You might also like

- You Exec - MECE Principle FreeDocument6 pagesYou Exec - MECE Principle FreefullaNo ratings yet

- Attachment - HRDD - Official List of ParticipantsDocument109 pagesAttachment - HRDD - Official List of ParticipantsXer Jr GnacagNo ratings yet

- Alpha Beta - Beta RoleDocument3 pagesAlpha Beta - Beta RoleHaung TuanNo ratings yet

- PitchBook For Venture Capital Firms - Ebook - GlobalDocument20 pagesPitchBook For Venture Capital Firms - Ebook - GlobalHun Yao ChongNo ratings yet

- Manning and Construction Agencies: Tel No/s: 09171882711 / 09128402946 Official Representative: ARTURO C. SICATDocument22 pagesManning and Construction Agencies: Tel No/s: 09171882711 / 09128402946 Official Representative: ARTURO C. SICATXer Jr GnacagNo ratings yet

- Undertaking Business Permit-ToledoDocument2 pagesUndertaking Business Permit-Toledojunjunsscribdaccount100% (1)

- List of Authorised Visa Agents - 21122020Document9 pagesList of Authorised Visa Agents - 21122020office officeNo ratings yet

- Pathao-MIS205-Group-Project FinalDocument18 pagesPathao-MIS205-Group-Project FinalAmir Nahian100% (1)

- Malinao Aklan ES2016Document8 pagesMalinao Aklan ES2016J JaNo ratings yet

- Malay Executive Summary 2017Document7 pagesMalay Executive Summary 2017RM Rea RebNo ratings yet

- Apalit Executive Summary 2020Document6 pagesApalit Executive Summary 2020Terry AceNo ratings yet

- COA 2017 Annual Audit Report on City of BaguioDocument184 pagesCOA 2017 Annual Audit Report on City of BaguiorainNo ratings yet

- Executive Summary: A. IntroductionDocument9 pagesExecutive Summary: A. IntroductionKathleen Mae Amada - TorresNo ratings yet

- San Fernando City Executive Summary 2017Document7 pagesSan Fernando City Executive Summary 2017Ryan De GuzmanNo ratings yet

- Urdaneta-City-Executive-Summary-2015Document5 pagesUrdaneta-City-Executive-Summary-2015vialnetroscapeNo ratings yet

- Rizal Laguna ES2019Document8 pagesRizal Laguna ES2019Hannah Brynne UrreraNo ratings yet

- Santa Ignacia Executive Summary 2017Document6 pagesSanta Ignacia Executive Summary 2017Reyna YlenaNo ratings yet

- Executive Summary 2020Document5 pagesExecutive Summary 2020Marc CabreraNo ratings yet

- Olongapo City Executive Summary 2017Document8 pagesOlongapo City Executive Summary 2017Hi ShineNo ratings yet

- Meycauayan-City-Executive-Summary-2019Document8 pagesMeycauayan-City-Executive-Summary-2019Secret secretNo ratings yet

- Tagkawayan Quezon ES2016Document9 pagesTagkawayan Quezon ES2016J JaNo ratings yet

- Mati City Executive Summary 2014Document6 pagesMati City Executive Summary 2014Heart Trixie Tacder SalvaNo ratings yet

- Roxas Isabela ES2016Document4 pagesRoxas Isabela ES2016J JaNo ratings yet

- Asingan Executive Summary 2019Document4 pagesAsingan Executive Summary 2019izuku midoriyaNo ratings yet

- Talisay City Executive Summary 2019Document6 pagesTalisay City Executive Summary 2019patatas e.No ratings yet

- Mawab Executive Summary 2015Document6 pagesMawab Executive Summary 2015Inika QuisayNo ratings yet

- PPG Alaminos-City-Executive-Summary 2018Document7 pagesPPG Alaminos-City-Executive-Summary 2018retrouvaille astrumNo ratings yet

- Pila-Executive-Summary-2018Document6 pagesPila-Executive-Summary-2018Aleethea CastaloneNo ratings yet

- 1 AcknowledgementsDocument8 pages1 AcknowledgementsJohn Remmel RogaNo ratings yet

- Santo Nino Executive Summary 2017Document6 pagesSanto Nino Executive Summary 2017Meranie FrancisqueteNo ratings yet

- Aborlan Executive Summary 2019Document6 pagesAborlan Executive Summary 2019Arly TolentinoNo ratings yet

- IlaganCity Isabela ES2018Document6 pagesIlaganCity Isabela ES2018MelvinBuyagawonNo ratings yet

- Caloocan City Executive Summary 2021Document11 pagesCaloocan City Executive Summary 2021Ruffus TooqueroNo ratings yet

- Masantol Executive Summary 2019Document5 pagesMasantol Executive Summary 2019Juan Miguel NavarroNo ratings yet

- Apalit Executive Summary 2016Document7 pagesApalit Executive Summary 2016ktagle2020No ratings yet

