You might also like

- Introduction To Audting - Nature Purpose and Scope of Auditing - 2021Document29 pagesIntroduction To Audting - Nature Purpose and Scope of Auditing - 2021cleophacerevivalNo ratings yet

- Analytical Procedure, Audit Evidence and Audit TechniquesDocument29 pagesAnalytical Procedure, Audit Evidence and Audit TechniquescleophacerevivalNo ratings yet

- Classification of Auditing Bacc 2 - 2020-21-1Document26 pagesClassification of Auditing Bacc 2 - 2020-21-1Laila IbrahimNo ratings yet

- A6.4 A UNIT 1 & 2 Auditing PracticesDocument27 pagesA6.4 A UNIT 1 & 2 Auditing PracticesGaurav MahajanNo ratings yet

- Audit Planning 46 PagesDocument46 pagesAudit Planning 46 PagescleophacerevivalNo ratings yet

- Lecture 2 - Auditor Responsibility ObjectivesDocument32 pagesLecture 2 - Auditor Responsibility ObjectivesPriscella LlewellynNo ratings yet

- AUDITORSDocument88 pagesAUDITORSAmina AmenNo ratings yet

- Lecture OneDocument20 pagesLecture OnemmjzpfdjjgNo ratings yet

- Introduction To AuditingDocument12 pagesIntroduction To AuditingJahnavi BadlaniNo ratings yet

- Mid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Document7 pagesMid-Term Exam - IA - Ashilla Nadiya Amany - 2002030013Ashilla Nadya AmanyNo ratings yet

- Auditing Teaching MaterialDocument49 pagesAuditing Teaching MaterialGetachew JoriyeNo ratings yet

- Summary of Audit & Assurance Application Level - Self Test With Immediate AnswerDocument72 pagesSummary of Audit & Assurance Application Level - Self Test With Immediate AnswerIQBAL MAHMUDNo ratings yet

- CH 1Document15 pagesCH 1Harsh DaneNo ratings yet

- Audit and AssuranceDocument53 pagesAudit and Assuranceattaullah_niazi93No ratings yet

- Auditing Past Paper 2017Document11 pagesAuditing Past Paper 2017DaniyalNo ratings yet

- Year Unit I Introduction To Auditing Meaning and Definition of AuditingDocument53 pagesYear Unit I Introduction To Auditing Meaning and Definition of AuditingTimothy KambuniNo ratings yet

- READING REPORT in Auditing and Assurance Concepts and ApplicationDocument3 pagesREADING REPORT in Auditing and Assurance Concepts and Applicationhazel alvarezNo ratings yet

- Lecture 1-Part I: Introduction To Audit and Assurance ServicesDocument65 pagesLecture 1-Part I: Introduction To Audit and Assurance ServicesShueh Yi LimNo ratings yet

- Chapter 1Document21 pagesChapter 1Alice LowNo ratings yet

- Audit Framework and RegulationDocument16 pagesAudit Framework and RegulationTousif Galib100% (2)

- Lecture 08 Ch04Document12 pagesLecture 08 Ch04nanaNo ratings yet

- Chapter One An Overview of Auditing: Auditing Principles and Practices IDocument36 pagesChapter One An Overview of Auditing: Auditing Principles and Practices IYehualashet MulugetaNo ratings yet

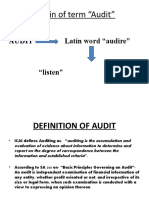

- Origin of Term "Audit": AUDIT Latin Word "Audire"Document17 pagesOrigin of Term "Audit": AUDIT Latin Word "Audire"ranjana7123No ratings yet

- Auditing Corporate Governance B.Com Semester VI - CBCS+1Document146 pagesAuditing Corporate Governance B.Com Semester VI - CBCS+1Beauty AdhikaryNo ratings yet

