You might also like

- A Feast of Vultures: The Hidden Business of Democracy in IndiaFrom EverandA Feast of Vultures: The Hidden Business of Democracy in IndiaRating: 4 out of 5 stars4/5 (1)

- The Rise And Fall Of The Largest 3Rd World BankFrom EverandThe Rise And Fall Of The Largest 3Rd World BankRating: 5 out of 5 stars5/5 (1)

- Dongri to Dubai - Six Decades of the Mumbai MafiaFrom EverandDongri to Dubai - Six Decades of the Mumbai MafiaRating: 3.5 out of 5 stars3.5/5 (26)

- Harshad Mehta: From Pied Piper of The Markets To India's Best-Known ScamsterDocument2 pagesHarshad Mehta: From Pied Piper of The Markets To India's Best-Known ScamsterPankaj KhindriaNo ratings yet

- Fractured Freedom: A Prison Memoir - A Story of Passion, Commitment and a Search for Justice and FreedomFrom EverandFractured Freedom: A Prison Memoir - A Story of Passion, Commitment and a Search for Justice and FreedomRating: 5 out of 5 stars5/5 (1)

- Harshad MehtaDocument10 pagesHarshad MehtaKrutika AbitkarNo ratings yet

- Mamata Banerjee - Judgements For SALEDocument168 pagesMamata Banerjee - Judgements For SALENagaraja Mysore RaghupathiNo ratings yet

- Ninety Days: The True Story of the Hunt for Rajiv Gandhi's AssassinsFrom EverandNinety Days: The True Story of the Hunt for Rajiv Gandhi's AssassinsNo ratings yet

- Trials of Truth PDFDocument140 pagesTrials of Truth PDFRittik Prakash100% (2)

- Walking With Lions: Tales From A Diplomatic PastFrom EverandWalking With Lions: Tales From A Diplomatic PastRating: 3.5 out of 5 stars3.5/5 (7)

- Harshad MehtaDocument4 pagesHarshad MehtacuribenNo ratings yet

- Continue: Mitrokhin Archive Lal Bahadur Shastri PDFDocument2 pagesContinue: Mitrokhin Archive Lal Bahadur Shastri PDFAmit SinghNo ratings yet

- Headley Saga: Mumbai Attack Was A Joint IB-CIA-Mossad - RSS ProjectDocument3 pagesHeadley Saga: Mumbai Attack Was A Joint IB-CIA-Mossad - RSS ProjectMoinullah KhanNo ratings yet

- What Harshad Mehta DidDocument5 pagesWhat Harshad Mehta Didyatheesh07No ratings yet

- mg337 AllDocument24 pagesmg337 AllsyedsrahmanNo ratings yet

- Harshad Mehta Scams 26 PageDocument28 pagesHarshad Mehta Scams 26 PageSky509No ratings yet

- Harshad Mehta: What All He DidDocument4 pagesHarshad Mehta: What All He DidPrakashramkumharNo ratings yet

- The British, The Bandits and The Bordermen: From the diaries and articles of K F RustamjiFrom EverandThe British, The Bandits and The Bordermen: From the diaries and articles of K F RustamjiNo ratings yet

- Shri Shri L L..K K. - Advaniji Advaniji''s Latest Blog S Latest Blog ""The The ''Operation Polo' in Operation Polo' in Hyderabad Hyderabad""Document6 pagesShri Shri L L..K K. - Advaniji Advaniji''s Latest Blog S Latest Blog ""The The ''Operation Polo' in Operation Polo' in Hyderabad Hyderabad""rahul_didoNo ratings yet

- Case Study - Harshad MehtaDocument5 pagesCase Study - Harshad MehtaMudit AgarwalNo ratings yet

- Harshad Mehta (Big Bull)Document13 pagesHarshad Mehta (Big Bull)barun432No ratings yet

- India Legal 15 April 2014Document84 pagesIndia Legal 15 April 2014vikram1972No ratings yet

- The Forum Gazette Vol. 2 No. 14 July 20-August 4, 1987Document16 pagesThe Forum Gazette Vol. 2 No. 14 July 20-August 4, 1987SikhDigitalLibraryNo ratings yet