- Executive Summary Highlights Sasmuan Municipality AuditDocument7 pagesExecutive Summary Highlights Sasmuan Municipality AuditWilmar AbriolNo ratings yet

- Canaman Executive Summary 2013Document6 pagesCanaman Executive Summary 2013Arkie TectureNo ratings yet

- Motiong Executive Summary 2017Document7 pagesMotiong Executive Summary 2017Ronel CadelinoNo ratings yet

- San Juan City Executive Summary 2022Document7 pagesSan Juan City Executive Summary 2022MAYON NAGANo ratings yet

- Silang Executive Summary 2018Document6 pagesSilang Executive Summary 2018Realie BorbeNo ratings yet

- Executive Summary: A. Introduction The AgencyDocument5 pagesExecutive Summary: A. Introduction The Agencysandra bolokNo ratings yet

- San Pablo City Executive Summary 2022Document4 pagesSan Pablo City Executive Summary 2022JelaNo ratings yet

- Tayabas City Executive Summary 2021Document5 pagesTayabas City Executive Summary 2021rhanagailsolisNo ratings yet

- Dipaculao Aurora ES2017Document6 pagesDipaculao Aurora ES2017kim ann m. avenillaNo ratings yet

- Sample 4Document10 pagesSample 4Michael AngeloNo ratings yet

- Catarman Municipality 2019 Executive SummaryDocument7 pagesCatarman Municipality 2019 Executive SummaryJeanine IlaganNo ratings yet

- Cabuyao City Executive Summary 2019Document13 pagesCabuyao City Executive Summary 2019borgygavinaNo ratings yet

- Santo Tomas Executive Summary 2016Document4 pagesSanto Tomas Executive Summary 2016Justine CastilloNo ratings yet

- Catarman Executive Summary 2017Document6 pagesCatarman Executive Summary 2017Jeanine IlaganNo ratings yet

- Malolos City Executive Summary 2018Document8 pagesMalolos City Executive Summary 20182022105431No ratings yet

- Executive SummaryDocument8 pagesExecutive SummaryNathan Roy OngcarrancejaNo ratings yet

- Davao City Executive Summary 2014Document6 pagesDavao City Executive Summary 2014Cristina ChiNo ratings yet

- Bacarra IN ES2015Document7 pagesBacarra IN ES2015Chelcee Ulnagan CacalNo ratings yet

- Tayug-Executive-Summary-2020Document5 pagesTayug-Executive-Summary-2020Adrian Jay JavierNo ratings yet

- Butuan City Executive Summary 2014Document5 pagesButuan City Executive Summary 2014Primo V. LIlagan IIINo ratings yet

- San Pablo City Executive Summary 2013Document11 pagesSan Pablo City Executive Summary 2013Asteraceae ChrysanthNo ratings yet

- Executive Summary: A. IntroductionDocument5 pagesExecutive Summary: A. IntroductionAlicia NhsNo ratings yet

- Basco Municipality 2016 Financial ReportDocument3 pagesBasco Municipality 2016 Financial ReportREGGIE MARG MENDOZANo ratings yet

- Butuan City Executive Summary 2018Document6 pagesButuan City Executive Summary 2018ebustillobxuNo ratings yet

- Executive Summary: City of Vigan 2010 Financial ReportDocument3 pagesExecutive Summary: City of Vigan 2010 Financial ReportQueng QuintinitaNo ratings yet

- Iligan City Executive Summary 2016Document11 pagesIligan City Executive Summary 2016crizeljane.enayudaNo ratings yet

- Executive Summary: Municipality of Sta. MonicaDocument6 pagesExecutive Summary: Municipality of Sta. MonicaGenevieve TersolNo ratings yet

- Indang Cavite ES2019nhaulingDocument5 pagesIndang Cavite ES2019nhaulingMS NIQUEENo ratings yet

- Malolos City Executive Summary 2019Document7 pagesMalolos City Executive Summary 2019Arisu SakamotoNo ratings yet

- TolosaLeyte2016 Audit ReportDocument190 pagesTolosaLeyte2016 Audit ReportJulPadayaoNo ratings yet

- Josefina Executive Summary 2017Document8 pagesJosefina Executive Summary 2017Virgo Philip Wasil ButconNo ratings yet

- Santa Maria Executive Summary 2019Document7 pagesSanta Maria Executive Summary 2019kmarkcramosNo ratings yet

- Local Public Finance Management in the People's Republic of China: Challenges and OpportunitiesFrom EverandLocal Public Finance Management in the People's Republic of China: Challenges and OpportunitiesNo ratings yet

- Consolidated Registered Scrap Buyers As of April 01 2022Document24 pagesConsolidated Registered Scrap Buyers As of April 01 2022Xer Jr GnacagNo ratings yet

