You might also like

- Tax Invoice: Your Order SummaryDocument2 pagesTax Invoice: Your Order SummaryDaveNo ratings yet

- Case Study SolutionDocument4 pagesCase Study Solutionganesh teja0% (1)

- 1 SEM BCOM - Indian Financial System PDFDocument35 pages1 SEM BCOM - Indian Financial System PDFLohithashva Nanjesh Gowda100% (5)

- Toys R Us Bankruptcy CaseDocument2 pagesToys R Us Bankruptcy CaseIan GreyNo ratings yet

- FIC77LIFE - Bene ChangeDocument6 pagesFIC77LIFE - Bene ChangeMary GeorgeNo ratings yet

- Government Spending Theories Lecture NotesDocument6 pagesGovernment Spending Theories Lecture NotesrichelNo ratings yet

- MS Brothers Super Rice MillDocument9 pagesMS Brothers Super Rice MillMasud Ahmed khan100% (1)

- GK Audited Financial-31 December 2012Document101 pagesGK Audited Financial-31 December 2012Dante GillespieNo ratings yet

- Financial Statement SingerDocument13 pagesFinancial Statement SingerAnuja PasandulNo ratings yet

- RUE Hread TD: Ompany AckgroundDocument3 pagesRUE Hread TD: Ompany AckgroundAthulya SanthoshNo ratings yet

- IMT CeresDocument10 pagesIMT Cerescabmeuk07No ratings yet

- Performance Task: Holy Child College of Davao S.Y. 2020-2021Document2 pagesPerformance Task: Holy Child College of Davao S.Y. 2020-2021christine senajononNo ratings yet

- Tab D - Detailed Financial StatementsDocument13 pagesTab D - Detailed Financial Statementsarellano lawschoolNo ratings yet

- PBCC ActivitiesDocument25 pagesPBCC ActivitiesykwaiNo ratings yet

- Basic Financial Accounting Course for Human Resource StudentsDocument10 pagesBasic Financial Accounting Course for Human Resource StudentsNur Syafiqah NurNo ratings yet

- Lion Brewery (Ceylon) PLC: Interim Condensed Financial Statements For The Third Quarter Ended 31st December 2021Document13 pagesLion Brewery (Ceylon) PLC: Interim Condensed Financial Statements For The Third Quarter Ended 31st December 2021hvalolaNo ratings yet

- XYZ CompanyDocument4 pagesXYZ CompanycarinolokmoNo ratings yet

- Cap II Group I RTP Dec2023Document84 pagesCap II Group I RTP Dec2023pratyushmudbhari340No ratings yet

- Financial Statement Analysis: Jeddah International College Answer PaperDocument4 pagesFinancial Statement Analysis: Jeddah International College Answer PaperBushraYousafNo ratings yet

- WBD 1Q23 Trending Schedule Final 05 04 23Document12 pagesWBD 1Q23 Trending Schedule Final 05 04 23Stephano Gomes GabrielNo ratings yet

- Ceylon Beverage Holdings PLC: Interim Condensed Financial Statements For The Third Quarter Ended 31st December 2021Document14 pagesCeylon Beverage Holdings PLC: Interim Condensed Financial Statements For The Third Quarter Ended 31st December 2021hvalolaNo ratings yet

- Reliance Industries LTD.: Balance SheetDocument10 pagesReliance Industries LTD.: Balance SheetAayush PeriwalNo ratings yet

- Practice Problems, CH 12Document6 pagesPractice Problems, CH 12scridNo ratings yet

- K. V. Pendharkar College of Arts, Scienceand Commerce (Autonomous)Document12 pagesK. V. Pendharkar College of Arts, Scienceand Commerce (Autonomous)Nayna PanigrahiNo ratings yet

- Advanced Financial Management - Finals-11Document2 pagesAdvanced Financial Management - Finals-11graalNo ratings yet

- Kin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021Document37 pagesKin Pang Holdings Limited 建 鵬 控 股 有 限 公 司: Audited Annual Results Announcement For The Year Ended 31 December 2021ALNo ratings yet

- Problem 18-7Document4 pagesProblem 18-7api-254635136No ratings yet

- Group AssignmentDocument6 pagesGroup AssignmentIshiyaku Adamu NjiddaNo ratings yet

- TPG - Annual Report 2020 Income Statemnt 1Document2 pagesTPG - Annual Report 2020 Income Statemnt 1Pei Ling Ch'ngNo ratings yet

