You might also like

- Comprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeFrom EverandComprehensive Manual of Internal Audit Practice and Guide: The Most Practical Guide to Internal Auditing PracticeRating: 5 out of 5 stars5/5 (1)

- May 17 20 Effective Audit Report WritingDocument16 pagesMay 17 20 Effective Audit Report WritingIda DawsonNo ratings yet

- Topic 1Document15 pagesTopic 1farai mokinaNo ratings yet

- Overview of The Professional Practices Framework: Presented To The Dallas Chapter IIA By: Lori Rainwater, CIA, CPA, CFEDocument35 pagesOverview of The Professional Practices Framework: Presented To The Dallas Chapter IIA By: Lori Rainwater, CIA, CPA, CFEAaronJosiahNo ratings yet

- Chapter 2 IA StandardsDocument16 pagesChapter 2 IA Standards陈韦杰No ratings yet

- SIBULO - ACEL 407 - Assignment #1 - The IPPFDocument4 pagesSIBULO - ACEL 407 - Assignment #1 - The IPPFNicole Anne Santiago SibuloNo ratings yet

- Internal Control Frameworks, Standards and Guidelines ComparisonDocument51 pagesInternal Control Frameworks, Standards and Guidelines ComparisonJoana Maiko Rizon AcostaNo ratings yet

- Presentation of Expertise Training CourseDocument74 pagesPresentation of Expertise Training CourseOmnia HassanNo ratings yet

- Quality Assurance and Improvement ProgramDocument4 pagesQuality Assurance and Improvement ProgramIvan Jake GonzalesNo ratings yet

- IppfDocument2 pagesIppfjukuNo ratings yet

- UI Internal Audit Syllabus 2017Document5 pagesUI Internal Audit Syllabus 2017blackraidenNo ratings yet

- Factsheet: The International Professional Practices Framework (IPPF)Document2 pagesFactsheet: The International Professional Practices Framework (IPPF)hisham hussainNo ratings yet

- Silabus Internal Audit FEB 2017-2018Document5 pagesSilabus Internal Audit FEB 2017-2018agus suhendraNo ratings yet

- 02 - PG - Creating An IA Competency Process For The Public Sector (February 2015)Document24 pages02 - PG - Creating An IA Competency Process For The Public Sector (February 2015)Herman EfNo ratings yet

- Audit Management: Gede Leo Nadi Danuarta Kevin Harijanto Caren Angellina MimakiDocument15 pagesAudit Management: Gede Leo Nadi Danuarta Kevin Harijanto Caren Angellina MimakiLeo DanuartaNo ratings yet

- The IIA Standards: The IPPF Framework: Speaker: Dott. Roberto RosatoDocument38 pagesThe IIA Standards: The IPPF Framework: Speaker: Dott. Roberto RosatoAntoniaAyuMahardika100% (2)

- GTAG-14 Edited With Ad 05-20-20101 PDFDocument32 pagesGTAG-14 Edited With Ad 05-20-20101 PDFpiornelNo ratings yet

- AUDIT Journal 14Document12 pagesAUDIT Journal 14Daena NicodemusNo ratings yet

- The Framework For Internal Audit Effectiveness The New IPPF BrochureDocument10 pagesThe Framework For Internal Audit Effectiveness The New IPPF Brochureaichaanalyst4456100% (1)

- Presentation On ThemeDocument37 pagesPresentation On Themeembiale ayaluNo ratings yet

- Presentation Internal Audit StandardsDocument98 pagesPresentation Internal Audit StandardsAbera100% (1)

- Ios Aud 2016 06 Saiv ReportDocument15 pagesIos Aud 2016 06 Saiv ReportAndrew WainainaNo ratings yet

- Practice Bulletin - Assessment of Internal Audit FunctionDocument14 pagesPractice Bulletin - Assessment of Internal Audit FunctionCherylNo ratings yet

- TESDA Circular No. 079-2020Document23 pagesTESDA Circular No. 079-2020Twinkle MiguelNo ratings yet

- SlideDocument21 pagesSlidePhumzile MpanzaNo ratings yet

- GTAG-15 Edited With Ad 05-20-20101 PDFDocument28 pagesGTAG-15 Edited With Ad 05-20-20101 PDFpiornelNo ratings yet

- Information Security Governance: IPPF - Practice GuideDocument27 pagesInformation Security Governance: IPPF - Practice GuideFrancisco Menacho Farroñay100% (1)

- Introduction to International Professional Practices Framework (IPPFDocument17 pagesIntroduction to International Professional Practices Framework (IPPFJanysse CalderonNo ratings yet