- Ro6 Peso DirectoryDocument6 pagesRo6 Peso DirectoryXer Jr GnacagNo ratings yet

- CPDprovider LETDocument17 pagesCPDprovider LETXer Jr GnacagNo ratings yet

- TSD As of July 31 2022Document144 pagesTSD As of July 31 2022Xer Jr GnacagNo ratings yet

- APP - RedemptionDocument10 pagesAPP - RedemptionXer Jr GnacagNo ratings yet

- List of Registered Contractors and Subcontractors With Valid List of RegistrationDocument9 pagesList of Registered Contractors and Subcontractors With Valid List of RegistrationXer Jr GnacagNo ratings yet

- DENTAL NETWORK ACTIVE LISTDocument3 pagesDENTAL NETWORK ACTIVE LISTXer Jr GnacagNo ratings yet

- Updated List of Dentists As of September 2021Document4 pagesUpdated List of Dentists As of September 2021Xer Jr GnacagNo ratings yet

- Name TagDocument1 pageName TagXer Jr GnacagNo ratings yet

- TimesheetsDocument4 pagesTimesheetsXer Jr GnacagNo ratings yet

- Updated List of Dental Network As of September 2021Document3 pagesUpdated List of Dental Network As of September 2021Xer Jr GnacagNo ratings yet

- Cuaderno Técnico Schneider Electric N 145 Estudio Térmico de Cuadros EléctricosDocument1 pageCuaderno Técnico Schneider Electric N 145 Estudio Térmico de Cuadros EléctricosisaacingNo ratings yet

- Chapter 6Document25 pagesChapter 6syafikaabdullahNo ratings yet

- Research Report For Praedico GlobalDocument3 pagesResearch Report For Praedico GlobalAbhishek PatilNo ratings yet

- How Much Does AdSense Pay Per 1000 Views Ultimate GuideDocument4 pagesHow Much Does AdSense Pay Per 1000 Views Ultimate GuideCreatom WorkNo ratings yet

- Risk Based PNLDocument27 pagesRisk Based PNLSherry YangNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Raj SakariaNo ratings yet

- Module 1 PDFDocument9 pagesModule 1 PDFUday GowdaNo ratings yet

- Yuson Vs Vitan To Almira Vs CADocument5 pagesYuson Vs Vitan To Almira Vs CAMariaAyraCelinaBatacanNo ratings yet

- ICCE 2017: Invitation to SponsorsDocument6 pagesICCE 2017: Invitation to Sponsorsajaythermal100% (1)

- Sika AG FS Dec-18Document165 pagesSika AG FS Dec-18PratikNo ratings yet

- Fintech and E Commerce in MyanmarDocument34 pagesFintech and E Commerce in MyanmarTHU RA AUNGNo ratings yet

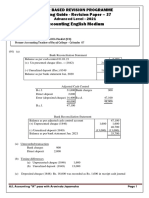

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- R.Chitra Devi 10MBA58: Click To Edit Master Subtitle StyleDocument17 pagesR.Chitra Devi 10MBA58: Click To Edit Master Subtitle StyleShyamala RajendranNo ratings yet

- 13 Essential Accounting PrinciplesDocument3 pages13 Essential Accounting PrinciplesRae MichaelNo ratings yet

- Financial Reporting: Ca P. C. SainiDocument103 pagesFinancial Reporting: Ca P. C. SainiFaraz AliNo ratings yet

- Reversing EntriesDocument4 pagesReversing EntriesCatherine GonzalesNo ratings yet

- Literature ReviewDocument2 pagesLiterature ReviewLokesh SharmaNo ratings yet

- Sitxccs007 Assessment Task 3Document7 pagesSitxccs007 Assessment Task 3komal sharmaNo ratings yet

- BSBOPS601 Project PortfolioDocument16 pagesBSBOPS601 Project PortfolioNishchal TimsinaNo ratings yet

- Unit 2 - Developing and Applying Retail StrategyDocument6 pagesUnit 2 - Developing and Applying Retail StrategyPoorna VenkatNo ratings yet

- A Study On Customer Satisfaction Towards Godrej Refrigerator With Reference To Coimbatore CityDocument3 pagesA Study On Customer Satisfaction Towards Godrej Refrigerator With Reference To Coimbatore Citysanyam jainNo ratings yet

- BELONIO QUEENIE ALICABA DoneDocument7 pagesBELONIO QUEENIE ALICABA DoneDaryl OrtizNo ratings yet

- QCA After Mid QuizDocument5 pagesQCA After Mid QuizHaris MalikNo ratings yet

- Recruitment Process TrendsDocument7 pagesRecruitment Process TrendsPoorani RaveendirakumarNo ratings yet

- Hi! I'am Paddma Sambhav: Graphic Design Intern - Jan-Mar 2022 2019-2023Document1 pageHi! I'am Paddma Sambhav: Graphic Design Intern - Jan-Mar 2022 2019-2023Tanya rajNo ratings yet