You might also like

- Sample PlaintDocument2 pagesSample Plaintshweta76% (17)

- RFBT-08 (Government Procurement Law)Document10 pagesRFBT-08 (Government Procurement Law)Aman Sinaya100% (1)

- N 38 2023 ST GGSTDocument18 pagesN 38 2023 ST GGSTsolanki.bharatNo ratings yet

- ct26-2022Document18 pagesct26-2022cadeepaksingh4No ratings yet

- Budget 2022-Indirect Tax - FinalDocument45 pagesBudget 2022-Indirect Tax - Finalahjchogle2No ratings yet

- Notification 14Document11 pagesNotification 14Amol MoreNo ratings yet

- NN 14 2022 EnglishDocument13 pagesNN 14 2022 EnglishManish sharmaNo ratings yet

- CBEC issues notification on Aadhaar authenticationDocument4 pagesCBEC issues notification on Aadhaar authenticationSIR GNo ratings yet

- Act 32 of 2023Document12 pagesAct 32 of 2023Kriti KumarNo ratings yet

- Act 39 of 2021Document9 pagesAct 39 of 2021Kriti KumarNo ratings yet

- Notfctn 40 Central Tax English 2021Document12 pagesNotfctn 40 Central Tax English 2021sridharanNo ratings yet

- Central Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inDocument9 pagesCentral Goods and Services Tax (Fourteenth Amendment) Rules, 2020 - Taxguru - inwaqtkeebaatein12No ratings yet

- The Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Central Rules, 1980Document29 pagesThe Inter-State Migrant Workmen (Regulation of Employment and Conditions of Service) Central Rules, 1980Ayesha AlwareNo ratings yet

- Summary of Notififcation Dated 26.12.2022Document3 pagesSummary of Notififcation Dated 26.12.2022Akshat MehariaNo ratings yet

- Act 20 of 2020Document8 pagesAct 20 of 2020Kriti KumarNo ratings yet

- Amendment To Rules, 2006Document7 pagesAmendment To Rules, 2006Latest Laws TeamNo ratings yet

- 003 ITC Mismatch in GSTR 2A Vs 2BDocument7 pages003 ITC Mismatch in GSTR 2A Vs 2BAman GargNo ratings yet

- Excise: 1 of 1944. Amendment of Section 9Document2 pagesExcise: 1 of 1944. Amendment of Section 9vickytatkareNo ratings yet

- Effective GST Changes W.E.F. October 01 2023Document9 pagesEffective GST Changes W.E.F. October 01 2023ravitop2006No ratings yet

- Finance (Supplementary) Act, 2023Document9 pagesFinance (Supplementary) Act, 2023Umair NeoronNo ratings yet

- Relevant Amendments For November 2019 Examination in Paper 6D: Economic LawsDocument28 pagesRelevant Amendments For November 2019 Examination in Paper 6D: Economic LawsJP GuptaNo ratings yet

- VATActNo15 (E) 2008Document12 pagesVATActNo15 (E) 2008jing qiangNo ratings yet

- Further To Amend Certain Tax LawsDocument16 pagesFurther To Amend Certain Tax LawsMuhammad IlyasNo ratings yet

- GST Changes Explained by Govt 2022Document7 pagesGST Changes Explained by Govt 2022JoshuaNo ratings yet

- 06 A Idt Ammentments 2 in 1Document33 pages06 A Idt Ammentments 2 in 1Venkat RamanaNo ratings yet

- Economic Law Paper AmendmentDocument39 pagesEconomic Law Paper AmendmentcadkmarwahNo ratings yet

- Vatactno7 (E) 2003Document19 pagesVatactno7 (E) 2003jing qiangNo ratings yet

- Annex-A: Further To Amend Certain Tax LawsDocument7 pagesAnnex-A: Further To Amend Certain Tax LawsAfreen MirzaNo ratings yet

- Amendments For May 19Document24 pagesAmendments For May 19deepak pacharNo ratings yet

- Laws of Malaysia: Act A1632Document11 pagesLaws of Malaysia: Act A1632Wei LinNo ratings yet

- Claim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022Document3 pagesClaim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022ravindra kumar jainNo ratings yet

- Tax 4Document3 pagesTax 4JK Lights TradingNo ratings yet

- SEC Compliance Regulations SummaryDocument30 pagesSEC Compliance Regulations SummaryMurtaza TaqiNo ratings yet

