You might also like

- AEG1004 Spycraft 1e - Shadowforce Archer - The ShopDocument129 pagesAEG1004 Spycraft 1e - Shadowforce Archer - The Shopbyeorama100% (2)

- UTA v. KassanDocument13 pagesUTA v. KassanTHR100% (1)

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionFrom EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionRating: 5 out of 5 stars5/5 (1)

- Solution Manual For Financial and Managerial Accounting 8th by WildDocument45 pagesSolution Manual For Financial and Managerial Accounting 8th by WildTiffanyFowlercftzi100% (48)

- Chapter 2 Review Sheet AnswersDocument7 pagesChapter 2 Review Sheet AnswersKenneth DayohNo ratings yet

- The Genius Princes Guide To Raising A Nation Out of Debt (Hey, How About Treason) Vol 1Document214 pagesThe Genius Princes Guide To Raising A Nation Out of Debt (Hey, How About Treason) Vol 1Gusti Ahmad Faiz100% (8)

- Pivot Point Indicator: Cheat SheetDocument4 pagesPivot Point Indicator: Cheat SheetOlalekan Akinola100% (1)

- Journalizing, Posting and Trial Balance: For Non-WiredDocument8 pagesJournalizing, Posting and Trial Balance: For Non-WiredCj ArquisolaNo ratings yet

- QuickBooks Online for Beginners: A Quick Reference and Step-by-Step Guide to Mastering QuickBooks Online for Small Business Owners from Beginners to ExpertFrom EverandQuickBooks Online for Beginners: A Quick Reference and Step-by-Step Guide to Mastering QuickBooks Online for Small Business Owners from Beginners to ExpertNo ratings yet

- Solution Manual For Financial Accounting 9th Edition by WeygandtDocument22 pagesSolution Manual For Financial Accounting 9th Edition by Weygandta540142314100% (3)

- Additional Problem Chap 3 SolutionDocument10 pagesAdditional Problem Chap 3 Solutionprincetonu67% (3)

- Chapter 08Document26 pagesChapter 08Dan ChuaNo ratings yet

- Artificial Intelligence Cyberattack and Nuclear Weapons A Dangerous CombinationDocument7 pagesArtificial Intelligence Cyberattack and Nuclear Weapons A Dangerous CombinationgreycompanionNo ratings yet

- Sant BhindranwaleDocument28 pagesSant BhindranwaleHarpreet Singh88% (16)

- CEO or GENERAL MANAGER or MANAGING DIRECTOR or COUNTRY MANAGERDocument3 pagesCEO or GENERAL MANAGER or MANAGING DIRECTOR or COUNTRY MANAGERapi-79146273100% (1)

- CH 2 ExercisesDocument4 pagesCH 2 ExercisesAnonymous Jf9PYY2E80% (1)

- Bhagavad GitaDocument82 pagesBhagavad Gitasonalpatil09No ratings yet

- Trusted ScholarsDocument46 pagesTrusted ScholarsNabeelNo ratings yet

- Case StudyDocument21 pagesCase StudyHuda Siddiqua70% (10)

- CH 02Document20 pagesCH 02duy blaNo ratings yet

- Solutions To Brief Exercises - Chapter 12Document12 pagesSolutions To Brief Exercises - Chapter 12Anh KietNo ratings yet

- Kunci Jawaban Ak Peng 1Document64 pagesKunci Jawaban Ak Peng 1Golddia JegesNo ratings yet

- Processing Accounting Information: QuestionsDocument57 pagesProcessing Accounting Information: QuestionsYousifNo ratings yet

- Ch02-Solutions To Brief ExercisesDocument5 pagesCh02-Solutions To Brief ExercisesAmanda_CChenNo ratings yet

- Solution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 6Th Edition by Harrison Isbn 0134141091 978013414109 Full Chapter PDFcarmen.hall969100% (11)

- Solution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFDocument36 pagesSolution Manual For Financial Accounting Canadian 5Th Edition by Harrison Isbn 0132979276 9780132979276 Full Chapter PDFcarmen.hall969100% (12)

- Dbb1202 - Financial AccountingDocument5 pagesDbb1202 - Financial AccountingVansh JainNo ratings yet

- ACCT1100 PA1 AssignmentSolutionManual 1Document6 pagesACCT1100 PA1 AssignmentSolutionManual 1Chi IuvianamoNo ratings yet

- Financial Accounting in An Economic Context 8Th Edition Pratt Solutions Manual Full Chapter PDFDocument48 pagesFinancial Accounting in An Economic Context 8Th Edition Pratt Solutions Manual Full Chapter PDFthomasowens1asz100% (9)

- Extra Applications - Lecture Week 3Document7 pagesExtra Applications - Lecture Week 3Muhammad HusseinNo ratings yet

