You might also like

- 08 Chapter 1 - Managerial RemunerationDocument26 pages08 Chapter 1 - Managerial RemunerationMbaStudent56No ratings yet

- Are Ceos Rewarded by LuckDocument33 pagesAre Ceos Rewarded by LuckLeonardo SimonciniNo ratings yet

- Executive PayDocument6 pagesExecutive PayVenkat VenkatesanNo ratings yet

- Taking Stock: Why Executive Pay Results in An Unstable and Inequitable EconomyDocument16 pagesTaking Stock: Why Executive Pay Results in An Unstable and Inequitable EconomyRoosevelt InstituteNo ratings yet

- Perf & Rew MGT Assign 0910Document15 pagesPerf & Rew MGT Assign 0910leviahanNo ratings yet

- Why Has CEO Pay Increased So Much? (Gabaix & Landier, 2006)Document48 pagesWhy Has CEO Pay Increased So Much? (Gabaix & Landier, 2006)DanielCoimbra100% (1)

- 90 Cents of Every 'Pay-For-Performance' Dollar Are Paid For LuckDocument28 pages90 Cents of Every 'Pay-For-Performance' Dollar Are Paid For LuckAlistair ThorntonNo ratings yet

- Meaning of Reward SchemesDocument11 pagesMeaning of Reward SchemesAPMNo ratings yet

- AssignmentDocument5 pagesAssignmentarthurmpendamaniNo ratings yet

- Reward schemes-WPS OfficeDocument4 pagesReward schemes-WPS OfficeDengdit AkolNo ratings yet

- 2003.bebchuk Fried - Executive.compensationDocument22 pages2003.bebchuk Fried - Executive.compensationflorensinurayaNo ratings yet

- Loyalty-Based Portfolio Choice: Lauren CohenDocument33 pagesLoyalty-Based Portfolio Choice: Lauren Cohench_arfan2002No ratings yet

- CG and Ceo CompensationDocument12 pagesCG and Ceo Compensationdinesh8maharjanNo ratings yet

- Agency ProblemDocument22 pagesAgency ProblemNeelangie MahawanniarachchiNo ratings yet

- 2003 - LA Bebchuk, JM Fried - Executive Compensation As An Agency ProblemDocument89 pages2003 - LA Bebchuk, JM Fried - Executive Compensation As An Agency Problemahmed sharkasNo ratings yet

- Model Answer: Literature review on Employee motivation, rewards and performanceFrom EverandModel Answer: Literature review on Employee motivation, rewards and performanceNo ratings yet

- CH 15Document7 pagesCH 15leisurelarry999No ratings yet

- Exam AbiDocument4 pagesExam AbiCarl Matthew Dela PeñaNo ratings yet

- Mullainathan - CEO Pay and LuckDocument32 pagesMullainathan - CEO Pay and Luckanusharam2014No ratings yet

- DataDocument70 pagesDataSai PradeepNo ratings yet

- Executive CompensationDocument10 pagesExecutive Compensationtanmoynaskar100No ratings yet

- Corporate Governance and Business EthicsDocument9 pagesCorporate Governance and Business EthicsRahul SaxenaNo ratings yet

- Ethics of Executive CompensationDocument15 pagesEthics of Executive CompensationmanbranNo ratings yet

- I&C Week 5Document4 pagesI&C Week 5AleksandraNo ratings yet

- Kate Liu Ethics Argument Essay v4Document9 pagesKate Liu Ethics Argument Essay v4api-726975695No ratings yet

- The Economics of Super ManagersDocument48 pagesThe Economics of Super ManagersAlfaez RidhoNo ratings yet

- Background of The Project StudyDocument10 pagesBackground of The Project Studyjohn_muellorNo ratings yet

- Phil301 Research Paper Lee JodyDocument10 pagesPhil301 Research Paper Lee Jodyapi-596306890No ratings yet

- Commitment and Optimal IncentiveDocument44 pagesCommitment and Optimal IncentivegedleNo ratings yet

- Heitz ManDocument45 pagesHeitz ManmahapatrarajeshranjanNo ratings yet

- 7 Myths of Corporate GovernanceDocument10 pages7 Myths of Corporate GovernanceJawad UmarNo ratings yet

- Ceo of BankDocument13 pagesCeo of Bankhaseeb_tankiwalaNo ratings yet

- CEO Compensation: Carola Frydman Dirk JenterDocument47 pagesCEO Compensation: Carola Frydman Dirk JenterMitesh PatelNo ratings yet

- What Is CEO Talent Worth?Document7 pagesWhat Is CEO Talent Worth?Brian TayanNo ratings yet

