You might also like

- Bikaji Foods International LTDDocument3 pagesBikaji Foods International LTDdeepaksinghbishtNo ratings yet

- Of The Day (Short Term Delivery Call) - PI Industries LTDDocument3 pagesOf The Day (Short Term Delivery Call) - PI Industries LTDdeepaksinghbishtNo ratings yet

- Pick of The Day (Short Term Delivery Call) - Va Tech Wabag LTD - 08-11-2023Document3 pagesPick of The Day (Short Term Delivery Call) - Va Tech Wabag LTD - 08-11-2023Anurag SanodiaNo ratings yet

- MOIL LTDDocument3 pagesMOIL LTDdeepaksinghbishtNo ratings yet

- Pick of The Day (Short Term Delivery Call) - National Aluminium LTDDocument3 pagesPick of The Day (Short Term Delivery Call) - National Aluminium LTDRAMA MURTHY KNo ratings yet

- Pick of The Day (Short Term Delivery Call) - Cochin Shipyard LTDDocument3 pagesPick of The Day (Short Term Delivery Call) - Cochin Shipyard LTDdeepaksinghbishtNo ratings yet

- Of The Day (Short Term Delivery Call) - Jupiter Wagons LTDDocument3 pagesOf The Day (Short Term Delivery Call) - Jupiter Wagons LTDdeepaksinghbishtNo ratings yet

- Of The Day (Short Term Delivery Call) - Larsen Toubro LTDDocument3 pagesOf The Day (Short Term Delivery Call) - Larsen Toubro LTDdeepaksinghbishtNo ratings yet

- Bernstein India Financials Best in The Decade Metrics Below AverageDocument39 pagesBernstein India Financials Best in The Decade Metrics Below Averageagarwal.deepak6688No ratings yet

- PSO Profit Margins and EPS May Improve in FY24: Securities (PVT.) LTDDocument3 pagesPSO Profit Margins and EPS May Improve in FY24: Securities (PVT.) LTDShoaib A. KaziNo ratings yet

- JS-MCB 29feb24Document3 pagesJS-MCB 29feb24Rizwan IqbalNo ratings yet

- Astra Microwave Products LTD PDFDocument4 pagesAstra Microwave Products LTD PDFAwakash DixitNo ratings yet

- Acnb Stock AnalyisisDocument6 pagesAcnb Stock Analyisisphysicallen1791No ratings yet

- PDF Report-1163880230324Document7 pagesPDF Report-1163880230324ravibv2305No ratings yet

- How We Side-Step Bubbles in Double IncomeDocument11 pagesHow We Side-Step Bubbles in Double IncomePIYUSH GOPALNo ratings yet

- Ujjivan SFB Analyst Day 9jun23Document6 pagesUjjivan SFB Analyst Day 9jun23Sharath JuturNo ratings yet

- Pdfreport 2335062240108Document7 pagesPdfreport 2335062240108vemulakondavenky7No ratings yet

- July Basket 300623Document4 pagesJuly Basket 300623coinage capitalNo ratings yet

- Slic UlipDocument12 pagesSlic UlipARKAJIT DEY-DMNo ratings yet

- File PDFDocument6 pagesFile PDFKenNo ratings yet

- DIVIS LABORATORIES - IIFL - Co Update - 170124 - Elevated Expectations, Underwhelming DeliveryDocument8 pagesDIVIS LABORATORIES - IIFL - Co Update - 170124 - Elevated Expectations, Underwhelming DeliveryP.VenkateshNo ratings yet

- Vivos Thera Report 11.30.23Document6 pagesVivos Thera Report 11.30.23physicallen1791No ratings yet

- Investor Presentation Q3FY22 23Document31 pagesInvestor Presentation Q3FY22 23Dimitrios LiakosNo ratings yet

- QEPLCiZrErJan hDCb6i0xfoI2etvifuiKNPTFhY7QDocument41 pagesQEPLCiZrErJan hDCb6i0xfoI2etvifuiKNPTFhY7Qmanoj8942No ratings yet

- BCG NBFC Sector Update H1FY24Document48 pagesBCG NBFC Sector Update H1FY24ashi.reportsNo ratings yet

- PDF Report-23244420Document2 pagesPDF Report-23244420Rakesh Kumar MundaNo ratings yet

- DSP Banking & PSU Debt FundDocument1 pageDSP Banking & PSU Debt FundTrivikram AsNo ratings yet

