You might also like

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionFrom EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionRating: 5 out of 5 stars5/5 (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- FM Chapter 16Document16 pagesFM Chapter 16Nguyễn Hoàng Anh ThưNo ratings yet

- Business - Valuation - Modeling - Assessment FileDocument6 pagesBusiness - Valuation - Modeling - Assessment FileGowtham VananNo ratings yet

- Excel TopgloveDocument21 pagesExcel Topglovearil azharNo ratings yet

- AnswerDocument23 pagesAnswerYousaf BhuttaNo ratings yet

- Model 2 TDocument6 pagesModel 2 TVidhi PatelNo ratings yet

- César Iván Carranza A01334512 Fecha 2/6/2022 Tarea 5 Introducción A Las Finanzas CorporativasDocument12 pagesCésar Iván Carranza A01334512 Fecha 2/6/2022 Tarea 5 Introducción A Las Finanzas CorporativasCesar Ivan CarranzaNo ratings yet

- Financial Model 3 Statement Model - Final - MotilalDocument13 pagesFinancial Model 3 Statement Model - Final - MotilalSouvik BardhanNo ratings yet

- DCF Practice ProblemDocument4 pagesDCF Practice Problemshairel-joy marayagNo ratings yet

- Yates Financial ModellingDocument18 pagesYates Financial ModellingJerryJoshuaDiazNo ratings yet

- DCF Case Sample 1Document4 pagesDCF Case Sample 1Gaurav SethiNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Assignment ..Document5 pagesAssignment ..Mohd Saddam Saqlaini100% (1)

- DCF Model - Blank: Strictly ConfidentialDocument5 pagesDCF Model - Blank: Strictly ConfidentialaeqlehczeNo ratings yet

- DCF 2 CompletedDocument4 pagesDCF 2 CompletedPragathi T NNo ratings yet

- Financial Report - ShyamDocument14 pagesFinancial Report - ShyamYaswanth MaripiNo ratings yet

- Proyecto Final Eq. 3Document25 pagesProyecto Final Eq. 3Arath Eduardo Balcazar AntonioNo ratings yet

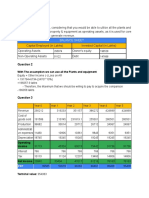

- Balance Sheet: With The Assumption We Can Use All The Plants and EquipmentDocument4 pagesBalance Sheet: With The Assumption We Can Use All The Plants and EquipmentPriadarshini Subramanyam DM21B093No ratings yet

- Naztech - 27.01.2021 - IrrDocument81 pagesNaztech - 27.01.2021 - IrrRashan Jida ReshanNo ratings yet

- DCF 3 CompletedDocument3 pagesDCF 3 CompletedPragathi T NNo ratings yet

- ST ND RD TH THDocument4 pagesST ND RD TH THSanam ShresthaNo ratings yet

- Module-10 Additional Material FSA Template - Session-11 vrTcbcH4leDocument6 pagesModule-10 Additional Material FSA Template - Session-11 vrTcbcH4leBhavya PatelNo ratings yet

- CFI 3 Statement Model Complete in ClassDocument10 pagesCFI 3 Statement Model Complete in ClassThiện NhânNo ratings yet

- Wipro Afm DataDocument5 pagesWipro Afm DataDevam DixitNo ratings yet

- 545 L2 (Projection of Income Statement, Balance Sheet and Cash Flow)Document10 pages545 L2 (Projection of Income Statement, Balance Sheet and Cash Flow)Äyušheë TŸagïNo ratings yet

- Finicial Model: Cost of Goods Sold (COGS)Document9 pagesFinicial Model: Cost of Goods Sold (COGS)Lawzy Elsadig SeddigNo ratings yet

- Yates Case Study - LT 11Document23 pagesYates Case Study - LT 11JerryJoshuaDiazNo ratings yet

- IFS Dividends IntroductionDocument2 pagesIFS Dividends IntroductionMohamedNo ratings yet

- 5 Cs of Credit - Caskey Trucking FinancialsDocument5 pages5 Cs of Credit - Caskey Trucking FinancialsHazem ElsherifNo ratings yet

