You might also like

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Corporate Income TaxDocument70 pagesCorporate Income TaxNhung HồngNo ratings yet

- Chapter 3. Corporate Income TaxDocument90 pagesChapter 3. Corporate Income TaxVu Thi ThuongNo ratings yet

- Chapter 3. CITDocument57 pagesChapter 3. CITKhuất Thanh HuếNo ratings yet

- VAT, WHT and CIT SummaryDocument8 pagesVAT, WHT and CIT Summarymariko1234No ratings yet

- Corporate - Income - Tax (CIT) 2022Document44 pagesCorporate - Income - Tax (CIT) 2022Thảo Nhi Đinh TrầnNo ratings yet

- MOF Circular 134-2008 ForeignCtr Tax Summary (En)Document4 pagesMOF Circular 134-2008 ForeignCtr Tax Summary (En)quangpqNo ratings yet

- HANDOUT FOR VAT-NewDocument25 pagesHANDOUT FOR VAT-NewCristian RenatusNo ratings yet

- Report of Law1 - Other Percentage TaxDocument16 pagesReport of Law1 - Other Percentage TaxJonalyn Maraña-ManuelNo ratings yet

- Tax 5Document88 pagesTax 5Thái Minh ChâuNo ratings yet

- Value Added Tax ActDocument18 pagesValue Added Tax ActStephen Amobi OkoronkwoNo ratings yet

- PWC Vietnam Pocket Tax Book 2013Document43 pagesPWC Vietnam Pocket Tax Book 2013Angie NguyenNo ratings yet

- VAT Other Aspects - January 2024Document5 pagesVAT Other Aspects - January 2024Charisma CharlesNo ratings yet

- PWC Vietnam Pocket Tax Book 2014 enDocument27 pagesPWC Vietnam Pocket Tax Book 2014 entieuquan42No ratings yet

- On Taxation and About Form 16Document21 pagesOn Taxation and About Form 16Kawalpreet Singh MakkarNo ratings yet

- Chapt-2 Taxation - Source of Public RevenueDocument26 pagesChapt-2 Taxation - Source of Public RevenueYitera SisayNo ratings yet

- TAXATION - Value-Added TaxDocument10 pagesTAXATION - Value-Added TaxJohn Mahatma Agripa100% (2)

- Gross Income Deductions - Lecture Handout PDFDocument4 pagesGross Income Deductions - Lecture Handout PDFKarl RendonNo ratings yet

- Vol7 - No2.pdf.. TaxationDocument6 pagesVol7 - No2.pdf.. TaxationReyboom BautistaNo ratings yet

- Value Added Tax - VatDocument37 pagesValue Added Tax - VatTimoth MbwiloNo ratings yet

- Cambodia Other Corporate TaxesDocument5 pagesCambodia Other Corporate TaxesJanNo ratings yet

- Value Added TaxDocument23 pagesValue Added Taxnjuafac donatusNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- Group Members:: Basit Ali (326) Faizan Khalid (348) Adnan SiddiqueDocument9 pagesGroup Members:: Basit Ali (326) Faizan Khalid (348) Adnan Siddiqueiza khanNo ratings yet

- Other Income Tax AccountingDocument19 pagesOther Income Tax AccountingHabtamu Hailemariam AsfawNo ratings yet

- Defășurarea Afacerii În RomaniaDocument17 pagesDefășurarea Afacerii În RomaniaAnda PopaNo ratings yet

- TaxDocument11 pagesTaxmnoor13245mnNo ratings yet

- Transfer and Business Taxation: Module WritersDocument129 pagesTransfer and Business Taxation: Module WritersPaulita GomezNo ratings yet

- Ad TaxDocument64 pagesAd TaxNiyitegeka EricNo ratings yet

- VAT Basics - July 2023Document8 pagesVAT Basics - July 2023maharajabby81No ratings yet

- UP Nepal Tax FeeDocument7 pagesUP Nepal Tax FeeAnil ShahNo ratings yet

- Lecture 1: Moldovan Versus International Tax Payment OptimizationDocument13 pagesLecture 1: Moldovan Versus International Tax Payment OptimizationIon CaraNo ratings yet

- Taxation ProjectDocument14 pagesTaxation ProjectrahulkoduvanNo ratings yet

- 2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFDocument18 pages2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFtendaicrosby100% (1)

- EY Tax Watch Update English August 2012Document7 pagesEY Tax Watch Update English August 2012KyleRodSimpsonNo ratings yet

