You might also like

- Mckinsey Technology Trends Outlook 2023 v2Document81 pagesMckinsey Technology Trends Outlook 2023 v2dacembaplacement dace100% (2)

- Disruptive Technologies A 2021 UpdateDocument37 pagesDisruptive Technologies A 2021 UpdateCTRM CenterNo ratings yet

- @navisworks BIM Today March 2020Document99 pages@navisworks BIM Today March 2020Johnny MongesNo ratings yet

- Me Construction Gccpoc-2023Document42 pagesMe Construction Gccpoc-2023Chhaya DhawanNo ratings yet

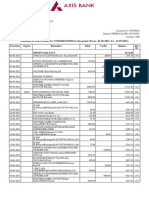

- Statement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Document6 pagesStatement of Axis Account No:917010066315582 For The Period (From: 01-06-2021 To: 12-09-2021)Anirban DebNo ratings yet

- KPMG Global Construction Survey 2019Document44 pagesKPMG Global Construction Survey 2019Prem JerardNo ratings yet

- Construction Technology TrendsDocument22 pagesConstruction Technology TrendsaungksintNo ratings yet

- How Construction Technology Is Reshaping The Construction IndustryDocument17 pagesHow Construction Technology Is Reshaping The Construction IndustryAlex ResearchersNo ratings yet

- Sustainable Development: San Carlos CollegeDocument13 pagesSustainable Development: San Carlos CollegeArya Guzman80% (10)

- Industry 4. 0 Solutions For Building Design and ConstructionDocument421 pagesIndustry 4. 0 Solutions For Building Design and ConstructionGardener Ayu100% (2)

- Brochure BIMDocument26 pagesBrochure BIMtomimito100% (2)

- Digital Twins: How Engineers Can Adopt Them To Enhance PerformancesFrom EverandDigital Twins: How Engineers Can Adopt Them To Enhance PerformancesNo ratings yet

- Navigating The Digital Future The Disruption of Capital Projects PDFDocument12 pagesNavigating The Digital Future The Disruption of Capital Projects PDFGustavo AHNo ratings yet

- Reimagining Construction - ADSK CIOB - Discussion Paper - ReleasedDocument28 pagesReimagining Construction - ADSK CIOB - Discussion Paper - ReleasedWan Yusoff Wan MahmoodNo ratings yet

- Digital Opportunities in Engineering ConstructionDocument16 pagesDigital Opportunities in Engineering ConstructionLee HuynhNo ratings yet

- Carving Out A Digital Future For Epc IndustryDocument7 pagesCarving Out A Digital Future For Epc Industryaanchal_friend4everNo ratings yet

- Digital Data Driven Are You ReadyDocument12 pagesDigital Data Driven Are You ReadyKite DireNo ratings yet

- Blockchain Technology in ConstructionDocument52 pagesBlockchain Technology in ConstructionWan Yusoff Wan MahmoodNo ratings yet

- The Future of Telecom: A Dual Transformation: Industry Horizons // December 2017Document10 pagesThe Future of Telecom: A Dual Transformation: Industry Horizons // December 2017John100% (1)

- Blockchain Technology in The Construction Industry: Digital Transformation For High ProductivityDocument52 pagesBlockchain Technology in The Construction Industry: Digital Transformation For High ProductivityAnonymous zwnFXURJNo ratings yet

- Artificial Intelligence Construction Technologys Next FrontierDocument8 pagesArtificial Intelligence Construction Technologys Next FrontierMV0% (1)

- 2024 TMT Outlook TechnologyDocument16 pages2024 TMT Outlook TechnologyKhouni ChihebNo ratings yet

- Point of View On Digital ConstructionDocument16 pagesPoint of View On Digital ConstructionIrsyad RabbaniNo ratings yet

- Lesson 1Document52 pagesLesson 1Maryann Mojica GonzalesNo ratings yet

- Engineering and ConstructionDocument7 pagesEngineering and ConstructionALNo ratings yet

- Results in Engineering: Muhammad Ali Musarat, Wesam Salah Alaloul, Abdul Mateen Khan, Saba Ayub, Nathan JousseaumeDocument18 pagesResults in Engineering: Muhammad Ali Musarat, Wesam Salah Alaloul, Abdul Mateen Khan, Saba Ayub, Nathan JousseaumeMuhamad IrfanNo ratings yet

- Global Value of Deals by Corporate Investors in Energy Technology Companies, by Sector of InvestorDocument5 pagesGlobal Value of Deals by Corporate Investors in Energy Technology Companies, by Sector of Investornewc1236No ratings yet

- Wei2018 Copy 3Document1 pageWei2018 Copy 3newc1236No ratings yet

- 1 s2.0 S2352710221005842 MainDocument15 pages1 s2.0 S2352710221005842 MainYash ChorariaNo ratings yet

- Strategies For Realizing The Benefits of 3D Integrated Modeling of Buildings For The AEC IndustryDocument6 pagesStrategies For Realizing The Benefits of 3D Integrated Modeling of Buildings For The AEC IndustryVimal KaulNo ratings yet

