You might also like

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- 1600-VT 0322Document3 pages1600-VT 0322Mishelle RamosNo ratings yet

- 1600-VT MaterialsDocument2 pages1600-VT MaterialsgennadacaweNo ratings yet

- 2551Q Jan 2018 ENCS Final Rev 3Document2 pages2551Q Jan 2018 ENCS Final Rev 3MIS MijerssNo ratings yet

- RMC No. 13-2020 Annex B - 1600-PT January 2018 ENCSDocument2 pagesRMC No. 13-2020 Annex B - 1600-PT January 2018 ENCSGodfrey TejadaNo ratings yet

- Estate Tax Return: - Taxpayer InformationDocument2 pagesEstate Tax Return: - Taxpayer InformationKHAkadsbdhsgNo ratings yet

- Monthly Percentage Tax Return: 12 - December 06 - JuneDocument1 pageMonthly Percentage Tax Return: 12 - December 06 - JuneDana PardeNo ratings yet

- 1600-PT January 2018 ENCS FinalDocument2 pages1600-PT January 2018 ENCS FinalBrgy Sta. Cruz100% (7)

- 1801 Estate Tax Return FormDocument2 pages1801 Estate Tax Return FormMay DinagaNo ratings yet

- Monthly Remittance Return of Value-Added Tax Withheld 2 0: BIR Form NoDocument2 pagesMonthly Remittance Return of Value-Added Tax Withheld 2 0: BIR Form NoMark Joseph Baja67% (3)

- Competency Assessment (ACC 311) PDFDocument14 pagesCompetency Assessment (ACC 311) PDFLealyn CuestaNo ratings yet

- Donor's Tax Return: O, Kerwin Michael Cheng 195-773-545Document2 pagesDonor's Tax Return: O, Kerwin Michael Cheng 195-773-545Ackie ValderramaNo ratings yet

- 1701 2551 Merged TaxDocument5 pages1701 2551 Merged TaxGrace DyyNo ratings yet

- MiggMatugas 1701Q 1st Quarter 2023P1Document2 pagesMiggMatugas 1701Q 1st Quarter 2023P1stillwinmsNo ratings yet

- Quarterly Income Tax Return For Corporations, Partnerships and Other Non-Individual TaxpayersDocument2 pagesQuarterly Income Tax Return For Corporations, Partnerships and Other Non-Individual TaxpayersRegs AccountingTaxNo ratings yet

- 1701Q BIR Form PDFDocument3 pages1701Q BIR Form PDFJihani A. SalicNo ratings yet

- Miflores-1701A-2023Document3 pagesMiflores-1701A-2023catherine aleluyaNo ratings yet

- Monthly Percentage Tax Return: 12 - December 04 - AprilDocument1 pageMonthly Percentage Tax Return: 12 - December 04 - AprilTamara HamiltonNo ratings yet

- 1 0 2 0 1 0 8 0 0 National Agency Deped - Division of Las Piñas City Gabaldon BLDG Diego Cera Avenue E. Aldana, Las Piñas CityDocument3 pages1 0 2 0 1 0 8 0 0 National Agency Deped - Division of Las Piñas City Gabaldon BLDG Diego Cera Avenue E. Aldana, Las Piñas CityReese QuinesNo ratings yet

- OSD 3rd QuarterDocument2 pagesOSD 3rd QuarterMariela MirandaNo ratings yet

- 1701Q Jan 2018 Final Rev2Document2 pages1701Q Jan 2018 Final Rev2Balot EspinaNo ratings yet

- Bir Forms 1701Q 1701 2316 2307 1700Document11 pagesBir Forms 1701Q 1701 2316 2307 1700Geene CastroNo ratings yet

- OSD 2nd QuarterDocument2 pagesOSD 2nd QuarterMariela MirandaNo ratings yet

- Monthly Percentage Tax Return: Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X". X X 12Document2 pagesMonthly Percentage Tax Return: Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X". X X 12PingLomaadEdulanNo ratings yet

- Bir GinaDocument1 pageBir GinaApril ManjaresNo ratings yet

- BIR Form 1601-EDocument2 pagesBIR Form 1601-ELovella Phi Go100% (1)

- JUNNELA ANN LAGMAN .-BIR-Form-1701-and-1702Document16 pagesJUNNELA ANN LAGMAN .-BIR-Form-1701-and-1702Jennine ParuliNo ratings yet