- Assignment-1 (Eco & Actg For Engineers) Exercise - 1Document4 pagesAssignment-1 (Eco & Actg For Engineers) Exercise - 1Nayeem HossainNo ratings yet

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverNo ratings yet

- Accounting Applications - Part 4 - Lecture 2Document7 pagesAccounting Applications - Part 4 - Lecture 2Ahmed Mostafa ElmowafyNo ratings yet

- Adjusting Accounts and Preparing Financial StatementsDocument54 pagesAdjusting Accounts and Preparing Financial StatementsAmna TahirNo ratings yet

- AccountingDocument5 pagesAccountingAndrea Joy PekNo ratings yet

- Cash Budgeting Notes and QuestionsDocument39 pagesCash Budgeting Notes and Questions邹尧No ratings yet

- MGMT 026 Chapter 04 PracticeDocument5 pagesMGMT 026 Chapter 04 Practiceazizkhan256356No ratings yet

- Accounting Exercises AnswersDocument3 pagesAccounting Exercises AnswersGaia BautistaNo ratings yet

- Exam Revision - Chapter 3 4Document6 pagesExam Revision - Chapter 3 4Vũ Thị NgoanNo ratings yet

- Chapter 2 SolutionsDocument15 pagesChapter 2 SolutionsKashif IshaqNo ratings yet

- Brief Exercises PDFDocument6 pagesBrief Exercises PDFRamzan AliNo ratings yet

- Acc 1 QuizDocument7 pagesAcc 1 QuizAyat MukahalNo ratings yet

- Accounting Assignment 04A 207Document10 pagesAccounting Assignment 04A 207Aniyah's RanticsNo ratings yet

- TUGAS DASAR AKUNTANSI 4 - Samuel S Purba - 141200193Document24 pagesTUGAS DASAR AKUNTANSI 4 - Samuel S Purba - 141200193Samuel PurbaNo ratings yet

- Session 3 Part 2 Income Statement 2024-04-27 04-33-12Document4 pagesSession 3 Part 2 Income Statement 2024-04-27 04-33-12sarahzaki011No ratings yet

- Recording Business TransactionsDocument36 pagesRecording Business Transactionsnorman.washington378100% (10)

- Extra Applications - Lecture Week 3Document6 pagesExtra Applications - Lecture Week 3soliman salmanNo ratings yet

- Chapter 2 - The Recording Process Practice SolutionsDocument13 pagesChapter 2 - The Recording Process Practice SolutionsNguyễn Minh ĐứcNo ratings yet

- Exam Revision - 3 & 4 SolDocument6 pagesExam Revision - 3 & 4 SolNguyễn Minh ĐứcNo ratings yet

- 157 28395 EY111 2013 4 2 1 Chap003Document74 pages157 28395 EY111 2013 4 2 1 Chap003JasonNo ratings yet

- Adjusting Accounts and Preparing Financial Statements: QuestionsDocument74 pagesAdjusting Accounts and Preparing Financial Statements: QuestionsChaituNo ratings yet

- Problem Sheet 4 Summer 22Document4 pagesProblem Sheet 4 Summer 22Md Tanvir AhmedNo ratings yet

- CH 3Document10 pagesCH 3Mohammed mostafaNo ratings yet

- Arab Final 90% Fall2021 (YS)Document8 pagesArab Final 90% Fall2021 (YS)ahmed abuzedNo ratings yet

- Unit 4Document33 pagesUnit 4b21ai008No ratings yet

- Tugas Kelompok Ke-1 Week 3/ Sesi 4: EssayDocument5 pagesTugas Kelompok Ke-1 Week 3/ Sesi 4: Essayadelia zahraNo ratings yet

- Accounts Home Test 2Document7 pagesAccounts Home Test 2Ashish RaiNo ratings yet

- Accounting Concepts and PrinciplesDocument30 pagesAccounting Concepts and PrinciplesKristine Lei Del MundoNo ratings yet

- Working Paper-Chapters 1-4 Naser AbdelkarimDocument5 pagesWorking Paper-Chapters 1-4 Naser AbdelkarimHasan NajiNo ratings yet

- CH 4 Exercises ADocument5 pagesCH 4 Exercises AAhmed Abdel-FattahNo ratings yet

- Work Sheet On Financial AccountingDocument3 pagesWork Sheet On Financial AccountingFantayNo ratings yet

- FOA ExamDocument3 pagesFOA ExamyeshaNo ratings yet

- Solution Manual For Horngrens Financial and Managerial Accounting The Financial Chapters 4Th Edition Nobles Mattison Matsumura 970133255577 0133255573 Full Chapter PDFDocument36 pagesSolution Manual For Horngrens Financial and Managerial Accounting The Financial Chapters 4Th Edition Nobles Mattison Matsumura 970133255577 0133255573 Full Chapter PDFnorman.washington378100% (11)

