You might also like

- Chapter 1Document30 pagesChapter 1Christine ChuaNo ratings yet

- Train Law WordDocument12 pagesTrain Law WordIsaac CursoNo ratings yet

- TRAIN LAW - Individual Income TaxationDocument25 pagesTRAIN LAW - Individual Income TaxationJennilyn SantosNo ratings yet

- Tabc - Train - Noel N. Cobangbang, CpaDocument117 pagesTabc - Train - Noel N. Cobangbang, CpaIsaac CursoNo ratings yet

- Chapter 9 Other Percentage TaxesDocument56 pagesChapter 9 Other Percentage TaxesKarylle BartolayNo ratings yet

- SGV and Co Presentation On TRAIN LawDocument48 pagesSGV and Co Presentation On TRAIN LawPortCalls100% (8)

- Forecast in Taxation Law: Atty. Raegan L. CapunoDocument47 pagesForecast in Taxation Law: Atty. Raegan L. CapunoFrance SanchezNo ratings yet

- RC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeDocument7 pagesRC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeGwyneth GloriaNo ratings yet

- Train LawDocument25 pagesTrain LawMariel Mangalino BautistaNo ratings yet

- Tax Reform For Acceleration and Inclusion (Train Law) : Republic Act No. 10963Document41 pagesTax Reform For Acceleration and Inclusion (Train Law) : Republic Act No. 10963maricrisandem100% (2)

- Train LawDocument41 pagesTrain LawJoana Lyn GalisimNo ratings yet

- Republic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Document24 pagesRepublic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Johayra AbbasNo ratings yet

- Chapter 2 Income TaxDocument4 pagesChapter 2 Income TaxKyle Hannah NemiñoNo ratings yet

- Tax On Individuals Different Kinds of Taxpayers:: (Part 1 - Applicable From Year 2018 To 2022)Document9 pagesTax On Individuals Different Kinds of Taxpayers:: (Part 1 - Applicable From Year 2018 To 2022)Ellah MaeNo ratings yet

- Income Taxation: Classification of Individual TaxpayersDocument3 pagesIncome Taxation: Classification of Individual TaxpayersALMA MORENANo ratings yet

- Resident Citizen NRC, Ra, Nra-Etb Nra-Netb Regular Income Passive Income (Within The PH) Capital Gains Subject To CGTDocument19 pagesResident Citizen NRC, Ra, Nra-Etb Nra-Netb Regular Income Passive Income (Within The PH) Capital Gains Subject To CGTKrizza TerradoNo ratings yet

- CLWTAXN Income Taxation of Individuals PDFDocument12 pagesCLWTAXN Income Taxation of Individuals PDFBerlen BellezaNo ratings yet

- Provision of Train Law UpdatedDocument91 pagesProvision of Train Law UpdatedAldrich De VeraNo ratings yet

- TAX - Individual TaxationDocument40 pagesTAX - Individual TaxationErika Mae LegaspiNo ratings yet

- Module 1 - Cherry Alfuerte - Train LawDocument41 pagesModule 1 - Cherry Alfuerte - Train Lawgerry dacerNo ratings yet

- Income Tax Card 2019-20: Suite 021, Block B Abu Dhabi Towers, F-11 Markaz Islamabad-PakistanDocument18 pagesIncome Tax Card 2019-20: Suite 021, Block B Abu Dhabi Towers, F-11 Markaz Islamabad-PakistanZain RehmanNo ratings yet

- Income Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeDocument4 pagesIncome Tax Calculator FY 2015-16 (AY 2016-17) : Particulars Details TypeKamlesh ChauhanNo ratings yet

- 1997 Tax Code vs. TRAINDocument4 pages1997 Tax Code vs. TRAINCyrine CalagosNo ratings yet

- T 5 - IT For CorporationDocument35 pagesT 5 - IT For CorporationKristine Aubrey AlvarezNo ratings yet

- BAC103A-02c Income Tax For Individuals Week 8Document4 pagesBAC103A-02c Income Tax For Individuals Week 8Novelyn Degones DuyoganNo ratings yet

- Lesson 1 - 2 Tax On The Self Employed Andor Professional 2Document4 pagesLesson 1 - 2 Tax On The Self Employed Andor Professional 2Aaron HernandezNo ratings yet

- UAE Comprehensive VAT GuideDocument19 pagesUAE Comprehensive VAT GuidefasmekbakerNo ratings yet