- Khaki in Dust Storm: Communal Colours and Political Assassinations (1980–1991) Police Diaries Book 1From EverandKhaki in Dust Storm: Communal Colours and Political Assassinations (1980–1991) Police Diaries Book 1No ratings yet

- Harshad Shantilal MehtaDocument10 pagesHarshad Shantilal MehtaRishi JainNo ratings yet

- Harshad Mehta ScamDocument4 pagesHarshad Mehta Scamvanitathakur91No ratings yet

- Workbook on Red-Handed: How American Elites Get Rich Helping China Win by Peter Schweizer (Fun Facts & Trivia Tidbits)From EverandWorkbook on Red-Handed: How American Elites Get Rich Helping China Win by Peter Schweizer (Fun Facts & Trivia Tidbits)No ratings yet

- Brownie Tales: A Book on Corporate Political SavvyFrom EverandBrownie Tales: A Book on Corporate Political SavvyRating: 2 out of 5 stars2/5 (1)

- Hasan Ali Khan Alias Syed Mohammed Hasan Ali KhanDocument10 pagesHasan Ali Khan Alias Syed Mohammed Hasan Ali KhanGoodfeller RalphNo ratings yet

- Sirisena Presidency - A Parallax ViewDocument10 pagesSirisena Presidency - A Parallax ViewThavamNo ratings yet

- Summary of Secret Empires: How the American Political Class Hides Corruption and Enriches Family and Friends by Peter SchweizerFrom EverandSummary of Secret Empires: How the American Political Class Hides Corruption and Enriches Family and Friends by Peter SchweizerNo ratings yet

- Secret Empires: How the American Political Class Hides Corruption and Enriches Family and Friends by Peter Schweizer: Summary by Fireside ReadsFrom EverandSecret Empires: How the American Political Class Hides Corruption and Enriches Family and Friends by Peter Schweizer: Summary by Fireside ReadsNo ratings yet

- Hassan Ali Khan-Fiction or FactDocument10 pagesHassan Ali Khan-Fiction or Factsilvernitrate1953100% (1)

- Pandemonium: The Great Indian Banking TragedyFrom EverandPandemonium: The Great Indian Banking TragedyRating: 5 out of 5 stars5/5 (4)

- The Forum Gazette Vol. 3 No, 22 November 20-December 4, 1988Document16 pagesThe Forum Gazette Vol. 3 No, 22 November 20-December 4, 1988SikhDigitalLibraryNo ratings yet

- YOGESH KUMAR SAXENA KAYASTHA RATNADATE of BIRTH 29th November Advocate High Court and Supreme Court Representative of World Parliament ExperimentDocument3 pagesYOGESH KUMAR SAXENA KAYASTHA RATNADATE of BIRTH 29th November Advocate High Court and Supreme Court Representative of World Parliament Experimentyogesh saxenaNo ratings yet

- Harshad Mehta Scam - The Big Bull of India CIA-2 (Case Study)Document7 pagesHarshad Mehta Scam - The Big Bull of India CIA-2 (Case Study)Ashish RawatNo ratings yet

- Subramanian Swamy Tears Into RSS and ABV GovernmentDocument6 pagesSubramanian Swamy Tears Into RSS and ABV Governmentak.narendranathNo ratings yet

- What Harshad Mehta Did? - The Stock Scam: Read Indian Stock Market ArticlesDocument13 pagesWhat Harshad Mehta Did? - The Stock Scam: Read Indian Stock Market ArticlesAnu SuvaNo ratings yet

- ScamDocument23 pagesScameunice19970315No ratings yet

- 2Document1 page2animesh sarkarNo ratings yet

- 35 Days: How Politics In Maharashtra Changed Forever In 2019From Everand35 Days: How Politics In Maharashtra Changed Forever In 2019Rating: 4 out of 5 stars4/5 (4)

- AP SBTET VI Sem Data Communication & Computer Networks (C09) June 2019 QPDocument2 pagesAP SBTET VI Sem Data Communication & Computer Networks (C09) June 2019 QPalinisamaryam1No ratings yet

- Journal Test 50 MarksDocument3 pagesJournal Test 50 MarksYash TripathiNo ratings yet

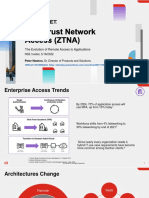

- NSE Solution Insider - Fortinet's ZTNA Solution and The 7.2 Improvements - May 19, 2022Document16 pagesNSE Solution Insider - Fortinet's ZTNA Solution and The 7.2 Improvements - May 19, 2022MonNo ratings yet