- Financial Accounting 9Th Edition Harrison Solutions Manual Full Chapter PDFDocument36 pagesFinancial Accounting 9Th Edition Harrison Solutions Manual Full Chapter PDFphyllis.horan125100% (10)

- qUIZ - FS TO PCTBDocument5 pagesqUIZ - FS TO PCTBGalang, Princess T.No ratings yet

- FoA I CH Two...Document31 pagesFoA I CH Two...Ela Man ĤămměŕşNo ratings yet

- Questions For Practice - BDocument11 pagesQuestions For Practice - BrsaldreesNo ratings yet

- Answer MahaDocument6 pagesAnswer Mahamohamadalsaygh232No ratings yet

- Chapter 4 - Complete The Accounting Cycle Practice Set A SolutionsDocument17 pagesChapter 4 - Complete The Accounting Cycle Practice Set A SolutionsNguyễn Minh ĐứcNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- ForecastingDocument9 pagesForecastingQuỳnh'ss Đắc'ssNo ratings yet

- Trial BalanceDocument1 pageTrial BalanceQuỳnh'ss Đắc'ssNo ratings yet

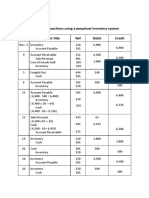

- Group 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditDocument6 pagesGroup 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditQuỳnh'ss Đắc'ssNo ratings yet

- Work in Group of 3Document1 pageWork in Group of 3Quỳnh'ss Đắc'ssNo ratings yet

- Exercise Ch5Document1 pageExercise Ch5Quỳnh'ss Đắc'ssNo ratings yet

- Couple Threatened by SRP-WithPhotosDocument5 pagesCouple Threatened by SRP-WithPhotosDLB777100% (1)

- 2059 w07 QP 02Document8 pages2059 w07 QP 02mstudy123456No ratings yet

- Prepositions PaysDocument4 pagesPrepositions PaysBulut MümünNo ratings yet

- Hindu Religious Mark On The Forehead 07-Nun WearsDocument2 pagesHindu Religious Mark On The Forehead 07-Nun WearsFrancis LoboNo ratings yet

- Non-Finite Forms of The VerbDocument25 pagesNon-Finite Forms of The VerbCésar TapiaNo ratings yet

- ProposalDocument5 pagesProposalDeepika KandiNo ratings yet

- Toyota Yaris 2013 12 Workshop Service ManualDocument22 pagesToyota Yaris 2013 12 Workshop Service Manualcourtneythomas261194yei100% (110)

- Script For "Is University Worth It?"Document2 pagesScript For "Is University Worth It?"Simran KabotraNo ratings yet

- EDCART - by DarwinDocument42 pagesEDCART - by DarwinDarWin MarCeloNo ratings yet

- Trends Lecture Notes Q2Document10 pagesTrends Lecture Notes Q2Pagaduan R-mie JaneNo ratings yet

- IBPS QuestionsDocument32 pagesIBPS QuestionsAmal PrakashNo ratings yet

- CRI - Solved Valuation Practical Sums - CS Vaibhav Chitlangia - Yes Academy, PuneDocument37 pagesCRI - Solved Valuation Practical Sums - CS Vaibhav Chitlangia - Yes Academy, Punegopika mundraNo ratings yet

- 10 Reasons Why You Should Do HomeworkDocument8 pages10 Reasons Why You Should Do Homeworkagbhqfuif100% (1)

- Ebook - Financial Statements of Not-for-Profit OrganizationsDocument38 pagesEbook - Financial Statements of Not-for-Profit OrganizationsRahulNo ratings yet

- DFA1101GZ5AD6J 907 Operational Manual 200606 - EnglishDocument0 pagesDFA1101GZ5AD6J 907 Operational Manual 200606 - EnglishSelmirije2No ratings yet

- Credit EDA Case Study Problem StatementDocument4 pagesCredit EDA Case Study Problem StatementPlaydo kidsNo ratings yet

- Glut of PaperDocument4 pagesGlut of PaperBryan OrtegaNo ratings yet

- Eight-Step Strategic Plan - FJVDocument17 pagesEight-Step Strategic Plan - FJVapi-487889494No ratings yet

- A Critical Analysis of Civil Disobedience An Essay by Henry David ThoreauDocument2 pagesA Critical Analysis of Civil Disobedience An Essay by Henry David Thoreaulavanya sivakumarNo ratings yet

- W P No 188722011Document71 pagesW P No 188722011RAMESH KNo ratings yet