- ICRA Analytics Mutual Fund Screener - Q4FY23Document44 pagesICRA Analytics Mutual Fund Screener - Q4FY23Tshering SherpaNo ratings yet

- PDF Report-1161121230323Document7 pagesPDF Report-1161121230323ravibv2305No ratings yet

- PDF Report-1213468230428Document7 pagesPDF Report-1213468230428ravibv2305No ratings yet

- Balkrishna Industries LTD.: Investor PresentationDocument32 pagesBalkrishna Industries LTD.: Investor PresentationHEMANTH KUMAR PNo ratings yet

- Sun Pharma Corporate PresentationDocument59 pagesSun Pharma Corporate PresentationRutvik ShahNo ratings yet

- Fund Focus - Axis Arbitrage Fund - June 2023Document3 pagesFund Focus - Axis Arbitrage Fund - June 2023YasahNo ratings yet

- Average Score: Hibiscus Petroleum (Hibiscs-Ku)Document11 pagesAverage Score: Hibiscus Petroleum (Hibiscs-Ku)archeryNo ratings yet

- Muthoot FinDocument12 pagesMuthoot FinMahesh Karande (KOEL)No ratings yet

- WRTNM 0001Document1 pageWRTNM 0001p srivastavaNo ratings yet

- PDF Report-1163892230324Document7 pagesPDF Report-1163892230324ravibv2305No ratings yet

- Public Asia Ittikal FundDocument1 pagePublic Asia Ittikal FundEileen LauNo ratings yet

- Baxter International Inc.: Price, Consensus & SurpriseDocument1 pageBaxter International Inc.: Price, Consensus & Surprisederek_2010No ratings yet

- Sub: Investor Presentation For The Quarter Ended 30th June, 2022Document24 pagesSub: Investor Presentation For The Quarter Ended 30th June, 2022Khemlal SahuNo ratings yet

- V-Mart - Pick of The Week - Axis Direct - 09072022 - 11-07-2022 - 12Document4 pagesV-Mart - Pick of The Week - Axis Direct - 09072022 - 11-07-2022 - 12Richa CNo ratings yet

- FMR - Oct23Document12 pagesFMR - Oct23maruf_tanmimNo ratings yet

- Fintech Barometer - Report by DLAI and CRIFDocument37 pagesFintech Barometer - Report by DLAI and CRIFsalgiashrenikNo ratings yet

- 2023 Cox Automotive Mid-Year Review PresentationDocument48 pages2023 Cox Automotive Mid-Year Review PresentationpedroemedinaNo ratings yet

- Bioverativ Inc: Price, Consensus & SurpriseDocument1 pageBioverativ Inc: Price, Consensus & Surprisederek_2010No ratings yet

- IIFL - WLDL - 3QFY24 - Result Note - 20240201Document9 pagesIIFL - WLDL - 3QFY24 - Result Note - 20240201Shirish ChikalgeNo ratings yet

- Pre-Sales - Process & Policy HandbookDocument6 pagesPre-Sales - Process & Policy Handbookshivali guptaNo ratings yet

- PDF Report-1522638230824Document6 pagesPDF Report-1522638230824Manu S KashyapNo ratings yet

- Zomato LTD.: Investment RationaleDocument10 pagesZomato LTD.: Investment RationaleSumundra RathNo ratings yet

- NSEIL Presentation Dec22Document14 pagesNSEIL Presentation Dec22Ranjan SharmaNo ratings yet

- MB - Afnan Iqbal - 04 May 2020Document21 pagesMB - Afnan Iqbal - 04 May 2020afnaniqbalNo ratings yet

- Zuari Agro Chemicals LTDDocument9 pagesZuari Agro Chemicals LTDAnnapurnaNo ratings yet

- NSE Website Presentation H1 FY24Document14 pagesNSE Website Presentation H1 FY24coolstiffler08No ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- RolloverDocument9 pagesRollovermanishmandal1976No ratings yet

