You might also like

- H. J. Heinz M&A: Case SynopsisDocument8 pagesH. J. Heinz M&A: Case SynopsisIA M.No ratings yet

- Zycus P2P Benchmark Report 2019 PDFDocument33 pagesZycus P2P Benchmark Report 2019 PDFpradeepvedulaNo ratings yet

- PROJECT TITLE - Value Chain Analysis of Hindustan Unilever LimitedDocument39 pagesPROJECT TITLE - Value Chain Analysis of Hindustan Unilever LimitedAnkita100% (1)

- Assessment Pack-BSBMKG501-OD (26) - 3.en - Id.id - enDocument16 pagesAssessment Pack-BSBMKG501-OD (26) - 3.en - Id.id - enihda0farhatun0nisakNo ratings yet

- L1-D5 Inference and PresentationDocument10 pagesL1-D5 Inference and PresentationSimarNo ratings yet

- Raw Materials Analyst ReportDocument6 pagesRaw Materials Analyst ReportGaurav ChandelNo ratings yet

- Case Study - Agvs - ProcurementDocument17 pagesCase Study - Agvs - ProcurementSrividhyaNo ratings yet

- Oracle Fusion Applications OverviewDocument38 pagesOracle Fusion Applications OverviewSreenivas PNo ratings yet

- Procurement Management Plan TemplateDocument7 pagesProcurement Management Plan Templatekareem3456No ratings yet

- Banking Basics SBI PDFDocument90 pagesBanking Basics SBI PDFjaytrips9881No ratings yet

- Global Business Services: Performance ImprovementDocument139 pagesGlobal Business Services: Performance ImprovementBea Cassandra EdnilaoNo ratings yet

- New Jda Board Appointed at The 22nd Annual General MeetingDocument3 pagesNew Jda Board Appointed at The 22nd Annual General MeetingJDANo ratings yet

- 2018 ERP ReportDocument40 pages2018 ERP ReportkhalideNo ratings yet

- 2021 State of ESG Reporting and PerformanceDocument21 pages2021 State of ESG Reporting and PerformanceJerry AndayaNo ratings yet

- MultiplesDocument49 pagesMultiplesDekov72No ratings yet

- PWC PreSIP Diptimaya SarangiDocument15 pagesPWC PreSIP Diptimaya SarangiChandan KumarNo ratings yet

- GX 2021 Global Shared Services Report DeloitteDocument27 pagesGX 2021 Global Shared Services Report DeloittearrassenNo ratings yet

- Report 2020 State of Agility Procurement Supply R1.1Document12 pagesReport 2020 State of Agility Procurement Supply R1.1Joost van BoeschotenNo ratings yet

- Wipro Limited: Investor PresentationDocument19 pagesWipro Limited: Investor PresentationKaveri PandeyNo ratings yet

- Global Shared Services 2021 150621Document27 pagesGlobal Shared Services 2021 150621Salma BennaniNo ratings yet

- CXO Increments Survey 2023 ReportDocument12 pagesCXO Increments Survey 2023 Reportmarvel mNo ratings yet

- Us 2023 Global Shared Services and Outsourcing Survey Executive SummaryDocument29 pagesUs 2023 Global Shared Services and Outsourcing Survey Executive SummaryReipudaman Singh ShahiNo ratings yet

- Report On Goods and Services Tax Survey: Industry Expectations and PerceptionsDocument32 pagesReport On Goods and Services Tax Survey: Industry Expectations and PerceptionsdesaikeyurNo ratings yet

- SGR - GCC Consulting Market 2016 - ExcerptDocument12 pagesSGR - GCC Consulting Market 2016 - Excerptmr6356No ratings yet

- Singapore Fintech Report 2021 Alibaba Cloud Fintech News SGDocument19 pagesSingapore Fintech Report 2021 Alibaba Cloud Fintech News SGCHOIRUL HIDAYATNo ratings yet

- ImportantDocument25 pagesImportantHossein SassaniNo ratings yet

- 2020 REPORT: Leveraging Technology To Optimize Your BusinessDocument39 pages2020 REPORT: Leveraging Technology To Optimize Your Business9980139892No ratings yet

- Crayon State of Competitive Intelligence 2019Document57 pagesCrayon State of Competitive Intelligence 2019Rodrigo MazuNo ratings yet

- 2021 Recruiting Metrics and KPIsDocument34 pages2021 Recruiting Metrics and KPIsAttyubNo ratings yet

- Company Profile Infosys Limited PremiumDocument30 pagesCompany Profile Infosys Limited PremiumRubina RubinaNo ratings yet

