You might also like

- Shrewsbury Herbal Products, LTDDocument1 pageShrewsbury Herbal Products, LTDWulandari Pramithasari0% (1)

- Gitman pmf13 ppt05Document79 pagesGitman pmf13 ppt05moonaafreenNo ratings yet

- M05 Gitman50803X 14 MF C05Document61 pagesM05 Gitman50803X 14 MF C05layan123456No ratings yet

- Materi TVM 1 Dan TVM 2 PDFDocument73 pagesMateri TVM 1 Dan TVM 2 PDFamirah muthiaNo ratings yet

- Week 2A - Time Value of MoneyDocument48 pagesWeek 2A - Time Value of MoneyWgp 87100No ratings yet

- CHP 5Document72 pagesCHP 5Khaled A. M. El-sherifNo ratings yet

- Time Value of Money 1Document46 pagesTime Value of Money 1Aaron ManalastasNo ratings yet

- Time Value of Money: All Rights ReservedDocument50 pagesTime Value of Money: All Rights ReservedHasib NaheenNo ratings yet

- Tvom 1Document82 pagesTvom 1Jennifer KhoNo ratings yet

- Chapter 5Document72 pagesChapter 5NEW TECK INFINITYNo ratings yet

- Time Value of MoneyDocument49 pagesTime Value of MoneyThenappan GanesenNo ratings yet

- Time Value of Money: All Rights ReservedDocument55 pagesTime Value of Money: All Rights Reservedjaz hoodNo ratings yet

- Chapter 5 - Time Value of Money - RevisedDocument53 pagesChapter 5 - Time Value of Money - RevisedMahbuba RahmanNo ratings yet

- Fin 254 - Chapter 5 CorrectedDocument61 pagesFin 254 - Chapter 5 CorrectedsajedulNo ratings yet

- CH 5 Time Value of MoneyDocument94 pagesCH 5 Time Value of MoneyTarannum TahsinNo ratings yet

- CH 5-Time Value of Money-Gitman - pmf13 - ppt05 GeDocument94 pagesCH 5-Time Value of Money-Gitman - pmf13 - ppt05 Gekim taehyung100% (1)

- Time Value of Money NotesDocument95 pagesTime Value of Money NotesGabriel Trinidad SonielNo ratings yet

- Time ValueDocument43 pagesTime ValueJaneNo ratings yet

- Time Value of Money: All Rights ReservedDocument94 pagesTime Value of Money: All Rights Reservedjcgaide3No ratings yet

- BWFF2033 - Topic 5 - Time Value of Money - Part 1Document17 pagesBWFF2033 - Topic 5 - Time Value of Money - Part 1ZiaNaPiramLiNo ratings yet

- BWFF2033 - Topic 5 - Time Value of Money - Part 2Document30 pagesBWFF2033 - Topic 5 - Time Value of Money - Part 2ZiaNaPiramLiNo ratings yet

- Fin254 Ch05 NNH TVM UpdatedDocument80 pagesFin254 Ch05 NNH TVM Updatedamir khanNo ratings yet

- Time Value of Money: All Rights ReservedDocument23 pagesTime Value of Money: All Rights ReservedAnonymous f7wV1lQKRNo ratings yet

- Time Value of MoneyDocument60 pagesTime Value of MoneyZain AbbasNo ratings yet

- Chapter 05 SlidesDocument70 pagesChapter 05 Slidesbebo7usaNo ratings yet

- Time Value of Money-PowerpointDocument83 pagesTime Value of Money-Powerpointhaljordan313No ratings yet

- Finance and Management Accounting 2 Week 2Document29 pagesFinance and Management Accounting 2 Week 2565961628No ratings yet

- 4-Time Value of MoneyDocument35 pages4-Time Value of Moneysherif_awad100% (1)

- Chapter 3 Time Value of MoneyDocument163 pagesChapter 3 Time Value of MoneyMoieenNo ratings yet

- Chapter One - Time Value of Money-1-29 Part OneDocument29 pagesChapter One - Time Value of Money-1-29 Part OnesamicoNo ratings yet

- The Time Value of Money: All Rights ReservedDocument29 pagesThe Time Value of Money: All Rights ReservednikowawaNo ratings yet

- Chapter 4Document50 pagesChapter 422GayeonNo ratings yet

- CH 5 Time Value of Money Long VersionDocument147 pagesCH 5 Time Value of Money Long Versionalmandouh.mustafa.khaledNo ratings yet

- Chapter 5Document35 pagesChapter 5Ahmed El KhateebNo ratings yet

- Week 4 (Lecture 4) : The Time Value of Money: Effective Annual Rate, Annuities & PerpetuitiesDocument39 pagesWeek 4 (Lecture 4) : The Time Value of Money: Effective Annual Rate, Annuities & PerpetuitiesIsaac NahNo ratings yet

- FM TheoryDocument55 pagesFM TheoryDAHIWALE SANJIVNo ratings yet

- Chapter 02Document4 pagesChapter 02Gautam DNo ratings yet

- Time Value of MoneyDocument10 pagesTime Value of MoneyMary Ann MarianoNo ratings yet

- CH 05Document40 pagesCH 05saeed75.ksaNo ratings yet

- Time Value of Money: All Rights ReservedDocument79 pagesTime Value of Money: All Rights ReservedBilal SahuNo ratings yet

- Muhammad Shoaib Sajjad: The Time Value of MoneyDocument47 pagesMuhammad Shoaib Sajjad: The Time Value of MoneyMuhammad MudassarNo ratings yet

- The Time Value of Money: Topic 3Document35 pagesThe Time Value of Money: Topic 3lazycat1703No ratings yet

- Chapter 2 Time Value of Money Edited (Student)Document20 pagesChapter 2 Time Value of Money Edited (Student)Nguyễn Thái Minh ThưNo ratings yet