- Chatto PT 3Document2 pagesChatto PT 3LabLab Chatto0% (1)

- OSD 1st QuarterDocument2 pagesOSD 1st QuarterMariela MirandaNo ratings yet

- 1601C Final Jan 2018 With DPA Comp 2Document2 pages1601C Final Jan 2018 With DPA Comp 2Donjoe JoejoejoejoeNo ratings yet

- 1701 Jan 2018 Final With RatesDocument4 pages1701 Jan 2018 Final With RatesexquisiteNo ratings yet

- RMC No. 13-2020 Annex A - 1600-VT January 2018 ENCS PDFDocument2 pagesRMC No. 13-2020 Annex A - 1600-VT January 2018 ENCS PDFGodfrey Tejada0% (1)

- RMC No. 13-2020 Annex A - 1600-VT January 2018 ENCSDocument2 pagesRMC No. 13-2020 Annex A - 1600-VT January 2018 ENCSGodfrey Tejada100% (2)

- Estate Tax Return: Part I - Taxpayer InformationDocument3 pagesEstate Tax Return: Part I - Taxpayer InformationHartel BuyuccanNo ratings yet

- BIR Form 1702RT Annual Income Tax ReturnDocument2 pagesBIR Form 1702RT Annual Income Tax ReturnRic Dela CruzNo ratings yet

- Sample Bir Form - CorporationsDocument4 pagesSample Bir Form - CorporationsChristine ViernesNo ratings yet

- RMC No. 9-2023 Annex ADocument2 pagesRMC No. 9-2023 Annex ASean AndersonNo ratings yet

- Annual Income Tax Return: BrianDocument4 pagesAnnual Income Tax Return: BrianChristine ViernesNo ratings yet

- 1702RT SYNERGETIC TRADING 2023 pg1Document1 page1702RT SYNERGETIC TRADING 2023 pg1RACHEL DAMALERIONo ratings yet

- UYLC Income Tax Return For 2022 (1702RT 2018C) - DraftDocument4 pagesUYLC Income Tax Return For 2022 (1702RT 2018C) - DraftVirgelio AbarquezNo ratings yet

- BIR Form No. 1801 (Estate Tax Return)Document2 pagesBIR Form No. 1801 (Estate Tax Return)Juan Miguel UngsodNo ratings yet

- 1701Q Jan 2018 Final Rev2Document2 pages1701Q Jan 2018 Final Rev2Donna Gracia QuiranteNo ratings yet

- Fill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Document4 pagesFill in All Applicable Spaces. Mark All Appropriate Boxes With An "X"Emelyn Ventura SantosNo ratings yet

- BIR Form 1701A Filing GuideDocument3 pagesBIR Form 1701A Filing GuideRhon MarlNo ratings yet

- 0619-E HenryDocument1 page0619-E HenryAkawnting MaterialsNo ratings yet

- BSA1Document2 pagesBSA1Ashly MateoNo ratings yet

- Barleta 1701Q Q2 - Page 1Document1 pageBarleta 1701Q Q2 - Page 1Benson Jay AlmonteNo ratings yet

- 1801 - Estate Tax ReturnDocument2 pages1801 - Estate Tax ReturnErikajane BolimaNo ratings yet

- 1801 Estate Tax ReturnDocument2 pages1801 Estate Tax ReturnCheska MangahasNo ratings yet

- Illustration 1 SampleDocument2 pagesIllustration 1 SampleGwen ClarinNo ratings yet

- Ntni Itr Final 2021 PDFDocument4 pagesNtni Itr Final 2021 PDFmario j padillaNo ratings yet

- Annex A-RMC 26-2018Document2 pagesAnnex A-RMC 26-2018Anonymous LC5kFdtc100% (1)

- Annual Income Tax Return: (DonotentercentavosDocument2 pagesAnnual Income Tax Return: (DonotentercentavosKuhramaNo ratings yet

- Tal 1600 Pt for FilingDocument1 pageTal 1600 Pt for FilingKatherine Anne SantosNo ratings yet

- IFI HCJKS July 31, 2019Document1 pageIFI HCJKS July 31, 2019Christopher Allan MorteraNo ratings yet

- EFPS Home - EFiling and Payment SystemDocument2 pagesEFPS Home - EFiling and Payment SystemJinkieNo ratings yet

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesFrom EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesNo ratings yet