- Far Eastern University - Manila Income Taxation TAX1101 PartnershipDocument3 pagesFar Eastern University - Manila Income Taxation TAX1101 PartnershipRyan Christian BalanquitNo ratings yet

- Business PlanDocument14 pagesBusiness PlanghadaNo ratings yet

- Copy Individual Income TaxDocument10 pagesCopy Individual Income TaxMari Louis Noriell MejiaNo ratings yet

- Reviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%Document7 pagesReviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%LeeshNo ratings yet

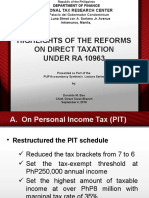

- Highlights of The Reforms On Direct Taxation UNDER RA 10963: National Tax Research CenterDocument33 pagesHighlights of The Reforms On Direct Taxation UNDER RA 10963: National Tax Research CenterCourt NanquilNo ratings yet

- Income Tax Calculator FY 2014 15Document2 pagesIncome Tax Calculator FY 2014 15atul bansalNo ratings yet

- New Tax ReformDocument4 pagesNew Tax ReformEDISON SAGUIRERNo ratings yet

- Tax Rebate Calculator of Salaried Class Indviduals 2013-14Document4 pagesTax Rebate Calculator of Salaried Class Indviduals 2013-14waheedNo ratings yet

- Sep - Presentation - Taxation SystemDocument18 pagesSep - Presentation - Taxation SystemDanial ShadNo ratings yet

- TRAIN Law On Income Tax For Individuals, Partnerships & Corporations - Part 1Document44 pagesTRAIN Law On Income Tax For Individuals, Partnerships & Corporations - Part 1ranichi14No ratings yet

- 3109 - Taxation of Non-Individual TaxpayersDocument9 pages3109 - Taxation of Non-Individual TaxpayersMae Angiela TansecoNo ratings yet

- SGV Train LawDocument149 pagesSGV Train LawEm-em CantosNo ratings yet

- Income TaxDocument70 pagesIncome TaxMary Fatima LiganNo ratings yet

- TAXDocument20 pagesTAXkate trishaNo ratings yet

- Chapter8 TaxationonindividualsDocument12 pagesChapter8 TaxationonindividualsChristine Joy Rapi MarsoNo ratings yet

- Activity 3 Gross IncomeDocument16 pagesActivity 3 Gross IncomeAnne OlitoquitNo ratings yet

- Tax XXXXDocument60 pagesTax XXXXGerald Bowe ResuelloNo ratings yet

- Individual Income Tax Rate Schedule - (Sec. 24 (A) (2) (A) )Document12 pagesIndividual Income Tax Rate Schedule - (Sec. 24 (A) (2) (A) )jimmatthamNo ratings yet

- PH Tax RMC No 19 2015 NoexpDocument1 pagePH Tax RMC No 19 2015 NoexpRodel Ryan YanaNo ratings yet

- Other Percentage Taxes PDFDocument16 pagesOther Percentage Taxes PDFJociel De GuzmanNo ratings yet

- 2018-Tax Reform For Acceleration and Inclusion2Document14 pages2018-Tax Reform For Acceleration and Inclusion2Sinetch EteyNo ratings yet

- TRAIN LAW Comparative AnalysisDocument2 pagesTRAIN LAW Comparative AnalysisElaine100% (3)

- 5.0 Intro To Income TaxDocument31 pages5.0 Intro To Income TaxAllan BacudioNo ratings yet

- Tax On Salary: Income Tax Law & CalculationDocument6 pagesTax On Salary: Income Tax Law & CalculationmuqtadirNo ratings yet

- Tax Supplemental Reviewer - October 2019Document46 pagesTax Supplemental Reviewer - October 2019Daniel Anthony CabreraNo ratings yet

- Individual Income Tax Rate Schedule - (Sec. 24 (A) (2) (A) )Document12 pagesIndividual Income Tax Rate Schedule - (Sec. 24 (A) (2) (A) )jimmatthamNo ratings yet

- Tax1 SummaryDocument8 pagesTax1 SummarychimchimcoliNo ratings yet

- 8.special Tax Rates of Companies & MATDocument22 pages8.special Tax Rates of Companies & MATMuthu nayagamNo ratings yet

- Tax On Income From Business and Profession: Activi TY SheetDocument11 pagesTax On Income From Business and Profession: Activi TY SheetJudylyn SakitoNo ratings yet

- Tax Table-Individuals-2022Document2 pagesTax Table-Individuals-2022Xandredg Sumpt LatogNo ratings yet

