You might also like

- CH 2 ExercisesDocument4 pagesCH 2 ExercisesAnonymous Jf9PYY2E80% (1)

- Name:John Michael Najarro Course&Year: BSBA 1 Date: 10/7/20: Colegio de Santa Rita de San Carlos, IncDocument3 pagesName:John Michael Najarro Course&Year: BSBA 1 Date: 10/7/20: Colegio de Santa Rita de San Carlos, IncRod Najarro100% (1)

- Practice Problems On Special JournalsDocument24 pagesPractice Problems On Special JournalsJenny Boo67% (3)

- Ict 2 Finals Exam Besa Bsa2aDocument4 pagesIct 2 Finals Exam Besa Bsa2aJoyce Ann Cortez100% (1)

- Diploma in Financial StrategyDocument16 pagesDiploma in Financial StrategyMphoNo ratings yet

- Task Performance I. Horizontal AnalysisDocument3 pagesTask Performance I. Horizontal AnalysisarisuNo ratings yet

- Statement 2023 3Document1 pageStatement 2023 3Pakinan ZeidNo ratings yet

- Environgrad Corporation: A Case StudyDocument25 pagesEnvirongrad Corporation: A Case StudyAbhi Krishna ShresthaNo ratings yet

- Assignment 2Document13 pagesAssignment 2Lyca Mae Cubangbang100% (2)

- Ems - Grade - 7 - Financial - Literacy - 2022 - Term 2 & 4 - UpdatedDocument24 pagesEms - Grade - 7 - Financial - Literacy - 2022 - Term 2 & 4 - UpdatedMIKEMPHALO100% (1)

- BAAB1014 Quiz 1 (B) AnswersDocument4 pagesBAAB1014 Quiz 1 (B) AnswersHareen JuniorNo ratings yet

- Worksheet 1 NMIMS SolutionsDocument7 pagesWorksheet 1 NMIMS SolutionsvipulNo ratings yet

- Accounting ConceptDocument35 pagesAccounting ConceptNik AimanNo ratings yet

- AccountingDocument13 pagesAccountingBaktash AhmadiNo ratings yet

- Exercises and Problem Debit 2-A May 2 CashDocument16 pagesExercises and Problem Debit 2-A May 2 CashRenz MoralesNo ratings yet

- 3 - Book of Prime Entry - CashbookDocument37 pages3 - Book of Prime Entry - Cashbooknurzbiet8587No ratings yet

- Accruals and Prepayments: AlreadyDocument4 pagesAccruals and Prepayments: AlreadyLOW YAN QINNo ratings yet

- Introduction To Financial Accounting and Reporting (Acc106)Document8 pagesIntroduction To Financial Accounting and Reporting (Acc106)ammarNo ratings yet

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- Single EntryDocument5 pagesSingle Entrysmit9993No ratings yet

- Group Assignment Acc 1Document10 pagesGroup Assignment Acc 1jul janzNo ratings yet

- 高一簿记模拟试卷Document6 pages高一簿记模拟试卷Carpenters ForeverNo ratings yet

- EXERCISE 8 With AnswersDocument10 pagesEXERCISE 8 With AnswershanaNo ratings yet

- Accounting Tutorial 2 Part 2Document18 pagesAccounting Tutorial 2 Part 2Sim Pei Ying100% (1)

- Chapter 5 - Three Column Cash BookDocument32 pagesChapter 5 - Three Column Cash BookclintonchimeriNo ratings yet

- Tutorial Chapter 4 (TRIAL BALANCE)Document2 pagesTutorial Chapter 4 (TRIAL BALANCE)azra balqisNo ratings yet

- Poa T - 1Document3 pagesPoa T - 1SHEVENA A/P VIJIANNo ratings yet

- 179200Document13 pages179200Ankita GuptaNo ratings yet

- Effects and Equation-Individual AssignmentDocument8 pagesEffects and Equation-Individual AssignmentAbduzzahir Bin Mohd SaidNo ratings yet

- Financial StatementsDocument13 pagesFinancial StatementsAlbert Jun Piquero AlegadoNo ratings yet