- Post-Test L1 Introduction To Internal AuditingDocument6 pagesPost-Test L1 Introduction To Internal Auditinglena cpaNo ratings yet

- Glimpse Over The Amendments in The: Revised StandardsDocument53 pagesGlimpse Over The Amendments in The: Revised Standardsmaterials downloadNo ratings yet

- Final IA Guidelines For National Government 10th March 2016Document74 pagesFinal IA Guidelines For National Government 10th March 2016Blessed VinnyNo ratings yet

- Committee Presentation: An Overview of The External Audit Process and Types of AuditsDocument20 pagesCommittee Presentation: An Overview of The External Audit Process and Types of AuditsMa KếtNo ratings yet

- SOX 404 - GuideDocument68 pagesSOX 404 - GuideMauro Aquino100% (1)

- Evaluating Ethics Related Programmes and ActivitiesDocument36 pagesEvaluating Ethics Related Programmes and Activitiesgalal2720006810No ratings yet

- Creating IA Competency in Public SectorDocument24 pagesCreating IA Competency in Public SectorwphethiNo ratings yet

- Michel Audit ManajemenDocument15 pagesMichel Audit ManajemenLeo DanuartaNo ratings yet

- Ippf 2017Document6 pagesIppf 2017Brylle TamañoNo ratings yet

- EthicsDocument41 pagesEthicsMERINANo ratings yet

- PG Assessing Organizational Governance in The Public SectorDocument36 pagesPG Assessing Organizational Governance in The Public SectorRobertoNo ratings yet

- Get To Know The Global Internal Audit StandardsDocument42 pagesGet To Know The Global Internal Audit StandardsLara Kroft100% (1)

- Audit PlaningDocument14 pagesAudit PlaningFarraNo ratings yet

- Resume Audit InternalDocument6 pagesResume Audit InternalPatricia Alvani GultomNo ratings yet

- State of Compliance of LGU To IASDocument13 pagesState of Compliance of LGU To IASIvan Jon FerriolNo ratings yet

- The International Professional Practices Framework: Jean-Pierre Garitte, CIA, CCSA, CISA, CFEDocument47 pagesThe International Professional Practices Framework: Jean-Pierre Garitte, CIA, CCSA, CISA, CFEKaren Somcio100% (1)

- The Professional Standards PDFDocument11 pagesThe Professional Standards PDFHazel Bianca GabalesNo ratings yet

- Final Draft MPA 626 Group 2 PresentationDocument215 pagesFinal Draft MPA 626 Group 2 Presentationronie alpajaroNo ratings yet

- 2019 EQA Report OIAI Internal Audit FunctionDocument35 pages2019 EQA Report OIAI Internal Audit FunctionThomas BoegballeNo ratings yet

- RMK Week 2Document10 pagesRMK Week 2rizki nurNo ratings yet

- IPPF Practice Guide. MeasurINg INterNal Audit Effectiveness and EfficiencyDocument19 pagesIPPF Practice Guide. MeasurINg INterNal Audit Effectiveness and EfficiencyFazlihaq Durrani100% (1)

- INTERNAL AUDITING OVERVIEWDocument8 pagesINTERNAL AUDITING OVERVIEWRohit SharmaNo ratings yet

- Internal Audit StrategyDocument5 pagesInternal Audit StrategyRoberto Vega100% (1)

- Examining Ethiopia's Internal Audit Regulatory FrameworkDocument12 pagesExamining Ethiopia's Internal Audit Regulatory Frameworkamanawite TeshomeNo ratings yet

- AI-X-S5-G5-Arief Budi NugrohoDocument9 pagesAI-X-S5-G5-Arief Budi Nugrohoariefmatani73No ratings yet

- Final Version MPA 626 Group 2 PresentationDocument231 pagesFinal Version MPA 626 Group 2 PresentationSherry Mae EsteleydesNo ratings yet

- Chapter 1 The Nature of Internal AuditingDocument15 pagesChapter 1 The Nature of Internal Auditingdictus_sba5008100% (3)

- IDAP Briefing071409Document101 pagesIDAP Briefing071409J. O. M. SalazarNo ratings yet

- Intosai Framework Auditing StandardDocument21 pagesIntosai Framework Auditing StandardYOGA ANINDITANo ratings yet

- Topic 4 - Internal AuditingDocument19 pagesTopic 4 - Internal AuditingSandile Henry DlaminiNo ratings yet

- Proposed Enhancements To IPPF-August 2014Document26 pagesProposed Enhancements To IPPF-August 2014Md. Milon ChowdhuryNo ratings yet

