You might also like

- Artist Management Contract 07Document14 pagesArtist Management Contract 07Yah MCNo ratings yet

- Business Ethics Q4 Mod4 Introduction To The Notion of Social Enterprise-V3Document29 pagesBusiness Ethics Q4 Mod4 Introduction To The Notion of Social Enterprise-V3Charmian100% (1)

- Last 6 Months Bank StatementDocument8 pagesLast 6 Months Bank StatementGajanandNo ratings yet

- Revenue Regulations No 2-2015Document4 pagesRevenue Regulations No 2-2015Yaz Carloman0% (1)

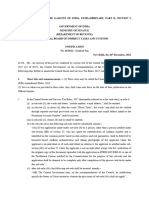

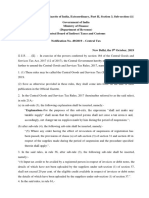

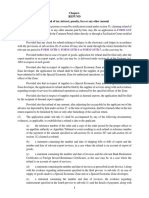

- GST CT 38 2023Document18 pagesGST CT 38 2023Raju BhaiNo ratings yet

- N 38 2023 ST GGSTDocument18 pagesN 38 2023 ST GGSTsolanki.bharatNo ratings yet

- ct26-2022Document18 pagesct26-2022cadeepaksingh4No ratings yet

- 003 ITC Mismatch in GSTR 2A Vs 2BDocument7 pages003 ITC Mismatch in GSTR 2A Vs 2BAman GargNo ratings yet

- GST Changes Explained by Govt 2022Document7 pagesGST Changes Explained by Govt 2022JoshuaNo ratings yet

- Summary of Notififcation Dated 26.12.2022Document3 pagesSummary of Notififcation Dated 26.12.2022Akshat MehariaNo ratings yet

- Notfctn 40 Central Tax English 2021Document12 pagesNotfctn 40 Central Tax English 2021sridharanNo ratings yet

- NN 14 2022 EnglishDocument13 pagesNN 14 2022 EnglishManish sharmaNo ratings yet

- CBEC issues notification on Aadhaar authenticationDocument4 pagesCBEC issues notification on Aadhaar authenticationSIR GNo ratings yet

- 06 A Idt Ammentments 2 in 1Document33 pages06 A Idt Ammentments 2 in 1Venkat RamanaNo ratings yet

- Central Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inDocument9 pagesCentral Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inwaqtkeebaatein12No ratings yet

- Key Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestDocument23 pagesKey Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestshwetaNo ratings yet

- TRANSITIONAL PROVISIONS UNDER CGST ACTDocument29 pagesTRANSITIONAL PROVISIONS UNDER CGST ACTSATYANARAYANA MOTAMARRINo ratings yet

- Draft Refund RulesDocument7 pagesDraft Refund RulessridharanNo ratings yet

- Input Tax Credit 36. Documentary Requirements and Conditions For Claiming Input Tax Credit.Document22 pagesInput Tax Credit 36. Documentary Requirements and Conditions For Claiming Input Tax Credit.KaranNo ratings yet

- Effective GST Changes W.E.F. October 01 2023Document9 pagesEffective GST Changes W.E.F. October 01 2023ravitop2006No ratings yet

- Notification 14Document11 pagesNotification 14Amol MoreNo ratings yet

- Act 20 of 2020Document8 pagesAct 20 of 2020Kriti KumarNo ratings yet

- Act 32 of 2023Document12 pagesAct 32 of 2023Kriti KumarNo ratings yet

- Annex-A: Further To Amend Certain Tax LawsDocument7 pagesAnnex-A: Further To Amend Certain Tax LawsAfreen MirzaNo ratings yet

- CGST Sixth Amendment Rules 2019Document5 pagesCGST Sixth Amendment Rules 2019Yatrik GandhiNo ratings yet

- Act 39 of 2021Document9 pagesAct 39 of 2021Kriti KumarNo ratings yet

- Circular CGST 193Document4 pagesCircular CGST 193Jaipur-B Gr-2No ratings yet

- Highlights of Key Changes in GST W.E.F January 01, 2022Document5 pagesHighlights of Key Changes in GST W.E.F January 01, 2022sumathiravirajNo ratings yet

- Taxmann's Analysis - Rule 37A - Navigating Through The Intricacies and GSTN AdvisoryDocument10 pagesTaxmann's Analysis - Rule 37A - Navigating Through The Intricacies and GSTN AdvisoryThouseefNo ratings yet

