You might also like

- Loan SyndicationDocument12 pagesLoan SyndicationArpit Jain100% (1)

- Real Estate Principles A Value Approach 5Th Edition Ling Solutions Manual Full Chapter PDFDocument19 pagesReal Estate Principles A Value Approach 5Th Edition Ling Solutions Manual Full Chapter PDFoctogamyveerbxtl100% (8)

- Banking Unit 4Document12 pagesBanking Unit 4PaatrickNo ratings yet

- Real Estate Principles A Value Approach 5th Edition Ling Solutions ManualDocument23 pagesReal Estate Principles A Value Approach 5th Edition Ling Solutions Manualleightonayarza100% (18)

- Lu 6Document40 pagesLu 6Phetho MachiliNo ratings yet

- Loan Syndication: 1. Pre-Signing StageDocument5 pagesLoan Syndication: 1. Pre-Signing StageFarhan Ashraf SaadNo ratings yet

- Assignment IIDocument47 pagesAssignment IIapi-19984025No ratings yet

- Group 3Document9 pagesGroup 3eranyigiNo ratings yet

- Loan SyndicationDocument2 pagesLoan SyndicationChandan Kumar ShawNo ratings yet

- Corporate BankingDocument6 pagesCorporate BankingDeven RanaNo ratings yet

- TB Bank loans-đã chuyển sang wordDocument8 pagesTB Bank loans-đã chuyển sang wordVi TrươngNo ratings yet

- Law and Practice of International FinanceDocument9 pagesLaw and Practice of International FinanceCarlos Belando PastorNo ratings yet

- This Study Resource Was: Page - 1Document9 pagesThis Study Resource Was: Page - 1NishiNo ratings yet

- Understanding MortgagorsDocument2 pagesUnderstanding MortgagorsDiane ヂエンNo ratings yet

- This Study Resource Was: Page - 1Document9 pagesThis Study Resource Was: Page - 1NishiNo ratings yet

- Indonesia Loans & Secured Financing - Getting The Deal Through - GTDTDocument12 pagesIndonesia Loans & Secured Financing - Getting The Deal Through - GTDTDewa Gede Praharyan JayadiputraNo ratings yet

- This Study Resource Was: Page - 1Document9 pagesThis Study Resource Was: Page - 1NishiNo ratings yet

- BNKINGDocument6 pagesBNKINGjyotiprashad041No ratings yet

- The Risks and Rewards of Multiple Lender FinancingsDocument5 pagesThe Risks and Rewards of Multiple Lender Financingsjude loh wai sengNo ratings yet

- CH 8 Sources of Business Finance Class 11 BSTDocument19 pagesCH 8 Sources of Business Finance Class 11 BSTRaman SachdevaNo ratings yet

- 3.2. Law Relating To Commercial Banks-2Document51 pages3.2. Law Relating To Commercial Banks-2Madan ShresthaNo ratings yet

- Edurev - In-Social Studies SST Class 10Document9 pagesEdurev - In-Social Studies SST Class 10asfiyarahmath2008No ratings yet

- Lecture 4 - Syndicated - LoansDocument12 pagesLecture 4 - Syndicated - LoansYvonneNo ratings yet

- Important Quess) Tions ch-3Document9 pagesImportant Quess) Tions ch-3AnnaNo ratings yet

- Tutorial For Financial Markets & Institutions An Economic Analysis of Financial StructureDocument3 pagesTutorial For Financial Markets & Institutions An Economic Analysis of Financial StructureHi I'm ConyNo ratings yet

- A Domestic Framework For Group InsolvencyDocument23 pagesA Domestic Framework For Group InsolvencyPradhuymn MishraNo ratings yet

- Company LawDocument6 pagesCompany LawshreyanshiNo ratings yet

- Loan SyndicationDocument57 pagesLoan SyndicationSandya Gundeti100% (1)

- Introduction of Credit Default Swaps For Corporate Bonds in IndiaDocument11 pagesIntroduction of Credit Default Swaps For Corporate Bonds in Indiagagan3211No ratings yet

- Loan SyndicationDocument4 pagesLoan Syndicationsantu15038847420No ratings yet

- Lecture 4 - Syndicated LoansDocument13 pagesLecture 4 - Syndicated LoansEmmanuel MwapeNo ratings yet

