You might also like

- The Commercial Real Estate Tsunami: A Survival Guide for Lenders, Owners, Buyers, and BrokersFrom EverandThe Commercial Real Estate Tsunami: A Survival Guide for Lenders, Owners, Buyers, and BrokersNo ratings yet

- Financial InformationDocument42 pagesFinancial InformationAbdisalam UnshurNo ratings yet

- Asia Pacific Real Estate: Still Good Value in A Changed WorldDocument11 pagesAsia Pacific Real Estate: Still Good Value in A Changed WorldIvan DidiNo ratings yet

- MRO Forecast Trend - 2018Document38 pagesMRO Forecast Trend - 2018Andrew MicallefNo ratings yet

- Company Equity Enterprise Value Sales Gross Profit: Market Valuation LTM Financial StatisticsDocument34 pagesCompany Equity Enterprise Value Sales Gross Profit: Market Valuation LTM Financial StatisticsRafał StaniszewskiNo ratings yet

- WACC AnalysisDocument9 pagesWACC AnalysisFadhilNo ratings yet

- EFI - FS Moderate Portolio ETP - 2023.Q3.EN - EUDocument1 pageEFI - FS Moderate Portolio ETP - 2023.Q3.EN - EUpderby1No ratings yet

- Barbell Income Fund BrochureDocument8 pagesBarbell Income Fund BrochurecsNo ratings yet

- UBS RE ResearchDocument89 pagesUBS RE Researchmr1234blogguyNo ratings yet

- GCA Altium Digital - Media & Internet Monitor Q3 2020Document26 pagesGCA Altium Digital - Media & Internet Monitor Q3 2020John SmithNo ratings yet

- Analysis IDocument4 pagesAnalysis IBeugh RiveraNo ratings yet

- Q2 2020 Earnings Presentation American Tower CorporationDocument25 pagesQ2 2020 Earnings Presentation American Tower CorporationKenya ToledoNo ratings yet

- Financial Crisis Inquiry Commission: Mike Mayo, CFADocument14 pagesFinancial Crisis Inquiry Commission: Mike Mayo, CFAosmar92387No ratings yet

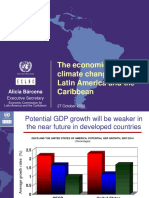

- The Economics of Climate Change in Latin America and The CaribbeanDocument23 pagesThe Economics of Climate Change in Latin America and The Caribbeanknowledge3736 jNo ratings yet

- Emerson Capital Quarterly Performance - 3Q 2009Document1 pageEmerson Capital Quarterly Performance - 3Q 2009Joseph HarrisonNo ratings yet

- Emirates TelecommunicationsDocument6 pagesEmirates TelecommunicationsSunil KumarNo ratings yet

- Boeing Current Market Outlook 2013Document37 pagesBoeing Current Market Outlook 2013VaibhavNo ratings yet

- Capitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalDocument54 pagesCapitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalMukarangaNo ratings yet

- Forrester PC Insurers ITSpend 060409Document40 pagesForrester PC Insurers ITSpend 060409Jonathan MartinNo ratings yet

- Latam Investment Banking Review q42021Document19 pagesLatam Investment Banking Review q42021eadadaNo ratings yet

- HR Team Day Out - May 2012 v3Document61 pagesHR Team Day Out - May 2012 v3sashaNo ratings yet

- Myanmar Country Report 2016 - Euler HermesDocument2 pagesMyanmar Country Report 2016 - Euler Hermesmarcmyomyint16630% (1)

- The Good, The Bad and The Ugly On Tech Valuations, AI, Energy and US PoliticsDocument11 pagesThe Good, The Bad and The Ugly On Tech Valuations, AI, Energy and US Politicsmuratc.cansoyNo ratings yet

- 0902 Californias Tax SystemDocument21 pages0902 Californias Tax SystemalcofribassNo ratings yet

- Webinar h1 2023 For ParticipantsDocument66 pagesWebinar h1 2023 For ParticipantsChchristiantoNo ratings yet

- AnalysisDocument5 pagesAnalysisBeugh RiveraNo ratings yet

- 10 Loreal en ChiffresDocument6 pages10 Loreal en ChiffresArthur NguyenNo ratings yet

- AMERCO Finance Slides 2021Document24 pagesAMERCO Finance Slides 2021Daniel KwanNo ratings yet