- Nature of AuditingDocument11 pagesNature of AuditingSoma BanikNo ratings yet

- C9ay1 HsijbDocument15 pagesC9ay1 HsijbEyob FirstNo ratings yet

- Introduction To AuditingDocument35 pagesIntroduction To Auditing21BCO097 ChelsiANo ratings yet

- Auditing Teaching Material Edited OneDocument64 pagesAuditing Teaching Material Edited OneGetachew JoriyeNo ratings yet

- Auditing: Chapter 1: Introduction To AuditingDocument45 pagesAuditing: Chapter 1: Introduction To AuditingMIR AADILNo ratings yet

- AuditDocument90 pagesAuditSailesh GoenkkaNo ratings yet

- Audit 10 JournalDocument7 pagesAudit 10 Journalkris salacNo ratings yet

- FAU Review Note - Chapter 2 Auditor's ResponsibilitiesDocument5 pagesFAU Review Note - Chapter 2 Auditor's ResponsibilitiesMonikachhna HuotNo ratings yet

- Difference Between Accounting and AuditingDocument21 pagesDifference Between Accounting and AuditingLaraib SalmanNo ratings yet

- Auditor's ReportDocument23 pagesAuditor's ReportcleophacerevivalNo ratings yet

- Audit and Assurance (AA)Document30 pagesAudit and Assurance (AA)YousafNo ratings yet

- Principles of Auditing FinishedDocument85 pagesPrinciples of Auditing FinishedDeepan KumarNo ratings yet

- Week 1 Overview of Audit - ACTG411 Assurance Principles, Professional Ethics & Good GovDocument6 pagesWeek 1 Overview of Audit - ACTG411 Assurance Principles, Professional Ethics & Good GovMarilou PanisalesNo ratings yet

- AUDITING one 2015 √√√√√√√√√√√√πππππDocument41 pagesAUDITING one 2015 √√√√√√√√√√√√πππππoliifan HundeNo ratings yet

- Module 2 - Introduction To FS AuditDocument5 pagesModule 2 - Introduction To FS AuditLysss EpssssNo ratings yet

- Auditing and EthicsDocument97 pagesAuditing and EthicsdeterminemsNo ratings yet

- AaaaDocument18 pagesAaaaPinak DebNo ratings yet

- Lesson - Substantive ProceduresDocument8 pagesLesson - Substantive ProceduresCherise TrollipNo ratings yet

- Solution Manual For Auditing and Assurance Services 4th Edition by LouwersDocument14 pagesSolution Manual For Auditing and Assurance Services 4th Edition by LouwersMohammad Monir uz ZamanNo ratings yet

- Introduction To Audit and Assurance ServicesDocument61 pagesIntroduction To Audit and Assurance ServicesMAAN SHIN ANGNo ratings yet

- F8 ACCA Summary + Revision Notes 2017Document148 pagesF8 ACCA Summary + Revision Notes 2017Arbab JhangirNo ratings yet

- AUDIT BasicDocument10 pagesAUDIT BasicKingo StreamNo ratings yet

- Chapter 1 Overview of AuditingDocument28 pagesChapter 1 Overview of AuditingTesfaye DesalegnNo ratings yet

- 1498721945audit JoinerDocument70 pages1498721945audit JoinerRockNo ratings yet

- DFM Auditing Notes SpecialDocument120 pagesDFM Auditing Notes SpecialMwesigwa DaniNo ratings yet

- PSBA - Introduction To Assurance and Related ServicesDocument6 pagesPSBA - Introduction To Assurance and Related ServicesephraimNo ratings yet

- 5th SEM AUDITING MATERIAL - pdf300Document33 pages5th SEM AUDITING MATERIAL - pdf300TayyabshabbirNo ratings yet

- Auditing NotesDocument65 pagesAuditing NotesTushar GaurNo ratings yet

- IR4&6 - at 01 - Introduction To Assurance and Related Services (Incl. Intro To Audit)Document5 pagesIR4&6 - at 01 - Introduction To Assurance and Related Services (Incl. Intro To Audit)angelinodaivehNo ratings yet

