Professional Documents

Culture Documents

Ben Amar2011

Uploaded by

NiaOriginal Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Ben Amar2011

Uploaded by

NiaCopyright:

Available Formats

British Journal of Management, Vol.

••, ••–•• (2011)

DOI: 10.1111/j.1467-8551.2011.00789.x

What Makes Better Boards? A Closer

Look at Diversity and Ownership

Walid Ben-Amar, Claude Francoeur,1 Taïeb Hafsi1 and Réal Labelle1

Telfer School of Management, University of Ottawa, 55 Laurier East, Ottawa, Ontario K1N 6N5, and

1

HEC Montreal, 3000 Côte-Sainte-Catherine Road, Montreal, Quebec H3T 2A7, Canada

Email: benamar@telfer.uottawa.ca, claude.francoeur@hec.ca, taieb.2.hafsi@hec.ca, real.labelle@hec.ca

This study investigates the joint effect of corporate ownership and board of directors’

diversity configurations on the success of strategic merger and acquisition (M&A)

decisions. Board diversity is defined as the extent to which its demographic diversity as

measured by the culture, nationality, gender and experience of its directors complements

its statutory diversity. A theoretical framework linking ownership, board diversity and

M&A strategic decision making is proposed and tested. Based on a sample of 289 M&A

decisions undertaken by Canadian firms over the period 2000–2007, demographic diver-

sity is found to have a clear and non-linear effect on M&A performance while statutory

diversity is of limited influence. Ownership is found to influence the effect of diversity,

making the relation finer and more precise. This has practical implications. First,

statutory diversity is not sufficient for well-performing boards. Also, ownership is an

important factor. The most advocated board diversity aimed at insuring the board’s

independence is not valid across all ownership configurations. From a public policy

perspective, results provide support for the principles-based approach in governance.

Governance regimes should encourage the search for a balance between board diversity

and the need for cohesion that best serves the firm’s purpose and obligations.

Introduction Jensen, 1983). SD is mandated by law or best

practices and is often reduced to board members’

Board’s diversity and its effect on firm perform- independence from management. The second

ance have been extensively studied and yet it important issue is the belief that there is a linear

seems that we know little about the issue. Con- relationship between diversity and performance.

flicting findings, unclear or unclean methodolo- This is questioned by both logic and extant

gies, leave scholars and managers in a quandary. research (Manzoni, Strebel and Barsoux, 2010;

The first important reason for such a situation is Milliken and Martins, 1996). The third important

the dominant use of agency theory premises that issue is ownership. It is increasingly believed that

statutory diversity (SD) is all that counts to different owners pursue different goals, even when

control management and provide it with incen- they share the same kinds of assets. This may have

tives to protect shareholder value (Fama and significant effects on firm governance and ulti-

mately performance (Sur, 2009).

Claude Francoeur and Réal Labelle gratefully acknowl- In this study, we propose what we believe is a

edge financial support from the Social Sciences and more convincing theory and finer empirical find-

Humanities Research Council of Canada (Grant 410- ings by considering these issues. To do so, we

2011-2639), the Stephen A. Jarislowsky Chair in govern- recognize that SD has an effect, but we consider

ance and the CGA Professorship in Strategic Financial such effect to be contingent on individual charac-

Information. Taïeb Hafsi acknowledges support from

the Montreal Interuniversity Institute of Governance teristics of actual board members, or demo-

(IGOPP), from the Rebrab, and from the Somers graphic diversity (DD), and on the nature of

families. owners. SD, and in particular DD, are measures

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management. Published by Blackwell Publishing Ltd,

9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA, 02148, USA.

2 W. Ben-Amar et al.

of pluralism or heterogeneity in the composition the tenure of directors. These differences may

of boards of directors. This is seen as breeding a explain why Molz’s (1988, 1995) proposition that

higher level of openness and decision making ana- performance is related to pluralism was not sup-

lytical quality, and despite expected difficulties in ported by his empirical investigations. Neither

reconciling the resulting variety of perspectives, social (Molz, 1995) nor financial (Molz, 1988)

leading to better decisions (Erhardt, Werbel and performance was found to be significantly related

Shrader, 2003; Watson, Kumar and Michaelsen, to pluralism.

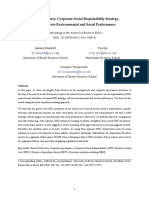

1993). The framework presented in Figure 1 structures

In the second section of the paper, our exami- and motivates what we do. It underlines the dual

nation of the literature supports these assertions but complementary fiduciary and advisory gov-

and is used to build a theoretical model and ernance roles the board plays in strategic decision

develop hypotheses. Then, we subject the model making, given the firm’s ownership structure.

and hypotheses to various statistical tests using a From a fiduciary or statutory perspective, the

sample of 289 merger and acquisition (M&A) board is deemed to indirectly influence firm per-

decisions undertaken by Canadian firms over the formance by focusing on decision control to mini-

2000–2007 period. As in McDonald, Westphal mize agency costs. This monitoring role, where

and Graebner (2008), we focus on M&A decisions independence and related statutory board charac-

as it might reasonably be expected that boards teristics are assumed to ensure better representa-

exercise greater influence on acquisition perform- tion and protection of minority shareholders’

ance than on overall firm performance, the latter interests, has been the main proposition of agency

being related to a wider array of organizational theory (Fama and Jensen, 1983) and the focus of

and environmental factors (Hermalin and most governance research and reforms, such as

Weisbach, 2001). Sarbanes-Oxley. From such a perspective, board

The following section describes the findings, effectiveness is measured in terms of its independ-

and in particular the joint effects of SD, DD and ence from management or SD. This means that

ownership on firm performance. In the final the diversity of incentives between outsiders and

section, these findings and the methods used are insiders represented on the board should help

discussed, and a few concluding comments and them meet their fiduciary obligations (Fama,

suggestions for future research are offered. 1980; Hillman, Nicholson and Shropshire, 2008;

Jensen and Meckling, 1976) and keep managerial

discretion within proper bounds. However, the

Theoretical framework and hypotheses results of empirical research on the relation

development between performance and statutory independence

are mixed (Bhagat and Black, 2002). This may not

The question of what impact board characteristics come as a surprise given that in theory, as

have on firm performance is among the most described in our framework, the main goal of

extensively researched topics in the large body fiduciary governance is to minimize agency costs,

of corporate governance research (McDonald, thus only indirectly affecting the strategic decision

Westphal and Graebner, 2008). The first attempt making process. This is the basis of our first

to explain performance, taking into account the hypothesis where we test the relationship between

interactions among the factors that make up SD and M&A performance.

diversity and independence, was Molz’s (1988, In contrast, the left-hand side of the proposed

1995). He developed a pluralism index to that framework asserts that board members are a key

effect, and classified boards into management resource and directly contribute to better strategic

dominated and pluralistic. In contrast to what we decision making (Raatikainen, 2002). By ques-

are proposing in this paper, Molz (1988, 1995) did tioning, criticizing, advising and counselling, they

not distinguish between DD and SD, lumping enhance the strategic decision making process.

them together, and did not take the firm’s owner- They also provide ‘access to channels of informa-

ship structure into account. Furthermore, his tion between the firm and environmental contin-

model only integrated gender diversity while we gences, preferential access to resources, and

also include diversity of culture and experience as legitimacy’ (Hillman, Withers and Collins, 2009,

measured by the presence of foreign directors and p. 1408). So, given that SD may be necessary but

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 3

Figure 1. Ownership, diversity in corporate governance and board strategic decisions: theoretical framework

not sufficient to materially influence corporate broad construct (Hambrick and Mason, 1984)

value, other theories based on the provision of that may include measurable demographics

resources, competences and cultural values including innate characteristics which are social,

(Barney, 1991; Hillman, Nicholson and Shrop- racial, cultural diversity, and acquired character-

shire, 2008; Selznick, 1990) must be harnessed to istics related to life experience. In this research,

complement the insights of agency-based theories DD refers to the participation of women and

and to better understand the governance– foreign directors with diverse cultures on the

performance relation. From this advisory per- board as well as to the experience of directors as

spective, board effectiveness also requires a measured by their tenure.1 Knowledge and com-

diversity of cultures, experiences and genders, petences per se are seen as exogenous. In other

referred to as demographic diversity (DD), in words, all firms are assumed to select their direc-

order to guide and contribute to organizational tors with the objective of optimizing the level of

learning and improved management strategic knowledge and competence obtained. It is their

decision making. The emphasis is on the directors’ decision relative to the mix of SD and DD which

ability to counsel and ‘mentor’ rather than may make a difference.

