You might also like

- Taxation and Income DistributionDocument23 pagesTaxation and Income DistributionNateNo ratings yet

- EPCS47992-0®2020030180172®®®-72.142g : Actual - !' "6Document1 pageEPCS47992-0®2020030180172®®®-72.142g : Actual - !' "6Adam MamboNo ratings yet

- Bai 2Document4 pagesBai 2khanginvest03No ratings yet

- Codigo Iso 4406Document4 pagesCodigo Iso 4406Patricia MenaNo ratings yet

- Tiempo (H) PP (Increm. MM) Intensidad (MM/H) FT FT (Tasa Inf Potencial)Document7 pagesTiempo (H) PP (Increm. MM) Intensidad (MM/H) FT FT (Tasa Inf Potencial)VictoriaSantosNo ratings yet

- Gtp38r CompDocument1 pageGtp38r Compgabe.sotoNo ratings yet

- Red de Agua Fría Sin Bomba, (Acometida de La Calle)Document5 pagesRed de Agua Fría Sin Bomba, (Acometida de La Calle)María Belén MaldonadoNo ratings yet

- Potential EnergyDocument4 pagesPotential EnergyshahqazwsxNo ratings yet

- Ed sq2 3ph 200 60 s2 15 enDocument2 pagesEd sq2 3ph 200 60 s2 15 ensáng nguyễnNo ratings yet

- Table2 5Document3 pagesTable2 5Alexander 'Tory' HinchliffeNo ratings yet

- ComparisonDocument2 pagesComparisonMuhammad AliNo ratings yet

- Comparison Capacitance Balance For EveryoneDocument2 pagesComparison Capacitance Balance For EveryoneMuhammad AliNo ratings yet

- Performance CheckDocument61 pagesPerformance CheckOscar LosadaNo ratings yet

- Econometrics Report, Salvatore IngenitoDocument13 pagesEconometrics Report, Salvatore IngenitoChi-Chi ArisNo ratings yet

- Real Options Exercis - WeGig-2Document17 pagesReal Options Exercis - WeGig-2Anirudh SinghNo ratings yet

- Page 71 IV GraphDocument4 pagesPage 71 IV Graphrosemarymanoj.xNo ratings yet

- Quality Assurance: QP 7.2 S03 Form 7 Capability of Measurement Processes Procedure 2 程序2 (Gauge R&R)Document20 pagesQuality Assurance: QP 7.2 S03 Form 7 Capability of Measurement Processes Procedure 2 程序2 (Gauge R&R)cong daNo ratings yet

- 2D Frame Analysis: Analysis of A 2D Frame Subject To Distributed Loads, Point Loads and MomentsDocument26 pages2D Frame Analysis: Analysis of A 2D Frame Subject To Distributed Loads, Point Loads and MomentsShadin Asari ArabaniNo ratings yet

- 2D Frame Analysis: Analysis of A 2D Frame Subject To Distributed Loads, Point Loads and MomentsDocument26 pages2D Frame Analysis: Analysis of A 2D Frame Subject To Distributed Loads, Point Loads and MomentsChris LuNo ratings yet

- SL No Description No L B D CF Quantity RemarkDocument11 pagesSL No Description No L B D CF Quantity RemarkhasiljiNo ratings yet

- Book1 (AutoRecovered)Document5 pagesBook1 (AutoRecovered)Claret AmorNo ratings yet

- Alex Gabriel Choque - Cerchas 3dDocument2 pagesAlex Gabriel Choque - Cerchas 3dIsmael CopaNo ratings yet

- Crane Productivity Review: Mth:Sep'09 Location: XXXXX Category-80T Crawler Crane - 6 NosDocument16 pagesCrane Productivity Review: Mth:Sep'09 Location: XXXXX Category-80T Crawler Crane - 6 NosdcsekharNo ratings yet

- 2021 05 16 5500063616Document4 pages2021 05 16 5500063616karely jackson lopezNo ratings yet

- Data Analisis ArchimedesDocument6 pagesData Analisis ArchimedesAkhmd RdlNo ratings yet

- Tarea V - Alfredo NororiDocument24 pagesTarea V - Alfredo NororiALFREDO ANTONIO NORORI ARIASNo ratings yet

- Viscosity Converting ChartDocument3 pagesViscosity Converting ChartMaria Victoria Morales GalindezNo ratings yet

- Unidades Vendidas 120 120 120 120 120 Precio de Venta 3 3 3 3 3 Costo Unitario 1.8 1.8 1.8 1.8 1.8Document11 pagesUnidades Vendidas 120 120 120 120 120 Precio de Venta 3 3 3 3 3 Costo Unitario 1.8 1.8 1.8 1.8 1.8Juan MaldiñigNo ratings yet