- Basic Concepts in AuditingDocument28 pagesBasic Concepts in AuditingHarikrishnaNo ratings yet

- Auditing Semester VI PDFDocument71 pagesAuditing Semester VI PDFjishnu SNo ratings yet

- AuditingDocument16 pagesAuditingkkvNo ratings yet

- Concept and Need For AssuranceDocument5 pagesConcept and Need For AssuranceAudit and Assurance100% (1)

- Assignment - 1 - AuditDocument9 pagesAssignment - 1 - AuditMuskan singh RajputNo ratings yet

- Cma Inter Audit - Marathon Notes Relevant For June and Dec 23Document64 pagesCma Inter Audit - Marathon Notes Relevant For June and Dec 23Sarfaraz ShaikhNo ratings yet

- The Institute of Finance ManagementDocument5 pagesThe Institute of Finance ManagementcleophacerevivalNo ratings yet

- PopDocument17 pagesPopcleophacerevivalNo ratings yet

- Mysterious Things in My LifeDocument1 pageMysterious Things in My LifecleophacerevivalNo ratings yet

- Muddy BTCTX 0797Document4 pagesMuddy BTCTX 0797cleophacerevivalNo ratings yet

- Book 1 GHYHJDocument2 pagesBook 1 GHYHJcleophacerevivalNo ratings yet

- Godlizen Felix Malle PDFDocument1 pageGodlizen Felix Malle PDFcleophacerevivalNo ratings yet

- AdventureDocument2 pagesAdventurecleophacerevivalNo ratings yet

- Evan Work 3Document4 pagesEvan Work 3cleophacerevivalNo ratings yet

- Group Assignment MaintenanceDocument2 pagesGroup Assignment MaintenancecleophacerevivalNo ratings yet

- Table of ContentsDocument15 pagesTable of ContentscleophacerevivalNo ratings yet

- Presentation 1Document1 pagePresentation 1cleophacerevivalNo ratings yet

- SushDocument1 pageSushcleophacerevivalNo ratings yet

- Official PabloDocument2 pagesOfficial PablocleophacerevivalNo ratings yet

- Lab 5Document2 pagesLab 5cleophacerevivalNo ratings yet

- CharlzDocument3 pagesCharlzcleophacerevivalNo ratings yet

- NAMPENDADocument1 pageNAMPENDAcleophacerevivalNo ratings yet

- MahunnahDocument5 pagesMahunnahcleophacerevivalNo ratings yet

- EDITHADocument2 pagesEDITHAcleophacerevivalNo ratings yet

- The Institute of Finance ManagementDocument1 pageThe Institute of Finance ManagementcleophacerevivalNo ratings yet

- Lecture 6.network LayerDocument21 pagesLecture 6.network LayercleophacerevivalNo ratings yet

- JGDocument3 pagesJGcleophacerevivalNo ratings yet

- Solution of ExercisesDocument4 pagesSolution of ExercisescleophacerevivalNo ratings yet

- Auditing Review QnsDocument10 pagesAuditing Review QnscleophacerevivalNo ratings yet

- Audit StrategyDocument4 pagesAudit StrategycleophacerevivalNo ratings yet

- The Enity Relationship ModelDocument39 pagesThe Enity Relationship ModelcleophacerevivalNo ratings yet

- Auditing Set 2Document7 pagesAuditing Set 2cleophacerevivalNo ratings yet

- Introduction To DatabaseDocument23 pagesIntroduction To DatabasecleophacerevivalNo ratings yet

- Auditor's ReportDocument23 pagesAuditor's ReportcleophacerevivalNo ratings yet

- Flotation Plant Optimisation s16Document223 pagesFlotation Plant Optimisation s16Jerzain AguilatNo ratings yet

- Forms of Business Ownership - Unit 5Document20 pagesForms of Business Ownership - Unit 5Nishant Sharma100% (1)

- CISM Study NotesDocument4 pagesCISM Study NotesLa Vita Di Lusso44% (9)