- ITC Reversal Due To Non-Payment Within 180 DaysDocument2 pagesITC Reversal Due To Non-Payment Within 180 DaysRajdev AssociatesNo ratings yet

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- TAXO Union Budget 2022Document27 pagesTAXO Union Budget 2022sanjayNo ratings yet

- Claim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022Document3 pagesClaim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022ravindra kumar jainNo ratings yet

- Indirect Tax Budget Updates 2022Document36 pagesIndirect Tax Budget Updates 2022ajitNo ratings yet

- Chapter - Returns: Form Gstr-1Document13 pagesChapter - Returns: Form Gstr-1DevNo ratings yet

- GST 31.03.17 Itc Rules PDFDocument9 pagesGST 31.03.17 Itc Rules PDFParthibanNo ratings yet

- S Natarajan 1Document44 pagesS Natarajan 1Uday KiranNo ratings yet

- GST Supplement - Dec 2022Document10 pagesGST Supplement - Dec 2022SAMAR SINGH CHAUHANNo ratings yet

- Section 16 of CGST Act 2017 - Eligibility & Conditions For Taking Input Tax Credit - Taxguru - inDocument3 pagesSection 16 of CGST Act 2017 - Eligibility & Conditions For Taking Input Tax Credit - Taxguru - inDHANNNo ratings yet

- Tax 4Document3 pagesTax 4JK Lights TradingNo ratings yet

- Chapter 11 GST ReturnsDocument18 pagesChapter 11 GST ReturnsDR. PREETI JINDALNo ratings yet

- Itc 2022-23Document24 pagesItc 2022-23Chutmaarika GoteNo ratings yet

- Form GST RFD-01: 1. Application For Refund of Tax, Interest, Penalty, Fees or Any Other AmountDocument7 pagesForm GST RFD-01: 1. Application For Refund of Tax, Interest, Penalty, Fees or Any Other AmountSarinNo ratings yet

- Bos 62607Document79 pagesBos 62607Alan JosephNo ratings yet

- circular-CBDT Clarifies Provisions RelatingDocument6 pagescircular-CBDT Clarifies Provisions RelatingYogesh KanojiyaNo ratings yet

- Amendment To Rules, 2006Document7 pagesAmendment To Rules, 2006Latest Laws TeamNo ratings yet

- Excise: 1 of 1944. Amendment of Section 9Document2 pagesExcise: 1 of 1944. Amendment of Section 9vickytatkareNo ratings yet

- ITC Reversal - 180 DaysDocument2 pagesITC Reversal - 180 DaysVijayNo ratings yet

- Chapter - Registration 1. Application For Registration: Form GST Reg-01Document10 pagesChapter - Registration 1. Application For Registration: Form GST Reg-01Abhishek MehtaNo ratings yet

- GST & Customs II Unit 1Document11 pagesGST & Customs II Unit 1GagandeepNo ratings yet

- The Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Central Rules, 1980Document29 pagesThe Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Central Rules, 1980Ayesha AlwareNo ratings yet

- Finance (Supplementary) Act, 2023Document9 pagesFinance (Supplementary) Act, 2023Umair NeoronNo ratings yet

- Latest TDS Forms, Return and procedure at eTaxIndiaDocument25 pagesLatest TDS Forms, Return and procedure at eTaxIndiaSanjay AjudiaNo ratings yet

- Major Changes in New Form 3CD (Tax Audit Report Format) #SIMPLETAXINDIADocument4 pagesMajor Changes in New Form 3CD (Tax Audit Report Format) #SIMPLETAXINDIAశ్రీనివాసకిరణ్కుమార్చతుర్వేదులNo ratings yet

- Circulars/Notifications: Legal UpdateDocument13 pagesCirculars/Notifications: Legal UpdateAnupam BaliNo ratings yet

- Highlights of 47th GST Council Meeting - Taxguru - inDocument2 pagesHighlights of 47th GST Council Meeting - Taxguru - inBharath ChootyNo ratings yet

- Do You Know GST I March 2021 I Ranjan MehtaDocument15 pagesDo You Know GST I March 2021 I Ranjan MehtaCA Ranjan MehtaNo ratings yet

- VATActNo15 (E) 2008Document12 pagesVATActNo15 (E) 2008jing qiangNo ratings yet

- Indirect Taxes / Indirect Tax Laws: Amendments by The Finance (No. 2) Act, 2009Document57 pagesIndirect Taxes / Indirect Tax Laws: Amendments by The Finance (No. 2) Act, 2009Mukul MograNo ratings yet