- VP Value Based Healthcare Sales in Charleston SC Resume Mitchell BaileyDocument2 pagesVP Value Based Healthcare Sales in Charleston SC Resume Mitchell BaileyMitchellBaileyNo ratings yet

- Financial Accounting Assignment 1 PDFDocument26 pagesFinancial Accounting Assignment 1 PDFUmair MughalNo ratings yet

- Guide To Participating Policies - EnglishDocument5 pagesGuide To Participating Policies - EnglishTemp RoryNo ratings yet

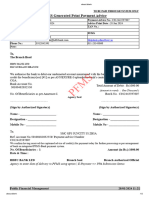

- PFMSDocument2 pagesPFMStanishka.engNo ratings yet

- Import Business in KenyaDocument131 pagesImport Business in KenyaDj Backspin254No ratings yet

- Fee - Abasynisb.edu - PK S Challan - PHPDocument1 pageFee - Abasynisb.edu - PK S Challan - PHPaltaf30895No ratings yet

- Day in The Life of A Pharmacist PDFDocument3 pagesDay in The Life of A Pharmacist PDFjoanne_rawksNo ratings yet

- CMA Part 1 Sec CDocument131 pagesCMA Part 1 Sec CMusthaqMohammedMadathilNo ratings yet

- Bonded Warehouse VS NonDocument3 pagesBonded Warehouse VS Nonphuong leNo ratings yet

- Erop 16Document553 pagesErop 16Ari cNo ratings yet

- Bill of Exchange ChargebackDocument9 pagesBill of Exchange Chargebackkingtbrown50100% (8)

- Amadeus Electronic TicketingDocument81 pagesAmadeus Electronic TicketingKablan Koye Christ ArnauldNo ratings yet

- Accounts Cec 1year Test PaparDocument2 pagesAccounts Cec 1year Test PaparMohammad MoinuddinNo ratings yet

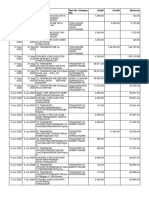

- Standard Chartered Bank Nepal MISDocument23 pagesStandard Chartered Bank Nepal MISManishDangolNo ratings yet

- Types of InsuranceDocument92 pagesTypes of InsuranceRajat BansalNo ratings yet

- Htay (Ko) & Brothers (Myanmar) - Contact Phone, AddressDocument6 pagesHtay (Ko) & Brothers (Myanmar) - Contact Phone, AddressChit LoonNo ratings yet

- Clovis Medicaid NotesDocument4 pagesClovis Medicaid NotesNM Human Services DepartmentNo ratings yet

- 2023 NSE Updates Engage Equivalence Program One PagerDocument1 page2023 NSE Updates Engage Equivalence Program One PagerPedro AlcantaraNo ratings yet

- @@assessment of Medical Documentation As Per Joint Commission InternationDocument6 pages@@assessment of Medical Documentation As Per Joint Commission InternationNahari ArifinNo ratings yet

- Free-Business English - English Marketing and Sales VocabularyDocument3 pagesFree-Business English - English Marketing and Sales VocabularyMF NNo ratings yet

- FWD: Email From IRCTC Transaction ID:2005420171: Ights@irctc - Co.inDocument2 pagesFWD: Email From IRCTC Transaction ID:2005420171: Ights@irctc - Co.inSintu DasNo ratings yet

- Accounting 1Document16 pagesAccounting 1Rommel Angelo AgacitaNo ratings yet

- BISECDocument4 pagesBISECZiauddin AhmedNo ratings yet

- Arista C 360 DatasheetDocument10 pagesArista C 360 DatasheetArjun KharidehalNo ratings yet

- Veeraiyan 02Document10 pagesVeeraiyan 02Unlimited AppsNo ratings yet

- Sta. Ana, Erica Mae SD. 2018006871 Learning Activities No. 1Document12 pagesSta. Ana, Erica Mae SD. 2018006871 Learning Activities No. 1Erica Sta Ana0% (1)

- Production Cycle QuizDocument6 pagesProduction Cycle Quizsky wayNo ratings yet