You might also like

- Mastering Financial Risk Management : Strategies for SuccessFrom EverandMastering Financial Risk Management : Strategies for SuccessNo ratings yet

- Market Riask of Ambee PharmaDocument12 pagesMarket Riask of Ambee PharmaSabbir ZamanNo ratings yet

- Literature ReviewDocument3 pagesLiterature ReviewneerjamNo ratings yet

- Multi-Asset Risk Modeling: Techniques for a Global Economy in an Electronic and Algorithmic Trading EraFrom EverandMulti-Asset Risk Modeling: Techniques for a Global Economy in an Electronic and Algorithmic Trading EraRating: 4.5 out of 5 stars4.5/5 (2)

- The Practice of Lending: A Guide to Credit Analysis and Credit RiskFrom EverandThe Practice of Lending: A Guide to Credit Analysis and Credit RiskNo ratings yet

- MFS- Risk Management in Banks muskanDocument54 pagesMFS- Risk Management in Banks muskansangambhardwaj64No ratings yet

- The Measurement and Management of Risks in BanksDocument21 pagesThe Measurement and Management of Risks in BanksGaurav GehlotNo ratings yet

- Return On Risk Managment FINAL PDFDocument8 pagesReturn On Risk Managment FINAL PDFJasonNo ratings yet

- Financial Markets and Inst Unit 4Document8 pagesFinancial Markets and Inst Unit 4Nitin PanwarNo ratings yet

- Fin Risk MGTDocument11 pagesFin Risk MGTmahipal2009No ratings yet

- Dissertation Project Report On Risk Management in BanksDocument38 pagesDissertation Project Report On Risk Management in BanksKelly HamiltonNo ratings yet

- Risk Measure Estimation in FinanceDocument4 pagesRisk Measure Estimation in FinanceAli SaeiNo ratings yet

- Alm Review of LiteratureDocument17 pagesAlm Review of LiteratureSai ViswasNo ratings yet

- Paper - Teoria de CuerdasDocument12 pagesPaper - Teoria de CuerdasSolver TutorNo ratings yet

- Executive SummaryDocument3 pagesExecutive SummaryArin ChattopadhyayNo ratings yet

- Risk AssessmentDocument4 pagesRisk AssessmentTijana DoberšekNo ratings yet

- Operational Risk Management in BanksDocument47 pagesOperational Risk Management in BanksJuhi Ansari100% (3)

- Risk management roles in insurance companiesDocument8 pagesRisk management roles in insurance companiesSaad MalikNo ratings yet

- Dissertation On Risk Management in Banking SectorDocument9 pagesDissertation On Risk Management in Banking SectorWhereCanIBuyResumePaperAkronNo ratings yet

- Risk Management 2Document45 pagesRisk Management 2virajNo ratings yet

- Master Thesis Financial Risk ManagementDocument6 pagesMaster Thesis Financial Risk Managementjilllyonstulsa100% (2)

- Dissertation - Credit Risk Management Priority, Case Study of Russian BankingDocument32 pagesDissertation - Credit Risk Management Priority, Case Study of Russian Bankingthemany2292No ratings yet

- CH - 7 Project Risk ManagemtnDocument20 pagesCH - 7 Project Risk Managemtnamit_idea1No ratings yet

- Oriental Bank of Commerce,: Head Office, DelhiDocument32 pagesOriental Bank of Commerce,: Head Office, DelhiAkshat SinghalNo ratings yet

- Arthance Risk Management White Paper August 20131Document7 pagesArthance Risk Management White Paper August 20131tabbforumNo ratings yet

- Background: Types of RisksDocument7 pagesBackground: Types of Risksnandish30No ratings yet

- Chapter 5Document25 pagesChapter 5recarejoanadelNo ratings yet

- Risk Management of Banking Sector: A Critique Review: Wael Moustafa Hassan Mohamed, PHD, MbaDocument10 pagesRisk Management of Banking Sector: A Critique Review: Wael Moustafa Hassan Mohamed, PHD, Mbashumon2657No ratings yet

- Principles of Risk: Minimum Correct Answers For This Module: 4/8Document12 pagesPrinciples of Risk: Minimum Correct Answers For This Module: 4/8Jovan SsenkandwaNo ratings yet

- Market Risk: Value at Risk and Stop Loss PoliciesDocument4 pagesMarket Risk: Value at Risk and Stop Loss PoliciesAnam TawhidNo ratings yet

- Credit Risk ManagementDocument16 pagesCredit Risk Managementkrishnalohia9No ratings yet

- OF Strategic Management ON: Corporate Strategy: H. Igor AnsoffDocument29 pagesOF Strategic Management ON: Corporate Strategy: H. Igor AnsoffBrilliant ManglaNo ratings yet

