You might also like

- CF 4Document49 pagesCF 4Siddhartha SharmaNo ratings yet

- Lecture Bond MGT StrategyDocument25 pagesLecture Bond MGT StrategyKapil SharmaNo ratings yet

- CF 6Document19 pagesCF 6Siddhartha SharmaNo ratings yet

- Valcom - Chmsc.module 3 - Bond ValuationDocument5 pagesValcom - Chmsc.module 3 - Bond ValuationChristopher ApaniNo ratings yet

- The Analysis and Valuation of Bonds: Answers To QuestionsDocument4 pagesThe Analysis and Valuation of Bonds: Answers To QuestionsIsmat Jerin ChetonaNo ratings yet

- Bonds ValuationsDocument57 pagesBonds ValuationsarmailgmNo ratings yet

- F303 - Intermediate Investments: Interest Rate Sensitivity and Bond DurationDocument19 pagesF303 - Intermediate Investments: Interest Rate Sensitivity and Bond Durationhussain_nNo ratings yet

- Chapter 009Document33 pagesChapter 009AfnanNo ratings yet

- ch9 Solutions PDFDocument38 pagesch9 Solutions PDFHussnain NaneNo ratings yet

- Financial Institutions Management A Risk Management Approach 9th Edition Saunders Solutions ManualDocument40 pagesFinancial Institutions Management A Risk Management Approach 9th Edition Saunders Solutions Manualsyeniticbitts2y47j9100% (18)

- Case Mexico City - Grupo 3Document141 pagesCase Mexico City - Grupo 3Brisa LinaresNo ratings yet

- A Note On DurationDocument3 pagesA Note On Durationpriyank0407No ratings yet

- Valuation of BondsDocument27 pagesValuation of BondsAbhinav Rajverma100% (1)

- Measuring Interest-Rate Risk with DurationDocument7 pagesMeasuring Interest-Rate Risk with DurationArif AhmedNo ratings yet

- Chap 009Document39 pagesChap 009Shahrukh Mushtaq0% (1)

- You Have To Answer Each Section Separately, Handwritten Submission Shall Be PenalisedDocument6 pagesYou Have To Answer Each Section Separately, Handwritten Submission Shall Be PenalisedDavid ViksarNo ratings yet

- Financial Institutions Management A Risk Management Approach 8th Edition Saunders Solutions ManualDocument43 pagesFinancial Institutions Management A Risk Management Approach 8th Edition Saunders Solutions Manualfinntrangoxgu100% (21)

- BOND PORTFOLIO MANAGEMENT TACTICSDocument41 pagesBOND PORTFOLIO MANAGEMENT TACTICSvaibhavNo ratings yet

- Revision Exercise 2 - Int Rates + Capl Budgeting - SolutionsDocument25 pagesRevision Exercise 2 - Int Rates + Capl Budgeting - SolutionsBaher WilliamNo ratings yet

- Lecture 7 BH CH 7 Bond and ValuationDocument41 pagesLecture 7 BH CH 7 Bond and ValuationAydin GaniyevNo ratings yet

- Valuation of DebenturesDocument28 pagesValuation of DebenturesharmitkNo ratings yet

- Chapter 6 - Valuation of BondsDocument38 pagesChapter 6 - Valuation of BondsMalNo ratings yet

- Darren FIXED INCOMEDocument31 pagesDarren FIXED INCOMEAzadNo ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument37 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskVidhi DoshiNo ratings yet

- Bond ValuationDocument29 pagesBond ValuationNur Al AhadNo ratings yet

- FINE230 Chap 2 - BondsDocument12 pagesFINE230 Chap 2 - BondsMandy KhouryNo ratings yet

- Duration Convexity Bond Portfolio ManagementDocument49 pagesDuration Convexity Bond Portfolio ManagementParijatVikramSingh100% (1)

- Risk Management Chap 9 Interest Risk II MODDocument52 pagesRisk Management Chap 9 Interest Risk II MODYasser MishalNo ratings yet

- FOFA - Session 7-8 - 2023-24Document24 pagesFOFA - Session 7-8 - 2023-24rishit0504No ratings yet

- Chapter 5: Bond: BY: PN Azlida Binti AbdullahDocument44 pagesChapter 5: Bond: BY: PN Azlida Binti Abdullahazlida abdullahNo ratings yet

- Financial Management Assignment 6 Fixed Investment Management Submitted By-Faisal Ishaq B17079 Case BackgroundDocument6 pagesFinancial Management Assignment 6 Fixed Investment Management Submitted By-Faisal Ishaq B17079 Case BackgroundfaisalNo ratings yet