- Chapter 7. Sources of FinanceDocument20 pagesChapter 7. Sources of FinanceHastings KapalaNo ratings yet

- Corporate Finance Foundations Global Edition 15th Edition Block Solutions ManualDocument9 pagesCorporate Finance Foundations Global Edition 15th Edition Block Solutions Manualderrickjacksondimowfpcjz100% (27)

- How Bankruptcy Laws Affect Loan Supply and Recovery: Lecturer, School of Business and Economics North South UniversityDocument14 pagesHow Bankruptcy Laws Affect Loan Supply and Recovery: Lecturer, School of Business and Economics North South UniversitySalauddin Imran MumitNo ratings yet

- This Study Resource Was: Page - 1Document9 pagesThis Study Resource Was: Page - 1NishiNo ratings yet

- Loans and AdvanceDocument8 pagesLoans and AdvanceDjay SlyNo ratings yet

- Bankers Lien 3Document9 pagesBankers Lien 3NishiNo ratings yet

- 3.foreign Loan SyndicationDocument19 pages3.foreign Loan SyndicationAPOLLO BISWASNo ratings yet

- Financial Markets (Chapter 10)Document3 pagesFinancial Markets (Chapter 10)Kyla Dayawon100% (1)

- Banking Law FinalDocument20 pagesBanking Law FinalRoy Vincent ManiteNo ratings yet

- The Nigeria Deposit Insurance Corporation: The Journey So Far BYDocument26 pagesThe Nigeria Deposit Insurance Corporation: The Journey So Far BYrapidshonuffNo ratings yet

- Types of Lending and Facilities PDFDocument18 pagesTypes of Lending and Facilities PDFKnowledge GuruNo ratings yet

- Mortgage Markets and Derivatives 2Document35 pagesMortgage Markets and Derivatives 2caballerod0343No ratings yet

- This Study Resource Was: Page - 1Document9 pagesThis Study Resource Was: Page - 1NishiNo ratings yet

- Loan SyndicationDocument35 pagesLoan Syndicationdivyapillai0201_No ratings yet

- Loan Agreement As A Valid Form of Agreement in India.: Name: Trishit Kumar SatpatiDocument16 pagesLoan Agreement As A Valid Form of Agreement in India.: Name: Trishit Kumar SatpatiSAURABH SINGHNo ratings yet

- Class 5 Notes 27062022Document3 pagesClass 5 Notes 27062022Munyangoga BonaventureNo ratings yet

- Bank Management FIN 303: Overview of Loan SyndicationDocument4 pagesBank Management FIN 303: Overview of Loan SyndicationTashahudul IslamNo ratings yet

- FM302: Tutorial Questions Topic: Secured Transactions in The Pacic Region (Week 11)Document5 pagesFM302: Tutorial Questions Topic: Secured Transactions in The Pacic Region (Week 11)Hitesh MaharajNo ratings yet

- Syndicate LaonDocument6 pagesSyndicate Laonarpitm61No ratings yet

- Week 12: Chapter 17-Banking and Management of Financial InstitutionsDocument4 pagesWeek 12: Chapter 17-Banking and Management of Financial InstitutionsJay Ann DomeNo ratings yet

- Chapter01 TestbankDocument40 pagesChapter01 TestbankDuy ThứcNo ratings yet

- 14 Financing Foreign Investment: Chapter ObjectivesDocument18 pages14 Financing Foreign Investment: Chapter ObjectivesJayant312002 ChhabraNo ratings yet

- Trufis: Saujanya P. (Director)Document4 pagesTrufis: Saujanya P. (Director)Sudhanshu N RanjanNo ratings yet

- Research 3Document32 pagesResearch 3Andile MlotsaNo ratings yet

- Some SPECCOM BAR QUESTIONS AND ANSWERSDocument29 pagesSome SPECCOM BAR QUESTIONS AND ANSWERSMark TeaNo ratings yet

- Hard Money LendingDocument16 pagesHard Money Lendingnikhilraheja100% (1)

- Approval LetterDocument2 pagesApproval Lettersonebhadrahyundai salesNo ratings yet

- Data Envelopment Analysis: Joe Zhu EditorDocument594 pagesData Envelopment Analysis: Joe Zhu EditorBrahyam Emmanuel Cruz RinconNo ratings yet