- 01 Innovation - Performance - Indicators - For - ArchitectureDocument27 pages01 Innovation - Performance - Indicators - For - ArchitectureAbdullah AlaaNo ratings yet

- Top 50 Construction Technology Startups. Report 2023 PDFDocument19 pagesTop 50 Construction Technology Startups. Report 2023 PDFManuel del MoralNo ratings yet

- HWBN Report UKIDocument38 pagesHWBN Report UKIhps sgNo ratings yet

- Cfawcom 965317308Document26 pagesCfawcom 965317308ALNo ratings yet

- !! Architectural Services Market - 2022 - 27 - Industry Share, Size, Growth - Mordor IntelligenceDocument6 pages!! Architectural Services Market - 2022 - 27 - Industry Share, Size, Growth - Mordor IntelligenceAlexNo ratings yet

- How To Become Tech Forward A Technology Transformation Approach That WorksDocument7 pagesHow To Become Tech Forward A Technology Transformation Approach That WorksPatricia GarciaNo ratings yet

- Key For Entering Industry 4.0 in The AEC SectorDocument8 pagesKey For Entering Industry 4.0 in The AEC SectorMotasem AltamimiNo ratings yet

- Automation in Construction: Thomas BockDocument9 pagesAutomation in Construction: Thomas Bocksivabharath44No ratings yet

- 2020 Engineering Construction Industry OutlookDocument10 pages2020 Engineering Construction Industry OutlookiabhiuceNo ratings yet

- 1 s2.0 S0926580517309512 MainDocument13 pages1 s2.0 S0926580517309512 Mainhamed nozariNo ratings yet

- Technology Sector Outlook - FidelityDocument7 pagesTechnology Sector Outlook - Fidelityy.belausavaNo ratings yet

- Usage of Information Technology For The Construction Industry4Document2 pagesUsage of Information Technology For The Construction Industry4Lizza AnnaNo ratings yet

- Sustainability 15 00202Document20 pagesSustainability 15 00202Akshay RockzzNo ratings yet

- (DRAFT) Version 2Document53 pages(DRAFT) Version 2nghitran.31221020434No ratings yet

- Digitalizing Circular Economy Through Blockchains, The Blockchain Circular Economy Index - Basile, D. Et Al. (2023)Document14 pagesDigitalizing Circular Economy Through Blockchains, The Blockchain Circular Economy Index - Basile, D. Et Al. (2023)Pablo AsteteNo ratings yet

- WP - Digital Transformation Engineering and Construction IndustryDocument31 pagesWP - Digital Transformation Engineering and Construction IndustryWilly AragonNo ratings yet

- DE GRAFT Digital Twin in IndustryDocument39 pagesDE GRAFT Digital Twin in IndustryAjvaro ContiNo ratings yet

- UTI - Five Data Center Predictions For 2022Document21 pagesUTI - Five Data Center Predictions For 2022Elie SiNo ratings yet

- AT-07961 WP Sustainability SurveyFindingsDocument14 pagesAT-07961 WP Sustainability SurveyFindingsSadaf Tariq HameedNo ratings yet

- Na I Op Emerging Construction TechnologiesDocument45 pagesNa I Op Emerging Construction TechnologiesKhenneth ChiaNo ratings yet

- KSA IT Sector U CapitalDocument27 pagesKSA IT Sector U Capitalikhan809No ratings yet

- Trends: Major Trends in The Construction IndustryDocument3 pagesTrends: Major Trends in The Construction IndustryDipin MathewNo ratings yet

- Mr. Ketan Bakshi: Founder & Managing Director, NeilsoftDocument4 pagesMr. Ketan Bakshi: Founder & Managing Director, NeilsoftbkguptazNo ratings yet

- Assignment 1Document4 pagesAssignment 1amanda ngwenyaNo ratings yet

- 28 Lean PrinciplesDocument8 pages28 Lean PrincipleskarleinsNo ratings yet

- The Way Forward For Electronic DesignDocument32 pagesThe Way Forward For Electronic DesignEDA360No ratings yet

- PfizerDocument6 pagesPfizerKeerthana Raghu RamanNo ratings yet

- Supply Chain Management in Construction and Engineer-To-Order IndustriesDocument9 pagesSupply Chain Management in Construction and Engineer-To-Order IndustriesMuhammad ShoaibNo ratings yet

- Geoinformatics 2007 Vol05Document48 pagesGeoinformatics 2007 Vol05protogeografoNo ratings yet

- 2018-06-11 The European Construction Industry Manifesto On Digital Construction - A4Document4 pages2018-06-11 The European Construction Industry Manifesto On Digital Construction - A4CPittmanNo ratings yet

- A Review On Virtual Reality and Augmented Reality in Architecture, Engineering and Construction IndustryDocument7 pagesA Review On Virtual Reality and Augmented Reality in Architecture, Engineering and Construction Industry2GO18CV 025No ratings yet