- Components and Calculation of Regulatory CapitalDocument13 pagesComponents and Calculation of Regulatory CapitalMuhammad ZulkifulNo ratings yet

- Thesis Risk Management BanksDocument7 pagesThesis Risk Management Banksaliyahhkingnewark100% (2)

- Risk Management Dissertation ExampleDocument8 pagesRisk Management Dissertation ExamplePaySomeoneToWriteYourPaperSavannah100% (1)

- Risk Management in BanksDocument26 pagesRisk Management in BanksDivya Keswani0% (1)

- Risk Management Systems in Banks: Genesis, Significance and ImplementationDocument32 pagesRisk Management Systems in Banks: Genesis, Significance and Implementationmahajan87No ratings yet

- Market Risk: You Manage What You MeasureDocument14 pagesMarket Risk: You Manage What You MeasureLuis EcheNo ratings yet

- Risk Management in BankingDocument6 pagesRisk Management in BankingPranto Pritom Roy1531stNo ratings yet

- Risk Management in Banking Sector Project ReportDocument71 pagesRisk Management in Banking Sector Project ReportSami ZamaNo ratings yet

- Risk Management Systems in Banks Genesis, Significance and ImplementationDocument20 pagesRisk Management Systems in Banks Genesis, Significance and Implementationrajajee43No ratings yet

- RV RV RV RV RV RV RVDocument7 pagesRV RV RV RV RV RV RVchirubavaNo ratings yet

- Unit 5Document28 pagesUnit 5Mohammad ShahvanNo ratings yet

- Deb Ashish 1Document119 pagesDeb Ashish 1Somnath DasNo ratings yet

- Risk Management in Banking Sector - An Empirical Study: Thirupathi Kanchu M. Manoj KumarDocument9 pagesRisk Management in Banking Sector - An Empirical Study: Thirupathi Kanchu M. Manoj KumarKunTal MoNdalNo ratings yet

- 1.0 Stress TestingDocument21 pages1.0 Stress Testing2rmjNo ratings yet

- TIOB - Asset & Liability Management For Banks in Africa 2021Document7 pagesTIOB - Asset & Liability Management For Banks in Africa 2021Alex KimboiNo ratings yet

- Financial Risk (2) KKKKKKKKKKKKDocument26 pagesFinancial Risk (2) KKKKKKKKKKKKHamadaAttiaNo ratings yet

- Term Paper On Financial Risk ManagementDocument8 pagesTerm Paper On Financial Risk Managementea6xrjc4100% (1)

- Dissertation Report On Risk Management in BanksDocument6 pagesDissertation Report On Risk Management in BanksBestCustomPapersUK100% (1)

- Asset Liability ManagementDocument18 pagesAsset Liability Managementmahesh19689No ratings yet

- Chapter-1 Introduction To The StudyDocument70 pagesChapter-1 Introduction To The StudyMOHAMMED KHAYYUMNo ratings yet

- Credit Risk Management Master ThesisDocument5 pagesCredit Risk Management Master ThesisPapersHelpEvansville100% (2)

- Risk Assessment Methods in The Banking Sector 1711464428Document10 pagesRisk Assessment Methods in The Banking Sector 1711464428junaidNo ratings yet

- Derivative Market AnalysisDocument96 pagesDerivative Market AnalysisMaza StreetNo ratings yet

- Credit Risk ManagementDocument57 pagesCredit Risk ManagementP. RaghurekhaNo ratings yet

- Practical Guide To Risk Assessment (PWC 2008)Document40 pagesPractical Guide To Risk Assessment (PWC 2008)ducuh80% (5)

- Financial MarketsDocument2 pagesFinancial MarketsSheiryNo ratings yet

- LOB Assignment 2Document11 pagesLOB Assignment 2SheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument3 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- KM Assignment 2Document14 pagesKM Assignment 2SheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument3 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Financial MarketsDocument2 pagesFinancial MarketsSheiryNo ratings yet

- Financial Market Impact of The COVIDDocument7 pagesFinancial Market Impact of The COVIDSheiryNo ratings yet

- Coronavirus DiseaseDocument3 pagesCoronavirus DiseaseSheiryNo ratings yet

- Coronavirus DiseaseDocument3 pagesCoronavirus DiseaseSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument8 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Financial Market Impact of The COVIDDocument7 pagesFinancial Market Impact of The COVIDSheiryNo ratings yet

- M&A CH# 08 (Summary)Document14 pagesM&A CH# 08 (Summary)SheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument4 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument10 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument15 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument6 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Company vs PartnershipDocument20 pagesCompany vs PartnershipSheiryNo ratings yet

- Company vs PartnershipDocument20 pagesCompany vs PartnershipSheiryNo ratings yet

- National University M&A Report on Mergers and AcquisitionsDocument8 pagesNational University M&A Report on Mergers and AcquisitionsSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument8 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument15 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument10 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Perception and Decision Making FactorsDocument9 pagesPerception and Decision Making FactorsSheiryNo ratings yet

