You might also like

- Statement of Cash FlowsDocument18 pagesStatement of Cash FlowsHeyya HereNo ratings yet

- UK GAAP 2017: Generally Accepted Accounting Practice under UK and Irish GAAPFrom EverandUK GAAP 2017: Generally Accepted Accounting Practice under UK and Irish GAAPNo ratings yet

- IFRS Red Book - IAS 7 Statement of Cash FlowsDocument37 pagesIFRS Red Book - IAS 7 Statement of Cash FlowsAjmal HusseinNo ratings yet

- Statement of Cash FlowsDocument18 pagesStatement of Cash Flowslana del reyNo ratings yet

- Sb-Frs 7 (2022)Document13 pagesSb-Frs 7 (2022)peieng0409No ratings yet

- 19 Ind AS 7 Statement of Cash FlowsDocument20 pages19 Ind AS 7 Statement of Cash Flowsbixir86590No ratings yet

- IAS7Document16 pagesIAS7Fitri Putri AndiniNo ratings yet

- Statement of Cash Flows: International Accounting Standard 7Document9 pagesStatement of Cash Flows: International Accounting Standard 7Phương Vy Hà MaiNo ratings yet

- Unit 3: Indian Accounting Standard 7: Statement of Cash FlowsDocument37 pagesUnit 3: Indian Accounting Standard 7: Statement of Cash Flowspulkitddude_24114888No ratings yet

- Unit 3: Indian Accounting Standard 7: Statement of Cash FlowsDocument37 pagesUnit 3: Indian Accounting Standard 7: Statement of Cash Flowsvijaykumartax100% (4)

- IAS 7 (Statement of Cash Flows) - 123200Document6 pagesIAS 7 (Statement of Cash Flows) - 123200RashedNo ratings yet

- Statement of Cash Flows PDFDocument15 pagesStatement of Cash Flows PDFApril CaringalNo ratings yet

- IAS 7 Statement of Cash FlowDocument5 pagesIAS 7 Statement of Cash FlowLeen LurNo ratings yet

- IAS Plus IAS 7, Statement ..Document4 pagesIAS Plus IAS 7, Statement ..Buddha BlessedNo ratings yet

- Ias 7Document1 pageIas 7MR ANo ratings yet

- IAS Plus IAS 7, Statement of Cash FlowsDocument3 pagesIAS Plus IAS 7, Statement of Cash Flowsfrieda20093835No ratings yet

- Week 25 - IAS 7 Statement of Cash Flows - SlidesDocument56 pagesWeek 25 - IAS 7 Statement of Cash Flows - SlidesmamitjasNo ratings yet

- Cash Flows Statement - HandoutDocument15 pagesCash Flows Statement - HandoutThanh UyênNo ratings yet

- 14.01. Cash Flows Statement - HandoutDocument15 pages14.01. Cash Flows Statement - HandoutĐỗ LinhNo ratings yet

- IAS 7 - Statement of Cash FlowsDocument3 pagesIAS 7 - Statement of Cash Flowskapil agrawalNo ratings yet

- IAS 7 - Statement of Cash FlowsDocument4 pagesIAS 7 - Statement of Cash FlowsSky WalkerNo ratings yet

- Unit 7 Cash and Funds Flow Statements PDFDocument85 pagesUnit 7 Cash and Funds Flow Statements PDFPerumal DMNo ratings yet

- 20.0 NAS 7 - SetPasswordDocument8 pages20.0 NAS 7 - SetPasswordDhruba AdhikariNo ratings yet

- International Public Sector Accounting Standards (IPSAS)Document40 pagesInternational Public Sector Accounting Standards (IPSAS)budsy.lambaNo ratings yet

- Statement of Cash FlowsDocument3 pagesStatement of Cash FlowsLatte MacchiatoNo ratings yet

- IAS 7 - CashflowsDocument3 pagesIAS 7 - CashflowsYangatangNo ratings yet

- CH 03 IFRSDocument30 pagesCH 03 IFRSGebremedhin GebruNo ratings yet

- IAS 7 - Statement of Cash FlowsDocument3 pagesIAS 7 - Statement of Cash FlowsCaia VelazquezNo ratings yet

- 12 IAS 7 Statement of Cash FlowsDocument60 pages12 IAS 7 Statement of Cash Flowsamitsinghslideshare100% (1)