- 2 PutrajayaDocument32 pages2 PutrajayaAiman Ariffin NordinNo ratings yet

- MatricialDocument28 pagesMatricialvanesa NievesNo ratings yet

- Gantt de Inversion GeneralDocument6 pagesGantt de Inversion GeneralJORGE MACHADONo ratings yet

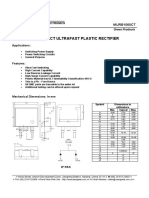

- Murb1060Ct Ultrafast Plastic Rectifier: Sangdest Microelectronics Green ProductsDocument5 pagesMurb1060Ct Ultrafast Plastic Rectifier: Sangdest Microelectronics Green ProductsJOHN BRICCO A. MATACSILNo ratings yet

- Fecha Precio Fecha Precio Fecha: Activo 1Document5 pagesFecha Precio Fecha Precio Fecha: Activo 1Alexis ClavijoNo ratings yet

- 4Q2020 Fullbook enDocument39 pages4Q2020 Fullbook enVincentNo ratings yet

- LTO 40AH CY - DatasheetDocument4 pagesLTO 40AH CY - DatasheetCorinne LawrenceNo ratings yet

- Case 1Document4 pagesCase 1imi.imtenanNo ratings yet

- Circuitos RLC To ShareDocument5 pagesCircuitos RLC To ShareAGR AGRNo ratings yet

- "NRTL" Etanol-Tolueno: Diagrama "P, X, Y"Document22 pages"NRTL" Etanol-Tolueno: Diagrama "P, X, Y"Zofi MarinNo ratings yet

- Account Summary For Account Number 169441334-8: Electric BillDocument2 pagesAccount Summary For Account Number 169441334-8: Electric BillMary Louise50% (2)

- Defect RatioDocument4 pagesDefect RatioMOBEX REFURBNo ratings yet

- Lec1 17Document39 pagesLec1 17RajulNo ratings yet

- 4 Units: Wali Bhai (Inara Garden)Document2 pages4 Units: Wali Bhai (Inara Garden)salmansaleemNo ratings yet

- Catalog Contactoare - Relee Termice Mitsubishi PDFDocument44 pagesCatalog Contactoare - Relee Termice Mitsubishi PDFNicuNo ratings yet

- Incline Exp.Document5 pagesIncline Exp.Yahia Abou-ShoshaNo ratings yet

- Estructuras 1: Dx Dy θyDocument28 pagesEstructuras 1: Dx Dy θykrenzhitaNo ratings yet

- 財管作業Document5 pages財管作業1 1No ratings yet

- Adobe Scan 01 Dec 2023Document1 pageAdobe Scan 01 Dec 2023paarvatiagencyNo ratings yet

- M/S Vivek Enterprsies: Tmujb T - 0 0 - 0,00Document1 pageM/S Vivek Enterprsies: Tmujb T - 0 0 - 0,00vm7769637No ratings yet

- Chapter 8 Shapiro Solutions 7th EdDocument207 pagesChapter 8 Shapiro Solutions 7th EdKalopsia SwevenNo ratings yet

- Earthquake Analysis According To BNBC 2020Document42 pagesEarthquake Analysis According To BNBC 2020SayeedNo ratings yet

- Bario Gram AsDocument16 pagesBario Gram AsJoseph Marroquin YucraNo ratings yet

- Foto Diodo Infrarrojo Receptor 5mmDocument1 pageFoto Diodo Infrarrojo Receptor 5mmcreative_26No ratings yet

- Performance Data: Section: Date: December 2008Document26 pagesPerformance Data: Section: Date: December 2008cesar moraNo ratings yet

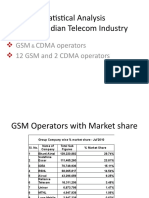

- Statistical Analysis of The Indian Telecom Industry: GSM CDMA Operators 12 GSM and 2 CDMA OperatorsDocument18 pagesStatistical Analysis of The Indian Telecom Industry: GSM CDMA Operators 12 GSM and 2 CDMA OperatorsSubaash KumaraswamyNo ratings yet

- Number of Traffic FlowsDocument12 pagesNumber of Traffic Flowsyahoo_veerNo ratings yet

- EDrive Actuators VecTac VT BrochureDocument4 pagesEDrive Actuators VecTac VT BrochureElectromateNo ratings yet

- 3rd RA of R.A. Enterprise of JCB & DumperDocument2 pages3rd RA of R.A. Enterprise of JCB & Dumpersmn.ussharNo ratings yet

- Uv0168 XLS EngDocument4 pagesUv0168 XLS EngKaushik DebnathNo ratings yet

- Conducting Focus GroupsDocument4 pagesConducting Focus GroupsOxfam100% (1)

