You might also like

- Tax Treaty Between SG and PHDocument9 pagesTax Treaty Between SG and PHCarmel LouiseNo ratings yet

- Related Tax LawDocument7 pagesRelated Tax LawNishad VTNo ratings yet

- 2015 ITAD - BIR - Ruling - No. - 335 1520210622 12 19ad6s6Document4 pages2015 ITAD - BIR - Ruling - No. - 335 1520210622 12 19ad6s6rian.lee.b.tiangcoNo ratings yet

- New Tax Law of Oman SummaryDocument7 pagesNew Tax Law of Oman SummaryNainesh JoshiNo ratings yet

- Peres 1Document4 pagesPeres 1janahh.omNo ratings yet

- PWC News Alert 28 October 2016 Revised Tax Treaty Signed Between India and South KoreaDocument4 pagesPWC News Alert 28 October 2016 Revised Tax Treaty Signed Between India and South KoreaTEJASWINo ratings yet

- Taxation of Corporate Dividends and Stock DividendsDocument16 pagesTaxation of Corporate Dividends and Stock DividendsGeralyn GabrielNo ratings yet

- Singapore Corporation Tax Guide: Single-Tier System and India DTADocument4 pagesSingapore Corporation Tax Guide: Single-Tier System and India DTAmd_h_irfanrehmniNo ratings yet

- BIR Ruling 101-18 wPEDocument8 pagesBIR Ruling 101-18 wPEKathyrn Ang-ZarateNo ratings yet

- ITAD BIR Ruling No. 311-14Document9 pagesITAD BIR Ruling No. 311-14cool_peachNo ratings yet

- Income Taxation BasicsDocument10 pagesIncome Taxation BasicsMichael Allen RodrigoNo ratings yet

- HK IRD Tax GuideDocument34 pagesHK IRD Tax GuideAlex LimNo ratings yet

- Avoidance of Double TaxDocument7 pagesAvoidance of Double Taxirma makharoblidzeNo ratings yet

- Notes On ACC406Document17 pagesNotes On ACC406annaNo ratings yet

- Mcdonald'S Philippines Realty Corporation Vs Cir Is MPRC'S Interest Income From Loans Subject To Vat?Document1 pageMcdonald'S Philippines Realty Corporation Vs Cir Is MPRC'S Interest Income From Loans Subject To Vat?Laika CorralNo ratings yet

- DST On Policy Holders Registered With PEZADocument5 pagesDST On Policy Holders Registered With PEZACkey ArNo ratings yet

- Digest (1986 To 2016)Document151 pagesDigest (1986 To 2016)Jerwin DaveNo ratings yet

- Ghana's Legislative System Provides A Framework For Investment - Ghana 2018 - Oxford Business GroupDocument13 pagesGhana's Legislative System Provides A Framework For Investment - Ghana 2018 - Oxford Business GroupEsinam AdukpoNo ratings yet

- Itad Bir Ruling No. 029-18: Puyat Jacinto and Santos Law OfficeDocument5 pagesItad Bir Ruling No. 029-18: Puyat Jacinto and Santos Law Officerian.lee.b.tiangcoNo ratings yet

- Other Percentage Taxes (OPT)Document56 pagesOther Percentage Taxes (OPT)Vince ManahanNo ratings yet

- CIR v. AcesiteDocument2 pagesCIR v. AcesiteATRNo ratings yet

- DTAA Nepal Final PDFDocument17 pagesDTAA Nepal Final PDFSichen UpretyNo ratings yet

- Direct Tax Code: Term ProjectDocument22 pagesDirect Tax Code: Term Projectvikaschugh01No ratings yet

- Isla Lipana & Co.Document3 pagesIsla Lipana & Co.edcbess23No ratings yet

- Sri Lanka 2018 PDFDocument24 pagesSri Lanka 2018 PDFSoofi AthamNo ratings yet

- Air Canada Tax Case Rules Carrier Not Liable for GPB Tax Under PH-Canada TreatyDocument1 pageAir Canada Tax Case Rules Carrier Not Liable for GPB Tax Under PH-Canada TreatyY P Dela PeñaNo ratings yet

- Question 1 Paper13Document6 pagesQuestion 1 Paper13Anshu AbhishekNo ratings yet

