You might also like

- Axia Corporation FY21 Earnings UpdateDocument3 pagesAxia Corporation FY21 Earnings UpdateMalcolm ChitenderuNo ratings yet

- AKD Federal Budget FY24 Jun 10 2023Document21 pagesAKD Federal Budget FY24 Jun 10 2023Asra IsarNo ratings yet

- FY22: Operating Leverage A Highlight: Nextdc (NXT)Document3 pagesFY22: Operating Leverage A Highlight: Nextdc (NXT)Muhammad ImranNo ratings yet

- Earnings Update ZENITHBANK 2022FYDocument6 pagesEarnings Update ZENITHBANK 2022FYShehu MusaNo ratings yet

- U/W: Investing To Fortify BTM Growth: Polynovo (PNV)Document7 pagesU/W: Investing To Fortify BTM Growth: Polynovo (PNV)Muhammad ImranNo ratings yet

- Earnings Update DANGCEM 2021FY 1Document6 pagesEarnings Update DANGCEM 2021FY 1kazeemsheriff8No ratings yet

- Ahluwalia Contracts: Strong Results Superior Fundamentals - Maintain BUYDocument6 pagesAhluwalia Contracts: Strong Results Superior Fundamentals - Maintain BUY14Myra HUNDIANo ratings yet

- Larsen & Toubro: Bottoming Out Order Pick-Up Awaited BUYDocument10 pagesLarsen & Toubro: Bottoming Out Order Pick-Up Awaited BUYVikas AggarwalNo ratings yet

- Rul Mamoelis Update 181122Document6 pagesRul Mamoelis Update 181122jonathan gohNo ratings yet

- Finance Briefings RamsayDocument35 pagesFinance Briefings RamsayRichard OonNo ratings yet

- Confluent Inc. (CFLT) - Cloud Momentum Continues As Growth Accelerates - 3Q21 ResultsDocument9 pagesConfluent Inc. (CFLT) - Cloud Momentum Continues As Growth Accelerates - 3Q21 ResultsShingYiuNo ratings yet

- O/W: Seeding More Growth in The Franchise Network: Silk Laser Australia (SLA)Document8 pagesO/W: Seeding More Growth in The Franchise Network: Silk Laser Australia (SLA)Muhammad ImranNo ratings yet

- Emlak Konut REIC: Price Target RevisionDocument6 pagesEmlak Konut REIC: Price Target RevisionCbpNo ratings yet

- Dixon Technologies Q1FY22 Result UpdateDocument8 pagesDixon Technologies Q1FY22 Result UpdateAmos RiveraNo ratings yet

- (Kotak) Zee Entertainment Enterprises, May 30, 2022Document11 pages(Kotak) Zee Entertainment Enterprises, May 30, 2022darshanmaldeNo ratings yet

- Seed Co International Limited FY23 Earnings UpdateDocument3 pagesSeed Co International Limited FY23 Earnings UpdatetawandaNo ratings yet

- Yes Securities (Q1 Fy22)Document10 pagesYes Securities (Q1 Fy22)harshbhutra1234No ratings yet

- Eco World Dev. Group Outperform : Buoyed by Industrial Land SaleDocument5 pagesEco World Dev. Group Outperform : Buoyed by Industrial Land Salehl lowNo ratings yet

- Simbisa Brands FY21 Earnings UpdateDocument3 pagesSimbisa Brands FY21 Earnings UpdateMalcolm ChitenderuNo ratings yet

- Phillip Capital Sees NO UPSIDE in HDFC AMC Strong Operating PerformanceDocument6 pagesPhillip Capital Sees NO UPSIDE in HDFC AMC Strong Operating Performanceharmanmultani786No ratings yet

- Cyient 28 11 2022 AnandDocument13 pagesCyient 28 11 2022 AnandParth DongaNo ratings yet

- RecDocument28 pagesRecChirag ShahNo ratings yet

- 1Q21 Operating EBITDA Below COL Estimates On Lower-Than-Expected RevenuesDocument8 pages1Q21 Operating EBITDA Below COL Estimates On Lower-Than-Expected RevenuesJajahinaNo ratings yet

- 141342112021251larsen Toubro Limited - 20210129Document5 pages141342112021251larsen Toubro Limited - 20210129Michelle CastelinoNo ratings yet

- Trent LTD - Q1FY22 - Edited - 11-08-2021 - 10Document7 pagesTrent LTD - Q1FY22 - Edited - 11-08-2021 - 10hackmaverickNo ratings yet

- Infosys 140422 MotiDocument10 pagesInfosys 140422 MotiGrace StylesNo ratings yet

- Q3 and Nine Months Period Ended 31 Dec 2020 Results PresentationDocument18 pagesQ3 and Nine Months Period Ended 31 Dec 2020 Results PresentationdarmawansusiloNo ratings yet

- 4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedDocument5 pages4716156162022739schneider Electric Infrastructure Ltd. Q4FY22 - SignedbradburywillsNo ratings yet