- Executive Compensation ThesisDocument7 pagesExecutive Compensation ThesisPaperWritingServiceReviewsSingapore100% (1)

- Iza Wol 237Document11 pagesIza Wol 237acebujerremyNo ratings yet

- The Quarterly Journal of Economics, February 2008Document52 pagesThe Quarterly Journal of Economics, February 2008totosilaciNo ratings yet

- Buku Chapter 12Document38 pagesBuku Chapter 12diolanaNo ratings yet

- NotesDocument13 pagesNotessuhailbapuji6No ratings yet

- 1b. LarckerTayan-Seven Myths of Corporate GovernanceDocument9 pages1b. LarckerTayan-Seven Myths of Corporate GovernanceAbhilasha BagariyaNo ratings yet

- Persons 2006Document16 pagesPersons 2006nshepardNo ratings yet

- Adrienne Smith 2177587 BUSE4031 Assignment 1Document7 pagesAdrienne Smith 2177587 BUSE4031 Assignment 1Adrienne SmithNo ratings yet

- ArticlesDocument21 pagesArticlesAkhila RaoNo ratings yet

- HRD Finals AnswerDocument10 pagesHRD Finals Answerscarlette.ivy.0892No ratings yet

- Optimal Executive Compensation vs. Managerial Power: A Review of Lucian Bebchuk and Jesse Fried's Pay Without Performance: TheDocument18 pagesOptimal Executive Compensation vs. Managerial Power: A Review of Lucian Bebchuk and Jesse Fried's Pay Without Performance: TheEugenijus LiaNo ratings yet

- Million-Dollar Hire: Build Your Bottom Line, One Employee at a TimeFrom EverandMillion-Dollar Hire: Build Your Bottom Line, One Employee at a TimeNo ratings yet

- 4.1.1. Theoretical Predictions. The First Set of Theories Deals With The Allocation of CashDocument11 pages4.1.1. Theoretical Predictions. The First Set of Theories Deals With The Allocation of CashHamid TalaiNo ratings yet

- Employee CompensationDocument10 pagesEmployee CompensationNoor Ul Huda 955-FSS/BSPSY/F17No ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- Centralized and Decentralized Decision Making in OrganizationsDocument22 pagesCentralized and Decentralized Decision Making in OrganizationsRenato SilvaNo ratings yet

- Chapter 9 Agency Conflicts and Corporate GovernanceDocument7 pagesChapter 9 Agency Conflicts and Corporate GovernanceSwee Yi LeeNo ratings yet

- After A CompanyDocument8 pagesAfter A CompanyDavid DeveraNo ratings yet

- Distortion and RiskDocument33 pagesDistortion and RiskAadhav JayarajNo ratings yet

- Director Optimal Pay Against Fat Cats in Taiwan: and Finance Research Vol. 4, No. 3 2015Document9 pagesDirector Optimal Pay Against Fat Cats in Taiwan: and Finance Research Vol. 4, No. 3 2015peter weinNo ratings yet

- Compensation Systems, Job Performance, and How to Ask for a Pay RaiseFrom EverandCompensation Systems, Job Performance, and How to Ask for a Pay RaiseNo ratings yet

- Alternative Corporate GovernanceDocument27 pagesAlternative Corporate GovernanceChandrika DasNo ratings yet

- Thesis Workers CompensationDocument5 pagesThesis Workers Compensationhollyvegacorpuschristi100% (2)

- Pay Perf Report 110812Document25 pagesPay Perf Report 110812brandon-harris-6868No ratings yet

- Compensation 8th Module NotesDocument45 pagesCompensation 8th Module NotesSreejith C S SreeNo ratings yet

- Preparing For A Succession Emergency Learning From Unexpected CEO DeparturesDocument12 pagesPreparing For A Succession Emergency Learning From Unexpected CEO DepartureswaqaslbNo ratings yet

- Replacement CEO in Unexpected CEO TurnoverDocument47 pagesReplacement CEO in Unexpected CEO TurnoverwaqaslbNo ratings yet

- Impact of Effective Succession Planning Practices PDFDocument35 pagesImpact of Effective Succession Planning Practices PDFAnonymous b4uZyiNo ratings yet

- The Effect of Work Stress, Compensation and Motivation On The Performance of Sales PeopleDocument18 pagesThe Effect of Work Stress, Compensation and Motivation On The Performance of Sales PeoplewaqaslbNo ratings yet

- SABRE GDS Booking Instructions For Transavia PDFDocument51 pagesSABRE GDS Booking Instructions For Transavia PDFMáté Bence TóthNo ratings yet

