You might also like

- RR 12-99Document16 pagesRR 12-99doraemoanNo ratings yet

- Entertainment Law Outline Winter 2008Document129 pagesEntertainment Law Outline Winter 2008downsowf100% (1)

- Special Audit in GSTDocument2 pagesSpecial Audit in GSTGautamNo ratings yet

- DRC-03 (4) Applicability and Procedure To Pay Additional TaxDocument3 pagesDRC-03 (4) Applicability and Procedure To Pay Additional Taxevertry27387No ratings yet

- Demand & RecoveryDocument24 pagesDemand & Recoverygeegostral chhabraNo ratings yet

- Provisional Assessment GSTDocument2 pagesProvisional Assessment GSTygscseNo ratings yet

- Demand and RecoveryDocument7 pagesDemand and RecoveryDebaNo ratings yet

- Instruction No 022022 GST Dated 22032022Document13 pagesInstruction No 022022 GST Dated 22032022GroupA PreventiveNo ratings yet

- Instruction NoticeDocument4 pagesInstruction Noticedeepakbhanwala66No ratings yet

- AssessmentDocument3 pagesAssessmentSWETCHCHA MISKANo ratings yet

- Assam Instruction No. 13 2023 GSTDocument2 pagesAssam Instruction No. 13 2023 GSTCA Kaushik Ranjan GoswamiNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismARJUNNo ratings yet

- CBICDocument4 pagesCBICArjun BiswasNo ratings yet

- GST Notices and CompliancesDocument7 pagesGST Notices and CompliancesSubhash VishwakarmaNo ratings yet

- Chapter 9 Reply of Notices Under GSTDocument15 pagesChapter 9 Reply of Notices Under GSTDR. PREETI JINDALNo ratings yet

- 20 BPI vs. CIR (GR No. 139736, October 17, 2005)Document41 pages20 BPI vs. CIR (GR No. 139736, October 17, 2005)Alfred Garcia100% (1)

- Offences and Penalties Under GST Act: Tax Law-Ii Assignment OnDocument14 pagesOffences and Penalties Under GST Act: Tax Law-Ii Assignment Onvinay sharmaNo ratings yet

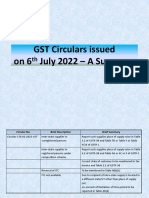

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- GST Refund 26102015 NewDocument30 pagesGST Refund 26102015 NewNikhil SinghalNo ratings yet

- RR No. 33-2020Document2 pagesRR No. 33-2020JejomarNo ratings yet

- Subpoena Duces TecumDocument3 pagesSubpoena Duces TecumerinemilyNo ratings yet

- Merely Signing The Statement During Investigation Under Coercion and Admitting Tax Liability Not Amounts To Self-Assessment or SelfDocument5 pagesMerely Signing The Statement During Investigation Under Coercion and Admitting Tax Liability Not Amounts To Self-Assessment or SelfShrey SharmaNo ratings yet

- Offences and Penalty Provisions Under GST: DisclaimerDocument8 pagesOffences and Penalty Provisions Under GST: DisclaimerHumanyu KabeerNo ratings yet

- Commissioner of Internal Revenue vs. Systems Technology Institute, Inc., 833 SCRA 285, July 26, 2017Document13 pagesCommissioner of Internal Revenue vs. Systems Technology Institute, Inc., 833 SCRA 285, July 26, 2017Wallaze EbdaoNo ratings yet

- SOP For ScrutinyDocument5 pagesSOP For Scrutinyacgstdiv4No ratings yet

- University Physicians Services Inc. - Management v. CirDocument27 pagesUniversity Physicians Services Inc. - Management v. CirBeltran KathNo ratings yet

- Do You Know GST JULY 21Document18 pagesDo You Know GST JULY 21CA Ranjan MehtaNo ratings yet

- Commissioner of Internal Revenue vs. BASF Coating + Inks Phil., Inc., 743 SCRA 113, November 26, 2014Document17 pagesCommissioner of Internal Revenue vs. BASF Coating + Inks Phil., Inc., 743 SCRA 113, November 26, 2014Maria Ana LemonNo ratings yet

- GST - CGST - Circulars - 178-10-2022 Dated - 03 August 2022Document9 pagesGST - CGST - Circulars - 178-10-2022 Dated - 03 August 2022Bhavya JindalNo ratings yet

- Suspension of Running of Statute of Limitations. Sec. 223, NIRCDocument2 pagesSuspension of Running of Statute of Limitations. Sec. 223, NIRCshiejingNo ratings yet