- Australia Investment Banking Review First Quarter 2021: Refinitiv Deals IntelligenceDocument15 pagesAustralia Investment Banking Review First Quarter 2021: Refinitiv Deals IntelligenceYohei John MikawaNo ratings yet

- Statistics Booklet 2021VFDocument51 pagesStatistics Booklet 2021VFjazz pastaNo ratings yet

- About FINN For CandidatesDocument26 pagesAbout FINN For CandidatesChinmay SHAHNo ratings yet

- Santander Mayo 2018 V FinalDocument37 pagesSantander Mayo 2018 V FinaldavidNo ratings yet

- Housing Market Update: Property Investor SummitDocument35 pagesHousing Market Update: Property Investor SummitTerry LollbackNo ratings yet

- LIAA Presentation Apr2011Document32 pagesLIAA Presentation Apr2011gunazacesteNo ratings yet

- MP - 3 - Peso Growth FundDocument2 pagesMP - 3 - Peso Growth FundFrank TaquioNo ratings yet

- 2018 Wilson Research Group: Functional Verification StudyDocument106 pages2018 Wilson Research Group: Functional Verification StudyBogdan raduNo ratings yet

- InteretrustDocument21 pagesInteretrustConstantin WellsNo ratings yet

- 2010 09 30 PH S DMCDocument3 pages2010 09 30 PH S DMCaaronsayNo ratings yet

- The Automotive Components Industry: Paul - Schockmel@iee - LuDocument20 pagesThe Automotive Components Industry: Paul - Schockmel@iee - LuRitika RathoreNo ratings yet

- 2018 q2 Forum HCMC en FinalDocument40 pages2018 q2 Forum HCMC en Finaldykim 김도연No ratings yet

- Enkomatsu 2021 Minexpo Investor RelationsDocument34 pagesEnkomatsu 2021 Minexpo Investor RelationsHugo Victor Huayanca ValverdeNo ratings yet

- Financial Model TemplateDocument42 pagesFinancial Model TemplatekissiNo ratings yet

- Quarterly Results 2010-11: HCL TechnologiesDocument31 pagesQuarterly Results 2010-11: HCL Technologies13lackhatNo ratings yet

- State of Play Western Europe: The Leasing and Automotive Rental Industry in 2008 and BeyondDocument18 pagesState of Play Western Europe: The Leasing and Automotive Rental Industry in 2008 and Beyondlévai_gáborNo ratings yet

- Analisis FinancieroDocument124 pagesAnalisis FinancieroJesús VelázquezNo ratings yet

- Radico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020Document23 pagesRadico Khaitan Ltd. Earnings Presentation: Q4 and Full Year FY2020UmangNo ratings yet

- Doomsday CycleDocument5 pagesDoomsday CyclenovriadyNo ratings yet

- Vanguard Global Stock Index FundDocument4 pagesVanguard Global Stock Index FundjorgeperezsidecarshotmailomNo ratings yet

- Quarter 2 Market Report: The Big PictureDocument9 pagesQuarter 2 Market Report: The Big PictureMridul SharmaNo ratings yet

- Microsoft 55326Document14 pagesMicrosoft 55326registerfakemailNo ratings yet

- Korn Ferry Salary Movement and Forecast Survey ReportDocument17 pagesKorn Ferry Salary Movement and Forecast Survey ReportTulshidasNo ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- AFM Mini Exam - SolutionDocument6 pagesAFM Mini Exam - SolutionHamid KhanNo ratings yet

- Goldman Prime Brokerage - Insights & Analytics Chart Pack April 2023Document30 pagesGoldman Prime Brokerage - Insights & Analytics Chart Pack April 2023ZerohedgeNo ratings yet

- THE Treasurer'S Toolkit: Unpacking The DNA of A Successful Treasurer in 2025Document19 pagesTHE Treasurer'S Toolkit: Unpacking The DNA of A Successful Treasurer in 2025mashael abanmiNo ratings yet

- SSRN Id3377016Document29 pagesSSRN Id3377016ninoloterte85No ratings yet

- Collective Insights: Minutes From Our Morning MeetingDocument2 pagesCollective Insights: Minutes From Our Morning Meetingapi-63645244No ratings yet

- Icici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021Document17 pagesIcici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021hackmeatakashNo ratings yet

- LG GuideDocument25 pagesLG GuideJoly SinhaNo ratings yet

- 3Q09 Business Conference)Document19 pages3Q09 Business Conference)sdey003No ratings yet