- Withholding Tax Rates MalawiDocument2 pagesWithholding Tax Rates Malawianraomca100% (1)

- Case Study - Chapter 1 2 3 4 - 2Document5 pagesCase Study - Chapter 1 2 3 4 - 2Lê Ngọc Vân NhiNo ratings yet

- Deductible ExpenseDocument26 pagesDeductible ExpenseBuniNo ratings yet

- Tax - AccountingDocument9 pagesTax - AccountingAn NguyenNo ratings yet

- TaxDocument6 pagesTaxKhánh LinhNo ratings yet

- Taxation Laws On QweDocument28 pagesTaxation Laws On QweRomani Noel S. Chavez Jr.No ratings yet

- Tax - Vat GuidenotesDocument13 pagesTax - Vat GuidenotesNardz AndananNo ratings yet

- Guide To Tanzania Taxation SystemDocument3 pagesGuide To Tanzania Taxation Systemhima100% (1)

- Cambodian 2018 Tax Booklet: A Summary of Cambodian TaxationDocument26 pagesCambodian 2018 Tax Booklet: A Summary of Cambodian TaxationLee XingNo ratings yet

- VAT Road To GSTDocument19 pagesVAT Road To GSTVarun PuriNo ratings yet

- Business Tax ReviewerDocument22 pagesBusiness Tax ReviewereysiNo ratings yet

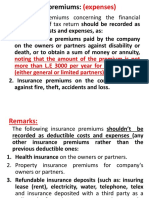

- Insurance Premiums Concerning The Financial (Fiscal) Year of Tax ReturnDocument30 pagesInsurance Premiums Concerning The Financial (Fiscal) Year of Tax ReturnBeshoyIsaacSaadNo ratings yet

- TaxLegalGuide CorporateIncomeTax 053011Document12 pagesTaxLegalGuide CorporateIncomeTax 053011Raluca GabrielNo ratings yet

- Module 4 - Value Added TaxDocument16 pagesModule 4 - Value Added Taxanon_455551365No ratings yet

- Value Added Tax in Romania VAT TVADocument6 pagesValue Added Tax in Romania VAT TVAmondlyNo ratings yet

- HK IRD Tax GuideDocument34 pagesHK IRD Tax GuideAlex LimNo ratings yet

- Administration of Value Added Tax-VatDocument13 pagesAdministration of Value Added Tax-VatRuth NyawiraNo ratings yet

- VatDocument37 pagesVatBảo BờmNo ratings yet

- Saudi Jan2010Document8 pagesSaudi Jan2010Shawkat AbbasNo ratings yet

- Notes On VATDocument15 pagesNotes On VATErnest Benz Sabella DavilaNo ratings yet

- Valuation - : Concepts and CasesDocument3 pagesValuation - : Concepts and Casesjonnajon92No ratings yet

- Tax System in ArgentinaDocument13 pagesTax System in ArgentinaSimon VotteroNo ratings yet

- Business Tax in Viet NamDocument3 pagesBusiness Tax in Viet NamLinh ĐỗNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Kido Group's DepartmentDocument2 pagesKido Group's Department36. Lê Minh Phương 12A3No ratings yet

- Business Statistics: LecturerDocument37 pagesBusiness Statistics: Lecturer36. Lê Minh Phương 12A3No ratings yet

- Chapter 7Document20 pagesChapter 736. Lê Minh Phương 12A3No ratings yet

- Chapter 5Document40 pagesChapter 536. Lê Minh Phương 12A3No ratings yet

- Vegan Leather - An Idea in EntrepreneurshipDocument3 pagesVegan Leather - An Idea in Entrepreneurship36. Lê Minh Phương 12A3No ratings yet

- Chapter 4.spDocument66 pagesChapter 4.sp36. Lê Minh Phương 12A3No ratings yet

- Chapter 3Document41 pagesChapter 336. Lê Minh Phương 12A3No ratings yet

- Chapter 2. Presenting Data in Tables and Charts: ObjectivesDocument44 pagesChapter 2. Presenting Data in Tables and Charts: Objectives36. Lê Minh Phương 12A3No ratings yet

- Time Series and Forecasting: ObjectivesDocument55 pagesTime Series and Forecasting: Objectives36. Lê Minh Phương 12A3No ratings yet

- ProbStat Lec07 MineDocument25 pagesProbStat Lec07 Mine36. Lê Minh Phương 12A3No ratings yet

- ProbStat Lec10 MineDocument21 pagesProbStat Lec10 Mine36. Lê Minh Phương 12A3No ratings yet