- AHM13e Chapter - 01 - Solution To Problems and Key To CasesDocument19 pagesAHM13e Chapter - 01 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Optiva Inc. Q2 2022 Financial Statements FinalDocument19 pagesOptiva Inc. Q2 2022 Financial Statements FinaldivyaNo ratings yet

- Dialog Finance PLC: ConfidentialDocument12 pagesDialog Finance PLC: ConfidentialgirihellNo ratings yet

- PT FLORIST GUMP INCOME STATEMENTDocument9 pagesPT FLORIST GUMP INCOME STATEMENTSu MiniNo ratings yet

- Daffodil Computers Limited Balance Sheet As at 30 June 2007: Aziz Halim Khair ChoudhuryDocument20 pagesDaffodil Computers Limited Balance Sheet As at 30 June 2007: Aziz Halim Khair ChoudhuryShafayet JamilNo ratings yet

- CAG Financials 2019Document4 pagesCAG Financials 2019AzliGhaniNo ratings yet

- Bursa Announcement DIYQ12022Document13 pagesBursa Announcement DIYQ12022Quint WongNo ratings yet

- CORPORATE REPORTING - MA-2022 - QuestionDocument7 pagesCORPORATE REPORTING - MA-2022 - Questionswarna dasNo ratings yet

- Case Study - Financial Statements & Future ProspectsDocument8 pagesCase Study - Financial Statements & Future Prospectsmm3289No ratings yet

- IMT CeresDocument11 pagesIMT CeresShivam GuptaNo ratings yet

- KasusDocument4 pagesKasusTry DharsanaNo ratings yet

- Case Enager IndustriesDocument4 pagesCase Enager IndustriesTry DharsanaNo ratings yet

- Group #1 - Presentation - Super Sports - QuestionDocument8 pagesGroup #1 - Presentation - Super Sports - QuestionNaruto MangaNo ratings yet

- Berger Paints Bangladesh Limited Statement of Financial PositionDocument8 pagesBerger Paints Bangladesh Limited Statement of Financial PositionrrashadattNo ratings yet

- Assessment Instructions (PGBM01 22-23 Semester 1)Document7 pagesAssessment Instructions (PGBM01 22-23 Semester 1)Md. Real MiahNo ratings yet

- Financial Accounting A November 2013Document7 pagesFinancial Accounting A November 2013Munodawafa ChimhamhiwaNo ratings yet

- NWC model + CF new versionDocument1 pageNWC model + CF new versionmichael odiemboNo ratings yet

- BDFA1103Document5 pagesBDFA1103Yukie LimNo ratings yet

- Statement August 31 2020Document30 pagesStatement August 31 2020NicolasNo ratings yet

- Acc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291Document201 pagesAcc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291290acc100% (2)

- M4 Example 2 SDN BHD FSADocument38 pagesM4 Example 2 SDN BHD FSAhanis nabilaNo ratings yet

- Question 2 (30 Marks) : Sales 8000 Cost of Sales (6000)Document4 pagesQuestion 2 (30 Marks) : Sales 8000 Cost of Sales (6000)Chitradevi RamooNo ratings yet

- A222 Tutorial 2QDocument5 pagesA222 Tutorial 2Qchong huisinNo ratings yet

- Fundamentals of Accountancy Business and Management 1 (Lehnard D. Gellor, CPA) Page 1 of 4Document6 pagesFundamentals of Accountancy Business and Management 1 (Lehnard D. Gellor, CPA) Page 1 of 4Lehnard Delos Reyes GellorNo ratings yet

- 1Q 2014 Op Supp Final 7-21-14Document19 pages1Q 2014 Op Supp Final 7-21-14bomby0No ratings yet

- CR-July-Aug-2022Document6 pagesCR-July-Aug-2022banglauserNo ratings yet

- Advanced - Yr 2022 Audited AccountsDocument22 pagesAdvanced - Yr 2022 Audited AccountswolekniceNo ratings yet

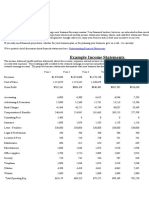

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- MSA 1 Winter2022Document16 pagesMSA 1 Winter2022gohar azizNo ratings yet

- Unaudited Consolidated Financial Statements: For The Quarter Ended 31 March 2022Document7 pagesUnaudited Consolidated Financial Statements: For The Quarter Ended 31 March 2022Fuaad DodooNo ratings yet

- BRD Group Interim Financial Statements for Q3 2022Document90 pagesBRD Group Interim Financial Statements for Q3 2022teoxysNo ratings yet