- Home Assignment - Financial Accounting PGPM 2019-20Document3 pagesHome Assignment - Financial Accounting PGPM 2019-20SidharthNo ratings yet

- Financial Accounting Group ProjectDocument15 pagesFinancial Accounting Group ProjectWan RauhahNo ratings yet

- Double Entry and Trial Balance ExtractionDocument15 pagesDouble Entry and Trial Balance ExtractionDavidNo ratings yet

- CH 2Document42 pagesCH 2monudeep aggarwalNo ratings yet

- Session 6 - Comprehensive Financial Statements - (IS BS)Document9 pagesSession 6 - Comprehensive Financial Statements - (IS BS)Darrel SamueldNo ratings yet

- A Presentation On Cash Book, Pass Book & Bank Reconciliation Statement - Sudarshan Kr. PatelDocument26 pagesA Presentation On Cash Book, Pass Book & Bank Reconciliation Statement - Sudarshan Kr. Patelsh0101100% (1)

- Books of Prime Entry and LedgersDocument10 pagesBooks of Prime Entry and LedgersLOW YAN QINNo ratings yet

- Partnerships-1Document20 pagesPartnerships-1samuelNo ratings yet

- Module 3 Chapter 7Document8 pagesModule 3 Chapter 7Angelie Bocala CatalanNo ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- MBA I Semester Supplementary Examinations December/January 2018/19Document2 pagesMBA I Semester Supplementary Examinations December/January 2018/19Chandra SekharNo ratings yet

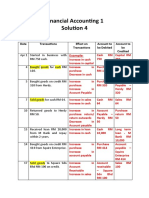

- Financial Accounting 1 - Solution 4Document3 pagesFinancial Accounting 1 - Solution 4mardhiahNo ratings yet

- Mid-Term Revision 2023.finalDocument8 pagesMid-Term Revision 2023.finalRabie HarounNo ratings yet

- Jayalakshmi Institute of Technology Accounting For Management Unit - Ii QuestionsDocument2 pagesJayalakshmi Institute of Technology Accounting For Management Unit - Ii QuestionsJayalakshmi Institute of TechnologyNo ratings yet

- Effects of Transactions and Double Entry Question 2 Page 65Document2 pagesEffects of Transactions and Double Entry Question 2 Page 65azra balqisNo ratings yet

- Branch Account2Document20 pagesBranch Account2choudharidip8No ratings yet

- Tugas Kasus-2Document13 pagesTugas Kasus-2Adri MuliaNo ratings yet

- Ex. 8.11 - B2 - A. Fuentes - Palacios - Lobangco - RonaCoDocument13 pagesEx. 8.11 - B2 - A. Fuentes - Palacios - Lobangco - RonaCoShwn Mchl SbynNo ratings yet

- Branch AccountingDocument14 pagesBranch AccountingKartikeya SaraswatNo ratings yet

- Topic 3 TutorialDocument10 pagesTopic 3 TutorialMimi ArniNo ratings yet

- Good Shepherd International School, Ooty: Winter Holiday HomeworkDocument12 pagesGood Shepherd International School, Ooty: Winter Holiday Homework6969 RithvikNo ratings yet

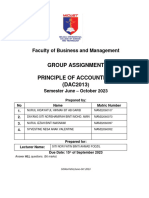

- Principle of Accounting (DAC2013)Document8 pagesPrinciple of Accounting (DAC2013)Hidayatul HikmahNo ratings yet

- Topic 6.Document5 pagesTopic 6.Ernie AbeNo ratings yet

- Journal EntriesDocument4 pagesJournal EntriesMeriam MacadaegNo ratings yet

- Joel Amos Periodic InventoryDocument7 pagesJoel Amos Periodic InventoryJasmine P. Manlungat - EMERALDNo ratings yet

- Week 3 Tutorial SolutionsDocument31 pagesWeek 3 Tutorial SolutionsalexandraNo ratings yet

- 5.Cash-Bank Book (Three Column)Document6 pages5.Cash-Bank Book (Three Column)jangirvihan2No ratings yet

- Debit and CreditDocument64 pagesDebit and CreditAngelita Capagalan100% (1)

- Amalgamation - Example 1 To 4Document4 pagesAmalgamation - Example 1 To 4Zhong HanNo ratings yet

