You might also like

- Cost-Volume-Profit Analysis: Mcgraw-Hill EducationDocument53 pagesCost-Volume-Profit Analysis: Mcgraw-Hill Educationkindergarten tutorialNo ratings yet

- Audit of Property, Plant & EquipmentDocument51 pagesAudit of Property, Plant & EquipmentKristina KittyNo ratings yet

- Loan Against Shares (LAS) AgreementDocument21 pagesLoan Against Shares (LAS) AgreementAshish ShahNo ratings yet

- Exhibit 2 Product Class Cost Analysis (Normal Year) : Units UnitsDocument6 pagesExhibit 2 Product Class Cost Analysis (Normal Year) : Units UnitsSangtani PareshNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Accounting Cycle Exercises IDocument58 pagesAccounting Cycle Exercises IMd Mobasshir Iqubal100% (1)

- Cost-Volume-Profit Relationships: Principles of Management AccountingDocument16 pagesCost-Volume-Profit Relationships: Principles of Management Accountingsyed haider ali shah shah100% (1)

- ABT Chart Analysis GuideDocument10 pagesABT Chart Analysis GuideBoyka KirovNo ratings yet

- Cost-Volume-Profit Relationships1Document52 pagesCost-Volume-Profit Relationships1Kamrul Huda100% (1)

- Inventory Valuation TutorialDocument4 pagesInventory Valuation TutorialSalma HazemNo ratings yet

- CHAPTER 3 Question SolutionsDocument3 pagesCHAPTER 3 Question Solutionscamd12900% (1)

- Chapter 11 Intagible AssetsDocument5 pagesChapter 11 Intagible Assetsmaria isabellaNo ratings yet

- Hilton 11e Chap007PPTDocument53 pagesHilton 11e Chap007PPTNgô Khánh HòaNo ratings yet

- Chapter 7Document36 pagesChapter 718071052 Nguyễn Thị MaiNo ratings yet

- Management Accounting: Dr. Jagriti AroraDocument31 pagesManagement Accounting: Dr. Jagriti AroraMahamNo ratings yet

- CVP Analysis 08Document52 pagesCVP Analysis 08Maulani DwiNo ratings yet

- Cost-Volume-Profit Analysis: Mcgraw-Hill/IrwinDocument78 pagesCost-Volume-Profit Analysis: Mcgraw-Hill/IrwinSheila Jane Maderse AbraganNo ratings yet

- IPPTChap 007Document53 pagesIPPTChap 007Khaled BarakatNo ratings yet

- Cost-Volume-Profit Relationships: Chapter FiveDocument82 pagesCost-Volume-Profit Relationships: Chapter FiveFahim RezaNo ratings yet

- CVP PPT 1st YrDocument81 pagesCVP PPT 1st YrZachary AstorNo ratings yet

- Hilton 11e Chap007 StudentsDocument38 pagesHilton 11e Chap007 StudentsMelix SianturiNo ratings yet

- Cost Volume Profit Analysis - Chapter 6Document39 pagesCost Volume Profit Analysis - Chapter 6Maria Maganda MalditaNo ratings yet

- MAS Hilton Chap07Document30 pagesMAS Hilton Chap07YahiMicuaVillandaNo ratings yet

- Chapter 1 Cost-Volume-Profit RelationshipsDocument51 pagesChapter 1 Cost-Volume-Profit Relationshipspamela dequillamorteNo ratings yet

- CVP AnalysisDocument36 pagesCVP Analysisghosh71No ratings yet

- Chapter - 8 - Cost-Volume-Profit Analysis - UETDocument19 pagesChapter - 8 - Cost-Volume-Profit Analysis - UETZia UddinNo ratings yet

- Act202 Chapter 5Document82 pagesAct202 Chapter 5Anonymous bh1JXMpntvNo ratings yet

- Lecture-6-CVP-A-Reading Materials PDFDocument71 pagesLecture-6-CVP-A-Reading Materials PDFFerdausNo ratings yet

- Chapter 6 CVPDocument81 pagesChapter 6 CVPPrometheus SmithNo ratings yet

- CVP AnalysisDocument22 pagesCVP AnalysisMolly RastogiNo ratings yet

- Break Even Analysis TemplateDocument2 pagesBreak Even Analysis TemplateSiyabongaNo ratings yet

- A181 Bkam3023 Topic 1 - CVP AnalysisDocument64 pagesA181 Bkam3023 Topic 1 - CVP AnalysisJagethiswari RajahNo ratings yet

- Chap 006Document82 pagesChap 006MD Solaiman Hossain RakibNo ratings yet

- Foundations of Financial Management: Spreadsheet TemplatesDocument7 pagesFoundations of Financial Management: Spreadsheet Templatesalaa_h1100% (1)

- Cost-Volume-Profit Relationships: Chapter FiveDocument82 pagesCost-Volume-Profit Relationships: Chapter FiveRahamat UllahNo ratings yet