- ProbStat Lec08 MineDocument22 pagesProbStat Lec08 Mine36. Lê Minh Phương 12A3No ratings yet

- ProbStat Lec09 MineDocument24 pagesProbStat Lec09 Mine36. Lê Minh Phương 12A3No ratings yet

- Assignment of Financial ManagementDocument7 pagesAssignment of Financial ManagementPRACHI DASNo ratings yet

- RFBT-05 Atty. Capuno Corporations Atty. Villegas: C. Appraisal RightDocument5 pagesRFBT-05 Atty. Capuno Corporations Atty. Villegas: C. Appraisal RightSean SanchezNo ratings yet

- Module 1 - Canvas SlidesDocument40 pagesModule 1 - Canvas SlidesAniKelbakianiNo ratings yet

- HRM - AskaribankDocument21 pagesHRM - Askaribankhamidmalik-10% (1)

- Financial Performance MeasureDocument2 pagesFinancial Performance MeasureMeghan Kaye LiwenNo ratings yet

- Steel NewsDocument32 pagesSteel NewsMoez MoezNo ratings yet

- Employee Master File Creation FormDocument4 pagesEmployee Master File Creation Formmuhammad younasNo ratings yet

- Ratio Analysis and Interpretation 8Document24 pagesRatio Analysis and Interpretation 8Shierwin Ebcas JavierNo ratings yet

- Annual Report 2015 16 PDFDocument132 pagesAnnual Report 2015 16 PDFVickesh MalkaniNo ratings yet

- Axis Offer Latter For SalariedDocument4 pagesAxis Offer Latter For Salariedyoursmanish8312No ratings yet

- Unit - 2 IllustrationsDocument2 pagesUnit - 2 IllustrationsRakesh SriNo ratings yet

- Income Tax ProblemsDocument6 pagesIncome Tax Problemskristian eldric BondocNo ratings yet

- Appointment - LetterDocument3 pagesAppointment - LetteraarifNo ratings yet

- Testbank - Multinational Business Finance - Chapter 12Document15 pagesTestbank - Multinational Business Finance - Chapter 12Uyen Nhi NguyenNo ratings yet

- Tata Motors European Technical Centre PLCDocument27 pagesTata Motors European Technical Centre PLCDhruv Singh GosainNo ratings yet

- Revolut LTD Annual Report YE 2020Document81 pagesRevolut LTD Annual Report YE 2020ForkLogNo ratings yet

- chp03 CevapDocument3 pageschp03 CevapSundus AshrafNo ratings yet

- P&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValueDocument66 pagesP&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValuePrabhdeep DadyalNo ratings yet

- PARTNERSHIP - 2nd Outline - Page 4-6Document4 pagesPARTNERSHIP - 2nd Outline - Page 4-6EsraRamosNo ratings yet

- The Business Strategy Game: Overview and OrientationDocument28 pagesThe Business Strategy Game: Overview and OrientationGangelNo ratings yet

- INDEMNITYDocument8 pagesINDEMNITYGaurav JindalNo ratings yet

- RoutingNo Bank USADocument224 pagesRoutingNo Bank USAWadnerson Boileau100% (1)

- Public Utility Entity Is Not Allowed To Use The Pfrs For Smes in The Philippines)Document6 pagesPublic Utility Entity Is Not Allowed To Use The Pfrs For Smes in The Philippines)Glen JavellanaNo ratings yet

- Financial Accounting Past Present and FutureDocument10 pagesFinancial Accounting Past Present and Futuresudarjanto100% (1)

- The Interaction of Contract Law and Tort and Property Law in Europe A Comparative StudyDocument574 pagesThe Interaction of Contract Law and Tort and Property Law in Europe A Comparative StudyIrma Rahmanisa75% (4)

- New Functionality in s4/HANA Simple FinanceDocument29 pagesNew Functionality in s4/HANA Simple Financeeason insightsNo ratings yet

- Handbook of Supply Chain 02Document8 pagesHandbook of Supply Chain 02JoyceNo ratings yet

- SCDL BusinessLaw Assignment Oct20Document9 pagesSCDL BusinessLaw Assignment Oct20priyajeejo100% (1)

- 4th Sem Project-Converted (3) 18mba06Document63 pages4th Sem Project-Converted (3) 18mba06seema malik100% (1)

- Workbook PDFDocument116 pagesWorkbook PDFSuvodeep GhoshNo ratings yet