- A.meaning and Scope of Education FinalDocument22 pagesA.meaning and Scope of Education FinalMelody CamcamNo ratings yet

- Job Satisfaction VariableDocument2 pagesJob Satisfaction VariableAnagha Pawar - 34No ratings yet

- Coding Rubric Unifix XXXX 75Document2 pagesCoding Rubric Unifix XXXX 75api-287660266No ratings yet

- Coaxial Cable Attenuation ChartDocument6 pagesCoaxial Cable Attenuation ChartNam PhamNo ratings yet

- Genil v. Rivera DigestDocument3 pagesGenil v. Rivera DigestCharmila SiplonNo ratings yet

- Grade 7 Nap MayDocument6 pagesGrade 7 Nap Mayesivaks2000No ratings yet

- Smart Door Lock System Using Face RecognitionDocument5 pagesSmart Door Lock System Using Face RecognitionIJRASETPublicationsNo ratings yet

- G2 Rust Grades USA PDFDocument2 pagesG2 Rust Grades USA PDFSt3fandragos4306No ratings yet

- Mission and VisionDocument5 pagesMission and VisionsanjedNo ratings yet

- The Mooring Pattern Study For Q-Flex Type LNG Carriers Scheduled For Berthing at Ege Gaz Aliaga LNG TerminalDocument6 pagesThe Mooring Pattern Study For Q-Flex Type LNG Carriers Scheduled For Berthing at Ege Gaz Aliaga LNG TerminalMahad Abdi100% (1)

- Safety Data Sheet SDS For CB-G PG Precision Grout and CB-G MG Multipurpose Grout Documentation ASSET DOC APPROVAL 0536Document4 pagesSafety Data Sheet SDS For CB-G PG Precision Grout and CB-G MG Multipurpose Grout Documentation ASSET DOC APPROVAL 0536BanyuNo ratings yet

- Immunity Question Paper For A Level BiologyDocument2 pagesImmunity Question Paper For A Level BiologyJansi Angel100% (1)

- Hare and Hyena: Mutugi KamundiDocument18 pagesHare and Hyena: Mutugi KamundiAndresileNo ratings yet

- Precursor Effects of Citric Acid and Citrates On Zno Crystal FormationDocument7 pagesPrecursor Effects of Citric Acid and Citrates On Zno Crystal FormationAlv R GraciaNo ratings yet

- Biotech NewsDocument116 pagesBiotech NewsRahul KapoorNo ratings yet

- Crypto Wall Crypto Snipershot OB Strategy - Day Trade SwingDocument29 pagesCrypto Wall Crypto Snipershot OB Strategy - Day Trade SwingArete JinseiNo ratings yet

- Colfax MR Series CompresorDocument2 pagesColfax MR Series CompresorinvidiuoNo ratings yet

- Existentialism in CinemaDocument25 pagesExistentialism in CinemanormatthewNo ratings yet

- RARE Manual For Training Local Nature GuidesDocument91 pagesRARE Manual For Training Local Nature GuidesenoshaugustineNo ratings yet

- The Checkmate Patterns Manual: The Ultimate Guide To Winning in ChessDocument30 pagesThe Checkmate Patterns Manual: The Ultimate Guide To Winning in ChessDusen VanNo ratings yet

- ..Product CatalogueDocument56 pages..Product Catalogue950 911No ratings yet

- Lab 3 Arduino Led Candle Light: CS 11/group - 4 - Borromeo, Galanida, Pabilan, Paypa, TejeroDocument3 pagesLab 3 Arduino Led Candle Light: CS 11/group - 4 - Borromeo, Galanida, Pabilan, Paypa, TejeroGladys Ruth PaypaNo ratings yet

- Module 5 What Is Matter PDFDocument28 pagesModule 5 What Is Matter PDFFLORA MAY VILLANUEVANo ratings yet

- Song Book Inner PagesDocument140 pagesSong Book Inner PagesEliazer PetsonNo ratings yet

- ReadingDocument205 pagesReadingHiền ThuNo ratings yet

- Inspección, Pruebas, Y Mantenimiento de Gabinetes de Ataque Rápido E HidrantesDocument3 pagesInspección, Pruebas, Y Mantenimiento de Gabinetes de Ataque Rápido E HidrantesVICTOR RALPH FLORES GUILLENNo ratings yet

- Universitas Tidar: Fakultas Keguruan Dan Ilmu PendidikanDocument7 pagesUniversitas Tidar: Fakultas Keguruan Dan Ilmu PendidikanTheresia Calcutaa WilNo ratings yet

- SafetyRelay CR30Document3 pagesSafetyRelay CR30Luis GuardiaNo ratings yet

- Subject OrientationDocument15 pagesSubject OrientationPearl OgayonNo ratings yet