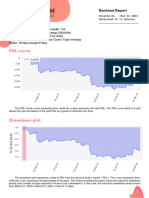

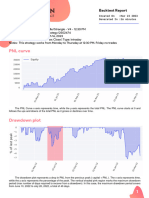

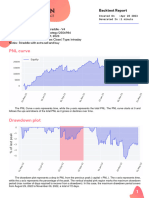

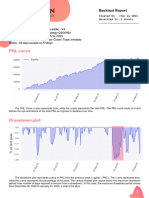

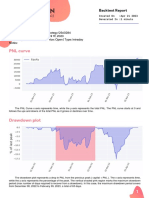

- Backtesting ReportDocument7 pagesBacktesting ReportSatvik JainNo ratings yet

- Macro Investing, New Recommendations & More... : in This ReportDocument12 pagesMacro Investing, New Recommendations & More... : in This ReportPIYUSH GOPALNo ratings yet

- ICRA - Mutual Fund Screener - June 2021Document29 pagesICRA - Mutual Fund Screener - June 2021Dhanush KodiNo ratings yet

- MPC - Impact Analysis - June 8, 2022 FinalDocument7 pagesMPC - Impact Analysis - June 8, 2022 FinalChucha LullNo ratings yet

- SBI Securities Morning Update - 13-12-2022Document6 pagesSBI Securities Morning Update - 13-12-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 02-11-2022Document5 pagesSBI Securities Morning Update - 02-11-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 18-11-2022Document4 pagesSBI Securities Morning Update - 18-11-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 05-12-2022Document6 pagesSBI Securities Morning Update - 05-12-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 18-11-2022Document4 pagesSBI Securities Morning Update - 18-11-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 09-11-2022Document5 pagesSBI Securities Morning Update - 09-11-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 07-11-2022Document5 pagesSBI Securities Morning Update - 07-11-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 15-12-2023Document4 pagesSBI Securities Morning Update - 15-12-2023deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 06-10-2022Document5 pagesSBI Securities Morning Update - 06-10-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 29-09-2022Document4 pagesSBI Securities Morning Update - 29-09-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 20-09-2022Document4 pagesSBI Securities Morning Update - 20-09-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 12-12-2023Document4 pagesSBI Securities Morning Update - 12-12-2023deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 07-10-2022Document5 pagesSBI Securities Morning Update - 07-10-2022deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 7-12-2023Document4 pagesSBI Securities Morning Update - 7-12-2023deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 8-12-2023Document3 pagesSBI Securities Morning Update - 8-12-2023deepaksinghbishtNo ratings yet

- Aaradhya DissertationDocument90 pagesAaradhya DissertationdeepaksinghbishtNo ratings yet

- Of The Day (Short Term Delivery Call) - Jupiter Wagons LTDDocument3 pagesOf The Day (Short Term Delivery Call) - Jupiter Wagons LTDdeepaksinghbishtNo ratings yet

- Of The Day (Short Term Delivery Call) - Jupiter Wagons LTDDocument3 pagesOf The Day (Short Term Delivery Call) - Jupiter Wagons LTDdeepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 18-12-2023Document5 pagesSBI Securities Morning Update - 18-12-2023deepaksinghbishtNo ratings yet

- SBI Securities Morning Update - 15-12-2023Document4 pagesSBI Securities Morning Update - 15-12-2023deepaksinghbishtNo ratings yet

- Premium Receipt: Say Hi To Us On Our Whatsapp NoDocument1 pagePremium Receipt: Say Hi To Us On Our Whatsapp NodeepaksinghbishtNo ratings yet

- VECA Center DetailsDocument3 pagesVECA Center DetailsdeepaksinghbishtNo ratings yet

- Aaradhya DissertationDocument90 pagesAaradhya DissertationdeepaksinghbishtNo ratings yet

- PC INVENTARYDocument4 pagesPC INVENTARYdeepaksinghbishtNo ratings yet

- Temple UkDocument7 pagesTemple UkdeepaksinghbishtNo ratings yet

- Assignment 5Document2 pagesAssignment 5deepaksinghbishtNo ratings yet

- Assignment 5Document2 pagesAssignment 5deepaksinghbishtNo ratings yet

- 3 AssignmentDocument1 page3 AssignmentdeepaksinghbishtNo ratings yet

- Advance Receipts Next Month Settlement Against Sale On GST in Tally PrimeDocument23 pagesAdvance Receipts Next Month Settlement Against Sale On GST in Tally PrimedeepaksinghbishtNo ratings yet

- Final Technical Documentation: Customer: Belize Sugar Industries Limited BelizeDocument9 pagesFinal Technical Documentation: Customer: Belize Sugar Industries Limited BelizeBruno SamosNo ratings yet