- Good Practice Internal Audit PEM PAL ENGDocument46 pagesGood Practice Internal Audit PEM PAL ENGAde Hanifa putriNo ratings yet

- 5 Topic For PNKHDocument5 pages5 Topic For PNKHBritt John BallentesNo ratings yet

- 5 HW For KMJMDocument5 pages5 HW For KMJMBritt John BallentesNo ratings yet

- CYKL Chapter 1Document4 pagesCYKL Chapter 1Britt John BallentesNo ratings yet

- Part I-1 Internal Control Fundamental ConceptsDocument51 pagesPart I-1 Internal Control Fundamental ConceptsYasser MangadangNo ratings yet

- 4 Homework Help For KMJMDocument2 pages4 Homework Help For KMJMBritt John BallentesNo ratings yet

- CYKL Exam 5Document2 pagesCYKL Exam 5Britt John BallentesNo ratings yet

- 2 Test Prep For SJBLDocument2 pages2 Test Prep For SJBLBritt John BallentesNo ratings yet

- 4 Cheat Sheet For RZTSDocument2 pages4 Cheat Sheet For RZTSBritt John BallentesNo ratings yet

- CYKL Homework Help 2Document3 pagesCYKL Homework Help 2Britt John BallentesNo ratings yet

- YHZT Lessons 3Document4 pagesYHZT Lessons 3Britt John BallentesNo ratings yet

- 4 Cheat Sheet For RZTSDocument2 pages4 Cheat Sheet For RZTSBritt John BallentesNo ratings yet

- CYKL Lecture 4Document2 pagesCYKL Lecture 4Britt John BallentesNo ratings yet

- YHZT Lessons 3Document4 pagesYHZT Lessons 3Britt John BallentesNo ratings yet

- 3 Practice For SJBLDocument2 pages3 Practice For SJBLBritt John BallentesNo ratings yet

- SJAT Answer Key 4Document2 pagesSJAT Answer Key 4andikahubirahmatNo ratings yet

- YHZT Answer 2Document3 pagesYHZT Answer 2Britt John BallentesNo ratings yet

- 1 Notes For SJBLDocument2 pages1 Notes For SJBLBritt John BallentesNo ratings yet

- YHZT Lec Notes 4Document2 pagesYHZT Lec Notes 4Britt John BallentesNo ratings yet

- TQRR Doc 4Document3 pagesTQRR Doc 4Britt John BallentesNo ratings yet

- YHZT Answer 2Document3 pagesYHZT Answer 2Britt John BallentesNo ratings yet

- TQRR Exam 1Document3 pagesTQRR Exam 1Britt John BallentesNo ratings yet

- Unauthorized Practice of Law Case Against SabandalDocument2 pagesUnauthorized Practice of Law Case Against SabandalBritt John BallentesNo ratings yet

- TQRR Lesson Plan 5Document3 pagesTQRR Lesson Plan 5Britt John BallentesNo ratings yet

- Pimentel vs. LEB case examines constitutionality of RA 7662 and powers of LEBDocument2 pagesPimentel vs. LEB case examines constitutionality of RA 7662 and powers of LEBBritt John BallentesNo ratings yet

- YHZT Summary 5Document3 pagesYHZT Summary 5Britt John BallentesNo ratings yet

- YHZT Problems 1Document3 pagesYHZT Problems 1Britt John BallentesNo ratings yet

- Elmo S. Abad, BM No. 139, March 18, 1983Document1 pageElmo S. Abad, BM No. 139, March 18, 1983Britt John BallentesNo ratings yet

- Updated 2016 Revised IRR of RA No. 9184 As of 30 June 2022 07142022aDocument391 pagesUpdated 2016 Revised IRR of RA No. 9184 As of 30 June 2022 07142022aBritt John BallentesNo ratings yet

- in Re Benjamin Dacanay, 540 SCRA 424 (2007)Document1 pagein Re Benjamin Dacanay, 540 SCRA 424 (2007)Britt John Ballentes100% (1)

- Aguirre vs. Rana, BM No. 1036, June 10, 2003Document1 pageAguirre vs. Rana, BM No. 1036, June 10, 2003Britt John BallentesNo ratings yet

- Case Study QuestionDocument3 pagesCase Study Questionathirah jamaludinNo ratings yet

- Springwell V JPMDocument80 pagesSpringwell V JPMSaqib AlamNo ratings yet

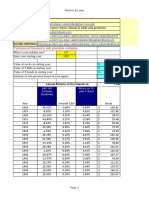

- Customized Geometric Risk Premium EstimatorDocument40 pagesCustomized Geometric Risk Premium EstimatorVíctor GómezNo ratings yet

