You might also like

- Unit 61: The Business CycleDocument17 pagesUnit 61: The Business CycleAiman AzNo ratings yet

- Table of ContentDocument37 pagesTable of ContentEmmaNo ratings yet

- Petroleum Economics Part2Document8 pagesPetroleum Economics Part2Syuhada RazakNo ratings yet

- Grade 12 Term 1 RevisionDocument17 pagesGrade 12 Term 1 Revisionthabileshab08No ratings yet

- Monetary and Fiscal PolicyDocument24 pagesMonetary and Fiscal PolicyBrunoNo ratings yet

- Fiscal Policy QuestionsDocument11 pagesFiscal Policy QuestionsmoosasuphiNo ratings yet

- PF 8Document96 pagesPF 8Justine MalumaNo ratings yet

- GIDB7341736-Structured Questions - 2Document3 pagesGIDB7341736-Structured Questions - 2Anvi ChoudharyNo ratings yet

- Chapter 3Document50 pagesChapter 3wudineh debebeNo ratings yet

- Increase in Demand and SupplyDocument9 pagesIncrease in Demand and SupplyJon LeinsNo ratings yet

- Mark Scheme (Post Standardisation) Summer 2009: GCE Economics (6EC01/01)Document22 pagesMark Scheme (Post Standardisation) Summer 2009: GCE Economics (6EC01/01)Lee Siew YenNo ratings yet

- Grade 12 Essays For The Next Three Years 2021-2023 AmendedDocument67 pagesGrade 12 Essays For The Next Three Years 2021-2023 AmendedSamuelNo ratings yet

- Chapter 1Document102 pagesChapter 1Chelsi XiaoNo ratings yet

- 9708 s05 Ms 2 PDFDocument7 pages9708 s05 Ms 2 PDFTawanda B MatsokotereNo ratings yet

- Chapter 1 - Tax BasicsDocument24 pagesChapter 1 - Tax Basicsrogue.pve1No ratings yet

- The Circular Flow Model of Income: and ItsDocument36 pagesThe Circular Flow Model of Income: and ItsM Shubaan Nachiappan(Student)No ratings yet

- Edexcel Year12Assessment Paper2 MSDocument11 pagesEdexcel Year12Assessment Paper2 MSnarjis kassamNo ratings yet

- 9708 Economics: MARK SCHEME For The October/November 2013 SeriesDocument6 pages9708 Economics: MARK SCHEME For The October/November 2013 SeriesRavi ChaudharyNo ratings yet

- A Level Economics Paper 2 MSDocument24 pagesA Level Economics Paper 2 MSYusuf SaleemNo ratings yet

- Second Meeting of The Canberra Group On Capital Stock StatisticsDocument13 pagesSecond Meeting of The Canberra Group On Capital Stock StatisticsKis NapraforgoNo ratings yet

- TAD CH.2 PritDocument76 pagesTAD CH.2 PritYitera SisayNo ratings yet

- Inflation Accounting Environment Accounting and ResponsibilDocument17 pagesInflation Accounting Environment Accounting and ResponsibilJaina DoshiNo ratings yet

- Tax ShiftingDocument9 pagesTax ShiftingNøthîñgLîfè100% (1)

- Full Chapter atDocument21 pagesFull Chapter atBrian Grossen100% (38)

- CBSE Class 12 Economics Question Paper 2020Document21 pagesCBSE Class 12 Economics Question Paper 2020Ayush JainNo ratings yet

- Macroeconomics Updated Apr2021Document44 pagesMacroeconomics Updated Apr2021Aashish sahuNo ratings yet

- Chapter 2Document35 pagesChapter 2ZachClementNo ratings yet

- Public Finance CH 2Document30 pagesPublic Finance CH 2kussia toramaNo ratings yet

- Economic - Financial - Social Cost Benefit AnalysisDocument11 pagesEconomic - Financial - Social Cost Benefit AnalysisProfessor Tarun Das100% (1)

- Explain The Potential Causes of A Balance of Payments Deficit On Current AccountDocument11 pagesExplain The Potential Causes of A Balance of Payments Deficit On Current AccountGirish SampathNo ratings yet