‘monitor’ management. DD goes beyond SD, Board diversity is expected to be positively

which mainly promotes financial literacy and the related to firm performance, especially in situa-

need for a diversity of incentives between mana- tions of complex decisions, because both DD and

gement and shareholders. Although minority SD should enhance the board’s overall qualifica-

investors’ protection still matters, under this per- tions and lead to better debates, thus triggering

spective a greater consideration is given to all

stakeholders and DD is intended to foster greater 1

pluralism on the board. Racial diversity on boards was not included in our index

as this information was not available in the proxy state-

We define board diversity or pluralism as the ments from which we manually collected the data. To the

extent to which its demographic characteristics best of our knowledge, this information is not available

complement its statutory characteristics. DD is a in any other public database in Canada.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

4 W. Ben-Amar et al.

better M&A decisions (Erhardt, Werbel and tions are based on the assumption that a board of

Shrader, 2003; Watson, Kumar and Michaelsen, directors’ independence from management

1993). Our research design distinguishes the effects enhances its monitoring function and indirectly

of ‘statutory’ diversity or highly recommended improves performance (Fama and Jensen, 1983;

‘best practices’ from ‘voluntary’ DD on firm per- John and Senbet, 1998). SD includes regulated or

formance. This leads to our second hypothesis that recommended governance practices, including in

there is a relationship between a firm’s level of DD particular a higher proportion of outside directors

and the success of its M&A decisions. However, as on the board and the separation of the functions

in Luis-Carnicer, Martínez-Sanchez and Pérez- of CEO and chairperson of the board, generally

Pérez (2008) and because heterogeneous groups referred to as the leadership structure. These are

have to work through their communication designed to foster a greater diversity of interests

problems and conflicts to end up making better or incentives than if executive directors or domi-

decisions, we expect a curvilinear relationship nant shareholders were controlling the board. It

between DD and M&A performance. also includes such other ‘best practices’ as encour-

Agency theory and recent governance reforms, aging share ownership by directors to further

which are mainly concerned with SD, have been align their interests with those of all shareholders.

respectively formulated and initiated in the Theoretical and empirical governance research

context of the US capital market where corporate (Dalton et al., 1998; John and Senbet, 1998) has

ownership is relatively more widely held than else- examined most of agency theory’s propositions,

where in the world (La Porta, Lopez-De-Silanes in particular that the board of directors monitor-

and Shleifer, 1999). Furthermore, Sur (2009) and ing function is an important pillar of a firm’s cor-

Klein, Shapiro and Young (2005) have shown porate governance system. As described on the

that governance arrangements and firm perform- right-hand side of Figure 1, from that fiduciary

ance are related to ownership characteristics. perspective, SD is assumed to indirectly improve

Thus, our last hypothesis concerns the presumed the board’s effectiveness in creating value through

joint effect of ownership and governance configu- minimizing agency costs. In other words, loss to

rations on performance. the principal resulting from interests’ divergence

Referring to the theoretical framework pre- may be curbed by imposing governance or deci-

sented in Figure 1, we shall now first justify why sion control structures to the agent. In so doing,

we distinguish board of directors SS and DD agency costs are minimized, which indirectly

given the firm’s ownership structure, then organ- affects value creation.

ize the relevant governance and M&A literatures To examine SD, we build a SD index based on

and finally develop hypotheses on their relative four proxies, all widely used in the governance–

effects on M&A performance. performance empirical literature, to measure the

board’s independence. These are the leadership

structure, the proportion of outside directors in

Statutory board diversity total board membership and the levels of owner-

‘Statutory’ board diversity (SD) refers to the ship by inside and outside directors.

regulation-mandated or highly recommended Empirical tests of the relation between tradi-

governance ‘best practices’ or guidelines put tional proxies for SD and firm performance are

forward in several countries.2 SD recommenda- generally inconclusive (Dalton et al., 1998).

According to Bhagat and Black (2002, p. 265), ‘a

2

priori, it is not obvious that independence (without

For instance, in the USA, ‘listed companies must have a knowledge or incentives) leads to better director

majority of independent directors’ on their board

(section 303A.01 of the New York Stock Exchange performance than knowledge and strong incen-

Listed Company Manual). Canada employs a principles- tives (without independence)’. This may not come

based approach to corporate governance through the as a surprise for two reasons. First, according to

implementation in National Instrument 58-101 and stewardship theory, there are ‘situations where

National Policy 58-201 of best practices guidelines. This executives as stewards [including those that are

approach is in combination with a mandatory ‘Statement

of corporate governance practices’ in the firm’s annual sitting as directors] are motivated to act in the best

report or proxy statement as to the extent of compliance interests of their principals’ (Davis, Schoorman

with such guidelines. and Donaldson, 1997, p. 24). Second, as shown in

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 5

our framework, according to agency theory the to the strategic issues that the organization is con-

main goal of fiduciary governance is to minimize fronted with. There may also, however, be an

agency costs, and thus improve performance, intriguing mediating effect of beliefs in diversity

though indirectly. Agency costs, and the effect of on group performance, as developed by van Knip-

SD, may be particularly important in major stra- penberg, Haslam and Platow (2007). According

tegic decisions such as M&As, which justifies our to this psychological perspective, when groups

desire to test the following hypothesis: value diversity they may be better able to use it

fruitfully. In contrast, when either diversity is

H1: There is a positive relationship between a

unexpected or its impact is downplayed, its effects

firm’s board SD and the quality of its board

may be depressed.3 Nevertheless, board DD could

strategic decisions.

also produce integration difficulties, result in

poorer strategic decisions in contexts that require

fast decisions (Milliken and Martins, 1996), and

Demographic diversity

even ‘backfire on company boards’ (Manzoni,

In the previous section, we referred to the stream of Strebel and Barsoux, 2010). In the context of

fiduciary governance research which mainly top managers, Hambrick, Cho and Chen (1996)

resorts to agency theory to examine the board of indicate that heterogeneity is negatively related

directors’ effectiveness. We now turn to advisory to the possibility of reaching a consensus in a

governance (left-hand side of Figure 1), which decision making process.4 According to them, het-

focuses on the board as a provider of key resources. erogeneity slows down the process by which strat-

There is substantial evidence (see Hillman, Withers egy is formulated and could considerably impair

and Collins (2009) for an overview) that boards of the decision making performance of managers

directors play an important advisory role in cor- and, ultimately, of the firm’s board members.

porate strategic decisions. From this advisory per- Diversity increases creativity (Pelled, Eisenhardt

spective, DD as more precisely specified later in and Xin, 1999), but also conflict (Jehn, 1995), and

this section is assumed to enhance the skills and decreases commitment and communication (Tsui,

general competence of boards of directors and Egan and O’Reilly, 1992).

directly impact strategic decision making and per- Prior research on diversity has mostly exam-

formance. According to Hillman and Dalziel ined the relation between one factor of DD at a

(2003) and Westphal (1999), directors are in a time and organizational performance. In this

position to affect strategy by providing advice and research, we test the joint effect of gender, culture

social support to the CEO. They can also affect the or nationality and tenure of board members on

organizational context within which strategic deci- M&A performance.

sions are made (McNulty and Pettigrew, 1999).

Hambrick and Mason (1984), focusing on the

Gender diversity. The complexity of board hete-

top management team, argue that demographic

rogeneity effects may explain that results of extant

heterogeneity enhances the ability to deal with

research on the relationship between board and

strategic change. More recently, building on their

top management gender diversity and financial

work on upper echelons of management, Ham-

performance are mixed and inconclusive (Adams,

brick (2001), Canella, Park and Lee (2008) and

Gupta and Leeth, 2009; Carter, Simkins and

Hambrick, Werder and Zajac (2008) extend the

Simpson, 2003; Daily, Trevis and Dalton, 1999;

theory to address the issue of diversity on the

Erhardt, Werbel and Shrader, 2003; Haslam

board. Raatikainen (2002) asserts that diverse

et al., 2010; Shrader, Blackburn and Iles, 1997).

groups make better decisions, which may lead

For instance, Adams, Gupta and Leeth (2009)

to better performance. Diversity improves the

knowledge base, the creativity and the quality of

the decision making and monitoring processes of 3

We gratefully acknowledge that this argument has been

a group (Erhardt, Werbel and Shrader, 2003; suggested and developed by one of this paper’s reviewers.