- Debt ValuationDocument30 pagesDebt ValuationSiddharth BirjeNo ratings yet

- Reading 43 - Risk and ReturnDocument24 pagesReading 43 - Risk and Returnshaili shahNo ratings yet

- Chapter 12 Bond Portfolio MGMTDocument41 pagesChapter 12 Bond Portfolio MGMTsharktale2828No ratings yet

- Fixed Income Chapter4Document51 pagesFixed Income Chapter4Sourabh pathakNo ratings yet

- Duration, Convexity & ImmunizationDocument120 pagesDuration, Convexity & ImmunizationSumit SinghNo ratings yet

- Valuation and Pricing of BondsDocument43 pagesValuation and Pricing of BondsSiddhartha PatraNo ratings yet

- FINC2011 Tutorial 4Document7 pagesFINC2011 Tutorial 4suitup100100% (3)

- Document Name Bond Math Version Number V1 Approved by Marisha Purohit Approval Date 03/05/2020 Creator Audience Students/Faculty/ManagementDocument20 pagesDocument Name Bond Math Version Number V1 Approved by Marisha Purohit Approval Date 03/05/2020 Creator Audience Students/Faculty/ManagementRavindra A. KamathNo ratings yet

- Bond Duration 2Document9 pagesBond Duration 2Mian Qamar Ul ZamanNo ratings yet

- FM Handout 3Document23 pagesFM Handout 3Rofiq VedcNo ratings yet

- Chap 9 Interest Rate Risk IIDocument123 pagesChap 9 Interest Rate Risk IIAfnan100% (3)

- Fins 2624 Problem Set 3 SolutionDocument11 pagesFins 2624 Problem Set 3 SolutionUnswlegend100% (2)

- Financial Derivatives: Prof. Scott JoslinDocument44 pagesFinancial Derivatives: Prof. Scott JoslinarnavNo ratings yet

- Chapter 7. Bonds and Their Valuation: A B C D E F G H I 1 2 3 4Document13 pagesChapter 7. Bonds and Their Valuation: A B C D E F G H I 1 2 3 4Naufal IhsanNo ratings yet

- R54-Understanding FI Risk and ReturnDocument37 pagesR54-Understanding FI Risk and ReturnBad AnikiNo ratings yet

- Interest RatesDocument28 pagesInterest RatesFirly IrhamniNo ratings yet

- Bond Valuation: Bond Analysis: Returns & Systematic RiskDocument50 pagesBond Valuation: Bond Analysis: Returns & Systematic RiskSamad KhanNo ratings yet

- AoF Tutorial02 SpotDocument3 pagesAoF Tutorial02 SpotSeebsNo ratings yet

- BMA - 12e - SM - CH - 03 - Final (AutoRecovered)Document16 pagesBMA - 12e - SM - CH - 03 - Final (AutoRecovered)Aalo M ChakrabortyNo ratings yet

- Calculate Bond Yields, Prices and DurationsDocument9 pagesCalculate Bond Yields, Prices and DurationsDebashis MallickNo ratings yet

- Bond Mathemetics BasicsDocument133 pagesBond Mathemetics BasicsHarshit DwivediNo ratings yet

- Tutorial 5 AnswerDocument5 pagesTutorial 5 AnswerSyuhaidah Binti Aziz ZudinNo ratings yet

- Civil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InterestDocument14 pagesCivil Engineering Construction and Graphics QUIZ#02 Topic:: Difference Between Simple and Compound InteresttayyabNo ratings yet

- Bond Market Maths: Group Members Swarana Biyani - 01 Sanket Desai - 02 Rohan Jadhav - 08 Shama Lonare - 14Document74 pagesBond Market Maths: Group Members Swarana Biyani - 01 Sanket Desai - 02 Rohan Jadhav - 08 Shama Lonare - 14Namrata KolteNo ratings yet

- Chapter 7: Interest Rates and Bond ValuationDocument36 pagesChapter 7: Interest Rates and Bond ValuationHins LeeNo ratings yet

- Lect7-2023Document94 pagesLect7-2023vitordias347No ratings yet

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2From EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2No ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Greendust: Revolutionizing The Returns Process: All Currency Amounts Are in U.S. DollarsDocument10 pagesGreendust: Revolutionizing The Returns Process: All Currency Amounts Are in U.S. DollarsvitrahulNo ratings yet

- Afklm Financial Statements Notes December 31 2020Document107 pagesAfklm Financial Statements Notes December 31 2020Siddhartha SharmaNo ratings yet

- Group-4 HRMDocument13 pagesGroup-4 HRMSiddhartha SharmaNo ratings yet

- Mahindra Finance ServicesDocument16 pagesMahindra Finance ServicesShravan Hegde100% (1)

