You might also like

- Brandbook FordDocument100 pagesBrandbook FordSatria Rangga Cipta100% (3)

- Marketing ImaginationDocument25 pagesMarketing ImaginationMatt CruzNo ratings yet

- CH 4 - Relevant Costing Principles ICAP Questions and SolutionDocument35 pagesCH 4 - Relevant Costing Principles ICAP Questions and SolutionMuhammad AzamNo ratings yet

- How To Use This Module: Module 6: Developing A Business PlanDocument17 pagesHow To Use This Module: Module 6: Developing A Business PlanYejira KionNo ratings yet

- This Study Resource Was: PAS 2 InventoriesDocument3 pagesThis Study Resource Was: PAS 2 Inventorieshsjhs100% (2)

- Marketing PlanDocument17 pagesMarketing PlanHamza ButtNo ratings yet

- Solution Manual For Strategic Management Theory Cases An Integrated Approach 13th Edition Charles W L Hill Melissa A Schilling Gareth R JonesDocument25 pagesSolution Manual For Strategic Management Theory Cases An Integrated Approach 13th Edition Charles W L Hill Melissa A Schilling Gareth R JonesBrandonBridgesqabm100% (32)

- Liquidation Value Act 1Document1 pageLiquidation Value Act 1Mika MolinaNo ratings yet

- QUIZZER Cost of CapitalDocument8 pagesQUIZZER Cost of CapitalJOHN PAOLO EVORANo ratings yet

- Chapter 11 Relevant Costs For Non Routine Decision MakingDocument24 pagesChapter 11 Relevant Costs For Non Routine Decision MakingCristine Jane Moreno Camba50% (2)

- Solutions Prada PDFDocument28 pagesSolutions Prada PDFneoss1190% (1)

- Cargo Management White PaperDocument10 pagesCargo Management White PaperFarhan AnjumNo ratings yet

- BlueprintDocument19 pagesBlueprintmaryamsiti504100% (1)

- Future of POL RetailingDocument18 pagesFuture of POL RetailingSuresh MalodiaNo ratings yet

- ZMSQ 08 Capital BudgetingDocument10 pagesZMSQ 08 Capital BudgetingMary Grace Narag100% (1)

- Digital MarketingDocument29 pagesDigital MarketingRitik Garodia100% (1)

- Paytmmm123 PDFDocument50 pagesPaytmmm123 PDFParth prajapati100% (1)

- Total Cost of Holding Inventory WhitepaperDocument2 pagesTotal Cost of Holding Inventory Whitepapershastri_shyam5073No ratings yet

- Review 105 - Day 18 MASDocument11 pagesReview 105 - Day 18 MASXNo ratings yet

- Review 105 - Day 18 MASDocument11 pagesReview 105 - Day 18 MASXNo ratings yet

- Inventory ModelDocument11 pagesInventory ModelAyrton BenavidesNo ratings yet

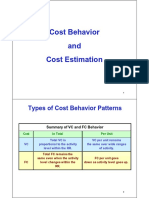

- Cost Behavior and Cost Estimation Cost EstimationDocument13 pagesCost Behavior and Cost Estimation Cost Estimationdannielle samatha tolentinoNo ratings yet

- Cost Acctg Absorption QuizDocument5 pagesCost Acctg Absorption QuizNah HamzaNo ratings yet

- Inventory Management, Supply Contracts and Risk PoolingDocument81 pagesInventory Management, Supply Contracts and Risk PoolingnaniagricoNo ratings yet

- Business Finance ReviewerDocument1 pageBusiness Finance Reviewercali kNo ratings yet

- Lecture Notes: Learning Objective 1: Understand How Fixed and Variable Costs Behave and How To Use Them To Predict CostsDocument19 pagesLecture Notes: Learning Objective 1: Understand How Fixed and Variable Costs Behave and How To Use Them To Predict CostsĐức LộcNo ratings yet

- Cost: Drivers of Supply ChainDocument3 pagesCost: Drivers of Supply ChainPooja ChaudharyNo ratings yet

- 74695bos60485 Inter p1 cp5 U1Document20 pages74695bos60485 Inter p1 cp5 U1Just KiddingNo ratings yet

- Inventory Management and Short Term Financing ManagementDocument2 pagesInventory Management and Short Term Financing ManagementYOSH 47No ratings yet

- D8Document11 pagesD8neo14100% (1)

- Cost Accounting Nature of Costs/Cost Volume Profit Analysis IDocument25 pagesCost Accounting Nature of Costs/Cost Volume Profit Analysis IMackenzie Heart Obien0% (1)

