You might also like

- Interpretation of Financial Statements & Ratio AnalysisDocument35 pagesInterpretation of Financial Statements & Ratio Analysisamitsinghslideshare50% (2)

- 05 Ratios and Trend AnalysisDocument11 pages05 Ratios and Trend AnalysisHaris IshaqNo ratings yet

- BA 117 MCS and StrategyDocument18 pagesBA 117 MCS and StrategyIan De DiosNo ratings yet

- Bank of America Global Equity ValuationDocument56 pagesBank of America Global Equity Valuationrichard100% (1)

- BAB 3 - Business Analysis - BtariDocument28 pagesBAB 3 - Business Analysis - BtariBtari BungaNo ratings yet

- BA449Chap005Document50 pagesBA449Chap005mashalerahNo ratings yet

- 2023 SMA Lecture 10Document47 pages2023 SMA Lecture 10Haniie NguyenNo ratings yet

- M&ADocument151 pagesM&APallavi Prasad100% (1)

- (Report Marking Rubric) (Round 2) (FINSPEED 2021)Document1 page(Report Marking Rubric) (Round 2) (FINSPEED 2021)CuongNo ratings yet

- Nism XV - RG (191-197)Document7 pagesNism XV - RG (191-197)Rishabh R. GuptaNo ratings yet

- Chapter 4 Analysis of Financial StatementsDocument16 pagesChapter 4 Analysis of Financial StatementsKate Jazleen BaldevinoNo ratings yet

- 7.3 Overall PerformanceDocument14 pages7.3 Overall PerformanceteeeNo ratings yet

- Business Valuation and Case Study at Petrom OmvDocument46 pagesBusiness Valuation and Case Study at Petrom OmvGrigoras Alexandru NicolaeNo ratings yet

- Performance Measurement: OutlineDocument17 pagesPerformance Measurement: OutlineLưu Hồng Hạnh 4KT-20ACNNo ratings yet

- Lecture 5 - Ratio AnalysisDocument37 pagesLecture 5 - Ratio AnalysisnopeNo ratings yet

- Goals, Value and PerformanceDocument18 pagesGoals, Value and PerformanceSamridh AgarwalNo ratings yet

- Business Monitoring and Evaluation Report Template v2Document2 pagesBusiness Monitoring and Evaluation Report Template v2diegoneespinalNo ratings yet

- Executive Summary: Profitability ROIDocument16 pagesExecutive Summary: Profitability ROIskittichungchitNo ratings yet

- 1.2.1 Financial Performance RatiosDocument135 pages1.2.1 Financial Performance RatiosGary ANo ratings yet

- A fact-based approach to Align your brand portfolioDocument48 pagesA fact-based approach to Align your brand portfolioJonathan WenNo ratings yet

- Date Session On Learning From ModuleDocument34 pagesDate Session On Learning From ModuleKishore KintaliNo ratings yet

- Mock - Answer 230602 001213Document12 pagesMock - Answer 230602 001213Sanaullah ButtNo ratings yet

- Analysis & Interpretation: Prepared By: Sir Hamza Abdul HaqDocument10 pagesAnalysis & Interpretation: Prepared By: Sir Hamza Abdul HaqSrabon BaruaNo ratings yet

- Market Approach ValuationDocument33 pagesMarket Approach ValuationHamiegwyne Nicole De VeraNo ratings yet

- BR Cashflow Jul2020 D2Document11 pagesBR Cashflow Jul2020 D2TheCuriousMindNo ratings yet

- Sample Skateboard Market Analysis and Segment Forecasts To 2025Document47 pagesSample Skateboard Market Analysis and Segment Forecasts To 2025Stefu RajNo ratings yet

- Krishna G. Palepu, Paul M. Healy, Erik Peek - Business Analysis and Valuation - IFRS Edition-Cengage Learning (2013) - Chapter 5 PDFDocument58 pagesKrishna G. Palepu, Paul M. Healy, Erik Peek - Business Analysis and Valuation - IFRS Edition-Cengage Learning (2013) - Chapter 5 PDFTrần BetaNo ratings yet

- Introduction To Financial Statement Analysis: by Prof Arun Kumar Agarwal, ACA, ACS IBS, GurgaonDocument13 pagesIntroduction To Financial Statement Analysis: by Prof Arun Kumar Agarwal, ACA, ACS IBS, GurgaonPRACHI DASNo ratings yet

- Financial Statement Analysis and Security Valuation: - October 26, 2022 Arnt VerriestDocument42 pagesFinancial Statement Analysis and Security Valuation: - October 26, 2022 Arnt VerriestfelipeNo ratings yet