- Cash Flow Statements Bas 7Document12 pagesCash Flow Statements Bas 7Hasnain MahmoodNo ratings yet

- Ias 7 Statement of Cash FlowsDocument3 pagesIas 7 Statement of Cash FlowsMehmood RafiqNo ratings yet

- SL NO Principles Name of IAS Details About IAS Principles Status of ACI With IAS Complied Not CompliedDocument6 pagesSL NO Principles Name of IAS Details About IAS Principles Status of ACI With IAS Complied Not CompliedNaimmul FahimNo ratings yet

- Chapter 4 PAS 7 Statement of Cash FlowsDocument20 pagesChapter 4 PAS 7 Statement of Cash FlowsSimon RavanaNo ratings yet

- Unit - 3 (Afm)Document29 pagesUnit - 3 (Afm)porseenaNo ratings yet

- Ifrs 7 Financial Instruments DisclosuresDocument70 pagesIfrs 7 Financial Instruments DisclosuresVilma RamonesNo ratings yet

- Pas 7 S of Cash FlowsDocument2 pagesPas 7 S of Cash FlowsDivine Grace BravoNo ratings yet

- Cash Flow Statements PDFDocument101 pagesCash Flow Statements PDFSubbu ..100% (1)

- The Effects of Changes in Foreign Exchange Rates: Financial Reporting Standard 121Document30 pagesThe Effects of Changes in Foreign Exchange Rates: Financial Reporting Standard 121jin862No ratings yet

- NZ IAS 7 Jan19 IASB 197306.1Document15 pagesNZ IAS 7 Jan19 IASB 197306.1Shiza SattiNo ratings yet

- Financial ReportingDocument22 pagesFinancial Reportingmusic niNo ratings yet

- IPSAS Detil StandardDocument93 pagesIPSAS Detil StandardNur AsniNo ratings yet

- Statement of Cash Flow (SCF)Document21 pagesStatement of Cash Flow (SCF)Elaijah D. SacroNo ratings yet

- Ind As 1Document50 pagesInd As 1mohd52No ratings yet

- Unit 7 Cash Flow Analysis: StructureDocument34 pagesUnit 7 Cash Flow Analysis: StructureTushar SharmaNo ratings yet

- Unit 7 Cash Flow Analysis: StructureDocument34 pagesUnit 7 Cash Flow Analysis: StructureTushar SharmaNo ratings yet

- AC119 Cashflow StatementDocument82 pagesAC119 Cashflow StatementTINASHENo ratings yet

- IPSAS Detil StandardDocument94 pagesIPSAS Detil StandardMaya IndriNo ratings yet

- Acc 1Document28 pagesAcc 1manishNo ratings yet

- Financial Reporting Standards GuideDocument24 pagesFinancial Reporting Standards Guidedinis irikaNo ratings yet

- Ifrs 7 Financial Instruments DisclosuresDocument68 pagesIfrs 7 Financial Instruments DisclosuresDivya TharshiniNo ratings yet

- Ias 7Document6 pagesIas 7Khaqan TahirNo ratings yet

- Cash Flow StatementDocument12 pagesCash Flow StatementChikwason Sarcozy MwanzaNo ratings yet

- Unit 7 Cash and Funds Flow StatementsDocument85 pagesUnit 7 Cash and Funds Flow StatementsASIFNo ratings yet

- Summary of Al STD - ImpDocument20 pagesSummary of Al STD - ImpamitsinghslideshareNo ratings yet

- Accounting Standard - 3Document29 pagesAccounting Standard - 3Nilotpal DasNo ratings yet

- 7-Financial Instrument DisclosureDocument56 pages7-Financial Instrument DisclosureChelsea Anne VidalloNo ratings yet

- Pas 1Document11 pagesPas 1yvetooot50% (4)

- Fas95 PDFDocument66 pagesFas95 PDFNaamir Wahiyd BeyNo ratings yet

- MOL ChargesDocument4 pagesMOL ChargesNiraj HattangdiNo ratings yet

- Global Occupational Safety and Health Management HandbookDocument359 pagesGlobal Occupational Safety and Health Management HandbookKay AayNo ratings yet

- Maersk Sealand Shipping Instruction AllDocument3 pagesMaersk Sealand Shipping Instruction AllArturo Chávez MogollónNo ratings yet

- An Ottoman-English Merchant in Tanzimat Era Henry James Hanson and His Position in Ottoman Commercial LifeDocument24 pagesAn Ottoman-English Merchant in Tanzimat Era Henry James Hanson and His Position in Ottoman Commercial LifeHalim KılıçNo ratings yet