4

Watson, Kumar and Michaelsen, 1993). Further- One of the reviewers wondered whether consensus was

necessary. We believe that in major M&A decisions, it is

more, Milliken and Martins (1996) suggest that important for the board to show a united front. A simple

diversity of qualifications engenders favourable majority decision is an ominous signal that may cast a

board dynamics and fosters innovative solutions shadow on the value to the firm of the M&A operation.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

6 W. Ben-Amar et al.

find no difference in firms’ financial performance members can affect the time value and the accuracy

around the appointment of a woman or a man as of decisions (Ruigrok, Peck and Tacheva, 2007).

a CEO in the USA. Haslam et al. (2010) also Empirical tests generally confirm the positive

report that there is no association between effect of foreign directors on firm performance.

women’s board representation and accounting- Oxelheim and Randøy (2003) document that

based performance measures but they find a nega- Swedish and Norwegian firms with Anglo-

tive correlation with stock-based performance American outside directors have higher valua-

measures. tions than comparable firms without foreign

In exploring the relationship further, Fran- outside directors. Choi, Park and Yoo (2007) also

coeur, Labelle and Sinclair-Desgagné (2008) report a positive effect of foreign directors on

document a positive relation between gender firm performance in the Korean context. So,

diversity and financial performance in the case of in general, international diversity among board

firms operating in riskier environments. The pres- members can be expected to have a positive effect

ence of women on boards appears to help deal on performance.

with more complex strategic issues. Recently,

Adams and Ferreira (2009) show that female Directors’ tenure. According to organizational

directors have a significant impact on board demography research, tenure in a group has an

inputs and governance. More specifically, gender- effect on firms’ performance (Kosnik, 1990), stra-

diverse boards allocate more effort to monitoring tegic actions, and strategic change (Golden and

management, but the true relation between Zajac, 2001). As their association with a board

gender diversity and firm performance is complex. lasts, directors’ experience and familiarity with

For instance, these authors find that the relation the corporation’s specific governance issues and

between gender diversity and firm performance is problems increase (Kesner, 1988). Directors with

contingent upon the quality of governance. ‘We longer board experience also better understand

find that diversity has a positive impact on per- the ongoing management team practices and can

formance in firms that otherwise have weak gov- carry their oversight responsibilities with greater

ernance, as measured by their abilities to resist skills. Experienced directors can also contribute

takeovers. In firms with strong governance, to company strategy (Bilimoria and Piderit, 1994)

however, enforcing gender quotas in the board- and have a better understanding of the firm’s

room could ultimately decrease shareholder resources and operations (Alderfer, 1986). In con-

value’ (Adams and Ferreira, 2009, p. 308). trast, newly appointed directors may be captured

Overall, empirically, gender diversity is found to by the incumbent CEO (Finkelstein and Ham-

be either positive or neutral vis-à-vis performance. brick, 1988). However, tenure diversity may have

negative consequences as well. Katz (1982) sug-

Culture or nationality diversity. Oxelheim and gests that longer tenure is associated with greater

Randøy (2003), Choi, Park and Yoo (2007) and rigidity, increased commitment to established

Ruigrok, Peck and Tacheva (2007) have explored practices and procedures, and increased insula-

the effect of foreign directors’ representation tion from new ideas. According to the manage-

on the board’s processes and dynamics and ment friendliness hypothesis (Vafeas, 2003),

ultimately on firm performance. Their findings directors with long board tenure are less effective

confirm the dialectic mentioned earlier. On the one at monitoring management, which increases the

hand, in agreement with the resource dependence chances of CEO entrenchment. Vafeas (2003)

perspective, foreign directors’ cultural knowledge argues that extended tenure may reduce intra-

and expertise in foreign markets is beneficial group communications and lower the quality of

(Ruigrok, Peck and Tacheva, 2007). In particular, firms’ decisions. This study shows that the partici-

foreign directors extend board international expo- pation of senior directors in the compensation

sure and its network of contacts, an important committee is associated with higher compensation

source of competitive advantage in international payments to the firm’s CEO.

acquisition strategies. On the other hand, diversity In summary, long tenure is useful and leads to

of nationalities on the board may create commu- better performance, but pushed to the extreme it

nication and integration problems. In particular, leads to groupthink and the tendency to suppress

misunderstandings and conflicts among board conflicts, even at the expense of good decisions.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 7

Overall, DD is seen as having a positive effect. family governance, first in terms of coherence,

But there are situations where negatives are also trust (Eddleston et al., 2010; Steier, 2001) and

observed. This mixed evidence suggests a non- long-term orientation of board members (Le

linear relationship with performance. Diversity Breton-Miller and Miller, 2006).

has to be significant before it can be domesticated Introducing SD in family firms’ boards reduces

and made acceptable to all board members (van reluctance towards R&D investment (Chen and

Knippenberg, Haslam and Platow, 2007). When Hsu, 2009) and voluntary disclosure (Chau and

it is, it improves performance. This leads to our Gray, 2010). Anderson and Reeb (2004) have also

second hypothesis. shown that public firms where independent direc-

tors balance family board representation perform

H2: There is a non-linear relationship between

better. However, higher levels of diversity are

a firm’s board DD and the quality of its board

likely to lead to conflicts and loss of firm-specific

strategic decisions. Low levels of DD diminish

knowledge detained by family members (Dyer,

the quality of board strategic decisions while

2006; Jones, Makri and Gomez-Mejia, 2008). We

higher levels of DD enhance it.

therefore suggest that board strategic decision

making may be adversely affected when the levels

of SD and DD in place are too high. This leads to

The ownership factor in governance

our last hypothesis.

Finally, Figure 1 shows that the diversity of the

H3: In the presence of high ownership concen-

board or its composition is affected by the firm

tration, low levels of diversity (SD and DD)

ownership configuration. This reflects the findings

enhance the quality of board strategic decisions

of studies conducted in the USA by Sur (2009)

while higher levels of diversity diminish it.

and in Canada by Klein, Shapiro and Young

(2005). Sur (2009) shows that board composition,

strategic decisions and performance are all related

Control variables

to ownership. He proposes three ownership types

other than the widely held firms: institutional, Prior research identifies several variables that are

family and corporate blockholder. For dispersed deemed to affect M&A success. A high relative

outside investors, the main concern is the quality size of the target company to the acquirer

of SD to ensure that managers’ opportunism is (Asquith, Bruner and Mullins, 1983; Kohers and

kept in check. Institutional behaviour is geared at Kohers, 2000) and paying in cash (Huang and

maximizing shareholders’ value within well diver- Walking, 1987; Travlos, 1987) are factors that are

sified portfolios; corporate blockholder behaviour generally viewed as favourable by the market. In

is guided by the strategy of the dominant owner; contrast, acquiring public targets, compared with

and owners of family firms are less diversified and private ones, is generally associated with lower

dominated by ideological or value considerations performance (Faccio, McConnel and Stolin,

(Sur, 2009). In Canada, Klein, Shapiro and 2006; Fuller, Netter and Stegemoller, 2002).