- Nigeria Tax & Fiscal RegulationsDocument9 pagesNigeria Tax & Fiscal RegulationsAparna SinghNo ratings yet

- 2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFDocument18 pages2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFtendaicrosby100% (1)

- Taxation ReportDocument3 pagesTaxation ReportBernard Jayson LausNo ratings yet

- Situs of IncomeDocument3 pagesSitus of IncomeElsie CayetanoNo ratings yet

- 132_2020_ND-CP_459238 -englishDocument56 pages132_2020_ND-CP_459238 -englishmaile.dhcdNo ratings yet

- F4 International Taxation NotesDocument4 pagesF4 International Taxation NotesAbdulgafoor NellogiNo ratings yet

- Taxation AspectDocument2 pagesTaxation AspectVishnu ChandranNo ratings yet

- Exemptions & Tax Incentives (Act 896) - Power Point PresentationDocument50 pagesExemptions & Tax Incentives (Act 896) - Power Point PresentationGabrielNo ratings yet

- Taxation Aspects of M&A: Capital GainDocument4 pagesTaxation Aspects of M&A: Capital Gainnikesh_shah_1No ratings yet

- DTAA Between India and MauritiusDocument16 pagesDTAA Between India and MauritiusAdv Aastha MakkarNo ratings yet

- JP K Tax Newsletter India Budget Pan en 210709Document2 pagesJP K Tax Newsletter India Budget Pan en 210709networkedNo ratings yet

- Bar Review Lecture - VATDocument71 pagesBar Review Lecture - VATIsagani DionelaNo ratings yet

- Withholding and Presumptive Taxes: Group 5Document9 pagesWithholding and Presumptive Taxes: Group 5Rumbidzaishe MunyanyiNo ratings yet

- Comparative Analysis On The Taxation of Transfer of Shares Under Indonesia MY, PH, & VT Treaty - Angeline & ArfianDocument6 pagesComparative Analysis On The Taxation of Transfer of Shares Under Indonesia MY, PH, & VT Treaty - Angeline & ArfianSolihin Makmur AlamNo ratings yet

- Regional Operating Headquarters TaxDocument3 pagesRegional Operating Headquarters TaxutaknghenyoNo ratings yet

- Paseo Realty and Development Corp. Vs - Court of Appealsg.R. No. 119286 October 13, 2004FACTSDocument8 pagesPaseo Realty and Development Corp. Vs - Court of Appealsg.R. No. 119286 October 13, 2004FACTSShynnMiñozaNo ratings yet

- Brief on Vietnam's Tax SystemDocument3 pagesBrief on Vietnam's Tax SystemSourav DasNo ratings yet

- Investing Uganda Laws Regulations and Tax AspectsDocument3 pagesInvesting Uganda Laws Regulations and Tax AspectsAttalo AlvinNo ratings yet

- Constitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL ExclusiveDocument14 pagesConstitution Statutes Executive Issuances Judicial Issuances Other Issuances Jurisprudence International Legal Resources AUSL Exclusivesbce14No ratings yet

- Digital PE-A Road AheadDocument22 pagesDigital PE-A Road AheadsandipgargNo ratings yet

- Taxation Aspects of M&A Carry Forward and Set Off of Accumulated Loss and Unabsorbed DepreciationDocument5 pagesTaxation Aspects of M&A Carry Forward and Set Off of Accumulated Loss and Unabsorbed DepreciationKARISHMAATA2No ratings yet

- Doing Business in Ghana: A Guide to Legal RequirementsDocument5 pagesDoing Business in Ghana: A Guide to Legal RequirementsenatagoeNo ratings yet

- Corporate Income Tax GuideDocument46 pagesCorporate Income Tax GuideCanapi AmerahNo ratings yet

- DTC Agreement Between Netherlands and BarbadosDocument10 pagesDTC Agreement Between Netherlands and BarbadosOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Rates of Tax:-: Individual/HUF/AOP/Artificial Juridical PersonDocument8 pagesRates of Tax:-: Individual/HUF/AOP/Artificial Juridical PersonKiran KumarNo ratings yet

- DTA AgreementDocument5 pagesDTA AgreementrohitNo ratings yet

- Qatar Tax Law 2009Document18 pagesQatar Tax Law 2009Jitendra NagvekarNo ratings yet

- Double Tax AgreementDocument8 pagesDouble Tax AgreementSiti NorhanaNo ratings yet

