You might also like

- 1 Unsolved Demand Supply and Market Equilibrium GK - Copy - 2Document18 pages1 Unsolved Demand Supply and Market Equilibrium GK - Copy - 2Muhammad SohailNo ratings yet

- Net Exam AnswerDocument19 pagesNet Exam AnswerSrithar Sai100% (1)

- Business Economics 1Document9 pagesBusiness Economics 1Papa DeltaNo ratings yet

- Questions For MicroeconomicsDocument5 pagesQuestions For MicroeconomicsOliver Talip100% (1)

- Econ 101 Multiple ChoiceDocument9 pagesEcon 101 Multiple ChoiceTendai Elvis MugoviNo ratings yet

- Man Econ Reviewer Base OnDocument7 pagesMan Econ Reviewer Base Ontjcute125No ratings yet

- (A) Table That Shows Relationship Between Price and Quantity DemandedDocument7 pages(A) Table That Shows Relationship Between Price and Quantity DemandedAjinkya ParkheNo ratings yet

- Revision Test - Ii STD - Xii (Economics) : Seventh Day Adventist Higher Secondary SchoolDocument7 pagesRevision Test - Ii STD - Xii (Economics) : Seventh Day Adventist Higher Secondary SchoolbhavyaNo ratings yet

- L-1344 Abdullah (A-5)Document20 pagesL-1344 Abdullah (A-5)AMIR KHANNo ratings yet

- Paper:4 Mock Test-5 MARKS:100Document16 pagesPaper:4 Mock Test-5 MARKS:100Ayathii EducareNo ratings yet

- MCQ Eco 1Document2 pagesMCQ Eco 1kavitachordiya860% (1)

- Managerial Economics Question BankDocument21 pagesManagerial Economics Question BankM.Satyendra kumarNo ratings yet

- Sample Questions - Quiz BeeDocument17 pagesSample Questions - Quiz BeeYumi GushikenNo ratings yet

- Business Economics MBA 103 MCOM 103Document13 pagesBusiness Economics MBA 103 MCOM 103poonamNo ratings yet

- Demand MCQDocument8 pagesDemand MCQsanchita kapoorNo ratings yet

- More Multiple Choice Questions With AnswersDocument14 pagesMore Multiple Choice Questions With AnswersJudz Sawadjaan100% (2)

- Sample Quiz EconomicsDocument8 pagesSample Quiz EconomicsCrystal GajoneraNo ratings yet

- Chapter 3 MCQs and Analytical Qs Supply and DemandDocument8 pagesChapter 3 MCQs and Analytical Qs Supply and Demandhamna ikramNo ratings yet

- Business Eco TestDocument8 pagesBusiness Eco Testca.krish2005No ratings yet

- Mefa Objective QuestionsDocument15 pagesMefa Objective QuestionsSaara Khan50% (4)

- Test Bank For Principles of Microeconomics 8th EditionDocument51 pagesTest Bank For Principles of Microeconomics 8th Editionmanuelphelimur4kd5No ratings yet

- CA Foundation EcoDocument14 pagesCA Foundation Ecorishab kumarNo ratings yet

- Exercises For ECO120 (Chapter 1-4)Document15 pagesExercises For ECO120 (Chapter 1-4)Celyn Anne Jati EkongNo ratings yet

- Quiz - Chapter 4 Multiple ChoiceDocument24 pagesQuiz - Chapter 4 Multiple Choicetheonelikejibi100% (1)

- Test Series: October, 2019 Foundation Course Mock Test Paper 1 Paper - 4: Part I: Business Economics Max. Marks: 60Document16 pagesTest Series: October, 2019 Foundation Course Mock Test Paper 1 Paper - 4: Part I: Business Economics Max. Marks: 60Likitha NNo ratings yet

- CB2400 Tick & Learn BASIC SUPPLY & DEMAND MODELDocument4 pagesCB2400 Tick & Learn BASIC SUPPLY & DEMAND MODELrickowongNo ratings yet

- Econ, Sample Exam 270Document8 pagesEcon, Sample Exam 270VivienNo ratings yet

- Microeconomics 1 Final ReviewDocument12 pagesMicroeconomics 1 Final ReviewCảnh Dương100% (1)

- Last Year Mid Exam QuestionsDocument8 pagesLast Year Mid Exam QuestionsTofik Mohammed100% (1)

- 12th Economics Revision MCQsDocument4 pages12th Economics Revision MCQsneerja.more2014No ratings yet

- Economics Aau Last Year Mid Exam NNMDocument12 pagesEconomics Aau Last Year Mid Exam NNMHana LeulsegedNo ratings yet