Young (2005) also conclude that the effect of Cross-border transactions create value for the

board independence or SD on performance differs acquiring firm by exploiting market imperfections

by ownership category. in outside markets (Eun, Kolodny and Scheraga,

So, a higher level of diversity, be it SD or DD, 1996). However, integration costs and cultural

is not a panacea for all types of firms in board problems could undermine these gains. Empirical

strategic decision making. Using a similar typol- results have been somewhat mixed (Cakici, Hessel

ogy as in Sur (2009), we argue that firms charac- and Tandon, 1991; Eun, Kolodny and Scheraga,

terized by high ownership concentration such as 1996; Faccio, McConnel and Stolin, 2006).

family firms will benefit more from low levels than Technology-based industries are characterized by

from high levels of SD and DD. high growth potential and high risk due to the

Introducing DD in the board at low levels may uncertainty associated with the complexity of

bring new ideas and perspectives to the directors their activities and the unproven nature of tech-

representing institutions or the controlling family nology used within these companies (Kohers and

without threatening their coherence. In general, Kohers, 2000, 2001). Finally Datta, Pinches and

there are indeed clear advantages to close-knit Narayanan (1992) note that the relatedness,

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

8 W. Ben-Amar et al.

among the acquiring and target firms’ activities, is Table 1. Sample selection

a key determinant of the level of value creation in Raw data from Thomson-SDC 941

their merger. Synergies are indeed easier to Less: income trusts (294)

achieve when the merged firms operate in the Less: overlapped transactions in estimation period (110)

same type of business (Rumelt, 1982). Less: missing returns in CFMRC database (168)

Less: missing predictor variables in SEDAR (80)

Final sample 289

Data and methodology

In this section, we first explain why we selected a

sample of M&As conducted by Canadian firms to M&A performance (dependent variable). M&As

examine the joint effect of ownership and diver- offer the right context within which to test

sity on the success of M&A strategic decisions. the contribution of diversity in governance to

We then present the dependent and independent enhanced decision making. M&A decisions are

variables of our empirical model. strategic, complex and fraught with uncertainty.

Also, complex strategies and decisions of M&As

Institutional setting and sampling procedure are typically under the responsibility of top man-

agement and the board of directors. Given the

The Canadian institutional setting offers a particu-

uncertainties related to both the transaction

larly good ‘laboratory’ to study ownership and

itself and the future integration of the firms

diversity configurations and their joint relation

involved, M&As are likely to reveal disagree-

with performance. With regards to ownership, its

ments among and a greater involvement of board

mix of closely and widely held firms is representa-

members.

tive of corporate ownership around the world

In line with research on the impact of M&As on

(Denis and McConnell, 2003; Faccio and Lang,

shareholders’ wealth, we use the Brown and

2002; La Porta, Lopez-De-Silanes and Shleifer,

Warner (1985) event study methodology to assess

1999). Yet, its mostly voluntary principles-based

the success of M&A strategic decisions.5

approach to corporate governance is significantly

different from the US mostly rules-based approach

(Broshko and Li, 2006) and the resulting manage-

Diversity configuration. If individual director

rial latitude may thus be more conducive to a

characteristics interact to produce the board’s

broader diversity. Our final sample consists of 289

behaviour, their diversity may constitute either a

observations covering 206 acquiring firms. Table 1

stimulus or a challenge (or both) to the board’s

summarizes the sample selection process.

effectiveness and innovativeness. Therefore,

rather than only examining the relationship

Empirical model between directors’ individual characteristics and

The resulting model is described in more detail performance, we combine all dimensions of diver-

later but can be summarized as follows: sity or pluralism discussed earlier into two indices,

SD and DD, to examine their interaction and

CAR it = constant effect on the success of M&A strategic decisions.

+ β1it STATUTORY_DIVERSITY The construction of our diversity indices is

+ β2 it DEMOGRAPHIC_DIVERSITY straightforward. As in prior research that calcu-

+ β3 it INST + β 4 it FAM + β5 it RELSIZE lated governance indices (e.g. Black, Jang and

+ β6 it CASH + β7 it TARGETPUB Kim, 2006; Gompers, Ishii and Metrick, 2003) we

+ β8 it CROSSBORDER

+ β9 it HIGH_TECH + β10 it RELATED

5

where CARit is the cumulative abnormal return This short-window event study methodology is widely

around the announcement date. Dependent and used in previous M&A studies (Bruner, 2002; McWil-

liams and Siegel, 1997; Tuch and O’Sullivan, 2007). It

control variables are described in Table 2. We produces the most statistically reliable evidence on

now turn to discussing both the dependent and whether M&As create value for shareholders (Andrade,

the independent variables. Mitchell and Stafford, 2001).

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 9

Table 2. Description of the ownership and control variables and hypothesized relationships

Hypothesized

relationship

Ownership variables

Widely held firms: dummy variable that equals 1 when there is no dominant shareholder at the 10% threshold or ?

when the largest shareholder is a widely held corporation

Institutional blockholder: dummy variable that equals 1 when the largest shareholder at the 10% threshold is an +

institutional shareholder (for instance, pension funds and mutual fund managers) (INST)

Family firms: dummy variable that equals 1 when the largest shareholder at the 10% threshold is an individual or a +

family (FAM)

Control variables

Relative size of the transaction to the acquiring firm market value prior to the deal announcement – RELSIZE +

Method of payment, binary variable – CASH +

Public status of the target (public or private), binary variable – TARGETPUB –

Cross-border transactions, binary variable – CROSSBORDER ?

Target operating in the high technology sector, binary variable – HIGH-TECH ?

Relatedness of the activities acquirer/target, binary variable – RELATED +

The dependent variable is the cumulative abnormal returns for a three-day window around the M&A announcement date (-1, 0, +1),

CAR.

compute our index scores by adding points for Table 3. Description of the independent variables and construc-

every characteristic that enhances the level of tion of the indexes

diversity of the board. Dichotomous variables Independent variables of Construction of the index

are given values of 0 and 1. As in Dittmar and interest

Mahrt-Smith (2007) and Francoeur, Labelle

Statutory diversity index (SD)

and Sinclair-Desgagné (2008) we split the sample CEO is not chairperson – 0 if CEO is also chairperson;

into terciles for continuous variables to rank binary variable 1 if not

firms’ board diversity levels. These groups then Percentage of independent First tercile: 0 mark

take values of 0, 1 and 2.6 The procedure is sum- directors Second tercile: 1 mark

marized in Table 3. Third tercile: 2 marks

Percentage of outside First tercile: 0 mark

directors ownership Second tercile: 1 mark

(voting rights) Third tercile: 2 marks

Ownership configuration. To take ownership

Percentage of inside First tercile: 0 mark

into consideration, we rely on the same method- directors ownership Second tercile: 1 mark

ology as La Porta, Lopez-De-Silanes and Shleifer (voting rights) Third tercile: 2 marks

(1999) and Faccio and Lang (2002) to measure the Demographic diversity index (DD)

ultimate voting and ownership rights held by the Percentage of women on the First tercile: 0 mark

firm’s largest blockholder. Sample firms are clas- board Second tercile: 1 mark

sified in three groups of owners: widely held, when Third tercile: 2 marks

CEO is a woman – binary 0 if the firm’s CEO is not

there is no dominant owner at the 10% threshold variable a woman; 1 otherwise

level; institutional investor, when the largest Percentage of foreign First tercile: 0 mark

shareholder at the 10% threshold level is a directors (residence is Second tercile: 1 mark

financial institution (e.g. mutual fund, pension outside Canada) Third tercile: 2 marks

fund etc.); and family firms, again when the Directors’ tenure (number of First tercile: 2 marks

years) within the firm Second tercile: 1 mark

largest shareholder at the 10% threshold level is a Third tercile: 0 mark

family.