- E5-11 (Statement of Financial Position Preparation) Presented Below Is TheDocument7 pagesE5-11 (Statement of Financial Position Preparation) Presented Below Is Thedebora yosika100% (1)

- ACC 124 Discussion - Dec. 11, 2023Document6 pagesACC 124 Discussion - Dec. 11, 2023racquelcamatchoNo ratings yet

- Tibajia V CaDocument1 pageTibajia V CaMylesNo ratings yet

- Equity SolutionsDocument12 pagesEquity Solutionsanant singhalNo ratings yet

- Banking Offences ActDocument6 pagesBanking Offences ActAnjit Singh100% (1)

- WSO Resume 119861Document1 pageWSO Resume 119861John MathiasNo ratings yet

- Accounting For Non-Profit Making Org-1Document14 pagesAccounting For Non-Profit Making Org-1Amelia Bailey100% (1)

- RegulationsDocument14 pagesRegulationsA BNo ratings yet

- RBI Master Circular on Customer ServiceDocument114 pagesRBI Master Circular on Customer Servicetejasj171484No ratings yet

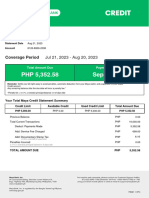

- MayaCredit SoA 2023AUGDocument3 pagesMayaCredit SoA 2023AUGJoMaye RodinasNo ratings yet

- CHAPTER 6 (Payroll)Document9 pagesCHAPTER 6 (Payroll)lc100% (1)

- Soal Mankeu1-5Document8 pagesSoal Mankeu1-5iwak_pheNo ratings yet

- Quiz-Acc 114Document4 pagesQuiz-Acc 114Rona Amor MundaNo ratings yet

- Reaction Paper - Cost CapitalDocument1 pageReaction Paper - Cost CapitalMerrylyn VargasNo ratings yet

- Fin621 MEGA FILE - MCQs From All MidTerm Papers & OLD Quizzes in One by Vuzs TeamDocument146 pagesFin621 MEGA FILE - MCQs From All MidTerm Papers & OLD Quizzes in One by Vuzs TeamZeeshan JunejoNo ratings yet

- Accounting CycleDocument16 pagesAccounting CycleBekanaNo ratings yet

- IshaqDocument1 pageIshaqishaqrashid36No ratings yet

- Macro Economics AssignmentDocument11 pagesMacro Economics AssignmentSalman83% (6)

- Chapter 8 SolutionsDocument4 pagesChapter 8 SolutionsNikulNo ratings yet

- Kolbe Fanning Sale 163Document157 pagesKolbe Fanning Sale 163msdoxseeNo ratings yet

- Ncert Solutions Class 12 Business Studies Chapter 10Document28 pagesNcert Solutions Class 12 Business Studies Chapter 10Rounak BasuNo ratings yet

- Test Series: April, 2021 Mock Test Paper 2 Intermediate (New) : Group - I Paper - 1: AccountingDocument7 pagesTest Series: April, 2021 Mock Test Paper 2 Intermediate (New) : Group - I Paper - 1: AccountingHarsh KumarNo ratings yet

- Exercises Intangible AssetsDocument3 pagesExercises Intangible AssetsNaresh SehdevNo ratings yet

- Millenials Preferences On Their Savings and Consumptions: Proposed FrameworkDocument8 pagesMillenials Preferences On Their Savings and Consumptions: Proposed FrameworkIAEME PublicationNo ratings yet

- Q1 2022 Fintech Report 1130Document30 pagesQ1 2022 Fintech Report 1130fakeid fakeidNo ratings yet

- PMT 8-K Acquires $140M Non-Performing Mortgage AssetsDocument2 pagesPMT 8-K Acquires $140M Non-Performing Mortgage Assetsank333No ratings yet

- Accounting For ReceivablesDocument16 pagesAccounting For ReceivablesAnna RoseNo ratings yet

- Analysis of Financial Statements of ICICI BankDocument77 pagesAnalysis of Financial Statements of ICICI BankMohit RohillaNo ratings yet

- Banking Ombudsman: Mr. Indranil Banerjee (Faculty of Banking Law)Document15 pagesBanking Ombudsman: Mr. Indranil Banerjee (Faculty of Banking Law)Amit GroverNo ratings yet

- Research Article: Linkage Between Economic Value Added and Market Value: An AnalysisDocument14 pagesResearch Article: Linkage Between Economic Value Added and Market Value: An Analysiseshu agNo ratings yet