- Shareholder Letter Q4 2020Document24 pagesShareholder Letter Q4 2020y_fakoriNo ratings yet

- 2021 Procurement Key Issues: ALL Spend, ALL Suppliers, NO CompromisesDocument19 pages2021 Procurement Key Issues: ALL Spend, ALL Suppliers, NO CompromisesMarcos TobarNo ratings yet

- Value Conservation To Value Creation: COVID-19: Path To RecoveryDocument25 pagesValue Conservation To Value Creation: COVID-19: Path To RecoveryPrem RavalNo ratings yet

- 2019 Digital Operations Study For ChemicalsDocument16 pages2019 Digital Operations Study For Chemicalssam.dmaNo ratings yet

- Annual Report 2020 Full Version PDF 1Document161 pagesAnnual Report 2020 Full Version PDF 1pukis pukisNo ratings yet

- FRA ASSIGNMENT - AnkitAgarwal - 22620Document1 pageFRA ASSIGNMENT - AnkitAgarwal - 22620Ankit AgarwalNo ratings yet

- Wipro Investor PresentationDocument18 pagesWipro Investor PresentationursimmiNo ratings yet

- EY India Gic Benchmarking StudyDocument9 pagesEY India Gic Benchmarking StudyaakilNo ratings yet

- Digital Vortex 2019Document16 pagesDigital Vortex 2019Miguel Peralta100% (1)

- Global in House Centers GIC Benchmarking Study 2015 Key Takeaways PDFDocument9 pagesGlobal in House Centers GIC Benchmarking Study 2015 Key Takeaways PDFSudip DahiyaNo ratings yet

- SAPIENS IR PPT Q3 2015 Results November 2015Document43 pagesSAPIENS IR PPT Q3 2015 Results November 2015Yves-donald MakoumbouNo ratings yet

- 2020 Freelancer Rates Report by YunoJunoDocument52 pages2020 Freelancer Rates Report by YunoJunorupert1974No ratings yet

- Management Development Institute: CRBV Project ReportDocument25 pagesManagement Development Institute: CRBV Project ReportPuneet GargNo ratings yet

- ReportDocument276 pagesReportishuch24No ratings yet

- How Much Disruption?: Deloitte Global Outsourcing Survey 2020Document20 pagesHow Much Disruption?: Deloitte Global Outsourcing Survey 2020Billy MaNo ratings yet

- Survey of Advert Leaders On Media Trends 2006Document21 pagesSurvey of Advert Leaders On Media Trends 2006Silvina TatavittoNo ratings yet

- Presentation On Research CaseDocument17 pagesPresentation On Research CaseRomanNo ratings yet

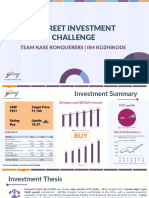

- R-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeDocument12 pagesR-Street Investment Challenge: Team Kase Konquerers - Iim KozhikodeApoorva JainNo ratings yet

- CSR Reading 5 KPMG India CSR Reporting Survey 2019Document108 pagesCSR Reading 5 KPMG India CSR Reporting Survey 2019Chetan ChughNo ratings yet

- Key Insights On M&A Advisory Fees in The Middle Market.: Partnered WithDocument27 pagesKey Insights On M&A Advisory Fees in The Middle Market.: Partnered Withnotcor nowNo ratings yet

- Bajaj Finance Limited Ar 2022 23Document415 pagesBajaj Finance Limited Ar 2022 23nowdu purnimaNo ratings yet

- CLOC 2019 State of The Industry FINALDocument26 pagesCLOC 2019 State of The Industry FINALDanielNo ratings yet

- Ashok VemuriDocument18 pagesAshok Vemurigauravspatil2211No ratings yet

- Bajaj Finance Limited Ar 2022 23Document473 pagesBajaj Finance Limited Ar 2022 23Gaurav SinghNo ratings yet

- Bao Zun PresentationDocument33 pagesBao Zun Presentationsiddharth_parikh4No ratings yet

- 2023 B2B Marketing Mix ReportDocument12 pages2023 B2B Marketing Mix ReportLahcen BoutayebNo ratings yet

- The Customer Data Platform ReportDocument28 pagesThe Customer Data Platform ReportCommon UserNo ratings yet

- Digital Enterprise MaturityDocument72 pagesDigital Enterprise MaturityTing wongNo ratings yet

- Document 2021 B2B Marketing Mix ReportDocument14 pagesDocument 2021 B2B Marketing Mix ReportBright Samuel100% (1)