- Pa Tax Brief - March 2018Document11 pagesPa Tax Brief - March 2018Teresita TibayanNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Amoroso - Inventory MethodDocument6 pagesAmoroso - Inventory MethodRovey JNo ratings yet

- 9222 - JointDocument4 pages9222 - JointLee DlwlrmaNo ratings yet

- Financial and Managerial Accounting The Basis For Business Decisions 18th Edition Williams Solutions ManualDocument87 pagesFinancial and Managerial Accounting The Basis For Business Decisions 18th Edition Williams Solutions ManualEmilyJonesizjgp100% (17)

- REO CPA Review: Separate and Consolidated FsDocument10 pagesREO CPA Review: Separate and Consolidated FsCriza MayNo ratings yet

- Newinc 2023-11-03Document10 pagesNewinc 2023-11-03B HamzaNo ratings yet

- Fund Flow PDFDocument16 pagesFund Flow PDFSamruddhiSatav0% (1)

- Ark Genomic Revolution Multisector Etf Arkg HoldingsDocument2 pagesArk Genomic Revolution Multisector Etf Arkg HoldingsElizabeth ParsonsNo ratings yet

- 8Document17 pages8Harsh KSNo ratings yet

- Topic 10: Equity and BondsDocument24 pagesTopic 10: Equity and BondsPremah BalasundramNo ratings yet

- Cash Flow StatementsDocument19 pagesCash Flow Statementsyow jing peiNo ratings yet

- DCF - QuestionsDocument7 pagesDCF - Questionsanon_747753998No ratings yet

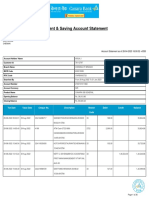

- Current & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiDocument26 pagesCurrent & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiArun Jayaprakash NarayananNo ratings yet

- Book Summary - Investment BankingDocument44 pagesBook Summary - Investment BankingabcdefNo ratings yet

- 3.CFA财报分析 Financial Statement AnalysisDocument408 pages3.CFA财报分析 Financial Statement AnalysisliujinxinljxNo ratings yet

- Tutorial Questions On Financial Ratio AnalysisDocument9 pagesTutorial Questions On Financial Ratio AnalysisSyazliana Kasim100% (9)

- Management and Cost Accounting Chapter 3Document28 pagesManagement and Cost Accounting Chapter 3Muhammad SohailNo ratings yet

- I-03 07problemDocument1 pageI-03 07problemmnrk 1997No ratings yet

- Sahand Lali Cover LetterDocument1 pageSahand Lali Cover LetterSahand LaliNo ratings yet

- Q.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementDocument5 pagesQ.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementNoor SehgalNo ratings yet

- Pre-Test 10Document2 pagesPre-Test 10BLACKPINKLisaRoseJisooJennieNo ratings yet

- Liquidity and Profitability RatioDocument5 pagesLiquidity and Profitability RatioRituraj RanjanNo ratings yet

- 2019 Caf-8 ST PDFDocument452 pages2019 Caf-8 ST PDFAbdurrehman Shaheen100% (1)

- PMS Revised SyllabusDocument197 pagesPMS Revised SyllabusFaisi GikianNo ratings yet

- New or Revised Interpretations.: Intended Learning Outcomes (Ilos)Document3 pagesNew or Revised Interpretations.: Intended Learning Outcomes (Ilos)Mon RamNo ratings yet

- Quizzes - Topic 2 - Xem L I Bài LàmDocument6 pagesQuizzes - Topic 2 - Xem L I Bài Làmnhunghuyen159No ratings yet

- A Comparative Study of Financial Performance of Sail and Tata Steel LTDDocument22 pagesA Comparative Study of Financial Performance of Sail and Tata Steel LTDpreetiaruNo ratings yet

- Managerial Economics and Strategy 2nd Edition Perloff Test BankDocument23 pagesManagerial Economics and Strategy 2nd Edition Perloff Test Banktranhhanr87100% (27)

- Your Company Name: Balance Sheet Projection Fiscal Year End DateDocument5 pagesYour Company Name: Balance Sheet Projection Fiscal Year End DateBohdan KozarNo ratings yet

- Indian and International Accounting StandardsDocument13 pagesIndian and International Accounting StandardsBhanu PrakashNo ratings yet

- Far First PB 1017Document25 pagesFar First PB 1017Din Rose Gonzales100% (1)