Control variables. The model controls for

factors that are identified in the literature as potentially affecting stock market returns at the

announcement date of M&A transactions. These

factors have been mentioned earlier, and their

6

For a robustness check, we divided our sample by the expected relationships with performance are

median or in quartiles and obtained similar results. summarized in Table 2.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

10 W. Ben-Amar et al.

Table 4. Descriptive statistics Table 5. Distribution of observations by diversity score

Mean Median Standard Statutory N Demographic N

deviation diversity diversity

Independent variable 0 2 0 42

CAR_mm 0.014*** 0.012 0.078 1 11 1 67

Diversity 2 39 2 87

Statutory 3.758 4 1.423 3 85 3 67

Demographic 1.931 2 1.276 4 58 4 16

5 61 5 8

Ownership 6 26 6 2

Widely held 0.494 0 0.495

7 7

Institutional 0.253 0 0.435

Total 289 289

Family 0.253 0 0.435 Mean 3.8 1.9

Control variables Median 4.0 2.0

Relsize 0.281 0.113 0.469 Standard deviation 1.4 1.3

Cash 0.588 1 0.493

Targetpub 0.28 0 0.45

Crossborder 0.54 1 0.499 Table 6 presents the distribution of SD and DD

High-tech 0.17 0 0.376 by type of ownership. Part (a) shows that firms

Related 0.574 1 0.495

controlled by institutional investors exhibit the

N 289 highest level of SD (average 4.14) among the firms

CAR_mm, cumulative market model abnormal return. of our sample, followed by widely held firms

***p < 0.01. (average 3.68) and family controlled firms (average

level 3.52). Table 6, part (a), also shows that the

difference between SD scores of firms controlled

Results and analyses by institutional investors and the two other groups

Descriptive statistics and univariate analyses is statistically significant. In contrast, family firms

do not seem to differ from widely held firms in the

Table 4 provides descriptive statistics. First, the level of SD. These results suggest that institutional

mean cumulative market model abnormal returns investors promote more intensely the adoption of

(CAR_mm) obtained in the three-day window best practices governance guidelines.

around the announcement date (-1, 0, +1) is posi- Table 6, part (b), compares the level of DD

tive and significant (1.4%, p = 0.01). The average between the three groups of owners. Widely held

SD score is 3.75 and the median is 4.00. Board firms exhibit the highest average DD score (2.14),

DD measures its gender diversity, its cultural and followed by family firms (1.74) and institutional

international exposure and its directors’ experi- investors firms (1.71). The results also show that

ence within the firm. The average DD score is 1.93 the DD level observed in widely held firms is sta-

while the median is 2.00. Results also show that tistically higher than the level achieved by family

42.2% of the firms in our sample are widely held, and institutional investors firms (at the 10% level).

25.3% are controlled by an institutional investor Taken together, the results presented in Table 6

and 25.3% are controlled by a family. The propor- show that owner identity has a significant effect

tion of family firms in our sample is comparable on the diversity configuration of firms.

with what it is in previous Canadian studies. Table 7 presents a matrix of correlations

The average relative deal size to the bidder between independent and explanatory variables.

market value is 28.1%, and 58.8% of the transac- The highest correlation coefficient is –0.338

tions are paid exclusively in cash. Moreover, 28% (correlation between family and institutional

of the transactions involve publicly held targets dummies). These results indicate that multicolline-

while 54% involve foreign targets. Table 4 also arity is not a serious problem in our multivariate

shows that 17.0% of the acquired companies analyses.

belong to the high-tech industry and 57.4% of the

transactions involve an acquirer and a target from

Multivariate analyses

related industries (same three-digit SIC code).

Table 5 presents the distribution of the SD and Table 8 presents the results of three ordinary least

DD indices. squares regressions testing the three hypotheses of

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 11

Table 6. Descriptive statistics and comparisons of group means by type of ownership

One-way ANOVA Scheffe multiple group comparisons:

row mean – column mean (p value)

Ownership Mean Standard deviation Frequency Widely held Institutional

(a) Statutory diversity

Widely held 3.6853 1.4013 143

Institutional 4.1370 1.2618 73 0.4517

(0.085)*

Family 3.5205 1.5555 73 –0.1648 –0.6164

(0.719) (0.032)**

Total 3.7578 1.4228 289

p value 3.87**

(b) Demographic diversity

Widely held 2.1399 1.1903 143

Institutional 1.7123 1.1605 73 –0.4275

(0.064)*

Family 1.7397 1.4816 73 –0.4001 0.0274

(0.090)* (0.991)

Total 1.9308 1.2756 289

p value 3.89**

*p < 0.10; **p < 0.05; ***p < 0.01.

our theoretical framework of Figure 1 and includ- relationship between board diversity and M&A

ing the control variables. In regression 1 we test for performance. The result of regression 2 shows a

a linear relationship between SD and DD non-linear relationship between the DD of the

(Hypothesis 1) and M&A financial performance. board members and CAR at the time of M&A

In regression 2 we consider that the tested relation- announcement which is in line with our second

ships between performance and board SD and hypothesis. The coefficient of the DD variable is

especially DD (Hypothesis 2) may not be linear. negative and statistically significant whereas the

Thus, we include the squared values for board coefficient of its squared value (DD2) is positive

diversity variables to test for the existence of and significant, which is consistent with an asym-

an inflexion point. Finally, in regression 3 we intro- metric U-shaped curve. Figure 2 graphically rep-

duce ownership dummies to test our third hy- resents the relationship between DD and M&A

pothesis of a joint interactive effect of board performance. It suggests that introducing DD on

diversity variables and owners’ identity on M&A the board of directors has at first a negative effect

performance. on the success of acquisition decisions, probably

As suggested by Aiken and West (1991), the because the benefits of DD are counterbalanced by

independent variables (SD and DD) are mean- problems related to integration difficulties. But

centred to attenuate the problem of multicolline- beyond a certain level,7 DD starts enhancing the

arity in our regression models when introducing board’s knowledge base and ability to deal with

quadratic terms. We also tested for multicollinear- complex strategic decisions and results in better

ity among our explanatory variables by computing M&A decisions. In total, these results confirm our

the variance inflation factors (VIF) for each of the second hypothesis.

regression coefficients. As presented in Table 8, the Regression 3 where ownership is introduced

highest VIF value in our models is 2.13, which is shows the same relation between DD and board

well below the cut-off value of 10 suggested by strategic decisions. Institutional and family own-

Neter, Wasserman and Kutner (1985). ership also have a significant positive impact on

Results of the first regression indicate that the the dependent variable over and above the widely

levels of SD or DD of the board of directors are not held firms. Figure 3 summarizes Table 8’s results

statistically related to the financial success of

M&As. We then use two quadratic regressions to 7

Technically, this level corresponds to the inflexion point

test the more plausible hypothesis of a non-linear of the U-shaped curve, a value of 1.1.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

12 W. Ben-Amar et al.

Table 8. Regressions of the acquiring firm’s CAR around the

FAM, dummy variable that equals 1 when the largest shareholder at the 10% threshold is an individual or a family; RELSIZE, value of transaction/acquirer’s market value ; CASH = 1

All correlations are based on the full sample of 289 observations. INST, dummy variable that equals 1 when the largest shareholder at the 10% threshold is an institutional shareholder;

if method of payment is cash only, 0 otherwise; TARGETPUB = 1 if target is publicly traded, 0 if target is private; CROSSBORDER = 1 if target nation is not Canada, 0 if it is;

HIGH-TECH

M&A announcement on their diversity index

0.072

Regression 1 Regression 2 Regression 3

SD 0.0023 0.0022 0.0013

(0.483) (0.486) (0.784)

CROSSBORDER

SD2 -0.0004 0.0044

0.158***

(0.763) (0.119)

0.020

DD -0.0051 -0.0066 -0.0177

(0.180) (0.090)* (0.008)***

HIGH-TECH = 1 if target is operating in the high tech industry; RELATED = 1 if three-digit SIC code of acquirer and target are the same, 0 if not.

DD2 0.0030 0.0056

(0.072)* (0.049)**

INST 0.0277

TARGETPUB

(0.046)**

–0.212***

0.148**

–0.056

FAM 0.0600

(0.002)***

SD_INST -0.0056

(0.439)

SD2_INST -0.0072

–0.308***

0.187***

CASH

(0.060)*

–0.072

0.034

DD_INST 0.0225

(0.014)**

DD2_INST 0.0046

–0.243***

(0.345)

RELSIZE

0.064

–0.059

–0.023

0.088

SD_FAM 0.0051

(0.523)

SD2_FAM -0.0083

(0.024)**

0.179***

–0.150**

–0.128**

DD_FAM 0.0242

FAM

–0.045

0.010

–0.008

(0.022)**

DD2_FAM -0.0090

(0.029)**

RELSIZE 0.0230 0.0224 0.0222

–0.338***

0.130**

–0.145**

–0.118**

INST

(0.082)* (0.073)* (0.082)*

–0.044

–0.029

0.049

CASH -0.0007 -0.0008 0.0028

(0.952) (0.942) (0.806)

TARGETPUB -0.0360 -0.0343 -0.0256

–0.100*

(0.002)*** (0.002)*** (0.032)**

–0.087

0.022

–0.046

0.040

0.086

0.017

0.052

Table 7. Pairwise correlations between the study’s variables

DD

CROSSBORDER 0.0143 0.0135 0.0157

(0.114) (0.134) (0.089)*

HIGH-TECH 0.0121 0.0128 0.0101

0.155***

–0.167***

(0.436) (0.412) (0.491)

–0.120**

–0.138**

SD

–0.097

0.027

0.068

0.032

0.090

RELATED 0.0040 0.0053 0.0024

(0.664) (0.562) (0.788)

CONSTANT 0.0069 0.0008 -0.0239

*p < 0.10; **p < 0.05; ***p < 0.01.