- Base DataDocument10 pagesBase DataAKASH CHAUHANNo ratings yet

- ForecastingDocument9 pagesForecastingQuỳnh'ss Đắc'ssNo ratings yet

- Current Ratio: Current Liabilities Quick Ratio: Current LiabilitiesDocument4 pagesCurrent Ratio: Current Liabilities Quick Ratio: Current LiabilitiesAdityaSharmaNo ratings yet

- Balance Sheet - Subros: Optimistic Senario Normal ScenarioDocument9 pagesBalance Sheet - Subros: Optimistic Senario Normal ScenarioAnonymous tgYyno0w6No ratings yet

- Financial Ratio AnalysisDocument6 pagesFinancial Ratio AnalysisSatishNo ratings yet

- Loganathan Exp 5Document2 pagesLoganathan Exp 5loganathanloganathancNo ratings yet

- FMCG - Dabur 21BSP2557 Kasturi GhanekarDocument5 pagesFMCG - Dabur 21BSP2557 Kasturi GhanekarKUMARI MADHU LATANo ratings yet

- ENTI Ver 1Document72 pagesENTI Ver 1krishna chaitanyaNo ratings yet

- Recap: Profitability:ROE - Dupont Solvency Capital Employed DER Debt/TA Interest Coverage RatioDocument7 pagesRecap: Profitability:ROE - Dupont Solvency Capital Employed DER Debt/TA Interest Coverage RatioSiddharth PujariNo ratings yet

- Aamir Ali Bba Viii ADocument9 pagesAamir Ali Bba Viii Aaamir aliNo ratings yet

- Exhibit No.1 Toy World, Inc.'s Pro-Forma Balance Sheet Under Level Production, 1994 (Thousands of Dollars)Document5 pagesExhibit No.1 Toy World, Inc.'s Pro-Forma Balance Sheet Under Level Production, 1994 (Thousands of Dollars)Rohit Jhawar100% (2)

- Financial Ratio Analysis of HBLDocument23 pagesFinancial Ratio Analysis of HBLThapa Pramod92% (13)

- IFS - Simple Three Statement ModelDocument1 pageIFS - Simple Three Statement ModelThanh NguyenNo ratings yet

- Financial Statement AnalysisDocument25 pagesFinancial Statement AnalysisAldrin CustodioNo ratings yet

- Avenue SuperDocument19 pagesAvenue Superanuda29102001No ratings yet

- Beximco Pharmaceuticals LimitedDocument4 pagesBeximco Pharmaceuticals Limitedsamia0akter-228864No ratings yet

- Bemd RatiosDocument12 pagesBemd RatiosPRADEEP CHAVANNo ratings yet

- V MartDocument44 pagesV MartPankaj SankholiaNo ratings yet

- Income Statement Format (KTV) KTV KTVDocument30 pagesIncome Statement Format (KTV) KTV KTVDarlene Jade Butic VillanuevaNo ratings yet

- Itsa Excel SheetDocument7 pagesItsa Excel SheetraheelehsanNo ratings yet

- Sir Sarwar AFSDocument41 pagesSir Sarwar AFSawaischeemaNo ratings yet

- Gyaan SessionDocument25 pagesGyaan SessionVanshGuptaNo ratings yet

- New Microsoft Excel WorksheetDocument10 pagesNew Microsoft Excel WorksheetakbarNo ratings yet

- Interloop Limited Income Statement: Rupees in ThousandDocument13 pagesInterloop Limited Income Statement: Rupees in ThousandAsad AliNo ratings yet

- Working Capital Management - docx.PDF 20231102 130330 0000Document3 pagesWorking Capital Management - docx.PDF 20231102 130330 0000Aarti SharmaNo ratings yet

- Balance Sheet: Particulars 2014 2015 AssetsDocument11 pagesBalance Sheet: Particulars 2014 2015 AssetsTaiba SarmadNo ratings yet

- Exhibit in ExcelDocument8 pagesExhibit in ExcelAdrian WyssNo ratings yet

- QUIZ 2 Sufyan Sarwar 02-112192-060Document1 pageQUIZ 2 Sufyan Sarwar 02-112192-060Sufyan SarwarNo ratings yet