- Chapter 34Document10 pagesChapter 34Kaila Mae Tan DuNo ratings yet

- Assessment and Audit Under GST-DGTPS-New Delhi-19!12!2023-FinalDocument118 pagesAssessment and Audit Under GST-DGTPS-New Delhi-19!12!2023-Finalsanjaypunjabi78No ratings yet

- GSTR-3B Vs GSTR 1 Mismatch - Rule 88C Perspective - Taxguru - inDocument4 pagesGSTR-3B Vs GSTR 1 Mismatch - Rule 88C Perspective - Taxguru - inRamkumar SNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismjaipalmeNo ratings yet

- Revenue Memorandum Order No. 42-03: October 23, 2003Document11 pagesRevenue Memorandum Order No. 42-03: October 23, 2003nathalie velasquezNo ratings yet

- CIR vs. Seagate Technology PhilippinesDocument29 pagesCIR vs. Seagate Technology PhilippinesAronJamesNo ratings yet

- CIR v. Isabela Cultural CorporationDocument14 pagesCIR v. Isabela Cultural CorporationkimNo ratings yet

- University of Physician V CIRDocument24 pagesUniversity of Physician V CIROlivia JaneNo ratings yet

- GST Unit 1 BDocument23 pagesGST Unit 1 BMukul BhatnagarNo ratings yet

- 4.1 Administration & Authorities Powes Under GSTDocument12 pages4.1 Administration & Authorities Powes Under GSTPoorboyNo ratings yet

- Bba GST Unit 4Document11 pagesBba GST Unit 4darshansah1990No ratings yet

- Payment of Tax: FAQ'sDocument23 pagesPayment of Tax: FAQ'smun1barejaNo ratings yet

- Merits of GST:: Compensation To Loss Making States For Five Years: It Has Been Proposed That TheDocument10 pagesMerits of GST:: Compensation To Loss Making States For Five Years: It Has Been Proposed That TheJyoti SinghNo ratings yet

- NIRC Tax RemediesDocument27 pagesNIRC Tax RemediesNodlesde Awanab ZurcNo ratings yet

- GST - Audit OffencesDocument35 pagesGST - Audit OffencesApurva DharNo ratings yet

- GST Weekly Update - 53 - 2023-24Document4 pagesGST Weekly Update - 53 - 2023-24Sarabjeet SinghNo ratings yet

- Cancellation of RegistrationDocument2 pagesCancellation of RegistrationRajdev AssociatesNo ratings yet

- CIR VDocument2 pagesCIR ValnaharNo ratings yet

- Recovery of Tax: (Goods and Services Tax)Document3 pagesRecovery of Tax: (Goods and Services Tax)11priyagargNo ratings yet

- Navigating The Labyrinth of GST NoticesDocument3 pagesNavigating The Labyrinth of GST Noticestarun pandeNo ratings yet

- REMEDIES by Atty. LimDocument4 pagesREMEDIES by Atty. LimJeninah Arriola CalimlimNo ratings yet

- GST Interest Liability U/Sec - 50 of CGST Act 2017Document6 pagesGST Interest Liability U/Sec - 50 of CGST Act 2017Saurabh JunejaNo ratings yet

- Philippine Bank of Communications Vs CIRDocument1 pagePhilippine Bank of Communications Vs CIRLisley Gem AmoresNo ratings yet

- PWC Client AdvisoryDocument8 pagesPWC Client AdvisoryFedsNo ratings yet

- Mismatch in Tax Liabilities-No Longer A Factual ConcernDocument4 pagesMismatch in Tax Liabilities-No Longer A Factual ConcernKunwarbir Singh lohatNo ratings yet

- Recovery of Tax: (Goods and Services Tax)Document3 pagesRecovery of Tax: (Goods and Services Tax)sridharanNo ratings yet

- Rev. Regs. 12-99Document21 pagesRev. Regs. 12-99Phoebe SpaurekNo ratings yet

- G.R. No. 165451. December 3, 2014. LG ELECTRONICS PHILIPPINES, INC., Petitioner, vs. Commissioner of Internal Revenue, RespondentDocument31 pagesG.R. No. 165451. December 3, 2014. LG ELECTRONICS PHILIPPINES, INC., Petitioner, vs. Commissioner of Internal Revenue, RespondentJessica mabungaNo ratings yet

- Tax AssignmentDocument6 pagesTax AssignmentShubh DixitNo ratings yet

- Tax-Remedies (Govt-Remedies-Highlights)Document38 pagesTax-Remedies (Govt-Remedies-Highlights)Yves Nicollete LabadanNo ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Internship Report 2023-2Document64 pagesInternship Report 2023-2Kajal Dnyaneshwar MhasalNo ratings yet