- MCQ Micro EconomicsDocument16 pagesMCQ Micro EconomicsINFOPARK CSCNo ratings yet

- 2.1 Bayne Chap 2Document5 pages2.1 Bayne Chap 2Jennifer PradoNo ratings yet

- CH 2Document11 pagesCH 2ceojiNo ratings yet

- Ca Foundation Business Economics Additional Question PaperDocument9 pagesCa Foundation Business Economics Additional Question PaperSushant TaleNo ratings yet

- Multiple Choice Q's For Revision 1-25Document6 pagesMultiple Choice Q's For Revision 1-25IDEAL DRAGONSNo ratings yet

- 856 Economics - Isc SpecimenDocument21 pages856 Economics - Isc SpecimenTeamURINo ratings yet

- MCQ and Conceptual QuestionsDocument14 pagesMCQ and Conceptual QuestionsAbhisek MishraNo ratings yet

- Microeconomics Sample Practice Multiple Choice QuestionsDocument10 pagesMicroeconomics Sample Practice Multiple Choice QuestionsManohar Reddy86% (59)

- 40 % MENDATARY OF Micro Economics - BDocument6 pages40 % MENDATARY OF Micro Economics - BBalochNo ratings yet

- Tutorial 3 QuestionsDocument7 pagesTutorial 3 QuestionsJudah SaliniNo ratings yet

- Managerial Economics MCQ"SDocument8 pagesManagerial Economics MCQ"SGuruKPO93% (14)

- Economics Test Demand and SupplyDocument10 pagesEconomics Test Demand and SupplyHarshit AgarwalNo ratings yet

- ADL 04 Managerial Economics V3Document6 pagesADL 04 Managerial Economics V3solvedcare100% (1)

- Practice Quizes 4Document6 pagesPractice Quizes 4Audrey JacksonNo ratings yet

- All in One-Test BankDocument33 pagesAll in One-Test BankSyed Irtiza HaiderNo ratings yet

- Business Economics Objective Type Questions Chapter - 1 Choose The Correct AnswerDocument11 pagesBusiness Economics Objective Type Questions Chapter - 1 Choose The Correct AnswerPraveen Perumal PNo ratings yet

- A. B. C. D.: EconomicsDocument57 pagesA. B. C. D.: EconomicsASMARA HABIBNo ratings yet

- MS EconomicsDocument16 pagesMS EconomicsSachinNo ratings yet

- Quiz 2 - Microeconomics Pindyck and Rubinfeld MCQ QuestionsDocument3 pagesQuiz 2 - Microeconomics Pindyck and Rubinfeld MCQ Questionsanusha50067% (3)

- Eco All Chap MCQDocument523 pagesEco All Chap MCQRadhaNo ratings yet

- Eco Nov 2023 Test Paper With AnswersDocument6 pagesEco Nov 2023 Test Paper With Answersbaidshruti123No ratings yet

- Chapter 4-Elasticity Practice QuestionsDocument6 pagesChapter 4-Elasticity Practice QuestionsTrung Kiên Nguyễn100% (1)

- Eco Second TermDocument5 pagesEco Second TermomotayoogundeleNo ratings yet

- Chapter 2 - Part 2Document9 pagesChapter 2 - Part 2dylanNo ratings yet

- ICAI CA Found. Eco & BCK Paper 30.07.2021Document14 pagesICAI CA Found. Eco & BCK Paper 30.07.2021Mitanshu MittalNo ratings yet

- Name: - Date: - : Table: Consumer Surplus and Phantom TicketsDocument12 pagesName: - Date: - : Table: Consumer Surplus and Phantom TicketsRacaz EwingNo ratings yet

- AP Computer Science Principles: Student-Crafted Practice Tests For ExcellenceFrom EverandAP Computer Science Principles: Student-Crafted Practice Tests For ExcellenceNo ratings yet

- 0 Transmitting 132Kv Substation 1 Project Master Schedule: Construction DrawingsDocument39 pages0 Transmitting 132Kv Substation 1 Project Master Schedule: Construction Drawingsshahidbolar0% (1)

- Distribution Control: Salma ElsayedDocument29 pagesDistribution Control: Salma ElsayedSalma El SayedNo ratings yet

- Kep Dirjen Migas No-84-K 38 DJM 1998Document22 pagesKep Dirjen Migas No-84-K 38 DJM 1998andika eka putraNo ratings yet

- MEFA Questions and AnswersDocument15 pagesMEFA Questions and AnswersG. Somasekhar SomuNo ratings yet