- Dealing Room StrategyDocument13 pagesDealing Room StrategyFatima MacNo ratings yet

- Mo Ghara GuidelinesDocument28 pagesMo Ghara GuidelinesRajnikant BilungNo ratings yet

- Internal Control Guide: The AES CorporationDocument70 pagesInternal Control Guide: The AES CorporationSaleem RahmanNo ratings yet

- Screenshot 2024-03-12 at 5.28.33 PMDocument8 pagesScreenshot 2024-03-12 at 5.28.33 PMchiraggajjar242No ratings yet

- TCH302-Topic 3&4-Time Value of Money & Applications PDFDocument38 pagesTCH302-Topic 3&4-Time Value of Money & Applications PDFHà ThưNo ratings yet

- CH 06Document62 pagesCH 06nguyenbuithao22No ratings yet

- FINAL REPORT WV Albania Buiding Futures PotentialDocument30 pagesFINAL REPORT WV Albania Buiding Futures PotentialVasilijeNo ratings yet

- Balance Sheet of Tata Power Company: - in Rs. Cr.Document3 pagesBalance Sheet of Tata Power Company: - in Rs. Cr.ashishrajmakkarNo ratings yet

- Chithra Baskar: Account StatementDocument5 pagesChithra Baskar: Account StatementSarath KumarNo ratings yet

- Newsletter 7Document2 pagesNewsletter 7Gustavo BenaderetNo ratings yet

- Assignment AnswerDocument2 pagesAssignment AnswerMims ChiiiNo ratings yet

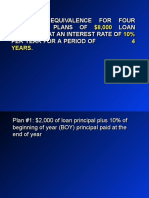

- Economic Equivalence For Four Repayment Plans of $8,000 Loan Borrowed at An Interest Rate of 10% Per Year For A Period of 4 YearsDocument21 pagesEconomic Equivalence For Four Repayment Plans of $8,000 Loan Borrowed at An Interest Rate of 10% Per Year For A Period of 4 YearsMuhammad atif latifNo ratings yet

- COOPDocument8 pagesCOOPJohn Kenneth BoholNo ratings yet

- General Mathematics: Simple InterestsDocument7 pagesGeneral Mathematics: Simple InterestsClaire BalatucanNo ratings yet

- DBA-724-Enterprise-Analysis-Final PaperDocument20 pagesDBA-724-Enterprise-Analysis-Final PaperEarl Louie MasacayanNo ratings yet

- Module 2 AnnuityDocument38 pagesModule 2 AnnuityOwel CabugawanNo ratings yet

- 11 ACC Journal'Document3 pages11 ACC Journal'Naman TiwariNo ratings yet

- Avon Stampings Private Limited: Plot No-18/21/2, Revenue Estate, Village Nathupur, Tehsil Rai, Sonipat, Haryana, 131029Document1 pageAvon Stampings Private Limited: Plot No-18/21/2, Revenue Estate, Village Nathupur, Tehsil Rai, Sonipat, Haryana, 131029vishal_srivastava_48No ratings yet

- Palma, Ian Jeric MagtalasDocument2 pagesPalma, Ian Jeric MagtalasIan PalmaNo ratings yet

- MCQ On MortgagesDocument3 pagesMCQ On MortgagesShyamNo ratings yet

- CALAMBA NegoSale Batch 47105 111422Document16 pagesCALAMBA NegoSale Batch 47105 111422Michael Chavez AlvarezNo ratings yet

- Max Loans Form 1Document2 pagesMax Loans Form 1cre8tiv1No ratings yet

- Mount Moreland Hospital: Perform Financial CalculationsDocument9 pagesMount Moreland Hospital: Perform Financial CalculationsJacob Sheridan0% (1)

- VIDA Living - HandbookDocument12 pagesVIDA Living - HandbookImranNo ratings yet

- 1 1backgroundDocument51 pages1 1backgroundAlpha BetaNo ratings yet

- 4th AssignmentDocument18 pages4th AssignmentLow El LaNo ratings yet

- Money and Credit: Economics Class-10Document7 pagesMoney and Credit: Economics Class-10Ankita MondalNo ratings yet

- Perpetual Bank: ReceivablesDocument13 pagesPerpetual Bank: ReceivablesYes ChannelNo ratings yet