- CFI 3 Statement Model CompleteDocument14 pagesCFI 3 Statement Model CompleteMAYANK AGGARWALNo ratings yet

- LTCGDocument1 pageLTCGRahul SatyakamNo ratings yet

- 375 PaladinDocument2 pages375 Paladinabdirahman farah AbdiNo ratings yet

- Compilation 1 (Midterms)Document22 pagesCompilation 1 (Midterms)Von Andrei Medina100% (12)

- Financial Statement 2162Document126 pagesFinancial Statement 2162YOLA DWI YULANDARINo ratings yet

- Accounting DictionaryDocument5 pagesAccounting DictionaryShazad HassanNo ratings yet

- Understanding of Compulsorily Convertible Debentures Vinod KothariDocument7 pagesUnderstanding of Compulsorily Convertible Debentures Vinod KothariNazir kondkariNo ratings yet

- A Taxonomy of Brand Valuation Practice - Methodoligies and Purposes - bm.2009.14Document23 pagesA Taxonomy of Brand Valuation Practice - Methodoligies and Purposes - bm.2009.14Kd dentNo ratings yet

- Balance Sheet PreparationDocument34 pagesBalance Sheet PreparationShafi Marwat KhanNo ratings yet

- Kbyabd8p0p9c F9FM Monitoring Test 1A Questions s16 j17Document10 pagesKbyabd8p0p9c F9FM Monitoring Test 1A Questions s16 j17Hamed Al-RiyamiNo ratings yet

- Accounting P1 May-June 2021 EngDocument14 pagesAccounting P1 May-June 2021 EngdanNo ratings yet

- Final Exams PArCOr 2020Document4 pagesFinal Exams PArCOr 2020John Alfred CastinoNo ratings yet

- 2010 Yr 9 POA AnsDocument67 pages2010 Yr 9 POA AnsMuhammad SamhanNo ratings yet

- China's $2bn Football Buying Spree Has Fans Fearful of Result PDFDocument9 pagesChina's $2bn Football Buying Spree Has Fans Fearful of Result PDFKrSamarNo ratings yet

- Ias32 SN PDFDocument8 pagesIas32 SN PDFShiza ArifNo ratings yet

- Events After The Balance SheetDocument7 pagesEvents After The Balance SheetirvanNo ratings yet

- Capital StructureDocument55 pagesCapital Structurekartik avhadNo ratings yet

- The Statement of Financial Position of Ninety LTD For The Last Two Years AreDocument2 pagesThe Statement of Financial Position of Ninety LTD For The Last Two Years Arenjoroge mwangiNo ratings yet

- Introduccion CashFlowDocument28 pagesIntroduccion CashFlowMercedes Figueroa HilarioNo ratings yet

- Chapter 9Document14 pagesChapter 9Cindy permatasariNo ratings yet

- Module 2Document6 pagesModule 2Mary Joy CabilNo ratings yet

- CH 01Document53 pagesCH 01Ismadth2918388No ratings yet

- Finance UbiDocument36 pagesFinance UbiRanjeet RajputNo ratings yet

- Laporan Keuangan TELE Q3 2017Document112 pagesLaporan Keuangan TELE Q3 2017Hastrid Rina DewiNo ratings yet

- Module 3 Problems On Income StatementDocument8 pagesModule 3 Problems On Income StatementShruthi PNo ratings yet

- CS As A ValuerDocument67 pagesCS As A ValuerGAURAVNo ratings yet

- Analysis & Findings - GPDocument79 pagesAnalysis & Findings - GPFarhat987No ratings yet

- Valuation of Equity ShareDocument11 pagesValuation of Equity ShareSarthak SharmaNo ratings yet

- CPINDocument114 pagesCPINHelenaNo ratings yet

- What Is Financial Structure?Document3 pagesWhat Is Financial Structure?JNo ratings yet

- Financial Statement Analysis - Concept Questions and Solutions - Chapter 8Document30 pagesFinancial Statement Analysis - Concept Questions and Solutions - Chapter 8Arshdeep Singh50% (2)