- KhawarijDocument5 pagesKhawarijoceanmist0101No ratings yet

- Roman V GrimaltDocument2 pagesRoman V GrimaltClarence ProtacioNo ratings yet

- Institutional CorrectionDocument9 pagesInstitutional CorrectionJoshua D None-NoneNo ratings yet

- Curriculum Leadership Strategies For Development and Implementation 4th Edition Glatthorn Test BankDocument25 pagesCurriculum Leadership Strategies For Development and Implementation 4th Edition Glatthorn Test BankMrRogerAndersonMDdbkj100% (58)

- 01 Worksheet 1BDocument1 page01 Worksheet 1BKarina GusionNo ratings yet

- Caurdanetaan Piece Worker v. LaguesmaDocument14 pagesCaurdanetaan Piece Worker v. LaguesmaJamiah Obillo HulipasNo ratings yet

- Petition: Regional Trial Court Branch 04Document3 pagesPetition: Regional Trial Court Branch 04cris baligodNo ratings yet

- Mediatraining GEPRA ENGDocument30 pagesMediatraining GEPRA ENGFollowTheSafeWayNo ratings yet

- Ambush at Keystone No.1: Coal Miners ProtestDocument28 pagesAmbush at Keystone No.1: Coal Miners ProtestcrumplepapertigersNo ratings yet

- Dwnload Full Statistics For Social Workers 8th Edition Weinbach Test Bank PDFDocument35 pagesDwnload Full Statistics For Social Workers 8th Edition Weinbach Test Bank PDFmasonh7dswebb100% (11)

- Final ThesisDocument75 pagesFinal ThesisThảo PhươngNo ratings yet

- Work of Investment Banking (Repaired)Document12 pagesWork of Investment Banking (Repaired)Shivani Singh ChandelNo ratings yet

- Company Law PDFDocument3 pagesCompany Law PDFJaspreet SinghNo ratings yet

- BGDRV1368F22DW800701Document2 pagesBGDRV1368F22DW800701alamgir80100% (1)

- Philosophy Education Society IncDocument31 pagesPhilosophy Education Society IncAnonymous lVC1HGpHP3No ratings yet

- Dawn (Newspaper) : Dawn Is Pakistan's Oldest, Leading and Most Widely Read EnglishDocument4 pagesDawn (Newspaper) : Dawn Is Pakistan's Oldest, Leading and Most Widely Read Englishسیاہ پوشNo ratings yet

- Great Pacific Life Insurance Corp Vs CADocument7 pagesGreat Pacific Life Insurance Corp Vs CALeigh BarcelonaNo ratings yet

- Chap 8 Distribution ManagementDocument30 pagesChap 8 Distribution ManagementThomas Niconar PalemNo ratings yet

- City of Charlotte Social Media Policy 5.1.2015Document7 pagesCity of Charlotte Social Media Policy 5.1.2015Hank LeeNo ratings yet

- 26 So Ping Bun v. Court of Appeals PDFDocument5 pages26 So Ping Bun v. Court of Appeals PDFAbegail GaledoNo ratings yet

- People V Sanchez - Compound CrimeDocument2 pagesPeople V Sanchez - Compound CrimeKiana AbellaNo ratings yet

- Massachusetts Institute of Technology: 8.223, Classical Mechanics II Exercises 1Document4 pagesMassachusetts Institute of Technology: 8.223, Classical Mechanics II Exercises 1Uriel MorenoNo ratings yet

- Empirical - Molecular - Formula - Drug - Bust 2021Document3 pagesEmpirical - Molecular - Formula - Drug - Bust 2021Linda EscobarNo ratings yet

- Ca2 Law440 AmanDocument29 pagesCa2 Law440 Amanmegha saxenaNo ratings yet

- INTERCHANGEDocument102 pagesINTERCHANGEDiego AvendañoNo ratings yet

- QAD 002 Change Control ProcedureDocument14 pagesQAD 002 Change Control ProcedureShejil BalakrishnanNo ratings yet

- Noachites SchwarzschildDocument37 pagesNoachites SchwarzschildpruzhanerNo ratings yet

- AFFIDAVIT (Rs. 10/-Stamp Paper Language) Attested by Notary PublicDocument1 pageAFFIDAVIT (Rs. 10/-Stamp Paper Language) Attested by Notary PublicRupali ChadhaNo ratings yet