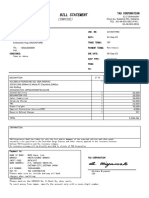

- Bill Statement: (Invoice)Document1 pageBill Statement: (Invoice)Terrence LimNo ratings yet

- Objectives of Financial StatementsDocument3 pagesObjectives of Financial StatementsNelly GomezNo ratings yet

- Ax Ujjivn1707300775682Document38 pagesAx Ujjivn1707300775682salomiv98No ratings yet

- YORK VRF IDU Ceiling Duct Compact - JTDN (022-071) - Installation Manual - FAN-1700 201602Document22 pagesYORK VRF IDU Ceiling Duct Compact - JTDN (022-071) - Installation Manual - FAN-1700 201602Daniela BecerraNo ratings yet

- Hatten Land Forms Joint Venture With Singapore Fintech Group Hydra XDocument4 pagesHatten Land Forms Joint Venture With Singapore Fintech Group Hydra XWeR1 Consultants Pte LtdNo ratings yet

- Work Sheet-Business Studies Chapter 3 Business EnvironmentDocument3 pagesWork Sheet-Business Studies Chapter 3 Business EnvironmentSafa SamreenNo ratings yet

- Cash Balance Per Bank Versus Per BookDocument6 pagesCash Balance Per Bank Versus Per BookSyrill CayetanoNo ratings yet

- SFA Framing Guide 07 PDFDocument12 pagesSFA Framing Guide 07 PDFalattar98No ratings yet

- Sol. Man. Chapter 10 Investments in Debt Securities Ia Part 1a 2020 EditionDocument34 pagesSol. Man. Chapter 10 Investments in Debt Securities Ia Part 1a 2020 EditionMizza Moreno Cantila100% (1)

- cl-12 Economics Lesson Plan 2023-24Document30 pagescl-12 Economics Lesson Plan 2023-24kuldeepbhatt0786No ratings yet

- UK Financial Regulation Ed23-5 PDFDocument298 pagesUK Financial Regulation Ed23-5 PDFVincenzo Somma100% (2)

- The New Normal Case Study TFC ScribdDocument2 pagesThe New Normal Case Study TFC ScribdTasneemNo ratings yet

- 11 Oct 2022Document3 pages11 Oct 2022Maestro ProsperNo ratings yet

- Marketing in Nepalese Microfinance InstitutionsDocument16 pagesMarketing in Nepalese Microfinance InstitutionschiranrgNo ratings yet

- Hasbah Offshore Gas Facilities Increment-II: Project at A Glance Field InformationDocument2 pagesHasbah Offshore Gas Facilities Increment-II: Project at A Glance Field InformationAltamas RehanNo ratings yet

- Five Year Plans: Presented By:Mr - Robin J Bhatti MSN-2 YearDocument36 pagesFive Year Plans: Presented By:Mr - Robin J Bhatti MSN-2 YearAsta LavistaNo ratings yet

- Morgan McKinley Sales & Marketing Salary Survey Guide - UAE 2014Document9 pagesMorgan McKinley Sales & Marketing Salary Survey Guide - UAE 2014amilaxpNo ratings yet

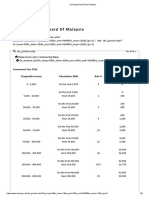

- Inland Revenue Board of Malaysia: Eng MalDocument6 pagesInland Revenue Board of Malaysia: Eng Malathirah jamaludinNo ratings yet

- Fib Assignment SolutionsDocument15 pagesFib Assignment SolutionsMusangabu EarnestNo ratings yet

- Paper No 123 - An Inquiry Into The Socio-Economic ConditionsDocument24 pagesPaper No 123 - An Inquiry Into The Socio-Economic ConditionsVibhu VikramadityaNo ratings yet

- KRA For GPPDocument1 pageKRA For GPPGPPAYASINo ratings yet

- Unit 2Document8 pagesUnit 2Tatiana DortaNo ratings yet

- Pemanfaatan Teknologi Pascapanen Untuk Pengembanga PDFDocument15 pagesPemanfaatan Teknologi Pascapanen Untuk Pengembanga PDFKhairil HarahapNo ratings yet

- Econ For IB Hoang ANSWERS Chapt1-15Document35 pagesEcon For IB Hoang ANSWERS Chapt1-15Tarini KETKAR [12S1]100% (1)

- Ass. 1Document2 pagesAss. 1Tamer MohamedNo ratings yet

- CB Insights - Tech MA Report Q3 2023Document40 pagesCB Insights - Tech MA Report Q3 2023Ishrak ZamanNo ratings yet