- JAR66Document100 pagesJAR66Nae GabrielNo ratings yet

- Test Bank For Global 4 4th Edition Mike PengDocument9 pagesTest Bank For Global 4 4th Edition Mike PengPierre Wetzel100% (32)

- Document 2 - Wet LeasesDocument14 pagesDocument 2 - Wet LeasesDimakatsoNo ratings yet

- Viking Solid Cone Spray NozzleDocument13 pagesViking Solid Cone Spray NozzlebalaNo ratings yet

- Chapter 1 Basic-Concepts-Of-EconomicsDocument30 pagesChapter 1 Basic-Concepts-Of-EconomicsNAZMULNo ratings yet

- Witherby Connect User ManualDocument14 pagesWitherby Connect User ManualAshish NayyarNo ratings yet

- Unit Iv - Lesson 1Document2 pagesUnit Iv - Lesson 1SHIERA MAE AGUSTINNo ratings yet

- Digi Bill 13513651340.010360825015067633Document7 pagesDigi Bill 13513651340.010360825015067633DAVENDRAN A/L KALIAPPAN MoeNo ratings yet

- Wind Energy JapanDocument10 pagesWind Energy JapanEnergiemediaNo ratings yet

- Slave Rebellions & The Black Radical Tradition: SOC3703 Social Movements, Conflict & Change Week 14Document16 pagesSlave Rebellions & The Black Radical Tradition: SOC3703 Social Movements, Conflict & Change Week 14rozamodeauNo ratings yet

- IGNOU Vs MCI High Court JudgementDocument46 pagesIGNOU Vs MCI High Court Judgementom vermaNo ratings yet

- Social Dimensions OF EducationDocument37 pagesSocial Dimensions OF Educationjorolan.annabelleNo ratings yet

- Working Capital FinancingDocument80 pagesWorking Capital FinancingArjun John100% (1)

- Commandos - Beyond The Call of Duty - Manual - PCDocument43 pagesCommandos - Beyond The Call of Duty - Manual - PCAlessandro AbrahaoNo ratings yet

- Travel Reservation August 18 For FREDI ISWANTODocument2 pagesTravel Reservation August 18 For FREDI ISWANTOKasmi MinukNo ratings yet

- If I Was The President of Uganda by Isaac Christopher LubogoDocument69 pagesIf I Was The President of Uganda by Isaac Christopher LubogolubogoNo ratings yet

- Strategic Management A Competitive Advantage Approach Concepts and Cases 17Th 17Th Edition Fred R David All ChapterDocument67 pagesStrategic Management A Competitive Advantage Approach Concepts and Cases 17Th 17Th Edition Fred R David All Chaptertabitha.turner568100% (3)

- CMSPCOR02T Final Question Paper 2022Document2 pagesCMSPCOR02T Final Question Paper 2022DeepNo ratings yet

- Aaron VanneyDocument48 pagesAaron VanneyIvan KelamNo ratings yet

- Tiktok PresentationDocument17 pagesTiktok Presentationapi-681531475No ratings yet

- Adobe Scan 04 Feb 2024Document1 pageAdobe Scan 04 Feb 2024biswajitrout13112003No ratings yet

- BÀI TẬP TRẮC NGHIỆM CHUYÊN ĐỀ CÂU BỊ ĐỘNGDocument11 pagesBÀI TẬP TRẮC NGHIỆM CHUYÊN ĐỀ CÂU BỊ ĐỘNGTuyet VuNo ratings yet

- Ashish TPR AssignmentDocument12 pagesAshish TPR Assignmentpriyesh20087913No ratings yet

- Corporate Social Responsibility (CSR) in GrameenphoneDocument7 pagesCorporate Social Responsibility (CSR) in GrameenphoneAfrina KarimNo ratings yet

- Philippine CuisineDocument1 pagePhilippine CuisineEvanFerrerNo ratings yet

- Periodical Test - English 5 - Q1Document7 pagesPeriodical Test - English 5 - Q1Raymond O. BergadoNo ratings yet

- Top 7506 SE Applicants For FB PostingDocument158 pagesTop 7506 SE Applicants For FB PostingShi Yuan ZhangNo ratings yet

- TRASSIR - Video Analytics OverviewDocument30 pagesTRASSIR - Video Analytics OverviewJhonattann EscobarNo ratings yet

- Super Typhoon HaiyanDocument25 pagesSuper Typhoon Haiyanapi-239410749No ratings yet