- IBISWorld - Tutoring & Test Preparation Franchises in The US - 2019Document29 pagesIBISWorld - Tutoring & Test Preparation Franchises in The US - 2019uwybkpeyawxubbhxjyNo ratings yet

- Tech Mahindra - Company AnalysisDocument27 pagesTech Mahindra - Company AnalysisAdesh D.100% (1)

- Persistent Sys Case StudyDocument34 pagesPersistent Sys Case StudyGrim ReaperNo ratings yet

- OpenView 2019 SaaS Benchmarks Report PDFDocument64 pagesOpenView 2019 SaaS Benchmarks Report PDFyann2No ratings yet

- Rapport HSBC M&ADocument19 pagesRapport HSBC M&AMatthieu LévêqueNo ratings yet

- BCG The Evolving State of Digital Transformation Slideshow Sept 2020Document17 pagesBCG The Evolving State of Digital Transformation Slideshow Sept 2020zl972098576No ratings yet

- RMK Aramark March 2006 PresentationDocument30 pagesRMK Aramark March 2006 PresentationAla BasterNo ratings yet

- Marketing - Mix - 2020 - Report Final-1 PDFDocument14 pagesMarketing - Mix - 2020 - Report Final-1 PDFJal JeetNo ratings yet

- Edppa Law 2020Document89 pagesEdppa Law 2020LIGALIZ GEOPHYSICALNo ratings yet

- A486163 PDFDocument146 pagesA486163 PDFfuckscribNo ratings yet

- Drug Policy of OdishaDocument150 pagesDrug Policy of OdishaprayasdansanaNo ratings yet

- User Role in ProcurementDocument3 pagesUser Role in Procurementbaomondi100% (2)

- Operacle Case StudyDocument7 pagesOperacle Case StudynisargNo ratings yet

- Pad370 - ProcurementDocument5 pagesPad370 - Procurement전수라No ratings yet

- Lidl SupplierInformationPack 2022Document28 pagesLidl SupplierInformationPack 2022royalbakerytNo ratings yet

- Mohit Rathi Sip Report 01Document19 pagesMohit Rathi Sip Report 01Aksh EximNo ratings yet

- Task ManagementDocument11 pagesTask Managementnaveedskhan100% (1)

- Final PPT E-ProcDocument40 pagesFinal PPT E-ProcMeet DedhiaNo ratings yet

- Lec 5 Selection of Civil EngineerDocument12 pagesLec 5 Selection of Civil EngineerDark bearcat ArzadonNo ratings yet

- Revised IRR of RA 9184Document114 pagesRevised IRR of RA 9184zanpaktho100% (3)

- Vacancy - Procurement Property Management Officer Paterson Job Grade c1 Mva FundDocument1 pageVacancy - Procurement Property Management Officer Paterson Job Grade c1 Mva FundkameeldoringnamibiaNo ratings yet

- Dispute Assingment Part A and B MBA CPM BG-2 SG-7Document34 pagesDispute Assingment Part A and B MBA CPM BG-2 SG-7Paras ChauhanNo ratings yet

- Gas Well POP Flow Time Improvemet PDFDocument10 pagesGas Well POP Flow Time Improvemet PDFAlif ArtantoNo ratings yet

- Social Sustainability Strategy Across The Supply Chain: A Conceptual Approach From The Organisational PerspectiveDocument16 pagesSocial Sustainability Strategy Across The Supply Chain: A Conceptual Approach From The Organisational PerspectiveSittie Faraidah Riga SalicNo ratings yet

- Session 1 NPF Overview & Introduction PDFDocument32 pagesSession 1 NPF Overview & Introduction PDFRico SamuelNo ratings yet

- Advanced Courseguide in Quantity SurveyingDocument2 pagesAdvanced Courseguide in Quantity Surveyingsmanikan03No ratings yet

- DO 032 s2017Document309 pagesDO 032 s2017Bien_Garcia_II_1841100% (1)

- Estimating The Benefits and Risks of Implementing E-ProcurementDocument13 pagesEstimating The Benefits and Risks of Implementing E-ProcurementPranay Singh RaghuvanshiNo ratings yet

- Balance of Plant Systems: Key Trends and OutlookDocument25 pagesBalance of Plant Systems: Key Trends and OutlookpvenkyNo ratings yet

- Chapter 4 - Procurment and Contract ManagementDocument31 pagesChapter 4 - Procurment and Contract ManagementYosef KirosNo ratings yet

- SCMDocument15 pagesSCMimran.pkNo ratings yet