- Chap 010Document19 pagesChap 010AshutoshNo ratings yet

- Habib Motors 2022Document6 pagesHabib Motors 2022usmansss_606776863No ratings yet

- Handout 1 (B) Ratio Analysis Practice QuestionsDocument5 pagesHandout 1 (B) Ratio Analysis Practice QuestionsMuhammad Asad AliNo ratings yet

- IMT CeresDocument7 pagesIMT Ceresraman.joshi751No ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Persistent Annual Report 2022Document2 pagesPersistent Annual Report 2022Ashwin GophanNo ratings yet

- Acer Philippines. vs. CIRDocument27 pagesAcer Philippines. vs. CIRFarina R. SalvadorNo ratings yet

- The Economics of Petroleum Refining: Understanding Factors that Impact ProfitabilityDocument20 pagesThe Economics of Petroleum Refining: Understanding Factors that Impact Profitabilitysnikraftar1406No ratings yet

- Module 4 - Financial Ratios S23Document27 pagesModule 4 - Financial Ratios S23Prachi YadavNo ratings yet

- Corporate Governance in Asia: Eight Case Studies: Robert W. Mcgee Florida International UniversityDocument38 pagesCorporate Governance in Asia: Eight Case Studies: Robert W. Mcgee Florida International UniversitySasboomNo ratings yet

- Trading ManualDocument24 pagesTrading Manualehsan453100% (1)

- A-Level Macroeconomics PLC (AQA)Document11 pagesA-Level Macroeconomics PLC (AQA)Karim El-GawlyNo ratings yet

- Provisions Of Companies Act 1956Document15 pagesProvisions Of Companies Act 19569986212378No ratings yet

- Guarantors Statement FormDocument5 pagesGuarantors Statement FormVeerababu AdapaNo ratings yet

- New Rev Financial Acc1Document22 pagesNew Rev Financial Acc1ahmedfaiyaz917No ratings yet

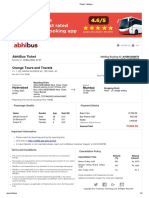

- Abibus RETURN TickDocument2 pagesAbibus RETURN Tickarun13091987No ratings yet

- Ffiffitrffi'': Karnataka Gramin BankDocument2 pagesFfiffitrffi'': Karnataka Gramin BankRøhíth Kumar CNo ratings yet

- Taxation Case Digests (Updated)Document5 pagesTaxation Case Digests (Updated)Anonymous FrkxzuNo ratings yet

- Tax Year 2013-14 (As Per Finance Act 2013) : Tax Card For Staff and Clients OnlyDocument1 pageTax Year 2013-14 (As Per Finance Act 2013) : Tax Card For Staff and Clients OnlyMuhammad sarfrazNo ratings yet

- Info On Tuition Free Universities in SwedenDocument4 pagesInfo On Tuition Free Universities in SwedencezeomedoNo ratings yet

- The Economic EnvironmentDocument16 pagesThe Economic EnvironmentvenkatNo ratings yet

- I Want The Earth Plus 5 PercentDocument12 pagesI Want The Earth Plus 5 PercentLara Dubugras Campos100% (1)

- Consistency Analysis of Mixed Mutual Fund Performance and Equity Mutual Funds Performance Between 2003-2014 Using Sharpe, Treynor, and Jensen MethodsDocument12 pagesConsistency Analysis of Mixed Mutual Fund Performance and Equity Mutual Funds Performance Between 2003-2014 Using Sharpe, Treynor, and Jensen MethodsNuniek KartikariniNo ratings yet

- Economic Value AddedDocument9 pagesEconomic Value AddedLimisha ViswanathanNo ratings yet

- United States Bankruptcy Court Southern District of New YorkDocument4 pagesUnited States Bankruptcy Court Southern District of New YorkChapter 11 DocketsNo ratings yet

- Investor LetterDocument3 pagesInvestor LetterRichard LiuNo ratings yet

- John Hay People's Alternative Coalition Vs Lim - 119775 - October 24, 2003 - JDocument12 pagesJohn Hay People's Alternative Coalition Vs Lim - 119775 - October 24, 2003 - JFrances Ann TevesNo ratings yet

- Workbook CH 1-5Document24 pagesWorkbook CH 1-5Krish BhasinNo ratings yet

- Bir Form 2305Document1 pageBir Form 2305MacneoNo ratings yet

- Bill No. 254Document1 pageBill No. 254Jignesh UpadhyayNo ratings yet