- RR 02-98Document60 pagesRR 02-98Michelle Ann OrendainNo ratings yet

- BIR Ruling 022-07 STT Not ITDocument12 pagesBIR Ruling 022-07 STT Not ITKathyrn Ang-ZarateNo ratings yet

- RR 02-01Document4 pagesRR 02-01saintkarriNo ratings yet

- Audit Assurance Paper 2.3 July 2023Document16 pagesAudit Assurance Paper 2.3 July 2023Godliving J LyimoNo ratings yet

- SSRN Id3423336Document7 pagesSSRN Id3423336batuchemNo ratings yet

- IfrsDocument108 pagesIfrshabeebbhai110No ratings yet

- WHVAT ReturnDocument6 pagesWHVAT ReturnbatuchemNo ratings yet

- Ifrs15 Are You Good To Go ConstructionDocument19 pagesIfrs15 Are You Good To Go ConstructionbatuchemNo ratings yet

- CST ActDocument7 pagesCST ActTimore FrancisNo ratings yet

- Practice Note On Repairs and Improvement Under The Income Tax Act 2015 ACT 896Document6 pagesPractice Note On Repairs and Improvement Under The Income Tax Act 2015 ACT 896batuchemNo ratings yet

- Lesson 5 Fund AccountingDocument18 pagesLesson 5 Fund AccountingbatuchemNo ratings yet

- Exemption Policy PDFDocument2 pagesExemption Policy PDFbatuchemNo ratings yet

- 2019 Budget Statement and Economic PolicyDocument302 pages2019 Budget Statement and Economic PolicyFuaad DodooNo ratings yet

- The Common Reporting Standard v3 PDFDocument40 pagesThe Common Reporting Standard v3 PDFbatuchemNo ratings yet

- Solution Cost and Management AccountingDocument6 pagesSolution Cost and Management AccountingbatuchemNo ratings yet

- ActivityDocument3 pagesActivitybatuchemNo ratings yet

- Content Dam Acca Global PDF-Students 2012s Sa Mar11 f9v2Document8 pagesContent Dam Acca Global PDF-Students 2012s Sa Mar11 f9v2Guna TripathiNo ratings yet

- Ghana Fiscal Guide 2015 2016Document10 pagesGhana Fiscal Guide 2015 2016batuchemNo ratings yet

- Horizontal Analysis PDFDocument3 pagesHorizontal Analysis PDFbatuchemNo ratings yet

- Horizontal Analysis PDFDocument3 pagesHorizontal Analysis PDFbatuchemNo ratings yet

- Jersey Guidance Notes Crs PDFDocument23 pagesJersey Guidance Notes Crs PDFbatuchemNo ratings yet

- Management Effectiveness Audit FormDocument16 pagesManagement Effectiveness Audit FormbatuchemNo ratings yet

- Jersey Guidance Notes Crs PDFDocument23 pagesJersey Guidance Notes Crs PDFbatuchemNo ratings yet

- C0216031322 PDFDocument10 pagesC0216031322 PDFbatuchemNo ratings yet

- The Use of Strategic Planning Tools and Techniques by Hotels in JordanDocument18 pagesThe Use of Strategic Planning Tools and Techniques by Hotels in JordanbatuchemNo ratings yet

- Business and Government Interdependence in Emerging Economies: Insights From Hotels in GhanaDocument33 pagesBusiness and Government Interdependence in Emerging Economies: Insights From Hotels in GhanabatuchemNo ratings yet

- Knowledge Horizons - Economics: Casiana RĂDUȚDocument6 pagesKnowledge Horizons - Economics: Casiana RĂDUȚbatuchemNo ratings yet

- Gh-Deloitte Tax Update 2019Document2 pagesGh-Deloitte Tax Update 2019batuchemNo ratings yet

- Hotels in GRDocument50 pagesHotels in GRMaria NikolaidiNo ratings yet

- Economics QuestionsDocument4 pagesEconomics QuestionsbatuchemNo ratings yet

- SolutionsDocument2 pagesSolutionsJan Aldrin AfosNo ratings yet

- 21-22 - P & L and BALANCE SHEETDocument2 pages21-22 - P & L and BALANCE SHEETSidvik InfotechNo ratings yet