- ACT202 Chapter 5 NewDocument82 pagesACT202 Chapter 5 NewAminaMatinNo ratings yet

- A WK6 Chp5Document97 pagesA WK6 Chp5Jocelyn LimNo ratings yet

- Chap 008Document34 pagesChap 008alishamrozNo ratings yet

- Pertemuan 11 Chap007-008 Hilton - EditDocument58 pagesPertemuan 11 Chap007-008 Hilton - Editferly12No ratings yet

- Chap5 (E)Document60 pagesChap5 (E)Kiên Lê TrungNo ratings yet

- Chapter 20: Break Even and Cost Volume Profit Analysis: Group MemebersDocument34 pagesChapter 20: Break Even and Cost Volume Profit Analysis: Group MemebersMuhammad HasanNo ratings yet

- Costing CaseDocument6 pagesCosting CasenguyenthingocmaimkNo ratings yet

- Chapter 9 - CVP AnalysisDocument60 pagesChapter 9 - CVP AnalysisKunal ObhraiNo ratings yet

- Assignment 02 - SolutionDocument4 pagesAssignment 02 - SolutionSuman Paul ChowdhuryNo ratings yet

- Chapter 4 CVP AnalysisDocument15 pagesChapter 4 CVP AnalysisMaria Beatriz NavecisNo ratings yet

- RatiosDocument79 pagesRatiosKim Bales BlayNo ratings yet

- Break Even Answer KeyDocument8 pagesBreak Even Answer Keyyea okayNo ratings yet

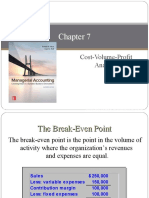

- Equation Method: Sales Variable Expenses + Fixed Expenses + Profits (At The Break-Even Point Profits Equal Zero)Document4 pagesEquation Method: Sales Variable Expenses + Fixed Expenses + Profits (At The Break-Even Point Profits Equal Zero)Aly TerrenalNo ratings yet

- Chapter 05Document97 pagesChapter 05milkie beigeNo ratings yet

- W11-12 Cost-Volume-Profit RelationshipsDocument82 pagesW11-12 Cost-Volume-Profit RelationshipsQurat SaboorNo ratings yet

- Break-Even Analysis Example Excel-TemplateDocument8 pagesBreak-Even Analysis Example Excel-TemplateFernando FlorNo ratings yet

- Week 2 CVP AnalysisDocument42 pagesWeek 2 CVP AnalysisMichel BanvoNo ratings yet

- Cost Volume Profit Analysis Lecture NotesDocument34 pagesCost Volume Profit Analysis Lecture NotesAra Reyna D. Mamon-DuhaylungsodNo ratings yet

- Suggested Solution To CVP TutorialDocument5 pagesSuggested Solution To CVP TutorialLiyendra FernandoNo ratings yet

- Exam Kit QnsDocument13 pagesExam Kit QnsFatemah MohamedaliNo ratings yet

- LO2 Prepare and Interpret A CostDocument8 pagesLO2 Prepare and Interpret A CostGayle SanchezNo ratings yet

- Chapter 05 Cost Volume Profit RelationshipDocument62 pagesChapter 05 Cost Volume Profit RelationshipFahim ShihabNo ratings yet

- Chapter Six Ba 315-Lpc Umsl: (Contribution Margin)Document53 pagesChapter Six Ba 315-Lpc Umsl: (Contribution Margin)NAZHIM KERENNo ratings yet

- The Basics of Cost-Volume-Profit (CVP) Analysis: After Covering Fixed Costs, Any Remaining CM Contributes To IncomeDocument10 pagesThe Basics of Cost-Volume-Profit (CVP) Analysis: After Covering Fixed Costs, Any Remaining CM Contributes To IncomeMozahar SujonNo ratings yet

- CVP Analysis - Jan18Document23 pagesCVP Analysis - Jan18Jobert DiliNo ratings yet

- Endterm AdvManAcc SampleDocument10 pagesEndterm AdvManAcc Samplemarinamuhtar0602No ratings yet

- Topic 04 - Cost and Management Accounting Course Notes 2021 PWC Conversion ProgrammeDocument84 pagesTopic 04 - Cost and Management Accounting Course Notes 2021 PWC Conversion ProgrammejerrymaNo ratings yet

- Cost-Volume-Profit: Prepared by Meifida IlyasDocument64 pagesCost-Volume-Profit: Prepared by Meifida IlyasDixi AndriantoNo ratings yet

- Chapter 12 AnswersDocument3 pagesChapter 12 AnswersMarisa Vetter100% (1)

- AF Ch. 4 - Analysis FS - ExcelDocument9 pagesAF Ch. 4 - Analysis FS - ExcelAlfiandriAdinNo ratings yet