- Department of Management Sciences, National University of Modern LanguagesDocument6 pagesDepartment of Management Sciences, National University of Modern LanguagesSheiryNo ratings yet

- Bibf Course Catalogue 2012 PDFDocument370 pagesBibf Course Catalogue 2012 PDFImad Mkanna100% (1)

- Kbyabd8p0p9c F9FM Monitoring Test 1A Questions s16 j17Document10 pagesKbyabd8p0p9c F9FM Monitoring Test 1A Questions s16 j17Hamed Al-RiyamiNo ratings yet

- Chapter 1.1 Introduction To Business Management. (Notes)Document7 pagesChapter 1.1 Introduction To Business Management. (Notes)S Ramesh100% (1)

- SEC Form 20-Is Definitive - 2015 - 0Document263 pagesSEC Form 20-Is Definitive - 2015 - 0Aeron Paul AntonioNo ratings yet

- Fixed Asset and Depreciation Schedule: Instructions: InputsDocument5 pagesFixed Asset and Depreciation Schedule: Instructions: InputsPatrick GhariosNo ratings yet

- ExercisesDocument3 pagesExercisesrhumblineNo ratings yet

- LendIt PDFDocument4 pagesLendIt PDFLuis GNo ratings yet

- Chap 016Document8 pagesChap 016Bobby MarionNo ratings yet

- HSBC Premier Savings Terms & Charges Disclosure: EligibilityDocument3 pagesHSBC Premier Savings Terms & Charges Disclosure: EligibilityAndi PrabowoNo ratings yet

- My CA Articleship Experience of Working at Deloitte (Big 4)Document5 pagesMy CA Articleship Experience of Working at Deloitte (Big 4)Rudrin Das100% (1)

- Statement of Financial Position Basic Problems Problem 1-1 (IFRS)Document18 pagesStatement of Financial Position Basic Problems Problem 1-1 (IFRS)student80% (5)

- Feven Engdawork Final PDFDocument57 pagesFeven Engdawork Final PDFNigussie BerhanuNo ratings yet

- Valuation of Tata SteelDocument3 pagesValuation of Tata SteelNishtha Mehra100% (1)

- Inclusive Growth With Disruptive Innovations: Gearing Up For Digital DisruptionDocument48 pagesInclusive Growth With Disruptive Innovations: Gearing Up For Digital DisruptionShashank YadavNo ratings yet

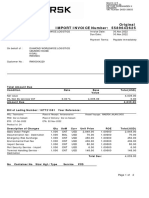

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- Ch14 Bonds - Intermediate 2Document103 pagesCh14 Bonds - Intermediate 2BLESSEDNo ratings yet

- Different Between Conventional Economics & Islamic EconomicsDocument1 pageDifferent Between Conventional Economics & Islamic EconomicsFieza Kyrana100% (2)

- Soal LatihanDocument1 pageSoal Latihanflypop13No ratings yet

- RETIREMENT & PENSION PLANNINGDocument25 pagesRETIREMENT & PENSION PLANNINGmyraNo ratings yet

- Annual Report of FAYSAL Bank Limited 2009Document129 pagesAnnual Report of FAYSAL Bank Limited 2009zabeehNo ratings yet

- Challenges For Foreign Banks Entering India Open New Opportunities For Consulting Firms PDFDocument11 pagesChallenges For Foreign Banks Entering India Open New Opportunities For Consulting Firms PDFTanu SinghNo ratings yet

- Investing Fundamentals: Stocks, Bonds, Mutual Funds and Home OwnershipDocument72 pagesInvesting Fundamentals: Stocks, Bonds, Mutual Funds and Home OwnershipMadeline PangilinanNo ratings yet

- Moving Average Guide Handout FinalDocument9 pagesMoving Average Guide Handout FinalSaurabh Jain100% (1)

- Evaluating A Firm's Financial PerformanceDocument47 pagesEvaluating A Firm's Financial PerformanceAhmed El KhateebNo ratings yet

- The Truth About MoneyDocument21 pagesThe Truth About MoneyTaha MirNo ratings yet

- Banking TSN 2018 2nd ExamDocument54 pagesBanking TSN 2018 2nd ExamAngel DeiparineNo ratings yet

- Taxau316 CSGDocument732 pagesTaxau316 CSGBb 8No ratings yet

- fm3 Chapter02Document165 pagesfm3 Chapter02catherinephilippouNo ratings yet

- Allen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Document317 pagesAllen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Stanford Victims CoalitionNo ratings yet

- Emmett T.J. Fibonacci Based Forecasts 1985Document4 pagesEmmett T.J. Fibonacci Based Forecasts 1985Om PrakashNo ratings yet