- Games World of Puzzles - April 2024Document84 pagesGames World of Puzzles - April 2024Gregorius HocevarNo ratings yet

- Tax Rates Card 2023 GC - 220819 - 230837Document5 pagesTax Rates Card 2023 GC - 220819 - 230837smnomanNo ratings yet

- Bharat Sanchar Nigam Limited: (A Govt. of India Enterprise)Document2 pagesBharat Sanchar Nigam Limited: (A Govt. of India Enterprise)Jinto JacobNo ratings yet

- Cash JournalDocument7 pagesCash JournalASHOKA GOWDANo ratings yet

- AirAsia Travel Itinerary and Invoice for Booking ZS82QXDocument2 pagesAirAsia Travel Itinerary and Invoice for Booking ZS82QX邱子桐No ratings yet

- My Transactions December 2021Document3 pagesMy Transactions December 2021Ian Carlo RoxasNo ratings yet

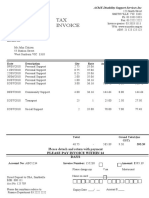

- Tax Invoice: Invoice Issued For FlightDocument2 pagesTax Invoice: Invoice Issued For FlightManab HalderNo ratings yet

- Tax Invoice: Billing Address Installation Address Invoice DetailsDocument1 pageTax Invoice: Billing Address Installation Address Invoice DetailsprofbhimashankarsNo ratings yet

- Pandemic DeadlinesDocument19 pagesPandemic DeadlinesChristine Joyce TaluaNo ratings yet

- Sample Invoice For Service ProvidersDocument2 pagesSample Invoice For Service Providers? New Emoji CharacterNo ratings yet

- High Seas Sale of Goods Under GSTDocument3 pagesHigh Seas Sale of Goods Under GSTSATYANARAYANA MOTAMARRINo ratings yet

- Bank Statement Template 27Document2 pagesBank Statement Template 27mohamed elmakhzni100% (1)

- Billings & HalsteadDocument1 pageBillings & HalsteadJo anne Jo anneNo ratings yet

- Total Parco Pakistan Ltd. Industrial Products Retail Price List Effective From 1st June 2020Document2 pagesTotal Parco Pakistan Ltd. Industrial Products Retail Price List Effective From 1st June 2020Ikhlaq AhmedNo ratings yet

- Hindalco LTA Policy: Tax Rules and Claim Process in 38 CharactersDocument7 pagesHindalco LTA Policy: Tax Rules and Claim Process in 38 CharactersSharun JacobNo ratings yet

- Batas Pambansa 22Document1 pageBatas Pambansa 22Ramil dela CruzNo ratings yet

- Countingup Statement 2023 07Document1 pageCountingup Statement 2023 07SophiaNo ratings yet

- Tax Notes (Dizon Book)Document3 pagesTax Notes (Dizon Book)Enteng KabisoteNo ratings yet

- Assignment Income Taxation 1 Version 2Document13 pagesAssignment Income Taxation 1 Version 2Juwed Mark TawaliNo ratings yet

- 1601-FQ Final Jan 2018 Rev DPADocument2 pages1601-FQ Final Jan 2018 Rev DPAMarvin AmparadoNo ratings yet

- GrupoDocument3 pagesGrupo28kpjrrx4nNo ratings yet

- 2014-2019 TAXATION LAW BAR Questions and AnswersDocument81 pages2014-2019 TAXATION LAW BAR Questions and AnswersJuris Mendoza74% (19)

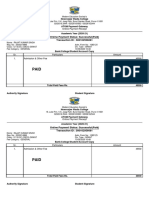

- Online Payment Status: Successful (Paid) Transaction ID: 500102956061Document2 pagesOnline Payment Status: Successful (Paid) Transaction ID: 500102956061binurajatNo ratings yet

- PAPA Session 5Document3 pagesPAPA Session 5Thomas KariukiNo ratings yet

- Tax Law 1 Course Outline 2021Document6 pagesTax Law 1 Course Outline 2021Sunny 022No ratings yet

- Domondon Taxation Notes 2010Document80 pagesDomondon Taxation Notes 2010ArahbellsNo ratings yet

- Invoice 20180611628622765Document1 pageInvoice 20180611628622765Nikhil Sharma RayaproluNo ratings yet

- TaxationDocument188 pagesTaxationNikolajay MarrenoNo ratings yet