- FInMan Chapter 1Document4 pagesFInMan Chapter 1foracademicfiles.01No ratings yet

- Time Value of MoneyDocument27 pagesTime Value of MoneyJessicaNo ratings yet

- Time Value of Money: All Rights ReservedDocument43 pagesTime Value of Money: All Rights ReservedAnonymous f7wV1lQKRNo ratings yet

- C05 06Document40 pagesC05 06Sankar RanjanNo ratings yet

- Concept of Value and Return Question and AnswerDocument4 pagesConcept of Value and Return Question and Answervinesh1515No ratings yet

- SessionDocument111 pagesSessionvidyadhar16No ratings yet

- 05 Zutter Smart MFBrief 15e ch05Document140 pages05 Zutter Smart MFBrief 15e ch05zainal arifinNo ratings yet

- Principles of Managerial Finance: Fifteenth Edition, Global EditionDocument151 pagesPrinciples of Managerial Finance: Fifteenth Edition, Global EditionMustafa VaranNo ratings yet

- TVM 2 Annuities PV FV 2Document20 pagesTVM 2 Annuities PV FV 2Sam Sep A SixtyoneNo ratings yet

- Chap 6Document65 pagesChap 6ahmad altoufailyNo ratings yet

- Brooks 3e PPT 05Document40 pagesBrooks 3e PPT 05Vy HoàngNo ratings yet

- YuiDocument5 pagesYuiPramod kNo ratings yet

- Lecture 4Document89 pagesLecture 4Lee Li HengNo ratings yet

- CF Lecture 2 Time Value of Money v1Document50 pagesCF Lecture 2 Time Value of Money v1Tâm NhưNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- BAI File Format ExplanationDocument12 pagesBAI File Format ExplanationThatra K ChariNo ratings yet

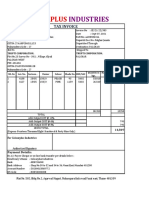

- Colourplus GST Invoice - 2020-2021 - TruptiDocument1 pageColourplus GST Invoice - 2020-2021 - TruptiSRJOFFICIAL7No ratings yet

- Valuation Practice QuizDocument6 pagesValuation Practice QuizSana KhanNo ratings yet

- Chapter 15 PPT - Holthausen & Zmijewski 2019Document100 pagesChapter 15 PPT - Holthausen & Zmijewski 2019royNo ratings yet

- Key Fact Sheett (HBL CarLoan) - July 2017Document1 pageKey Fact Sheett (HBL CarLoan) - July 2017Muhammad Ahmad MustafaNo ratings yet

- ITC SME Trade Academy - Post-Course Knowledge QuizDocument11 pagesITC SME Trade Academy - Post-Course Knowledge QuizUlul AzmiNo ratings yet

- 04 Subjective / Subjektif 2: Format Latihan: Subjektif. Tiada Sistem Pemarkahan, Contoh Jawapan DiberikanDocument16 pages04 Subjective / Subjektif 2: Format Latihan: Subjektif. Tiada Sistem Pemarkahan, Contoh Jawapan Diberikanforyourhonour wongNo ratings yet

- C2 Bank ReconciliationDocument22 pagesC2 Bank ReconciliationKenzel lawasNo ratings yet

- Financing The Venture: Week15 - Enmgmt1Document23 pagesFinancing The Venture: Week15 - Enmgmt1Shaira PunayNo ratings yet

- Stock - Practice QuestionsDocument1 pageStock - Practice QuestionsWaylee CheroNo ratings yet

- Complete POA SummaryDocument38 pagesComplete POA SummaryZara HazirahNo ratings yet

- Latih Soal Untuk Mhs Fin MGTDocument13 pagesLatih Soal Untuk Mhs Fin MGTnajNo ratings yet

- Main ReportDocument63 pagesMain ReportMOhibul Islam LimonNo ratings yet

- Internet BillDocument4 pagesInternet BillKanchan Asnani0% (1)

- Chapter 11 - Sources of CapitalDocument21 pagesChapter 11 - Sources of CapitalArman100% (1)

- F5 o VIGDj 8 Tpus IVDocument4 pagesF5 o VIGDj 8 Tpus IVThirupathi KotteNo ratings yet

- PMC Bank FraudDocument9 pagesPMC Bank FraudRaghav MittalNo ratings yet

- Money and Financial InstitutionsDocument26 pagesMoney and Financial InstitutionsSorgot Ilie-Liviu100% (1)

- Stability Index Fund $SIFU PDFDocument4 pagesStability Index Fund $SIFU PDFJonnyNo ratings yet

- Exercise 4Document17 pagesExercise 4LoyalNamanAko LLNo ratings yet

- Abt - 3Document3 pagesAbt - 3dhruvNo ratings yet

- InsuranceDocument188 pagesInsurancetura kedirNo ratings yet

- The Venus ProjectDocument27 pagesThe Venus Projectapi-252242159100% (1)

- Pal VS CaDocument2 pagesPal VS CaJesa Formaran100% (1)

- Lock Box in SAP ARDocument4 pagesLock Box in SAP ARNaveen KumarNo ratings yet

- Minggu 2 - Chapter 03 Interest and EquivalenceDocument38 pagesMinggu 2 - Chapter 03 Interest and EquivalenceAchmad Nabhan YamanNo ratings yet

- Ch10 PPTDocument62 pagesCh10 PPTmuhammad Adeel0% (1)

- Ivrcl Indore Toll Ways NCLTDocument15 pagesIvrcl Indore Toll Ways NCLTveeruNo ratings yet

- Kochi Issues With Initial of Haider AliDocument4 pagesKochi Issues With Initial of Haider AliJee Francis TherattilNo ratings yet