- SWOT Analysis SummaryDocument16 pagesSWOT Analysis SummaryMaricres BiandoNo ratings yet

- Air Weapons Complex: Building Emergency Power Supply SystemDocument23 pagesAir Weapons Complex: Building Emergency Power Supply Systemjuni1289No ratings yet

- Blecker's Critique of Fundamentals-Based International Financial Models by Siya Biniza PDFDocument10 pagesBlecker's Critique of Fundamentals-Based International Financial Models by Siya Biniza PDFSiya BinizaNo ratings yet

- Checkout - Y-StrapDocument3 pagesCheckout - Y-Strapsup nessNo ratings yet

- 2018 Immunization Case - QuestionDocument2 pages2018 Immunization Case - QuestionSofia LimaNo ratings yet

- CowlDocument3 pagesCowlPrasetyo Indra SuronoNo ratings yet

- Coursework 1: Module: Business Communication Module Code: Sbl-105 Module Leader: Patience ConlonDocument13 pagesCoursework 1: Module: Business Communication Module Code: Sbl-105 Module Leader: Patience ConlonLame JoelNo ratings yet

- Role of State Bank of Pakistan in EconomicDocument20 pagesRole of State Bank of Pakistan in Economiclaiba faizNo ratings yet

- Chapter 1 - IBFDocument11 pagesChapter 1 - IBFmariumzehraNo ratings yet

- Indicative Taxnet Profile: Personal InformationDocument3 pagesIndicative Taxnet Profile: Personal InformationNaveed Ahmad MushtaqNo ratings yet

- RECALLED QUESTIONS (2016-18) : (Ibps Different Banks Promotion Test)Document11 pagesRECALLED QUESTIONS (2016-18) : (Ibps Different Banks Promotion Test)Arun PrakashNo ratings yet

- Unit 1 Acf 255 ADocument32 pagesUnit 1 Acf 255 AAugustine Kwadjo GyeningNo ratings yet

- Horngren Ima16 Tif 17 GEDocument53 pagesHorngren Ima16 Tif 17 GEasem shabanNo ratings yet

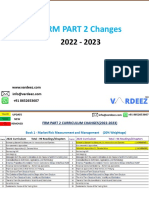

- Macro Curriculum Changes 2023 Part 2Document6 pagesMacro Curriculum Changes 2023 Part 2Al VelNo ratings yet

- Strong Tie LTDDocument15 pagesStrong Tie LTDchitu1992100% (4)

- General Principles & National Income Taxation Lecture Atty RizalinaDocument242 pagesGeneral Principles & National Income Taxation Lecture Atty RizalinaJoyce LapuzNo ratings yet

- Description of Research InterestsDocument6 pagesDescription of Research InterestsManas DimriNo ratings yet

- 5 Adjusting Entries For Prepaid ExpenseDocument4 pages5 Adjusting Entries For Prepaid Expenseapi-299265916No ratings yet

- An Assessment of The Emirates NBD BankDocument25 pagesAn Assessment of The Emirates NBD BankHND Assignment Help100% (1)

- 01-28-2022 CRC-ACE - AFAR - Week 01 - Accounting For Partnership - Part 1 FormationDocument5 pages01-28-2022 CRC-ACE - AFAR - Week 01 - Accounting For Partnership - Part 1 Formationjohn francisNo ratings yet

- IMS Internal Audit ScheduleDocument1 pageIMS Internal Audit ScheduleAkd DeshmukhNo ratings yet

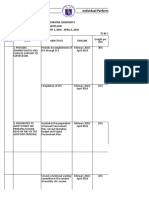

- Individual Performance Commitment and Review FormTITLE Individual Performance Commitment and Review FormDocument17 pagesIndividual Performance Commitment and Review FormTITLE Individual Performance Commitment and Review FormCabittaogan Nhs69% (13)

- Annual Report 2012 Al Arafa BankDocument150 pagesAnnual Report 2012 Al Arafa BankWasik Abdullah MomitNo ratings yet

- Pag-Ibig Mp2 Application FormDocument2 pagesPag-Ibig Mp2 Application Formroy czar pableoNo ratings yet

- DepEd - FMOM School-Based Financial Management Non IU FinalDocument62 pagesDepEd - FMOM School-Based Financial Management Non IU FinalJose Mari BaluranNo ratings yet

- Capital Structure Test QuestionsDocument28 pagesCapital Structure Test QuestionsSardonna FongNo ratings yet

- Warrant Buffet: Investment StrategyDocument16 pagesWarrant Buffet: Investment StrategyYassir SlaouiNo ratings yet