(0.685) (0.950) (0.122)

–0.218***

CAR_mm

0.131**

0.121**

0.123**

Prob > F 0.004*** 0.005*** 0.000***

0.030

–0.083

0.076

0.038

0.084

0.012

R2 0.087 0.094 0.166

N 289 289 289

Mean VIF 1.11 1.11 2.13

CROSSBORDER

Dependent variable is the market model cumulative abnormal

TARGETPUB

returns over the (-1, +1) window. SD and DD are mean-centred

HIGH-TECH

RELATED

(diversity index – mean of diversity index) in regressions 2 and 3;

RELSIZE

SD2, SD squared; DD2, DD squared. Variables with under-

CASH

INST

FAM

scores represent interactions.

DD

SD

p values in parentheses: *p < 0.10; **p < 0.05; ***p < 0.01.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 13

few SD variables aimed at having the differences

in incentives between outsiders and insiders rep-

resented on the board. Our research has three

important distinctive features. First, we distin-

guish SD, either mandated or normatively recom-

mended to monitor management, from DD which

is related to the resource provision function of

board members and refers to their individual

background characteristics (in this case gender,

experience, nationality and culture). We propose

indices to capture the effects of either SD or DD.

The second important feature is the investiga-

tion of the effect of ownership. Multivariate

analyses are first conducted without including the

Figure 2. Relationship between DD and M&A performance ownership variables. In this first model, the influ-

ence of board diversity is barely noticeable, and

relative to the moderating influence of ownership more generally not significant. When including

on board diversity and strategic decision making the ownership variables, the picture is completely

as measured by M&A success. As predicted by different. Ownership does definitely make a dif-

Hypothesis 3, in firms whose largest shareholder ference. In our analyses, we show that diversity

is an institutional investor, high levels of SD seem can have a generalized effect and a more specific

to be detrimental to the quality of board strategic effect depending on the type of ownership.

decisions. The effect is the same and even a little The third feature is that we examine decisions

more pronounced in family firms. of M&As, which are clearly board responsibility.

The effects of low levels of DD in both institu- Therefore, we believe that the validity of the

tional investor and family dominated firms are findings is much greater than when general firm

positive. But higher levels of DD are detrimental performance is considered.

to family firms. Therefore, even though the We developed a theoretical framework summa-

hypothesis holds only partially for institutional rized in Figure 1 and generated three hypotheses.

investor dominated firms, it holds completely for The first hypothesis concerning the effect of SD on

family dominated firms. board strategic decisions is not confirmed. We

Looking at control variables, several of the explain this result by the fact that SD has become a

extant literature traditional findings are con- must during the study period and no longer dis-

firmed. In particular, the public status of the target criminates among firms. There are also nuances to

firm produces a negative impact on the dependent take into account. We can state unambiguously

variable consistently across all the regression that, in the case of Canadian M&A performance,

models. In agreement with the limited competition there is no generalized board SD effect, which

hypothesis (Chang, 1998), our results suggest that appears to go against generally accepted corporate

acquiring companies are likely to pay lower premi- governance ‘best’ practices. Moreover, SD is less

ums and earn higher returns for deals involving favourable to institutional and family owned firms

private targets than in the case of publicly listed than to widely held firms. This implies that it is

ones. Table 8 also shows a positive association appropriate to insist on SD or fiduciary govern-

between the target size, relative to the bidder, and ance when mostly dealing with widely held firms as

CARs around announcement date. These results in the USA, but that SD appears to have a limited

are consistent with the literature findings. effect when shareholding is more concentrated.

This is an important finding both for practical and

academic reasons. It confirms that one has to pay

Discussion and conclusion attention to the premises of agency theory and

ensure that they apply.

The effect of board diversity on performance has Hypotheses 2 and 3 have been confirmed. DD

been the topic of a large number of studies. Most has a general negative effect at lower levels and the

research, however, has focused on the effect of a effect reverses at higher levels. This suggests that

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

14 W. Ben-Amar et al.

Figure 3. Path diagrams: influence of diversity, ownership and their interaction on board strategic decisions

Note: These results are relative to widely held firms.

there is a threshold level beyond which the effect between control and freedom when the time

becomes positive. There is also a more specific comes to select board members. Good governance

effect of DD depending on the ownership configu- is probably more about the building of such a

ration. At lower levels, it is positive for institu- balance than the simple implementation of pre-

tional owners and families, but at higher levels specified rules of statutory independence.

family firms are affected adversely. The coherence, Our findings apply to the Canadian context.

trust and long-term vision of these close-knit Nevertheless, they may have a more general

boards (Eddleston et al., 2010; Le Breton-Miller value, from a public policy perspective. In par-

and Miller, 2006; Steier, 2001) is lessened when ticular, the complex and non-linear relationship

subjected to higher levels of DD. Family firms are between board diversity and board strategic

founded on a belief in the value of a homogeneous decisions provides some support for the

management structure. These firms tend to principles-based approach in governance used in

perform best under conditions of low DD as they several other countries such as for instance

do not value diversity (van Knippenberg, Haslam Great Britain and Australia. Rather than provid-

and Platow, 2007).8 ing strict rules, regulatory authorities should

To sum up, what do these findings mean? The allow companies to design the composition of

effect of diversity on firms’ performance is multi- the board according to their organizational and

factorial. Several aspects have to be considered to financial characteristics and reach an ‘optimal

get a clear picture. Board diversity does not have level’ of diversity.

either an overall positive or negative effect. Its This study has limitations. First, we use an index

effect depends on contextual factors and in par- to assess diversity on the board. Lumping together

ticular on ownership configurations. Further- several variables in a single index may have unex-

more, it does not have a linear effect. Diversity at pected drawbacks. When variables work at cross-

lower levels can be favourable for some types of purpose, we may end up with effects being hidden

firms and unfavourable for others. At higher rather than revealed. Nevertheless, we took

levels, effects change. The general picture that comfort in the theoretical belief that all the DD

comes out is that a balance should be struck variables considered are believed to have positive

effects on the quality of board decisions. Second,

8

We thank one of the anonymous reviewers for pointing although our short-term window (i.e. three days

this out. around the announcement date) has often been

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 15

used in previous research (e.g. Bruner, 2002; Carter, D. A., B. J.Simkins and W. G. Simpson (2003). ‘Corpo-

McWilliams and Siegel, 1997) it may not fully rate governance, board diversity and firm value’, Financial

Review, 38, pp. 33–53.

reflect total value creation for M&As. Future Chang, S. (1998). ‘Takeovers of privately held targets, methods

research should investigate the relationship of payment and bidder returns’, Journal of Finance, 53,

between board diversity and the long-term success pp. 773–784.

of strategic decisions such as M&As. Chau, G. and S. J. Gray (2010). ‘Family ownership, board

independence and voluntary disclosure: evidence from Hong

Kong’, Journal of International Accounting, Auditing and

Taxation, 19, pp. 93–109.

