You might also like

- Tax Rates For Non-Salaried Individuals and AopsDocument4 pagesTax Rates For Non-Salaried Individuals and AopsAdeel QaiserNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Module 1. Transfer TaxesDocument4 pagesModule 1. Transfer TaxesYolly DiazNo ratings yet

- Wishways Assessment - 1 - Business FinanceDocument12 pagesWishways Assessment - 1 - Business Financewishways srinivasNo ratings yet

- Statement 73467376Document3 pagesStatement 73467376Nikita TishchenkoNo ratings yet

- Global Marketing, 6e, Chap03Document19 pagesGlobal Marketing, 6e, Chap03vdchuongNo ratings yet

- IRCTC Retiring RoomDocument2 pagesIRCTC Retiring RoomK KeerthiNo ratings yet

- Epda Mv. Tbn. Paria. Bombana Port. Sul-Tra. Sulawesi. 14 April 2020Document1 pageEpda Mv. Tbn. Paria. Bombana Port. Sul-Tra. Sulawesi. 14 April 2020Agus Shofyan TauryNo ratings yet

- Test 2Document3 pagesTest 2Awais ShahidNo ratings yet

- Test 2 CafDocument3 pagesTest 2 CafBrown BoiNo ratings yet

- Test - 2 PDFDocument6 pagesTest - 2 PDFHåris Khån MøhmånďNo ratings yet

- Tests - CAF 02 Tax Practices Sir Adnan Rauf (SPR24)Document87 pagesTests - CAF 02 Tax Practices Sir Adnan Rauf (SPR24)Umar HasanNo ratings yet

- Section:C-1/B-1 Subject: CAF-06 Teacher: Mr. Sir Adnan Rauf Total Marks: 33 Time Allowed: 55 Mints. Assessment-1 Date: 28oct, 2019Document5 pagesSection:C-1/B-1 Subject: CAF-06 Teacher: Mr. Sir Adnan Rauf Total Marks: 33 Time Allowed: 55 Mints. Assessment-1 Date: 28oct, 2019Shaheer MalikNo ratings yet

- Test 10Document4 pagesTest 10ls786580302No ratings yet

- Test 4Document3 pagesTest 4rehmamali98oNo ratings yet

- Taxation Mid Term Paper Fall 2020Document3 pagesTaxation Mid Term Paper Fall 2020umar khanNo ratings yet

- Principles of Taxation M. Khalid Petiwala: Income Tax Rates, Rebates & DeductionsDocument15 pagesPrinciples of Taxation M. Khalid Petiwala: Income Tax Rates, Rebates & DeductionsosamaNo ratings yet

- DRDDDDocument12 pagesDRDDDWaqar HussainNo ratings yet

- Test 8Document3 pagesTest 8lalshahbaz57No ratings yet

- Assignment 2 Maju LT Spring 2023Document4 pagesAssignment 2 Maju LT Spring 2023Maryam IkhlaqeNo ratings yet

- Test 5Document2 pagesTest 5ls786580302No ratings yet

- Sections:All Subject: CAF-06 Teacher: Sir Adnan/Salman Total Marks: 36 Time Allowed: 1 Hour 10 Minutes Assessment-1 Date: 17 May, 2021Document6 pagesSections:All Subject: CAF-06 Teacher: Sir Adnan/Salman Total Marks: 36 Time Allowed: 1 Hour 10 Minutes Assessment-1 Date: 17 May, 2021BablooNo ratings yet

- Test 6 PDFDocument3 pagesTest 6 PDFHåris Khån MøhmånďNo ratings yet

- f6pkn 2018 Jun QDocument12 pagesf6pkn 2018 Jun QZarnab RazaNo ratings yet

- Tax Slab 2019Document3 pagesTax Slab 2019Ahmed RazaNo ratings yet

- Super Hot Questions BankDocument56 pagesSuper Hot Questions BankClassicaverNo ratings yet

- Test 7Document4 pagesTest 7lalshahbaz57No ratings yet

- CONT .: (15 Minutes Extra Time Will Be Given Due To Slow Internet or Electricity Issues)Document2 pagesCONT .: (15 Minutes Extra Time Will Be Given Due To Slow Internet or Electricity Issues)ALEEM MANSOORNo ratings yet

- Rates of Income TaxDocument9 pagesRates of Income TaxAiza KhanNo ratings yet

- Laws of Taxation-QuizDocument6 pagesLaws of Taxation-QuizkirAn ShAikhNo ratings yet

- Test 5 (QP)Document4 pagesTest 5 (QP)iamneonkingNo ratings yet

- Salary Tax Rates (2022 & 2023 Comparison)Document2 pagesSalary Tax Rates (2022 & 2023 Comparison)by kirmaniNo ratings yet