- Lecture Notes: "In Business Insights"Document44 pagesLecture Notes: "In Business Insights"DIANE EDRANo ratings yet

- PB 3 Cost AccountingDocument5 pagesPB 3 Cost AccountingAccountantNo ratings yet

- Paper 3 Set 1 TybscDocument3 pagesPaper 3 Set 1 TybscJiteshNo ratings yet

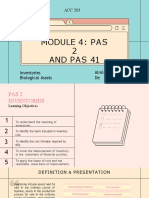

- ACC 203 Module 4 PAS 2 Inventories PAS 41 Biological AssetsDocument15 pagesACC 203 Module 4 PAS 2 Inventories PAS 41 Biological AssetsKirsty SicamNo ratings yet

- Determining The Target Cash Balance: Appendix 27ADocument8 pagesDetermining The Target Cash Balance: Appendix 27AEstefanīa Galarza100% (1)

- CA IPCC As - 2,7,9,10 Accounts As by Rohan SirDocument38 pagesCA IPCC As - 2,7,9,10 Accounts As by Rohan SirJoya AhasanNo ratings yet

- MAS 1 1st Long QuizDocument6 pagesMAS 1 1st Long QuizHanna Lyn BaliscoNo ratings yet

- Inventories ThoeryDocument10 pagesInventories ThoeryAltessa Lyn ContigaNo ratings yet

- This Study Resource Was: MASPW-TheoriesDocument1 pageThis Study Resource Was: MASPW-TheoriesMicaela EncinasNo ratings yet

- Basic Cost Term and Concepts - An Inrodution 13.12.22Document36 pagesBasic Cost Term and Concepts - An Inrodution 13.12.22JayaNo ratings yet

- Pricing Schemes: Lesson ProperDocument5 pagesPricing Schemes: Lesson ProperGoogle UserNo ratings yet

- Textbook+Examples+9.2-9.10+ Copy+From+Old+TextbookDocument13 pagesTextbook+Examples+9.2-9.10+ Copy+From+Old+Textbookotlotleng.sebelebeleNo ratings yet

- Assignment 2-Zienab MosabbehDocument3 pagesAssignment 2-Zienab MosabbehZienab MosabbehNo ratings yet

- Ch1 Aggregate InvventoryDocument29 pagesCh1 Aggregate InvventoryTommy WarNo ratings yet

- PDF Warren SM ch07 Final - CompressDocument20 pagesPDF Warren SM ch07 Final - CompressBerliana MustikasariNo ratings yet

- Lesson-04, DEPPRECIATION ACCDocument17 pagesLesson-04, DEPPRECIATION ACCZegera MgendiNo ratings yet

- Unit 3 Practice Exam: Answer The Questions On A Separate Sheet of Paperplease Do Not Write On This Practice TestDocument6 pagesUnit 3 Practice Exam: Answer The Questions On A Separate Sheet of Paperplease Do Not Write On This Practice TestKristina AnapeNo ratings yet

- 04 ABSORPTION AND VARIABLE COSTING - Rev23 24Document4 pages04 ABSORPTION AND VARIABLE COSTING - Rev23 24Kyn RusselNo ratings yet

- Cost of Sales and SG&ADocument2 pagesCost of Sales and SG&AUberNo ratings yet

- Total Cost of Ownership Analysis: by Mohammad Shujaat MubarikDocument15 pagesTotal Cost of Ownership Analysis: by Mohammad Shujaat MubarikHammad MirzaNo ratings yet

- Managerial Accounting Code: 0502603Document21 pagesManagerial Accounting Code: 0502603nanaNo ratings yet

- Chapter 2 Single Item Demand Varying at Approximate LevelDocument69 pagesChapter 2 Single Item Demand Varying at Approximate LevelSota BìnhNo ratings yet

- Costing Summary Notes HJ HandwrittenDocument39 pagesCosting Summary Notes HJ Handwrittenanshuno247No ratings yet

- Quizzer-Cost-Behavior - Docx Regression Analysis Least SquaresDocument1 pageQuizzer-Cost-Behavior - Docx Regression Analysis Least SquareslastjohnNo ratings yet

- Vada PavDocument8 pagesVada PavRytham BhutaniNo ratings yet

- Inventory ValuationDocument16 pagesInventory ValuationKillari PadmasriNo ratings yet

- Inventory Models: 1 SlideDocument31 pagesInventory Models: 1 SlidetecharupNo ratings yet