References Chen, H. L. and W. T. Hsu (2009). ‘Family ownership, board

independence, and R&D investment’, Family Business

Adams, R. and D. Ferreira (2009). ‘Women in the boardroom Review, 22, pp. 347–362.

and their impact on governance and performance’, Journal of Choi, J. J., S. W. Park and S. S. Yoo (2007). ‘The value of

Financial Economics, 94, pp. 291–309. outside directors: evidence from corporate governance reform

Adams, S., M. A. Gupta and J. D. Leeth (2009). ‘Are female in Korea’, Journal of Financial and Quantitative Analysis, 42,

executives over-represented in precarious leadership posi- pp. 941–962.

tions?’, British Journal of Management, 20, pp. 1–12. Daily, C. M., C. S. Trevis and D. R. Dalton (1999). ‘A decade

Aiken, L. S. and S. G. West (1991). Multiple Regression: Testing of corporate women: some progress in the boardroom, none

and Interpreting Interactions. Newbury Park, CA: Sage. in the executive suite’, Strategic Management Journal, 20,

Alderfer, C. P. (1986). ‘The invisible director on corporate pp. 93–99.

boards’, Harvard Business Review, 64, pp. 38–52. Dalton, D. R., C. M. Daily, A. E. Ellstrand and J. L. Johnson

Anderson, R. C. and D. M. Reeb (2004). ‘Board composition: (1998). ‘Meta-analytic reviews of board composition, leader-

balancing family influence in S&P500 firms’, Administrative ship structure, and financial performance’, Strategic Manage-

Science Quarterly, 49, pp. 209–237. ment Journal, 19, pp. 269–290.

Andrade, G., M. Mitchell and E. Stafford (2001). ‘New evidence Datta, D. K., G. E. Pinches and V. K. Narayanan (1992).

and perspectives on mergers’, Journal of Economic Perspec- ‘Factors influencing wealth creation from mergers and acqui-

tives, 15, pp. 103–120. sitions: a meta-analysis’, Strategic Management Journal, 13,

Asquith, P., R. F. Bruner and D. W. Mullins Jr (1983). ‘The pp. 67–84.

gains to bidding firms from mergers’, Journal of Financial Davis, J. H., F. D. Schoorman and L. Donaldson (1997).

Economics, 11, pp. 121–140. ‘Toward a stewardship theory of management’, Academy of

Barney, J. B. (1991). ‘Firm resources and sustained competitive Management Review, 22, pp. 20–47.

advantage’, Journal of Management, 17, pp. 99–120. Denis, D. K. and J. J. McConnell (2003). ‘International corpo-

Bhagat, S. and B. Black (2002). ‘The non-correlation between rate governance’, Journal of Financial and Quantitative Analy-

board independence and long-term firm performance’, sis, 38, pp. 1–36.

Journal of Corporation Law, 27, pp. 231–273. Dittmar, A. and J. Mahrt-Smith (2007). ‘Corporate governance

Bilimoria, D and S. K. Piderit (1994). ‘Qualifications of corpo- and the value of cash holdings’, Journal of Financial Econom-

rate board committee members’, Group and Organization ics, 83, pp. 599–634.

Management, 19, pp. 334–362. Dyer, W. G. (2006). ‘Examining the family effect on firm per-

Black, B. S., H. Jang and W. Kim (2006). ‘Does corporate formance’, Family Business Review, 19, pp. 253–273.

governance predict firms’ market values? Evidence from Eddleston, K., J. Chrisman, L. Steier and J. Chua (2010).

Korea’, Journal of Law, Economics and Organization, 22, ‘Governance and trust in family firms: an introduction’,

pp. 366–413. Entrepreneurship Theory and Practice, 34, pp. 1043–

Broshko, E. B. and K. Li (2006). ‘Playing by the rules: compar- 1056.

ing principles-based and rules-based corporate governance Erhardt, N. L., J. D. Werbel and C. B. Shrader (2003). ‘Board of

in Canada and the U.S.’, Canadian Investment Review, 19, director diversity and firm financial performance’, Corporate

pp. 18–23. Governance: An International Review, 11, pp. 102–111.

Brown, S. J. and J. B. Warner (1985). ‘Using daily stock returns: Eun, C. S., R. Kolodny and C. Scheraga (1996). ‘Cross-border

the case of event studies’, Journal of Financial Economics, 14, acquisitions and shareholder wealth: tests of the synergy and

pp. 3–31. internalization hypotheses’, Journal of Banking and Finance,

Bruner, R. F. (2002). ‘Does M&A pay? A survey of evidence 20, pp. 1559–1582.

for the decision maker’, Journal of Applied Finance, 12, Faccio, M. and L. H. P. Lang (2002). ‘The ultimate ownership

pp. 48–68. of western European corporations’, Journal of Financial Eco-

Cakici, N., S. A. Hessel and K. Tandon (1991). ‘Foreign acqui- nomics, 65, pp. 365–395.

sitions in the United States and the effect on shareholder Faccio, M., J. McConnel and D. Stolin (2006). ‘Returns to

wealth’, Journal of International Financial Management and acquirers of listed and unlisted targets’, Journal of Financial

Accounting, 3, pp. 39–60. and Quantitative Analysis, 41, pp. 197–220.

Canella A. A. Jr, J. H. Park and H. U. Lee (2008). ‘Top man- Fama, E. F. (1980). ‘Agency problems and the theory of the

agement team functional background diversity and firm per- firm’, Journal of Political Economy, 88, pp. 288–307.

formance: examining the roles of team member colocation Fama, E. F. and M. C. Jensen (1983). ‘Separation of ownership

and acquisition performance’, Academy of Management and control’, Journal of Law and Economics, 26, pp. 301–

Journal, 51, pp. 768–784. 325.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

16 W. Ben-Amar et al.

Finkelstein, S. and D. C. Hambrick (1988). ‘Chief executive traded, family-controlled firms: the case of diversification’,

compensation: a synthesis and reconciliation’, Strategic Man- Entrepreneurship Theory and Practice, 32, pp. 1007–1026.

agement Journal, 9, pp. 543–558. Katz, R. (1982). ‘The effects of group longevity on project

Francoeur, C., R. Labelle and B. Sinclair-Desgagné (2008). communication and performance’, Administrative Science

‘Gender diversity in corporate governance and top manage- Quarterly, 27, pp. 81–104.

ment’, Journal of Business Ethics, 81, pp. 83–95. Kesner, I. F. (1988). ‘Directors’ characteristics and committee

Fuller, K., J. Netter and M. Stegemoller (2002). ‘What do membership: an investigation of type, occupation, tenure,

returns to acquiring firms tell us? Evidence from firms that and gender’, Academy of Management Journal, 31, pp. 66–

make many acquisitions’, Journal of Finance, 57, pp. 1763– 84.

1793. Klein, P., D. Shapiro and J. Young (2005). ‘Corporate govern-

Golden, B. R. and E. J. Zajac (2001). ‘When will boards influ- ance, family ownership and firm value: the Canadian evi-

ence strategy? Inclination ¥ power = strategic change’, Stra- dence’, Corporate Governance: An International Review, 13,

tegic Management Journal, 22, pp. 1087–1111. pp. 769–784.

Gompers, P., J. Ishii and A. Metrick (2003). ‘Corporate govern- van Knippenberg, D., S. A. Haslam and M. J. Platow (2007).

ance and equity prices’, Quarterly Journal of Economics, 118, ‘Unity through diversity: value-in-diversity beliefs, work

pp. 107–155. group diversity, and group identification’, Group Dynamics:

Hambrick, D. C. (2001). ‘Better boards: the equity answers’, Theory, Research, and Practice, 11, pp. 207–222.

Chief Executive, 165, p. 58. Kohers, N. and T. Kohers (2000). ‘The value creation potential

Hambrick, D. C. and P. A. Mason (1984). ‘Upper echelons: the of high-tech mergers’, Financial Analysts Journal, 56, pp.

organization as a reflection of its top managers’, Academy of 40–50.

Management Review, 9, pp. 193–206. Kohers, N. and T. Kohers (2001). ‘Takeovers of technology

Hambrick, D., T. Cho and M. Chen (1996). ‘The influence of firms: expectations vs. reality’, Financial Management, 29, pp.

top management team heterogeneity on firms’ competitive 5–30.

moves’, Administrative Science Quarterly, 41, pp. 659–685. Kosnik, R. D. (1990). ‘Effects of board demography and direc-

Hambrick, D. C., A. v. Werder and E. J. Zajac (2008). ‘New tors’ incentives on corporate greenmail decisions’, Academy

directions in corporate governance research’, Organization of Management Journal, 33, pp. 129–150.