- Test 9Document4 pagesTest 9lalshahbaz57No ratings yet

- Test 6 (QP)Document4 pagesTest 6 (QP)iamneonkingNo ratings yet

- RTP June 2020 QNDocument14 pagesRTP June 2020 QNbinuNo ratings yet

- Chartered Accountancy Professional Ii (CAP-II) : Education Department The Institute of Chartered Accountants of NepalDocument192 pagesChartered Accountancy Professional Ii (CAP-II) : Education Department The Institute of Chartered Accountants of NepalPrashant Sagar GautamNo ratings yet

- TXPKN 2018 Dec Q PDFDocument17 pagesTXPKN 2018 Dec Q PDFYousuf khanNo ratings yet

- Listcontract1 282019162835 SE Intimation LOF Buyback 353 RepairedDocument67 pagesListcontract1 282019162835 SE Intimation LOF Buyback 353 RepairedSK MUKTAR ALLINo ratings yet

- Deepak QuestionsDocument5 pagesDeepak Questionsvivek ghatbandheNo ratings yet

- Income Tax Card 2019-20: Suite 021, Block B Abu Dhabi Towers, F-11 Markaz Islamabad-PakistanDocument18 pagesIncome Tax Card 2019-20: Suite 021, Block B Abu Dhabi Towers, F-11 Markaz Islamabad-PakistanZain RehmanNo ratings yet

- Test 8 (QP)Document5 pagesTest 8 (QP)iamneonkingNo ratings yet

- BakerTilly Tax Rates CardDocument15 pagesBakerTilly Tax Rates Cardydy9mwfqchNo ratings yet

- Test Series: March, 2021 Mock Test Paper 1 Intermediate (New) Course Paper - 4: Taxation Time Allowed - 3 Hours Maximum Marks - 100 Section - A: Income Tax Law (60 Marks)Document11 pagesTest Series: March, 2021 Mock Test Paper 1 Intermediate (New) Course Paper - 4: Taxation Time Allowed - 3 Hours Maximum Marks - 100 Section - A: Income Tax Law (60 Marks)M100% (1)

- Tax Rates 2021Document6 pagesTax Rates 2021Muazam memonNo ratings yet

- Tax Slabs For Salaried Person For Tax Year 20202021Document2 pagesTax Slabs For Salaried Person For Tax Year 20202021Abid BashirNo ratings yet

- Tax Card 2017 - LatestDocument9 pagesTax Card 2017 - LatestWaqas ShujaNo ratings yet

- Tata Capital Latest 1 PAGER POLICYDocument2 pagesTata Capital Latest 1 PAGER POLICYPRIYANKA DASNo ratings yet

- Income Tax Rates, Rebates & DeductionsDocument35 pagesIncome Tax Rates, Rebates & DeductionsMaryam IkhlaqeNo ratings yet

- Income Tax Slabs For FY 2019Document2 pagesIncome Tax Slabs For FY 2019Kamran KhanNo ratings yet

- Tax Slabs For Salaried Person For Tax Year 2020/2021Document2 pagesTax Slabs For Salaried Person For Tax Year 2020/2021Usama AlmasNo ratings yet

- Composition Scheme For Sarafa and JewellersDocument6 pagesComposition Scheme For Sarafa and JewellersVirender ChaudharyNo ratings yet

- Msme Loan - Upto 2lakhs: NF-546 NF-998 NF-588 NF-855 NF-803 NF-482 NF-373 NF-368Document4 pagesMsme Loan - Upto 2lakhs: NF-546 NF-998 NF-588 NF-855 NF-803 NF-482 NF-373 NF-368Santosh KumarNo ratings yet

- Wipro Letter of Offer For BuybackDocument64 pagesWipro Letter of Offer For Buybacksen chandanNo ratings yet

- Portal Investment Proof Verification Guidelines 2022 23Document11 pagesPortal Investment Proof Verification Guidelines 2022 23yfiamataimNo ratings yet

- ISCO Tax Card TY 2017 PDFDocument15 pagesISCO Tax Card TY 2017 PDFRehan FarhatNo ratings yet

- Question Test Paper 2 - NOV 2023Document2 pagesQuestion Test Paper 2 - NOV 2023ABCXYZNo ratings yet

- Revision Test Paper: Cap Ii (June 2017)Document12 pagesRevision Test Paper: Cap Ii (June 2017)binuNo ratings yet

- Revision - Test - Paper - CAP - II - June - 2017 9Document181 pagesRevision - Test - Paper - CAP - II - June - 2017 9Dipen AdhikariNo ratings yet

- CA INTER Paper 5 Expected Questions May 2022Document138 pagesCA INTER Paper 5 Expected Questions May 2022gimNo ratings yet