- Research Paper 1.1.1Document8 pagesResearch Paper 1.1.1Sailee RedkarNo ratings yet

- 2030 Towards Next Generation EPC CompaniesDocument6 pages2030 Towards Next Generation EPC CompaniesaarivalaganNo ratings yet

- Order in Respect of Bhavesh Kothari, Partner Money Magnet Securities in The Matter of Synchronized Trading by Connected Persons.Document9 pagesOrder in Respect of Bhavesh Kothari, Partner Money Magnet Securities in The Matter of Synchronized Trading by Connected Persons.Shyam SunderNo ratings yet

- CS619: Test Phase (OVS) : Requirements Salaried Individuals Business Persons Citizenship Age Minimum Monthly IncomeDocument2 pagesCS619: Test Phase (OVS) : Requirements Salaried Individuals Business Persons Citizenship Age Minimum Monthly Incomejabbarabdul301No ratings yet

- Rating Methodology: Evaluating The IssuerDocument35 pagesRating Methodology: Evaluating The Issuerizi25No ratings yet

- Penilaian Saham PT. Ultra Jaya Milk IndustryDocument12 pagesPenilaian Saham PT. Ultra Jaya Milk IndustryPricillia Aura100% (1)

- FIN2704 Tutorial 1 Question 3 SolutionDocument5 pagesFIN2704 Tutorial 1 Question 3 SolutionAndrew TungNo ratings yet

- Impact of Globalization On Human Rights Evidence From Sub-Saharan AfricaDocument29 pagesImpact of Globalization On Human Rights Evidence From Sub-Saharan AfricaPamela QuinteroNo ratings yet

- Tutorial 3 Solutions - ERPsDocument2 pagesTutorial 3 Solutions - ERPsKhathutshelo KharivheNo ratings yet

- Voltas Ac Lucknow BillDocument2 pagesVoltas Ac Lucknow BillGp NigamNo ratings yet

- Af313 Tutorial Collection 4 - Economic Order QuantityDocument2 pagesAf313 Tutorial Collection 4 - Economic Order QuantityArti SinghNo ratings yet

- Analisis Daya Saing Jambu Mete Di Kabupaten Wonogiri Jawa TengahDocument15 pagesAnalisis Daya Saing Jambu Mete Di Kabupaten Wonogiri Jawa TengahantoNo ratings yet

- Encyclopedia Central Banking Louis Philippe Rochon 514mUhKazmLDocument4 pagesEncyclopedia Central Banking Louis Philippe Rochon 514mUhKazmLNuwan Tharanga LiyanageNo ratings yet

- Duties of Procurement HeadDocument1 pageDuties of Procurement HeadstephenogunladeNo ratings yet

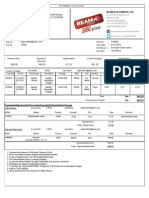

- Beam Telecom PVT LTD.: 8-2-610/A, Road No.10, Banjara Hills, Hyderabad-500034 Tel: +91-40-66272727Document2 pagesBeam Telecom PVT LTD.: 8-2-610/A, Road No.10, Banjara Hills, Hyderabad-500034 Tel: +91-40-66272727Raghav Reddy NelloreNo ratings yet

- Abm 112Document2 pagesAbm 112l mNo ratings yet

- Credit Suisse Equity Research - BP 2015Document7 pagesCredit Suisse Equity Research - BP 2015Chun Chun ChanNo ratings yet

- Present Value - Extra Topic Chapt 9 12 AdvDocument5 pagesPresent Value - Extra Topic Chapt 9 12 AdvlokNo ratings yet

- MBA View Book 08 09Document48 pagesMBA View Book 08 09Mahfuzur RahmanNo ratings yet

- FIN 534 Homework Chapter 9Document3 pagesFIN 534 Homework Chapter 9Jenna KiragisNo ratings yet

- Health Economics - Lecture Ch08Document64 pagesHealth Economics - Lecture Ch08Katherine SauerNo ratings yet

- 403b PlansDocument2 pages403b Plansapi-246909910No ratings yet

- Documented Essay Final Draft WeeblyDocument6 pagesDocumented Essay Final Draft Weeblyapi-241798291No ratings yet

- National Income: Submitted byDocument85 pagesNational Income: Submitted byShrutiNo ratings yet

- The Role of The State in Employment Relations: What The Chapter CoversDocument14 pagesThe Role of The State in Employment Relations: What The Chapter CoversKatinka AsquithNo ratings yet

- Chapter 4Document22 pagesChapter 4radha makmurNo ratings yet

- 0 MasterfileDocument598 pages0 MasterfileAngel VenableNo ratings yet

- 37 - Chevron Philippines vs. CIRDocument2 pages37 - Chevron Philippines vs. CIRLEIGH TARITZ GANANCIALNo ratings yet

- CVDocument2 pagesCVSaiPraneethNo ratings yet