- Formula: (Individual Sales/total Sales) No of Sales in Units. No of Sales in Unit Per ProductDocument6 pagesFormula: (Individual Sales/total Sales) No of Sales in Units. No of Sales in Unit Per ProductChris MarasiganNo ratings yet

- Principles of Marketing EM3211E: Hanoi University of Sience and Technology School of Management & EconomicsDocument30 pagesPrinciples of Marketing EM3211E: Hanoi University of Sience and Technology School of Management & EconomicsNgọc ĐỗNo ratings yet

- Principles of Marketing: Hanoi University of Sience and Technology School of Management & EconomicsDocument66 pagesPrinciples of Marketing: Hanoi University of Sience and Technology School of Management & EconomicsNgọc ĐỗNo ratings yet

- Principles of Marketing: Hanoi University of Sience and Technology School of Management & EconomicsDocument46 pagesPrinciples of Marketing: Hanoi University of Sience and Technology School of Management & EconomicsNgọc ĐỗNo ratings yet

- EM2301. Practical Class 2Document4 pagesEM2301. Practical Class 2Ngọc ĐỗNo ratings yet

- EM2301. Practical Class 1Document4 pagesEM2301. Practical Class 1Ngọc ĐỗNo ratings yet

- Hilton 11e Chap009PPTDocument51 pagesHilton 11e Chap009PPTNgọc ĐỗNo ratings yet

- Hilton 11e Chap010PPTDocument60 pagesHilton 11e Chap010PPTNgọc ĐỗNo ratings yet

- Note Buad829 Mod1 E7iy8uc55twyqkpDocument128 pagesNote Buad829 Mod1 E7iy8uc55twyqkpashamohartessNo ratings yet

- First Consolidated BankDocument3 pagesFirst Consolidated BankMichael John LunaNo ratings yet

- HCA16ge IM CH06Document14 pagesHCA16ge IM CH06Ann MaNo ratings yet

- Cost Volume Profit AnalysisDocument34 pagesCost Volume Profit AnalysisItachi UchihaNo ratings yet

- 4 Financial Proposal Template Annex 4Document15 pages4 Financial Proposal Template Annex 4Habtamu AsmareNo ratings yet

- RM Music Worksheet For The Ended Period July, 31 2016Document25 pagesRM Music Worksheet For The Ended Period July, 31 2016AmandaNo ratings yet

- MCQ Module 2Document4 pagesMCQ Module 2VIJAYA KUMAR YNo ratings yet

- Unit I Banking and Insurance Law Study NotesDocument12 pagesUnit I Banking and Insurance Law Study NotesSekar M KPRCAS-CommerceNo ratings yet

- Q1 2023 PitchBook Private Capital IndexesDocument24 pagesQ1 2023 PitchBook Private Capital IndexesmarianoveNo ratings yet

- 9421 - Non-Profit OrganizationDocument4 pages9421 - Non-Profit Organizationjsmozol3434qcNo ratings yet

- GPR 304 - LBA I Course Outline 2023Document18 pagesGPR 304 - LBA I Course Outline 2023Kimberly OdumbeNo ratings yet

- Bangko Sentral NG Pilipinas: (Central Bank of The Philippines)Document7 pagesBangko Sentral NG Pilipinas: (Central Bank of The Philippines)Lorraine Millama PurayNo ratings yet

- SEC Madoff Case Closing Recommendation 2006Document2 pagesSEC Madoff Case Closing Recommendation 2006Investor ProtectionNo ratings yet

- 300x Netflix USA by Jonathan OpDocument11 pages300x Netflix USA by Jonathan Op27999703210jNo ratings yet

- Corporate Financial Statements - IDocument11 pagesCorporate Financial Statements - ISoumya Ranjan PradhanNo ratings yet

- AFAR Review Semi-Finals ExamDocument10 pagesAFAR Review Semi-Finals ExamA PNo ratings yet

- Mundell-Fleming Model PDFDocument6 pagesMundell-Fleming Model PDFMarto Fe100% (1)

- Reliance Letter PadDocument60 pagesReliance Letter PadAnonymous V9E1ZJtwoENo ratings yet

- International Business New 11Document66 pagesInternational Business New 11tubenaweambroseNo ratings yet

- Arsenal FC - Financial AnalysisDocument14 pagesArsenal FC - Financial AnalysisDidiDieva0% (1)

- Caucasus School of BusinessDocument6 pagesCaucasus School of BusinessDavid ChikhladzeNo ratings yet

- Tax Incentives For Companies To Invest The Portuguese Case in 2019Document17 pagesTax Incentives For Companies To Invest The Portuguese Case in 2019Global Research and Development ServicesNo ratings yet

- AF102 Assignemnt - Group 4 (7533)Document10 pagesAF102 Assignemnt - Group 4 (7533)Anjali PrasadNo ratings yet

- Presentation IsfnDocument14 pagesPresentation IsfnAmirah ShukriNo ratings yet