- Group02 - HRM - Pulse SurveyDocument9 pagesGroup02 - HRM - Pulse SurveySiddhartha SharmaNo ratings yet

- 66 ProductDocument4 pages66 ProductSiddhartha SharmaNo ratings yet

- The Income StatementDocument10 pagesThe Income Statementayoub mechouatNo ratings yet

- Survey of Accounting 7th Edition Warren Test BankDocument27 pagesSurvey of Accounting 7th Edition Warren Test Bankdevinsmithddsfzmioybeqr100% (13)

- INSTRUMENTSDocument41 pagesINSTRUMENTS微微No ratings yet

- Important Questions For CBSE Class 12 Business Studies Chapter 9Document12 pagesImportant Questions For CBSE Class 12 Business Studies Chapter 9Smita SrivastavaNo ratings yet

- IAS 16 Problem SolutionsDocument2 pagesIAS 16 Problem SolutionsRimsha ArifNo ratings yet

- FAR Final Preboard SolutionsDocument6 pagesFAR Final Preboard SolutionsVillanueva, Mariella De VeraNo ratings yet

- Accounting p2 QP Gr12 Sept 2023 - EnglishDocument11 pagesAccounting p2 QP Gr12 Sept 2023 - Englishbrandon.tabaneNo ratings yet

- Financial Analysis Report of Marks and Spencer Group Plc 2021-2023Document17 pagesFinancial Analysis Report of Marks and Spencer Group Plc 2021-2023sadathamid03No ratings yet

- MCQ Ratio AnalysisDocument56 pagesMCQ Ratio Analysiskanakchauhan206No ratings yet

- 5.1. Ind AS 36Document30 pages5.1. Ind AS 36Ajay JangirNo ratings yet

- BIMB Vs BSN PDFDocument10 pagesBIMB Vs BSN PDFIelts TutorNo ratings yet

- Bài kiểm tra buổi 5 - Xem lại bài làmDocument4 pagesBài kiểm tra buổi 5 - Xem lại bài làmBảo KhangNo ratings yet

- L2 - Business Combinations II (2023)Document12 pagesL2 - Business Combinations II (2023)waiwaichoi112No ratings yet

- Stocks Assign.Document3 pagesStocks Assign.MR / Mohamed Hussein GhzaliNo ratings yet

- AP.3408 Audit of EquityDocument4 pagesAP.3408 Audit of EquityMonica GarciaNo ratings yet

- ĐỀ-kiểm tra tacn2 hvtc Học viện tài chínhDocument7 pagesĐỀ-kiểm tra tacn2 hvtc Học viện tài chínhMinh Anh NguyenNo ratings yet

- Bcoe 143 1Document1 pageBcoe 143 1ACS DersNo ratings yet

- Selection and Hierarchical Evaluation of Simple Investment Projects: NPV and IrrDocument24 pagesSelection and Hierarchical Evaluation of Simple Investment Projects: NPV and IrrFeenyxNo ratings yet

- 1.3) Accounting StandardsDocument15 pages1.3) Accounting StandardsF93 SHIFA KHANNo ratings yet

- Commercial and Taxation Law Past Bar QAs 2005 2022Document154 pagesCommercial and Taxation Law Past Bar QAs 2005 2022Dannah Louise Bonifacio100% (1)

- Accountancy Project Roll No. 19-24Document25 pagesAccountancy Project Roll No. 19-24Diya DileepNo ratings yet

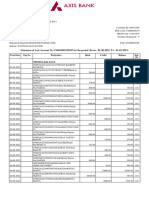

- Statement of Axis Account No:916010041539247 For The Period (From: 01-08-2022 To: 01-02-2023)Document18 pagesStatement of Axis Account No:916010041539247 For The Period (From: 01-08-2022 To: 01-02-2023)rahulbhasinNo ratings yet

- Financial Management Notebook 1Document14 pagesFinancial Management Notebook 1ngocmytrieuNo ratings yet

- Ap 400Document10 pagesAp 400Christine Jane AbangNo ratings yet

- TCDNDocument345 pagesTCDNAnh Thư PhạmNo ratings yet

- Module 2 Balance SheetsDocument26 pagesModule 2 Balance SheetsJecel Mahusay PuertoNo ratings yet

- 120 Keough V St. Paul Milk CoDocument2 pages120 Keough V St. Paul Milk CoJai HoNo ratings yet

- Lat TakeDocument8 pagesLat TakeCamila Gail GumbanNo ratings yet

- 73535bos59345 Final p2qDocument6 pages73535bos59345 Final p2qSakshi vermaNo ratings yet

- FOREXDocument5 pagesFOREXendouusaNo ratings yet