- 2005 09 SarDocument63 pages2005 09 SarD B Karron, PhDNo ratings yet

- Accounting Principles Chapter 7 Solution ManualDocument123 pagesAccounting Principles Chapter 7 Solution ManualKitchen UselessNo ratings yet

- Quiz #3Document4 pagesQuiz #3Lory Mae AlcosabaNo ratings yet

- Final SIP Akash MaloDocument61 pagesFinal SIP Akash MaloAKASH MALONo ratings yet

- Business Ethics and Social Responsibility: Business Essentials, 7 Edition Ebert/GriffinDocument59 pagesBusiness Ethics and Social Responsibility: Business Essentials, 7 Edition Ebert/GriffinAgung Destian PutraNo ratings yet

- Transportation Fundamentals: Dr. Anurag TiwariDocument57 pagesTransportation Fundamentals: Dr. Anurag Tiwariabhishek ladhaniNo ratings yet

- All Icai Idt Mcqs by Apamentor - 120919153723Document48 pagesAll Icai Idt Mcqs by Apamentor - 120919153723MlNo ratings yet

- Indian Economic Development Qus With AnswerDocument8 pagesIndian Economic Development Qus With AnswerTanishka SoniNo ratings yet

- Tamil Nadu Tnvat ActDocument63 pagesTamil Nadu Tnvat ActsamaadhuNo ratings yet

- 12th Balance of Payment MCQsDocument41 pages12th Balance of Payment MCQsrimjhim sahuNo ratings yet

- Sol. Man. Chapter 2Document5 pagesSol. Man. Chapter 2Jannelle Salac100% (1)

- Cash Count Certificate: N Code: - .. Sap-Sem Code: - ...................Document5 pagesCash Count Certificate: N Code: - .. Sap-Sem Code: - ...................Manjeet SinghNo ratings yet

- Trade UnionsDocument28 pagesTrade Unionssimply_coool100% (5)

- The Effects of Globalization On Procurement A Case of Nakumatt Holdings Kenya LTDDocument88 pagesThe Effects of Globalization On Procurement A Case of Nakumatt Holdings Kenya LTDadam mikidadi hijaNo ratings yet

- DHL Globalmail Brochure 2020 - UK (v2)Document21 pagesDHL Globalmail Brochure 2020 - UK (v2)Guglielmo GalluccioNo ratings yet

- Economic Impact of Tariff HikesDocument19 pagesEconomic Impact of Tariff HikesThu Phương NguyễnNo ratings yet

- An Introduction To Cost Terms and Purposes Problems 1 11Document3 pagesAn Introduction To Cost Terms and Purposes Problems 1 11b894qr949tNo ratings yet

- 1st PUC Business Studies Feb 2018Document2 pages1st PUC Business Studies Feb 2018Lokesh RaoNo ratings yet

- North American Free Trade Agreement (NAFTA)Document47 pagesNorth American Free Trade Agreement (NAFTA)Niki AcharyaNo ratings yet

- Clarity Inquiry #jqn39d08gqDocument15 pagesClarity Inquiry #jqn39d08gqChristopher IknerNo ratings yet

- Consumer Scrap Price List-23rdMar22-EXIDEDocument1 pageConsumer Scrap Price List-23rdMar22-EXIDEShubham SinghNo ratings yet

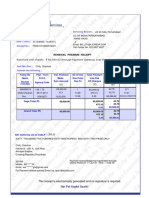

- Received With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromDocument1 pageReceived With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromCSK100% (1)

- If Midterm 2018Document4 pagesIf Midterm 2018BRIAN INCOGNITO100% (1)

- Basics of Financial ManagementDocument48 pagesBasics of Financial ManagementAntónio João Lacerda Vieira100% (1)

- ACCOUNTING 223n - Terminal OutputDocument6 pagesACCOUNTING 223n - Terminal OutputAys KopiNo ratings yet

- History of TaxationDocument12 pagesHistory of TaxationHai Bui thiNo ratings yet

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyFrom EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyRating: 4.5 out of 5 stars4.5/5 (37)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)From EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Rating: 4.5 out of 5 stars4.5/5 (24)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesFrom EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesRating: 5 out of 5 stars5/5 (4)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceFrom EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceNo ratings yet

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)