- Draft Refund RulesDocument7 pagesDraft Refund RulessridharanNo ratings yet

- State Notification 4 D 31023Document8 pagesState Notification 4 D 31023Rafeek MunnolliNo ratings yet

- Reportable: 1 For Short, "Impugned Circular" 2 For Short, "Commissioner (GST) "Document52 pagesReportable: 1 For Short, "Impugned Circular" 2 For Short, "Commissioner (GST) "AMAR GUPTANo ratings yet

- TAXO Union Budget 2022Document27 pagesTAXO Union Budget 2022sanjayNo ratings yet

- Key Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestDocument23 pagesKey Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestshwetaNo ratings yet

- IB Code Amendments Provide Relief for MSMEs and Real Estate ProjectsDocument5 pagesIB Code Amendments Provide Relief for MSMEs and Real Estate ProjectsAAKASH BATRANo ratings yet

- Application For RegistrationDocument9 pagesApplication For RegistrationSarinNo ratings yet

- Indirect Taxes / Indirect Tax Laws: Amendments by The Finance (No. 2) Act, 2009Document57 pagesIndirect Taxes / Indirect Tax Laws: Amendments by The Finance (No. 2) Act, 2009Mukul MograNo ratings yet

- GazetteDocument692 pagesGazetteKashif NiaziNo ratings yet

- Highlights of Key Changes in GST W.E.F January 01, 2022Document5 pagesHighlights of Key Changes in GST W.E.F January 01, 2022sumathiravirajNo ratings yet

- CGST Sixth Amendment Rules 2019Document5 pagesCGST Sixth Amendment Rules 2019Yatrik GandhiNo ratings yet

- Amendment of Section 46.: CustomsDocument4 pagesAmendment of Section 46.: CustomsvickytatkareNo ratings yet

- 0 - Late Filing Charges 50000 & Should Not Exceed Duty Amount - csnt36-2018Document3 pages0 - Late Filing Charges 50000 & Should Not Exceed Duty Amount - csnt36-2018Aravind GovindarajaluNo ratings yet

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- Finance Bill 2017-18 SummaryDocument19 pagesFinance Bill 2017-18 SummarymimrandawoodyNo ratings yet

- in The Income Tax Rules, 1962, Hereinafter Referred To As The Said Rules in Rule 31ADocument36 pagesin The Income Tax Rules, 1962, Hereinafter Referred To As The Said Rules in Rule 31Aabhinav_upadhyayNo ratings yet

- CBDT Notification30 2016Document6 pagesCBDT Notification30 2016Shaan BhasinNo ratings yet

- UntitledDocument22 pagesUntitledShivani KumariNo ratings yet

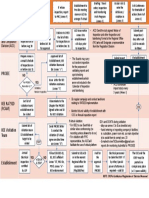

- Chapter - Registration 1. Application For Registration: Form GST Reg-01Document10 pagesChapter - Registration 1. Application For Registration: Form GST Reg-01Abhishek MehtaNo ratings yet

- Latest Idt AmendmentsDocument35 pagesLatest Idt Amendmentscsaditya20No ratings yet

- Ammendments 6D May 23Document31 pagesAmmendments 6D May 23fnNo ratings yet

- Circular CGST 193Document4 pagesCircular CGST 193Jaipur-B Gr-2No ratings yet

- Employment Regulations 1980 (Amended As at 2006)Document43 pagesEmployment Regulations 1980 (Amended As at 2006)Nelo BuensalidaNo ratings yet

- 65 Luxurty Tax Rule 2009Document10 pages65 Luxurty Tax Rule 2009shanuNo ratings yet

- 4.3 Design (Amendment) Rules, 2008Document26 pages4.3 Design (Amendment) Rules, 2008dhir.ankurNo ratings yet

- Law RTP NOV 23Document60 pagesLaw RTP NOV 23Kartikeya BansalNo ratings yet

- Final Law Amendment Nov 23Document40 pagesFinal Law Amendment Nov 23Vikash AgarwalNo ratings yet

- Bos 60318Document40 pagesBos 60318Subiksha LakshNo ratings yet

- RA7920 Visitation Process MapDocument1 pageRA7920 Visitation Process MapjanmczealNo ratings yet

- Report UniklDocument17 pagesReport Uniklcs1 accendingNo ratings yet

- Non-Payment of Highest BidderDocument1 pageNon-Payment of Highest Bidderstaircasewit4No ratings yet