- Valuation Theory and Implementation SeminarDocument29 pagesValuation Theory and Implementation SeminarmattNo ratings yet

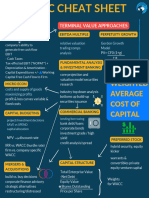

- Comprehensive Finance Cheat Sheet Collection 1698244606Document52 pagesComprehensive Finance Cheat Sheet Collection 1698244606muratgreywolf100% (1)

- CRSDocument59 pagesCRSaliotNo ratings yet

- 02 Don Angus-SP and ICR-Industry Insights v1Document15 pages02 Don Angus-SP and ICR-Industry Insights v1ticoNo ratings yet

- Ratio Analysis Template BreakdownDocument44 pagesRatio Analysis Template BreakdownrikitagujralNo ratings yet

- Business Valuation: by Ca. Aparna RammohanDocument46 pagesBusiness Valuation: by Ca. Aparna RammohanAvinash SharmaNo ratings yet

- 12 Interpretation & AnalysisDocument20 pages12 Interpretation & AnalysispesseNo ratings yet

- Economic Value AddedDocument25 pagesEconomic Value AddedSagar KansalNo ratings yet

- DELLFY10 Q2 Earnings PresentationDocument23 pagesDELLFY10 Q2 Earnings PresentationwagnebNo ratings yet

- Equity Valuation Report Singer Bangladesh LimitedDocument23 pagesEquity Valuation Report Singer Bangladesh LimitedSabrina Mila100% (1)

- PM 07 Divisional Performance Measures NotesDocument2 pagesPM 07 Divisional Performance Measures NotesTanyaNo ratings yet

- WH Tis ?: Fundamental Analysis A Fundamental AnalysisDocument7 pagesWH Tis ?: Fundamental Analysis A Fundamental AnalysisAbhinandan ChatterjeeNo ratings yet

- Financial Ratios and Analysis of Tata Motors: Research PaperDocument15 pagesFinancial Ratios and Analysis of Tata Motors: Research PaperMCOM 2050 MAMGAIN RAHUL PRASADNo ratings yet

- Good and Poor Examples of Executive SummariesDocument3 pagesGood and Poor Examples of Executive SummariesRamanpreet KaurNo ratings yet

- Options As A Strategic Investment PDFDocument5 pagesOptions As A Strategic Investment PDFArjun Bora100% (1)

- Fiche StratDocument11 pagesFiche StratOthman MouradiNo ratings yet

- Ratio analysis reveals financial healthDocument10 pagesRatio analysis reveals financial healthHoneylyn V. ChavitNo ratings yet

- (37-44) A Detailed Study of Financial Performance of Coal India Limited Post Disinvestment Using Dupont AnalysisDocument8 pages(37-44) A Detailed Study of Financial Performance of Coal India Limited Post Disinvestment Using Dupont Analysisscribd sogawNo ratings yet

- l20 To l21 - ControllingDocument68 pagesl20 To l21 - ControllinganvipotnisNo ratings yet

- Solutions - Chapter 5Document21 pagesSolutions - Chapter 5Dre ThathipNo ratings yet

- Maximizing The Value of G and ADocument5 pagesMaximizing The Value of G and AjrmachareNo ratings yet

- Managerial Accounting: Student EditionDocument19 pagesManagerial Accounting: Student EditionNadia TjiaNo ratings yet

- OpenView 2021 Financial and Operating Benchmarks ReportDocument58 pagesOpenView 2021 Financial and Operating Benchmarks ReportrrNo ratings yet

- Financial Statements Meaning and CharacteristicsDocument64 pagesFinancial Statements Meaning and CharacteristicsAbhishek SinhaNo ratings yet

- A222 - Topic 5 MacsDocument36 pagesA222 - Topic 5 MacsfiqNo ratings yet

- Lesson 8 Corporate DiversificationDocument14 pagesLesson 8 Corporate DiversificationNazia SyedNo ratings yet

- LU1 Overview of Financial Statement AnalysisDocument36 pagesLU1 Overview of Financial Statement AnalysisPriyah ThaiyalanNo ratings yet

- Value-Based Pricing: The Driver To Increased Short-Term ProfitsDocument4 pagesValue-Based Pricing: The Driver To Increased Short-Term ProfitsRiz DeenNo ratings yet

- How to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsFrom EverandHow to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsNo ratings yet

- International Business Control, Reporting and Corporate Governance: Global business best practice across cultures, countries and organisationsFrom EverandInternational Business Control, Reporting and Corporate Governance: Global business best practice across cultures, countries and organisationsRating: 5 out of 5 stars5/5 (2)