo ratings yet

- Intermediate Accounting 19th Edition Stice Test Bank 1Document40 pagesIntermediate Accounting 19th Edition Stice Test Bank 1pauline100% (45)

- FINMAR - Time Value of MoneyDocument2 pagesFINMAR - Time Value of MoneySean Patrick C. WONGNo ratings yet

- C U S T O M S: Boc Single Administrative DocumentDocument2 pagesC U S T O M S: Boc Single Administrative DocumentNaj MusorNo ratings yet

- ENGG ECON Part1Document32 pagesENGG ECON Part1ShaneP.HermosoNo ratings yet

- Block 6 MEC 007 Unit 17Document20 pagesBlock 6 MEC 007 Unit 17Adarsh Kumar GuptaNo ratings yet

- Role of Rbi in Controlling InflationDocument13 pagesRole of Rbi in Controlling InflationMukesh Kumar67% (3)

- Basics of Foreign ExchangeDocument162 pagesBasics of Foreign ExchangeClassicaverNo ratings yet

- Module 8 - Inventories Part IIDocument14 pagesModule 8 - Inventories Part IIMark Christian BrlNo ratings yet

- Chapter 2 Financial SystemDocument7 pagesChapter 2 Financial SystemsoleilNo ratings yet

- Muhammad Kashif Raheem 5212 Cost Accounting Sir Naveed AlamDocument8 pagesMuhammad Kashif Raheem 5212 Cost Accounting Sir Naveed AlamKashif RaheemNo ratings yet

- Wutong Gift Card 3Document1 pageWutong Gift Card 3Ronny VanoverNo ratings yet

- Acounting System SectionDocument98 pagesAcounting System SectionKaashifNo ratings yet

- CERTIFIED STATEMENT OF INCOMEDocument17 pagesCERTIFIED STATEMENT OF INCOMEArman BentainNo ratings yet

- DissertationDocument68 pagesDissertationMohit AgarwalNo ratings yet

- 2018 Tutorials - Chapter 12 - Session 3 - MoodleDocument27 pages2018 Tutorials - Chapter 12 - Session 3 - Moodlewandile majoziNo ratings yet

- AMTOI BrochureDocument8 pagesAMTOI Brochuremanishk_47No ratings yet

- 1.1 British Empire in IndiaDocument37 pages1.1 British Empire in IndialavanyaNo ratings yet

- Mba - 302Document15 pagesMba - 302Akash skillsNo ratings yet

- MBFM4002 Global Financial ManagementDocument3 pagesMBFM4002 Global Financial ManagementShakthi RaghaviNo ratings yet

- Master Budget - ProblemsDocument3 pagesMaster Budget - ProblemsVenus PalmencoNo ratings yet