- Mpkby FormsDocument8 pagesMpkby FormsmrinankadharlillyNo ratings yet

- Chapter 8 Consolidated Business OrganizationsDocument33 pagesChapter 8 Consolidated Business OrganizationsHazel Santos AgapitoNo ratings yet

- Romualdez-Yap V. CSCDocument3 pagesRomualdez-Yap V. CSCIvy ParillaNo ratings yet

- Argumentative Essay On TaxationDocument3 pagesArgumentative Essay On TaxationJonnifer Quiros100% (3)

- Assessing The Economic Implications Of: BrexitDocument5 pagesAssessing The Economic Implications Of: BrexitSpeculation OnlyNo ratings yet

- Loksabhaquestions Annex 1712 AU684Document27 pagesLoksabhaquestions Annex 1712 AU684Amit ChitwarNo ratings yet

- WTS Dhruva VAT Handbook UAEDocument125 pagesWTS Dhruva VAT Handbook UAEFarouk SarroubNo ratings yet

- Council Given Facts: On Building DelaysDocument4 pagesCouncil Given Facts: On Building DelaysdroshkyNo ratings yet

- As 1530.4-2005 Ifc Par-15668-01Document2 pagesAs 1530.4-2005 Ifc Par-15668-01ardabiliNo ratings yet

- Sold By: Friske Knits ,: Howrah, West Bengal, Uluberia, Howrah, West Bengal, India - 711316, IN-WBDocument1 pageSold By: Friske Knits ,: Howrah, West Bengal, Uluberia, Howrah, West Bengal, India - 711316, IN-WBSimfed SikkimNo ratings yet

- Form 5 Form 5A Form 5D Form 5EDocument2 pagesForm 5 Form 5A Form 5D Form 5Eمحمد ہاشمNo ratings yet

- Guideline 1 Project Concept Note Preparation and Preliminary ScreeningDocument48 pagesGuideline 1 Project Concept Note Preparation and Preliminary ScreeningEthiopian Citizen100% (3)

- Application Form For Admission 2Document2 pagesApplication Form For Admission 2faie alghanimNo ratings yet

- Sy Yong Hu and Sons et al v. CA: Difference Between Winding Up and Dissolution of a PartnershipDocument1 pageSy Yong Hu and Sons et al v. CA: Difference Between Winding Up and Dissolution of a PartnershipAnakataNo ratings yet

- Municipality Bid for 2-Story BuildingDocument2 pagesMunicipality Bid for 2-Story BuildingJohn Richard Delos ReyesNo ratings yet

- Law RTP NOV 23Document60 pagesLaw RTP NOV 23Kartikeya BansalNo ratings yet

- Defects and LiabilityDocument18 pagesDefects and LiabilityUsman AhmadNo ratings yet

- W-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Document1 pageW-8BEN: Certificate of Foreign Status of Beneficial Owner For United States Tax Withholding and Reporting (Individuals)Farhan HajarudinNo ratings yet

- UoB Registration Form (Private Students) NewDocument2 pagesUoB Registration Form (Private Students) NewSikandar KhanNo ratings yet

- District Wise Consolidated List of 433 Bank Branches of PNB, JK Bank and YES Bank For Yatra 2017 # State / Ut District Bank Branch AddressDocument20 pagesDistrict Wise Consolidated List of 433 Bank Branches of PNB, JK Bank and YES Bank For Yatra 2017 # State / Ut District Bank Branch Addressshahid2opuNo ratings yet

- Karnataka Industrial Policy 2014-19 Operative GuidelinesDocument173 pagesKarnataka Industrial Policy 2014-19 Operative GuidelinesAzhar ChakoliNo ratings yet

- Banking: New Bank Licensing Policy and Configuration of Public Sector BanksDocument8 pagesBanking: New Bank Licensing Policy and Configuration of Public Sector BanksGowtham TanneruNo ratings yet

- Public Sector Accounting Legal FrameworkDocument70 pagesPublic Sector Accounting Legal FrameworkElvis YarigNo ratings yet

- EventDocuments Afbc2001 6b70 4b9a 9d95 245ba1352efb 2Document8 pagesEventDocuments Afbc2001 6b70 4b9a 9d95 245ba1352efb 279mbvkv67yNo ratings yet

- Certificate of Incorporation-20160423Document1 pageCertificate of Incorporation-20160423keshavsomani19No ratings yet