- Case: Roger: (Reference Date: 1st April, 2019)Document6 pagesCase: Roger: (Reference Date: 1st April, 2019)Krish BhutaNo ratings yet

- Suggested Solutions TPExfpPDocument6 pagesSuggested Solutions TPExfpPtarangtgNo ratings yet

- GST Ca Interg9 QuestionDocument6 pagesGST Ca Interg9 QuestionVishal Kumar 5504No ratings yet

- Bba Sem-6 AssignmentDocument9 pagesBba Sem-6 Assignmentshyam visanaNo ratings yet

- Tax On Mutual Funds and SharesDocument6 pagesTax On Mutual Funds and SharesGiri SukumarNo ratings yet

- 0456Document4 pages0456Usman Shaukat Khan100% (1)

- Q&A, November 2023Document9 pagesQ&A, November 2023Cerealis FelicianNo ratings yet

- AE 5 Midterm TopicDocument9 pagesAE 5 Midterm TopicMary Ann GurreaNo ratings yet

- SezDocument34 pagesSezanuragNo ratings yet

- D) Igst: D) Supply of Services Whether The Job Work Is Carried Out With or WithoutDocument20 pagesD) Igst: D) Supply of Services Whether The Job Work Is Carried Out With or Withoutparesh shiralNo ratings yet

- புதிய மின் கட்டணம் 2022Document4 pagesபுதிய மின் கட்டணம் 2022arumugamks7628100% (1)

- Solution Manual For International Economics 15th Edition DownloadDocument3 pagesSolution Manual For International Economics 15th Edition DownloadJoshuaLunasago100% (37)

- HT2333I004659173Document5 pagesHT2333I004659173Tkdevarajan DevaNo ratings yet

- Account Key and AccuralDocument2 pagesAccount Key and AccuralPRATAP SAPMMNo ratings yet

- qCh.3 Topic 2-Taxes (Direct and Indirect)Document7 pagesqCh.3 Topic 2-Taxes (Direct and Indirect)Joshua MaNo ratings yet

- Amazon - in - Order 403-6742556-2759527Document1 pageAmazon - in - Order 403-6742556-2759527Bapi FlexNo ratings yet

- TAX QUIZ 1 ReviewerDocument8 pagesTAX QUIZ 1 ReviewerArrianne ObiasNo ratings yet

- Income Tax PPT 4Document19 pagesIncome Tax PPT 4RachnaNo ratings yet

- 6.protectionism Vs LiberalisationDocument4 pages6.protectionism Vs LiberalisationSilas SargunamNo ratings yet

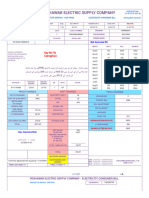

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply Complaintsvinay seemuNo ratings yet

- Ch.8 International Trade PolicyDocument42 pagesCh.8 International Trade PolicyDina SamirNo ratings yet

- #A#c#0#47m - 639034022092104544 - Itns280 - 22092021 - Aveva Information Technology India Private LimitedDocument1 page#A#c#0#47m - 639034022092104544 - Itns280 - 22092021 - Aveva Information Technology India Private LimitedVinayak DhotreNo ratings yet

- A Practical Guide To Increasing Mining Local Procurement in West AfricaDocument88 pagesA Practical Guide To Increasing Mining Local Procurement in West AfricaPRAMONO JATI PNo ratings yet

- Historical Development of of Taxation Principles and Law in KenyaDocument17 pagesHistorical Development of of Taxation Principles and Law in KenyaJustus AmitoNo ratings yet

- Pesco Online BillDocument2 pagesPesco Online BillMuhammad ShoaibNo ratings yet

- Transfer Pricing - F5 Performance Management - ACCA Qualification - Students - ACCA GlobalDocument13 pagesTransfer Pricing - F5 Performance Management - ACCA Qualification - Students - ACCA GlobalAshura ShaibNo ratings yet

- LT BILL 46429091009 Dec22Document2 pagesLT BILL 46429091009 Dec22Deepak JhaNo ratings yet

- Issue Date: Rating Area Locality Due Date YearDocument2 pagesIssue Date: Rating Area Locality Due Date YearSAWERA TEXTILES PVT LTDNo ratings yet

- Irctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Document1 pageIrctcs E-Ticketing Service Electronic Reservation Slip (Personal User)ved pNo ratings yet

- CIR vs. Sony 178697Document1 pageCIR vs. Sony 178697magenNo ratings yet

- Distribution System Loss Caps: Draft RulesDocument40 pagesDistribution System Loss Caps: Draft RulesFranz Xyrlo Ibarra TobiasNo ratings yet