You might also like

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Private Debt: Yield, Safety and the Emergence of Alternative LendingFrom EverandPrivate Debt: Yield, Safety and the Emergence of Alternative LendingNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Book Keeping & AccountsDocument390 pagesBook Keeping & AccountsAAISHA AHMED75% (4)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- QUIZ - CHAPTER 1 - STATEMENT OF FINANCIAL POSITION With SolutionsDocument9 pagesQUIZ - CHAPTER 1 - STATEMENT OF FINANCIAL POSITION With Solutionsfinn mertens100% (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Corporate Financial Distress, Restructuring, and Bankruptcy: Analyze Leveraged Finance, Distressed Debt, and BankruptcyFrom EverandCorporate Financial Distress, Restructuring, and Bankruptcy: Analyze Leveraged Finance, Distressed Debt, and BankruptcyNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Fundamentals of Accountancy, Business and Management 1: Quarter 3 - Module 5: Books of AccountsDocument29 pagesFundamentals of Accountancy, Business and Management 1: Quarter 3 - Module 5: Books of AccountsMarlyn Lotivio100% (2)

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Credit CardDocument77 pagesCredit CardSamuel DavisNo ratings yet

- Configuration Example: SAP Electronic Bank Statement (SAP - EBS)From EverandConfiguration Example: SAP Electronic Bank Statement (SAP - EBS)Rating: 3 out of 5 stars3/5 (1)

- Financial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersFrom EverandFinancial Analysis 101: An Introduction to Analyzing Financial Statements for beginnersNo ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- SAP SD ConfigurationDocument43 pagesSAP SD ConfigurationJibin Kuttappan100% (1)

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Direct Property & Casualty Insurance Carrier Revenues World Summary: Market Values & Financials by CountryFrom EverandDirect Property & Casualty Insurance Carrier Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

- Commercial Bank Revenues World Summary: Market Values & Financials by CountryFrom EverandCommercial Bank Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Credit Union Revenues World Summary: Market Values & Financials by CountryFrom EverandCredit Union Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Activities Related to Credit Intermediation Miscellaneous Revenues World Summary: Market Values & Financials by CountryFrom EverandActivities Related to Credit Intermediation Miscellaneous Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Consumer Lending Revenues World Summary: Market Values & Financials by CountryFrom EverandConsumer Lending Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Secondary Market Financing Revenues World Summary: Market Values & Financials by CountryFrom EverandSecondary Market Financing Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Tugas Plant Asset - Winda Gokma Fransiska Purba - 4112311090Document13 pagesTugas Plant Asset - Winda Gokma Fransiska Purba - 4112311090Winda FransiskaNo ratings yet

- Xplornet Pre-Installation Info For United TVDocument5 pagesXplornet Pre-Installation Info For United TVPam DavidsonNo ratings yet

- A. Journal Entries Accounts Debit CreditDocument3 pagesA. Journal Entries Accounts Debit CreditAnne AlagNo ratings yet

- ForxDocument12 pagesForxrahul857No ratings yet

- Adjusting Entries QuizDocument22 pagesAdjusting Entries QuizChris MartinezNo ratings yet

- Consolidated Financial Statements: On Date of Business CombinationDocument53 pagesConsolidated Financial Statements: On Date of Business Combinationankursharma06No ratings yet

- Financial Statements - I Class 11 Notes CBSE Accountancy Chapter 9 (PDF)Document7 pagesFinancial Statements - I Class 11 Notes CBSE Accountancy Chapter 9 (PDF)yashwini2827No ratings yet

- Handouts PartnershipDocument9 pagesHandouts PartnershipCPANo ratings yet

- SAMALA - DISCUSSION 4 (Audit of Stockholder's Equity, Share Based Payment & Book Value and Earnings Per Share)Document6 pagesSAMALA - DISCUSSION 4 (Audit of Stockholder's Equity, Share Based Payment & Book Value and Earnings Per Share)Jessalyn DaneNo ratings yet

- SW-16 UTB Merchandising AsDocument4 pagesSW-16 UTB Merchandising AsAlexis Marie Balagot100% (1)

- Slide f3 1 StudentDocument444 pagesSlide f3 1 Studentlinh nguyễn100% (1)

- ACCT Ch12 TestDocument55 pagesACCT Ch12 Testki100% (1)

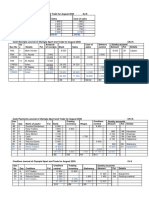

- Debtors Journal of Olympia Sport and Trade For August 2020DJ 8Document7 pagesDebtors Journal of Olympia Sport and Trade For August 2020DJ 8thokoanebokang00No ratings yet

- Account TableDocument1,612 pagesAccount TableleminhbkNo ratings yet

- Theoretical Framework Class Notes by NavkarDocument54 pagesTheoretical Framework Class Notes by Navkarmunusamy shanmugam100% (1)

- Control AccountingDocument7 pagesControl AccountingAmir RuplalNo ratings yet

- Ricardo Pangan Company General Journal For The Month of January 2021 Date Accounts Receivable Debit CreditDocument14 pagesRicardo Pangan Company General Journal For The Month of January 2021 Date Accounts Receivable Debit CreditTiamzon Ella Mae M.No ratings yet

- APY Subscriber-Details Modification FormDocument3 pagesAPY Subscriber-Details Modification FormManoj GoyalNo ratings yet

- MerimenOnline RegForm RepairerDocument9 pagesMerimenOnline RegForm RepairerMohd Syafiq Ab Manaf50% (2)

- Fundamentals of Accounting For Microfina PDFDocument42 pagesFundamentals of Accounting For Microfina PDFEmilenn Kate Sacdalan-PateñoNo ratings yet

- Basic Financial AccountingDocument118 pagesBasic Financial AccountingSaleem Javed100% (1)

- Accounting Guidance PDFDocument30 pagesAccounting Guidance PDFJade Diaz100% (1)

- ME/MMT: The Currency As A Public MonopolyDocument7 pagesME/MMT: The Currency As A Public MonopolyAdam Rice100% (1)

- Chapter 3Document12 pagesChapter 3Dùķe HPNo ratings yet

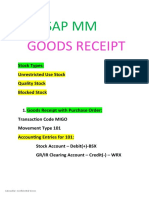

- Goods ReceiptDocument7 pagesGoods ReceiptghNo ratings yet