- SKA - Sectionwise GST Analysis - Finance Bill 2021Document24 pagesSKA - Sectionwise GST Analysis - Finance Bill 2021Sandip GoyalNo ratings yet

- Agenda Item 2 (2) - ITC RulesDocument9 pagesAgenda Item 2 (2) - ITC Rulesfintech ConsultancyNo ratings yet

- 180 days ITC reversal on non-payment of consideration – A dilemma for taxpayer- taxguru.in (1)Document9 pages180 days ITC reversal on non-payment of consideration – A dilemma for taxpayer- taxguru.in (1)kvmkinNo ratings yet

- PDD AutomationHub TemplateDocument15 pagesPDD AutomationHub TemplateGlo JosNo ratings yet

- Print - Udyam Registration CertificateDocument1 pagePrint - Udyam Registration CertificatelalitpooniaNo ratings yet

- Presentation 1Document57 pagesPresentation 1Marie TripoliNo ratings yet

- Solution Manual For Microeconomics 16th Canadian Edition Christopher T S Ragan Christopher RaganDocument14 pagesSolution Manual For Microeconomics 16th Canadian Edition Christopher T S Ragan Christopher RaganElizabethSteelefocgk100% (79)

- Mca Project Report Guidelines and FormatsDocument11 pagesMca Project Report Guidelines and Formatsvikram AjmeraNo ratings yet

- Balaji Company ProfileDocument14 pagesBalaji Company ProfileBalaji DefenceNo ratings yet

- Review JurnalDocument12 pagesReview JurnalMahatma RamantaraNo ratings yet

- Jai MiniDocument63 pagesJai MiniJaimini PrajapatiNo ratings yet

- Al Habtoor Motors Announcement - Pagani - ENGDocument2 pagesAl Habtoor Motors Announcement - Pagani - ENGMartín SacánNo ratings yet

- Introduction To Data Mining, 2 Edition: by Tan, Steinbach, Karpatne, KumarDocument95 pagesIntroduction To Data Mining, 2 Edition: by Tan, Steinbach, Karpatne, KumarsunilmeNo ratings yet

- Case Study Legal Forms of BusinessDocument5 pagesCase Study Legal Forms of BusinessRica BañaresNo ratings yet

- MY Price List With CSV SBDocument6 pagesMY Price List With CSV SBNini Syaheera Binti JasniNo ratings yet

- Hiring and Selection Case Group 0006BDocument10 pagesHiring and Selection Case Group 0006BKonanRogerKouakouNo ratings yet

- Full Download Advanced Accounting 6th Edition Jeter Test BankDocument35 pagesFull Download Advanced Accounting 6th Edition Jeter Test Bankjacksongubmor100% (40)

- CP Shipping Desk 2018Document18 pagesCP Shipping Desk 2018Farid OMARINo ratings yet

- Lesson 7: Markup and Markdown Problems: Student OutcomesDocument4 pagesLesson 7: Markup and Markdown Problems: Student OutcomesJoan BalmesNo ratings yet

- Factory Acceptance Test PlanDocument6 pagesFactory Acceptance Test PlanpreciosariyazNo ratings yet

- Case Presentation Group - 10 Company's Overview Growth StrategyDocument6 pagesCase Presentation Group - 10 Company's Overview Growth StrategyMaan MehtaNo ratings yet

- Pak PWDDocument2 pagesPak PWDSheikh BeryalNo ratings yet

- Book List PDFDocument4 pagesBook List PDFAnuragNo ratings yet

- Shanira Nuzrat - 111133013 - 30.05.2018Document80 pagesShanira Nuzrat - 111133013 - 30.05.2018Md. Mahade Hasan (153011061)No ratings yet

- Practicum LawrenceDocument20 pagesPracticum LawrenceAlfred MartinezNo ratings yet

- Legal Business Global 100 - Issue 317Document126 pagesLegal Business Global 100 - Issue 317Vivian Luiz CocoNo ratings yet

- ISO 55001 Client Guide WebDocument4 pagesISO 55001 Client Guide WebmohammedgamalattiaNo ratings yet

- Philippine Christian University: 1648 Taft Avenue Corner Pedro Gil ST., ManilaDocument4 pagesPhilippine Christian University: 1648 Taft Avenue Corner Pedro Gil ST., ManilaKatrizia FauniNo ratings yet

- Role Soft Switch in NGNDocument6 pagesRole Soft Switch in NGNHung Nguyen HuyNo ratings yet

- Pro forma invoice for horizontal drilling machineDocument1 pagePro forma invoice for horizontal drilling machineValiente InfratechNo ratings yet