- 9708 w07 Ms 2 PDFDocument4 pages9708 w07 Ms 2 PDFKarmen ThumNo ratings yet

- Chapter 4 - AbelDocument11 pagesChapter 4 - AbelShuvro Kumar Paul75% (4)

- ECF Saint Too Canaan College 2010 - 2011 2 Term Examination S.5 Economics Paper 2 Suggested Answers Section A Short Questions (46 Marks)Document6 pagesECF Saint Too Canaan College 2010 - 2011 2 Term Examination S.5 Economics Paper 2 Suggested Answers Section A Short Questions (46 Marks)Yuen Yee IuNo ratings yet

- Eco of Taxation NotesDocument17 pagesEco of Taxation NotesGaurav HandaNo ratings yet

- Slides 09 PublicFinance Part1Document30 pagesSlides 09 PublicFinance Part1Ashish PandeyNo ratings yet

- Economics MarkingDocument20 pagesEconomics Markingbugafrancesca3No ratings yet

- Economics Grade 9 Second TermDocument41 pagesEconomics Grade 9 Second TermpalaashparikhNo ratings yet

- Pract 6 Long Final PDFDocument3 pagesPract 6 Long Final PDFginny HeNo ratings yet

- CDIC - Deposit Insurance and Handling of A Bank FailureDocument3 pagesCDIC - Deposit Insurance and Handling of A Bank FailurerrrrraaalphNo ratings yet

- MATP-Practice End Term ExaminationDocument4 pagesMATP-Practice End Term Examinationum23106No ratings yet

- 6354 01 Rms 20080306Document18 pages6354 01 Rms 20080306Ismail MerajNo ratings yet

- TaxEvasionReportDFIDFINAL1906 CompressedDocument76 pagesTaxEvasionReportDFIDFINAL1906 Compressedjifri syamNo ratings yet

- Assignment On Tax and WealthDocument7 pagesAssignment On Tax and WealthAaron WatenaonaNo ratings yet

- Ðê Thi So: 07: Thòi Gian Làm Bài: 90 PhútDocument3 pagesÐê Thi So: 07: Thòi Gian Làm Bài: 90 PhútNguyen ThinhNo ratings yet

- CHAPTER 14: Aggregate Demand (AD)Document3 pagesCHAPTER 14: Aggregate Demand (AD)herrisenNo ratings yet

- MACROECONOMICSDocument9 pagesMACROECONOMICSTawanda Leonard CharumbiraNo ratings yet

- Individual and Taxation Portfolio Management Answers Part A: Real After-Tax Required ReturnDocument6 pagesIndividual and Taxation Portfolio Management Answers Part A: Real After-Tax Required ReturnHiếu Nhi TrịnhNo ratings yet

- Incidence of TaxationDocument12 pagesIncidence of TaxationRajesh ShahiNo ratings yet

- IB Economics SL Paper 1 Question Bank - TYCHRDocument25 pagesIB Economics SL Paper 1 Question Bank - TYCHRansirwayneNo ratings yet

- Theory & EmpiricsDocument15 pagesTheory & EmpiricskerrypwlNo ratings yet

- Day 2 SlidesDocument24 pagesDay 2 SlidesEyob MogesNo ratings yet

- Notes Public EconomicsDocument132 pagesNotes Public EconomicsTWIZERIMANA EVARISTENo ratings yet

- Week9 Thursday SlidesDocument36 pagesWeek9 Thursday SlidesSiham BuuleNo ratings yet

- Topic 06 FinanceDocument55 pagesTopic 06 Financemarvalle2001No ratings yet

- CUAC 408 Advanced Taxation Course Outline 2023Document9 pagesCUAC 408 Advanced Taxation Course Outline 2023Fungai ManganaNo ratings yet

- Economics AssignmentDocument10 pagesEconomics AssignmentRama ChandranNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- The Entrepreneur’S Dictionary of Business and Financial TermsFrom EverandThe Entrepreneur’S Dictionary of Business and Financial TermsNo ratings yet

- 2010 - VantWioud Book - TheIntegratedArchitectureFrame (H1 & H2)Document35 pages2010 - VantWioud Book - TheIntegratedArchitectureFrame (H1 & H2)Zubin PengelNo ratings yet