- Xc6o Cem Pinout Yr.09Document11 pagesXc6o Cem Pinout Yr.09TomášShishamanNo ratings yet

- Schengen VisaDocument4 pagesSchengen Visajannuchary1637No ratings yet

- TTL Digital ClockDocument5 pagesTTL Digital Clockyampire100% (1)

- Television and Video EngineeringDocument42 pagesTelevision and Video EngineeringGanesh ChandrasekaranNo ratings yet

- Program: 1St International Virtual Congress & 2021 Philippine Agriculturists' SummitDocument12 pagesProgram: 1St International Virtual Congress & 2021 Philippine Agriculturists' SummitCarla Malolot Miscala100% (1)

- Iqta'Document3 pagesIqta'ZABED AKHTARNo ratings yet

- ETM - Starter Picanto MT 2013Document1 pageETM - Starter Picanto MT 2013Hendra Gunawan100% (1)

- 122pm - Ijmr August 2023 Full JournalDocument488 pages122pm - Ijmr August 2023 Full Journalsinok5078No ratings yet

- Spareparts Air Suspension BPW 2022 EN 31052201Document154 pagesSpareparts Air Suspension BPW 2022 EN 31052201cursor10No ratings yet

- AgaSlots SASDocument3 pagesAgaSlots SASManolo GonzalezNo ratings yet

- Kyocera Fs-1020d Service ManualDocument109 pagesKyocera Fs-1020d Service ManualvonBoomslangNo ratings yet

- AdvtDocument5 pagesAdvtMohd KazimNo ratings yet

- TV LG LCD 32LG30 UD Chassis LA85DDocument35 pagesTV LG LCD 32LG30 UD Chassis LA85DIvan Leonardo Acevedo GalanNo ratings yet

- SPJ RB Script Group 3 - Final 1 1.2 2Document7 pagesSPJ RB Script Group 3 - Final 1 1.2 2YamSiriOdarnohNo ratings yet

- Rapid Visual Screening of Buildings For Potential Seismic Hazards FEMA P-154 Data Collection FormDocument1 pageRapid Visual Screening of Buildings For Potential Seismic Hazards FEMA P-154 Data Collection FormFauzy AslyNo ratings yet

- LXM23DU07M3X: Product Data SheetDocument10 pagesLXM23DU07M3X: Product Data SheetAshrafNo ratings yet

- Troubleshoot IP Configuration 3Document2 pagesTroubleshoot IP Configuration 3michaelNo ratings yet

- Standard 15 Progress Mapping and Sign OffDocument3 pagesStandard 15 Progress Mapping and Sign OffEstherNo ratings yet

- Lecture 11 DecantersDocument10 pagesLecture 11 DecantersfebrianNo ratings yet

- Bluman 5th - Chapter 8 HW Soln For My ClassDocument11 pagesBluman 5th - Chapter 8 HW Soln For My Classbill power100% (1)

- Manual C4 C5Document78 pagesManual C4 C5Leslie Morales75% (4)

- Sem3 MCQ HRMDocument8 pagesSem3 MCQ HRMvenkat annabhimoju50% (2)

- Multotec Trommel ScreensDocument6 pagesMultotec Trommel Screensalfredo_17110% (1)

- ME 522 - Power Plant Engineering - Steam Power Plant - Part 1 - LectureDocument56 pagesME 522 - Power Plant Engineering - Steam Power Plant - Part 1 - LectureJom Ancheta BautistaNo ratings yet

- Science, Technology, and Society: World History: Chapter OutlineDocument7 pagesScience, Technology, and Society: World History: Chapter OutlineRhea PicaNo ratings yet

- Interim Financial ReportingDocument10 pagesInterim Financial ReportingJoyce Ann Agdippa BarcelonaNo ratings yet

- Audi Qrs A4-2009 PDFDocument98 pagesAudi Qrs A4-2009 PDFJOHNNY5377No ratings yet