- Computation of EWTDocument9 pagesComputation of EWTJaeNo ratings yet

- Homework 2 DoneDocument4 pagesHomework 2 Donemythien94No ratings yet

- National Institute of Plant Health ManagementDocument5 pagesNational Institute of Plant Health ManagementVinodkumar NaikNo ratings yet

- Distribution Construction Standard Overhead SystemsDocument620 pagesDistribution Construction Standard Overhead SystemsRickNo ratings yet

- Master Fee Schedule (Policy-Fees) 2022 Draft Plus MemoDocument109 pagesMaster Fee Schedule (Policy-Fees) 2022 Draft Plus MemoNBC MontanaNo ratings yet

- Land Assignment in Kerala - Full Procedures From REALUTIONZ - The Best Land Problem Solvers in Kerala 9447464502Document89 pagesLand Assignment in Kerala - Full Procedures From REALUTIONZ - The Best Land Problem Solvers in Kerala 9447464502James Adhikaram100% (1)

- Stationarity, Cointegration: Arnaud Chevalier University College Dublin January 2004Document52 pagesStationarity, Cointegration: Arnaud Chevalier University College Dublin January 2004Josh2002No ratings yet

- Group 5 Patanjali PDFDocument8 pagesGroup 5 Patanjali PDFDakshNo ratings yet

- Management and AccountingDocument11 pagesManagement and AccountingPranesh MajumderNo ratings yet

- FYBMS Business Law SEM IDocument166 pagesFYBMS Business Law SEM IFearless GamingNo ratings yet

- Silver Members: Afghanistan Chamber of Commerce and IndustriesDocument78 pagesSilver Members: Afghanistan Chamber of Commerce and IndustriesHari BabuNo ratings yet

- JSRRDA - PMU - 16 JMF Observations PalamuDocument2 pagesJSRRDA - PMU - 16 JMF Observations Palamuprathuri sumanthNo ratings yet

- Ldce - Fasp - 06 PDFDocument8 pagesLdce - Fasp - 06 PDFDinesh Talele100% (4)

- Annexure-I Proforma of Application For Registration As A Political Party Under Section 29A of The Representation of The People Act, 1951Document36 pagesAnnexure-I Proforma of Application For Registration As A Political Party Under Section 29A of The Representation of The People Act, 1951Ravi SharmaNo ratings yet

- Kawooya RoscoDocument2 pagesKawooya RoscoMwesigwa SamuelNo ratings yet

- Ldis and RapidsDocument28 pagesLdis and RapidsRheii EstandarteNo ratings yet

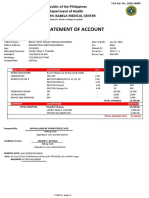

- Statement of Account: Republic of The Philippines Department of Health Southern Isabela Medical CenterDocument1 pageStatement of Account: Republic of The Philippines Department of Health Southern Isabela Medical CenterNHUJBETH INTERNET CAFENo ratings yet

- Arce - Chan Accounting FirmDocument38 pagesArce - Chan Accounting FirmshaneNo ratings yet

- Certificate of Incorporation - 2022-12-29T114941.900Document1 pageCertificate of Incorporation - 2022-12-29T114941.900MoizNo ratings yet

- Presented Here Are Selected Transactions For Norlan Inc During SeptemberDocument2 pagesPresented Here Are Selected Transactions For Norlan Inc During SeptemberMiroslav GegoskiNo ratings yet

- A Case Study of TanzaniaDocument15 pagesA Case Study of TanzaniaVladGrigoreNo ratings yet

- Brics JSP 2018 PDFDocument293 pagesBrics JSP 2018 PDFgustavo_uff1577No ratings yet

- Marxist Thought On Imperialism Survey and Critique by Charles A. BaroneDocument238 pagesMarxist Thought On Imperialism Survey and Critique by Charles A. BaroneFernandaNo ratings yet

- UntitledDocument3 pagesUntitledPutri Ayuningtyas KusumawatiNo ratings yet

- Gadaet Calculator: Questions CompulsoryDocument3 pagesGadaet Calculator: Questions CompulsoryYadNo ratings yet

- Chapter 10, Question 1. ADocument25 pagesChapter 10, Question 1. AAnh ThưNo ratings yet

- Case Study: Apollo TyresDocument9 pagesCase Study: Apollo TyresBhavjot DhaliwalNo ratings yet

- Transboundary Water Conflict Resolution Mechanisms: Substitutes or ComplementsDocument44 pagesTransboundary Water Conflict Resolution Mechanisms: Substitutes or ComplementsfulgentiosxNo ratings yet

- Vietnam May 23Document8 pagesVietnam May 23ImpExp TradeNo ratings yet

- Pareto Optimum PDFDocument19 pagesPareto Optimum PDFResti ViadonaNo ratings yet