- Draw Conclusions and Formulate Recommendations (ABM - BES12-Ia-c-4)Document6 pagesDraw Conclusions and Formulate Recommendations (ABM - BES12-Ia-c-4)Aimee LasacaNo ratings yet

- Literature Review On Underwater WindmillDocument7 pagesLiterature Review On Underwater Windmillc5rr5sqw100% (1)

- Buku Petunjuk Tata Cara Berlalu Lintas Highwaycode Di IndonesiaDocument17 pagesBuku Petunjuk Tata Cara Berlalu Lintas Highwaycode Di IndonesiadianNo ratings yet

- Underpass Top Down PaperDocument17 pagesUnderpass Top Down PaperAlok MehtaNo ratings yet

- Transportation Laws (Maritime Commerce)Document64 pagesTransportation Laws (Maritime Commerce)Angel Deiparine100% (1)

- Ford Ranger ManualDocument266 pagesFord Ranger ManualHerWagner100% (9)

- Tyco Hypermist - Full Manual (Recvd 22.04.2013)Document40 pagesTyco Hypermist - Full Manual (Recvd 22.04.2013)Rachit100% (2)

- Ethics Marks Improvement Booklet 2023Document63 pagesEthics Marks Improvement Booklet 2023Jas SinNo ratings yet

- Steve Transou JR ResumeDocument2 pagesSteve Transou JR Resumeapi-296273934No ratings yet

- Measure Theory Notes Anwar KhanDocument171 pagesMeasure Theory Notes Anwar KhanMegan SNo ratings yet

- Fuels and Fuel Handling Systems, For Steam GeneratorsDocument15 pagesFuels and Fuel Handling Systems, For Steam Generatorssam willNo ratings yet

- Public Sector Financial Accounting Techniques A. Public Sector Financial Accounting TechniquesDocument3 pagesPublic Sector Financial Accounting Techniques A. Public Sector Financial Accounting TechniquesRANIA ABDUL AZIZ BARABANo ratings yet

- Rolling of ShipsDocument37 pagesRolling of ShipsMark Antolino75% (8)

- Welding Journal 1959 8Document142 pagesWelding Journal 1959 8AlexeyNo ratings yet

- Keyman Insurance Lic India PolicyDocument2 pagesKeyman Insurance Lic India PolicyPriyanka KumariNo ratings yet

- "Doing" StrategyDocument10 pages"Doing" StrategyHendra PoltakNo ratings yet

- Application Form Incoming 1st Year CollegeDocument4 pagesApplication Form Incoming 1st Year Collegekrazy uwuNo ratings yet

- Darshan Shetty BeatDocument12 pagesDarshan Shetty Beatdarshan shettyNo ratings yet

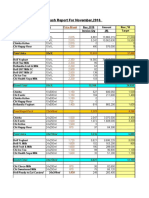

- Aba Monthly Report As at Nov (1) .'10Document78 pagesAba Monthly Report As at Nov (1) .'10Vivek RaghavNo ratings yet

- Microscan MS-3 Laser Scanner: Device Driver User GuideDocument43 pagesMicroscan MS-3 Laser Scanner: Device Driver User GuidePavan Kumar KattimaniNo ratings yet

- PESTEL Analysis of NigeriaDocument3 pagesPESTEL Analysis of NigeriaSUHANI JAIN 2023275No ratings yet

- Separate Legal EntityDocument1 pageSeparate Legal EntityShravan NiranjanNo ratings yet

- Pidex - MKP Invoice - RA Bill 02Document1 pagePidex - MKP Invoice - RA Bill 02kather MohideenNo ratings yet

- PragueDocument27 pagesPragueEric Livingston100% (1)

- Bank of India (Officers') Service Regulations, 1979Document318 pagesBank of India (Officers') Service Regulations, 1979AtanuNo ratings yet

- Tanglewood CasebookDocument86 pagesTanglewood CasebookMaricar Camagong AlbanoNo ratings yet

- Geomining Guide GBDocument165 pagesGeomining Guide GBProcess ScmiNo ratings yet

- PLC Work BookDocument15 pagesPLC Work BookAsrarLoonNo ratings yet

- BizhubPRO1050 1050e 1050P 1050ePFieldServiceDocument1,365 pagesBizhubPRO1050 1050e 1050P 1050ePFieldServiceMarcio York CardosoNo ratings yet