- Vagilidad v. VagilidadDocument2 pagesVagilidad v. VagilidadCarie LawyerrNo ratings yet

- What Is Housing?Document8 pagesWhat Is Housing?Psy Giel Va-ayNo ratings yet

- Yap Nyo Nyok V Bath Pharmacy SDN BHD, (1993) 2 MLJ 250Document9 pagesYap Nyo Nyok V Bath Pharmacy SDN BHD, (1993) 2 MLJ 250Hani Firdaus HashimNo ratings yet

- Lease FinancingDocument17 pagesLease FinancingPoonam Sharma100% (2)

- RDO No. 40 - CubaoDocument324 pagesRDO No. 40 - CubaoattyengrNo ratings yet

- LLB-306 Nov. 2020Document1 pageLLB-306 Nov. 2020nikita aroraNo ratings yet

- Special Power of Attorney-BaclaranDocument1 pageSpecial Power of Attorney-BaclaranMelinda LapusNo ratings yet

- Local Finance Circular No. 1-97Document21 pagesLocal Finance Circular No. 1-97Ah MhiNo ratings yet

- FSBO Resources & Checklist. 3A Properties SolutionsDocument5 pagesFSBO Resources & Checklist. 3A Properties SolutionsAlassane DraboNo ratings yet

- A221 MC 3 - StudentDocument5 pagesA221 MC 3 - StudentNajihah RazakNo ratings yet

- G.R. No. 218628Document12 pagesG.R. No. 218628Vince Anuta SalanapNo ratings yet

- News Developer Preer Building Tiny Homes in Victoria's Caravan ParksDocument5 pagesNews Developer Preer Building Tiny Homes in Victoria's Caravan Parksroshan24No ratings yet

- 41 Cruz vs. Filipinas Investment & Finance CorporationDocument2 pages41 Cruz vs. Filipinas Investment & Finance CorporationJemNo ratings yet

- Castillo v. Reyes - SalesDocument1 pageCastillo v. Reyes - SalesManasseh DizonNo ratings yet

- Brigade Sanctuary Agreement To SellDocument53 pagesBrigade Sanctuary Agreement To SellGaurav RanjanNo ratings yet

- Saln 2023Document4 pagesSaln 2023xylynn myka cabanatanNo ratings yet

- Dynamic Engineering Services: Valuer Empanelled With Hon'ble Calcutta High Court & Punjab National Bank (PM & IM)Document12 pagesDynamic Engineering Services: Valuer Empanelled With Hon'ble Calcutta High Court & Punjab National Bank (PM & IM)Souma Dip BhaduriNo ratings yet

- Real Estate Finance & Investments Midterm I Group ADocument8 pagesReal Estate Finance & Investments Midterm I Group AJiayu JinNo ratings yet

- AHC Eviction Reduction Recommendations FINAL 053023Document54 pagesAHC Eviction Reduction Recommendations FINAL 053023Sean KeenanNo ratings yet

- Pre Emption Under Non Agricultural Tenancy Act, 1949Document2 pagesPre Emption Under Non Agricultural Tenancy Act, 1949Kamruz ZamanNo ratings yet

- QuitclaimDocument2 pagesQuitclaimManny B. Victor VIIINo ratings yet

- Property OutlineDocument29 pagesProperty OutlineJillian WheelockNo ratings yet

- JSP PageDocument1 pageJSP PageSai SantoshNo ratings yet

- Modes Methods of Acquiring Land TitlesDocument5 pagesModes Methods of Acquiring Land TitlesAllysaJoyDadullaNo ratings yet

- Physical Surveys For TP 1Document15 pagesPhysical Surveys For TP 1Anna Maria DavidNo ratings yet

- Emergency Assistance Plan For Rental Housing - COVID-19Document1 pageEmergency Assistance Plan For Rental Housing - COVID-19Maritza NunezNo ratings yet

- TAX-302 (VAT-Exempt Transactions)Document7 pagesTAX-302 (VAT-Exempt Transactions)Edith DalidaNo ratings yet

- The Luxury Property Collections Lookbook - DigitalDocument70 pagesThe Luxury Property Collections Lookbook - DigitalClive WongNo ratings yet

- Real Estate MortgageDocument3 pagesReal Estate MortgageJuven MoradaNo ratings yet

- Course Outline 2023-24Document3 pagesCourse Outline 2023-24choudharyshaab383No ratings yet