- Questions - CVP Analysis and Decision MakingDocument58 pagesQuestions - CVP Analysis and Decision Makinghukumsingh01juneNo ratings yet

- Group Assignment 1Document2 pagesGroup Assignment 1raniNo ratings yet

- Intermediate Accounting 19th Edition Stice Solutions ManualDocument33 pagesIntermediate Accounting 19th Edition Stice Solutions Manualseteepupeuritor100% (17)

- Intermediate Accounting 19Th Edition Stice Solutions Manual Full Chapter PDFDocument66 pagesIntermediate Accounting 19Th Edition Stice Solutions Manual Full Chapter PDFDebraWhitecxgn100% (7)

- 13.3 As 2 Valuation of Inventories Revision Notes by Nitin Goel Sir PDFDocument6 pages13.3 As 2 Valuation of Inventories Revision Notes by Nitin Goel Sir PDFSrinishaNo ratings yet

- Long Lived AssetsDocument51 pagesLong Lived AssetsAshraf GeorgeNo ratings yet

- 064 PDFDocument9 pages064 PDFWe WNo ratings yet

- CostDocument10 pagesCostDanial KhawajaNo ratings yet

- Ia MidtermDocument4 pagesIa MidtermJim LubianoNo ratings yet

- Final Examination: Group - Iii Paper-13: Management Accounting - Strategic ManagementDocument42 pagesFinal Examination: Group - Iii Paper-13: Management Accounting - Strategic Management2k20dmba087 piyushkumarNo ratings yet

- Albania EST Application 20.2Document40 pagesAlbania EST Application 20.2ThierryNo ratings yet

- Factors Influencing eWOM Effects: Using Experience, Credibility, and SusceptibilityDocument6 pagesFactors Influencing eWOM Effects: Using Experience, Credibility, and Susceptibilityuki arrownaraNo ratings yet

- Dimensions of Consumer BehaviorDocument13 pagesDimensions of Consumer BehaviorlulughoshNo ratings yet

- Understanding Your Business - Situation AnalysisDocument16 pagesUnderstanding Your Business - Situation AnalysisNazish SohailNo ratings yet

- Exam Date Day Sub - Code/Name: 01 Semester Afternoon: 2 P.M. To 5 P.M. SessionDocument4 pagesExam Date Day Sub - Code/Name: 01 Semester Afternoon: 2 P.M. To 5 P.M. SessionMurali VasudevanNo ratings yet

- Week 5 Workshop Handbook BMC LC PricingDocument29 pagesWeek 5 Workshop Handbook BMC LC Pricingpratik.chitnis2325pNo ratings yet

- Bachelor Research Project GuideDocument16 pagesBachelor Research Project GuideMaestro SalvatoréNo ratings yet

- Business Idea CanvasDocument1 pageBusiness Idea CanvasActive88No ratings yet

- Quiz 13Document5 pagesQuiz 13operationNo ratings yet

- Group 1 Business Plan in EntrepDocument6 pagesGroup 1 Business Plan in EntrepLuis SistosoNo ratings yet

- Marketing Environment in Nepal and Its Impact On Marketing ActivitiesDocument9 pagesMarketing Environment in Nepal and Its Impact On Marketing ActivitieslaxmikatshankhiNo ratings yet

- STP: Segmentation, Targeting and Positioning: Presented By: Ravi RamoliyaDocument35 pagesSTP: Segmentation, Targeting and Positioning: Presented By: Ravi RamoliyaRavi RamoliyaNo ratings yet

- FM Case StudyDocument4 pagesFM Case StudyNathan ViñasNo ratings yet

- Internship Report On KhaadiDocument21 pagesInternship Report On KhaadiImtiaz AliNo ratings yet

- .Notes - Complete Digital Marketing Course PDFDocument26 pages.Notes - Complete Digital Marketing Course PDFabdul sagheerNo ratings yet

- Marketing Research Case StudyDocument5 pagesMarketing Research Case StudyMohit Kumar SinghNo ratings yet

- Core Competencies Cafe OutliDocument5 pagesCore Competencies Cafe OutliobisonandlawNo ratings yet

- Attitude of Delhi Shoppers Towards Mall Experience 2Document26 pagesAttitude of Delhi Shoppers Towards Mall Experience 2Soumya ShankarNo ratings yet

- Mobile Apps and AdvertisingDocument9 pagesMobile Apps and AdvertisingInMobi100% (1)

- Welcome To Our PresentationDocument28 pagesWelcome To Our PresentationSifath Adnan Khan SifathNo ratings yet