Science, 19, pp. 381–385. La Porta, R., F. Lopez-De-Silanes and A. Shleifer (1999). ‘Cor-

Haslam, S. A., M. K. Ryan, C. Kulich, G. Trojanowski and C. porate ownership around the world’, Journal of Finance, 54,

Atkins (2010). ‘Investing with prejudice: the relationship pp. 471–517.

between women’s presence on company boards and objective Le Breton-Miller, I. and D. Miller (2006). ‘Why do some family

and subjective measures of company performance’, British businesses out-compete? Governance, long-term orientations,

Journal of Management, 21, pp. 484–497. and sustainable capability’, Entrepreneurship Theory and

Hermalin, B. E. and M. S. Weisbach (2001). ‘Board of directors Practice, 30, pp. 731–746.

as an endogenously determined institution: a survey of the Luis-Carnicer, P., A. Martínez-Sanchez and M. Pérez-Pérez

economic literature’, National Bureau of Economic Research (2008). ‘Gender diversity in management: curvilinear rela-

Working Paper 8161. tionships to reconcile findings’, Gender in Management: An

Hillman, A. J. and T. Dalziel (2003). ‘Boards of directors and International Journal, 23, pp. 583–597.

firm performance: integrating agency and resource depend- Manzoni, J. F., P. Strebel and J. L. Barsoux (2010). ‘Why diver-

ence perspectives’, Academy of Management Review, 28, sity can backfire on company boards’, Wall Street Journal, 25

pp. 383–396. January.

Hillman, A. J., G. Nicholson and C. Shropshire (2008). ‘Direc- McDonald, M. L., J. D. Westphal and M. E. Graebner (2008).

tors’ multiple identities, identification, and board monitoring ‘What do they know? The effect of outside director acquisi-

and resource provision’, Organization Science, 19, pp. 441– tion experience on firm acquisition performance’, Strategic

456. Management Journal, 29, pp. 1155–1177.

Hillman, A. J., M. C. Withers and B. J. Collins (2009). McNulty, T. and A. Pettigrew (1999). ‘Strategists on the board’,

‘Resource dependence theory: a review’, Journal of Manage- Organization Studies, 20, pp. 47–74.

ment, 34, pp. 1404–1411. McWilliams, A. and D. Siegel (1997). ‘Event studies in manage-

Huang, Y. and R. Walking (1987). ‘Target abnormal returns ment research: theoretical and empirical issues’, Academy of

associated with acquisition announcements: payment, acqui- Management Journal, 40, pp. 626–657.

sition form and managerial resistance’, Journal of Financial Milliken, F. and L. Martins (1996). ‘Searching for common

Economics, 19, pp. 329–349. threads: understanding the multiple effects of diversity in

Jehn, K. A. (1995). ‘A multimethod examination of the benefits organizational groups’, Academy of Management Review, 21,

and detriments of intragroup conflict’, Administrative Science pp. 402–434.

Quarterly, 40, pp. 256–282. Molz, R. (1988). ‘Managerial domination of boards of directors

Jensen, M. C. and W. H. Meckling (1976). ‘Theory of the firm: and financial performance’, Journal of Business Research, 16,

managerial behavior, agency costs and ownership structure’, pp. 235–249.

Journal of Financial Economics, 3, pp. 305–360. Molz, R. (1995). ‘The theory of pluralism in corporate govern-

John, K. and L. W. Senbet (1998). ‘Corporate governance and ance: a conceptual framework and empirical test’, Journal of

board effectiveness’, Journal of Banking and Finance, 22, Business Ethics, 14, pp. 789–804.

pp. 371–403. Neter, J., W. Wasserman and M. H. Kutner (1985). Applied

Jones, C. D., M. Makri and L. R. Gomez-Mejia (2008). Linear Statistical Models: Regression, Analysis of Variance,

‘Affiliate directors and perceived risk bearing in publicly and Experimental Design. Homewood, IL: Richard Irwin.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

What Makes Better Boards? 17

Oxelheim, L. and T. Randøy (2003). ‘The impact of foreign Sur, S. (2009). ‘For whom the firm toils: a thesis investigating

board membership on firm value’, Journal of Banking and the ownership, board and performance linkages’. Unpub-

Finance, 27, pp. 2369–2392. lished doctoral dissertation, John Molson School of Business,

Pelled, L. H., K. M. Eisenhardt and K. R. Xin (1999). ‘Explor- Concordia University, Montreal.

ing the black box: an analysis of work group diversity, con- Travlos, N. G. (1987). ‘Corporate takeover bids, method of

flict, and performance’, Administrative Science Quarterly, 44, payment, and bidding firms’ stock return’, Journal of Finance,

pp. 1–28. 42, pp. 943–963.

Raatikainen, P. (2002). ‘Contributions of multiculturalism to Tsui, A. S., T. D. Egan and C. A. O’Reilly (1992). ‘Being dif-

the competitive advantage of an organisation’, Singapore ferent: relational demography and organizational attach-

Management Review, 24, pp. 81–85. ment’, Administrative Science Quarterly, 37, pp. 549–579.

Ruigrok, W., S. Peck and S. Tacheva (2007). ‘Nationality and Tuch, C. and N. O’Sullivan (2007). ‘The impact of acquisitions

gender diversity on Swiss corporate boards’, Corporate Gov- on firm performance: a review of the evidence’, International

ernance: an International Review, 15, pp. 546–557. Journal of Management Reviews, 9, pp. 141–170.

Rumelt, R. (1982). ‘Diversification strategy and profitability’, Vafeas, N. (2003). ‘Length of board tenure and outside director

Strategic Management Journal, 3, pp. 359–369. independence’, Journal of Business Finance and Accounting,

Selznick, P. (1990). The Moral Commonwealth. Los Angeles, 30, pp. 1043–1064.

CA: University of California Press. Watson, E., K. Kumar and L. Michaelsen (1993). ‘Cultural

Shrader, C. B., V. B. Blackburn and P. Iles (1997). ‘Women in diversity’s impact on interaction process and performance:

management and firm financial performance: an exploratory comparing homogeneous and diverse task groups’, Academy

study’, Journal of Managerial Issues, 9, pp. 355–372. of Management Journal, 36, pp. 590–603.

Steier, L. (2001). ‘Family firms, plural forms of governance, Westphal, J. D. (1999). ‘Collaboration in the boardroom:

and the evolving role of trust’, Family Business Review, 14, behavioural and performance consequences of CEO-board

pp. 353–368. social ties’, Academy of Management Journal, 42, pp. 7–24.

Walid Ben-Amar is Associate Professor of Accounting at the Telfer School of Management at the

University of Ottawa. He holds a PhD in accounting from HEC Montreal. His research interests

include corporate governance, mergers and acquisitions and corporate disclosure strategies. He has

published his work in academic journals such as Journal of Business Finance and Accounting, Cana-

dian Journal of Administrative Sciences and International Journal of Managerial Finance.

Claude Francoeur is CGA Associate Professor in Strategic Financial Information at HEC Montreal.

He earned a PhD in finance at the Université du Québec à Montréal. His research interests include

corporate governance and social responsibility, mergers and divestitures and financial reporting

quality. He has published in journals such as Journal of Business Ethics, Canadian Journal of Admin-

istrative Sciences and International Journal of Managerial Finance. He sits on the editorial board of

Contemporary Accounting Research.

Taïeb Hafsi is the Walter J. Somers Professor of International Strategic Management at HEC

Montreal. He has written numerous papers and books dealing with strategic management and change

in situations of complexity. He holds a Master of Science degree in management from the Sloan

School of Management at the Massachusetts Institute of Technology, Boston, and a Doctorate in

Business Administration from Harvard Business School.

Réal Labelle is Professor of Accounting and Ethics at HEC Montreal and holds the Stephen A.

Jarislowsky Chair in governance. He served as President of the Canadian Accounting Academic

Association and the International Academic Association of Governance. His research interests

mainly focus on governance, gender diversity, ethics and financial accounting. He has published

several peer reviewed book chapters and papers in among others Contemporary Accounting Research,

Journal of Business Ethics, Canadian Journal of Administrative Sciences and European Accounting

Review.

© 2011 The Author(s)

British Journal of Management © 2011 British Academy of Management.

You might also like

- Study of leader member relationship and emotional intelligence in relation to change in preparedness among middle management personnel in the automobile sectorFrom EverandStudy of leader member relationship and emotional intelligence in relation to change in preparedness among middle management personnel in the automobile sectorNo ratings yet