- MB0025 Financial and Management AccountingDocument7 pagesMB0025 Financial and Management Accountingvarsha100% (1)

- Question Bank (Accounting Problems)Document11 pagesQuestion Bank (Accounting Problems)Abhishek MohantyNo ratings yet

- AC PaperDocument2 pagesAC Paperpiyush kumarNo ratings yet

- Notes - Cashbook02 2Document4 pagesNotes - Cashbook02 2MAK- 47No ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- Sample Project of Mini Oil MillDocument6 pagesSample Project of Mini Oil MillLajpat Lala0% (3)

- RechargeDocument1 pageRechargeHemanth NaikNo ratings yet

- 073 - C5 Equity ValuationDocument77 pages073 - C5 Equity ValuationRazvan Dan0% (1)

- China BankDocument1 pageChina BankPSC.CLAIMS1No ratings yet

- Practice Set 1 ABC-3Document3 pagesPractice Set 1 ABC-3reiNo ratings yet

- Audit Top 250 Important Question @group1 - Notes PDFDocument29 pagesAudit Top 250 Important Question @group1 - Notes PDFJinal SanghviNo ratings yet

- Air Canada, WestJet Push Back Return of 737 MaxDocument1 pageAir Canada, WestJet Push Back Return of 737 MaxGenieNo ratings yet

- Early College Planning For ParentsDocument26 pagesEarly College Planning For Parentsjaypee pengNo ratings yet

- Wholesale Juice Business PlanDocument25 pagesWholesale Juice Business PlanKiza Kura CyberNo ratings yet

- Books of Original Entry (An Introduction)Document5 pagesBooks of Original Entry (An Introduction)Joshua BrownNo ratings yet

- Non-Resident Withholding Tax (NRWT) Rates and Country CodesDocument2 pagesNon-Resident Withholding Tax (NRWT) Rates and Country CodessamsujNo ratings yet

- Cash Flow Statement (Direct Method) FormulasDocument20 pagesCash Flow Statement (Direct Method) FormulasSilha JamilNo ratings yet

- Solutions To Activity 1 A, 1B, 1C and 1DDocument2 pagesSolutions To Activity 1 A, 1B, 1C and 1DPrincess Mae ArabitNo ratings yet

- Account StatementDocument12 pagesAccount StatementHunzlah AhmadNo ratings yet

- Income Approach: VR - Poovannan.A IIV-RVF April-2021Document96 pagesIncome Approach: VR - Poovannan.A IIV-RVF April-2021Muruga DasNo ratings yet

- Pay Sys ProceedingsDocument112 pagesPay Sys ProceedingsFlaviub23No ratings yet

- Why Study Money, Banking, and Financial Markets?Document29 pagesWhy Study Money, Banking, and Financial Markets?Lazaros KarapouNo ratings yet

- Asx24 Contract SpecificationsDocument42 pagesAsx24 Contract SpecificationsJohn SalazarNo ratings yet

- Dividend Hunter - Apr 2015 PDFDocument7 pagesDividend Hunter - Apr 2015 PDFRandora LkNo ratings yet

- Everything You Need To Know About Buying A New HomeDocument15 pagesEverything You Need To Know About Buying A New HomeAna BandeiraNo ratings yet

- Uncertainity and Consumer BehaviourDocument17 pagesUncertainity and Consumer BehaviourAroutselvam ChanemougameNo ratings yet

- Eco 531 - Chapter 1Document8 pagesEco 531 - Chapter 1Nurul Aina IzzatiNo ratings yet

- A Study of Mutual Fund Investment Awareness of People of Kalyan Dombivli Municipal Corporation RegionDocument8 pagesA Study of Mutual Fund Investment Awareness of People of Kalyan Dombivli Municipal Corporation RegionVaibhav GawandeNo ratings yet

- A Study On Financial Performance and Governance in Indian Aviation SectorDocument6 pagesA Study On Financial Performance and Governance in Indian Aviation SectorFir BhiNo ratings yet

- Indian Economy Previous Question Paper ?Document9 pagesIndian Economy Previous Question Paper ?Atharva SherkarNo ratings yet