- Oppenheimer RUN RUN Growth Continues With Strong DemandDocument10 pagesOppenheimer RUN RUN Growth Continues With Strong DemandBrian AhuatziNo ratings yet

- Serba Dinamik Holdings Under Review: Another Results DisappointmentDocument4 pagesSerba Dinamik Holdings Under Review: Another Results DisappointmentZhi_Ming_Cheah_8136No ratings yet

- 2023 q2 Earnings Results PresentationDocument15 pages2023 q2 Earnings Results PresentationZerohedgeNo ratings yet

- Novelis Q1FY22 Earnings PresentationDocument21 pagesNovelis Q1FY22 Earnings PresentationLourdu XavierNo ratings yet

- Meta Reports Fourth Quarter and Full Year 2022 Results 2023Document12 pagesMeta Reports Fourth Quarter and Full Year 2022 Results 2023Fady EhabNo ratings yet

- Q3 - 2023 - Investor PresentationDocument37 pagesQ3 - 2023 - Investor PresentationMo LaNo ratings yet

- Lumax Inds - Q3FY22 Result Update - 15022022 - 15-02-2022 - 14Document7 pagesLumax Inds - Q3FY22 Result Update - 15022022 - 15-02-2022 - 14Mridul Kumar BanerjeeNo ratings yet

- Bajaj Electricals - HaitongDocument12 pagesBajaj Electricals - HaitongGurjeevNo ratings yet

- MGT7103 Group 4 - Maxis - Presentation 2Document69 pagesMGT7103 Group 4 - Maxis - Presentation 2hpone.mbaNo ratings yet

- SBI Cards Q1FY21 PAT up 14%YoY on strong NII, lower provisionsDocument8 pagesSBI Cards Q1FY21 PAT up 14%YoY on strong NII, lower provisionswhitenagarNo ratings yet

- PSP Projects LTD - Q1FY24 Result Update - 28072023 - 28-07-2023 - 10Document8 pagesPSP Projects LTD - Q1FY24 Result Update - 28072023 - 28-07-2023 - 10samraatjadhavNo ratings yet

- Renewable Volume ObligationDocument9 pagesRenewable Volume ObligationHieu NgoNo ratings yet

- Zacks Small-Cap Research: Corecivic, IncDocument8 pagesZacks Small-Cap Research: Corecivic, IncKarim LahrichiNo ratings yet

- CNVRG Performance PlummetsDocument7 pagesCNVRG Performance PlummetsignaciomannyNo ratings yet

- Latest Ceat ReportDocument6 pagesLatest Ceat Reportshubhamkumar.bhagat.23mbNo ratings yet

- Mirae Asset Sekuritas Indonesia Indocement Tunggal PrakarsaDocument7 pagesMirae Asset Sekuritas Indonesia Indocement Tunggal PrakarsaekaNo ratings yet

- Airtel Africa PLC - Results For Half Year Ended 30 September 2023Document56 pagesAirtel Africa PLC - Results For Half Year Ended 30 September 2023Anonymous FnM14a0No ratings yet

- Stocks in Focus: DNL Earnings Improve in 3Q20 Ahead of EstimatesDocument12 pagesStocks in Focus: DNL Earnings Improve in 3Q20 Ahead of EstimatesJNo ratings yet

- Accumulate: Growth Momentum Continues!Document7 pagesAccumulate: Growth Momentum Continues!sj singhNo ratings yet

- Axis Securities Sees 2% DOWNSIDE in Bajaj Auto Another Robust QuarterDocument8 pagesAxis Securities Sees 2% DOWNSIDE in Bajaj Auto Another Robust QuarterDhaval MailNo ratings yet

- 3q23 Media Release en (1)Document15 pages3q23 Media Release en (1)Ashutos MohantyNo ratings yet

- SCMA - The Worst Might Be OverDocument5 pagesSCMA - The Worst Might Be OverBrilliant Indra KNo ratings yet

- RIL 2Q PresentationDocument56 pagesRIL 2Q PresentationElaineNo ratings yet

- Q2 FY24 Investor Presentation FINALDocument45 pagesQ2 FY24 Investor Presentation FINALDMT IPONo ratings yet

- Q32022 Shareholder LetterDocument25 pagesQ32022 Shareholder Lettertichips mobileNo ratings yet

- Q4 FY23 Performance ReviewDocument49 pagesQ4 FY23 Performance ReviewDennis AngNo ratings yet

- 1QFY23Document35 pages1QFY23Rajendra AvinashNo ratings yet

- KNR Constructions PDFDocument6 pagesKNR Constructions PDFAniket DhanukaNo ratings yet

- Wlcon - PS Wlcon PMDocument10 pagesWlcon - PS Wlcon PMP RosenbergNo ratings yet

- Infosys (INFO IN) : Q1FY21 Result UpdateDocument14 pagesInfosys (INFO IN) : Q1FY21 Result UpdatewhitenagarNo ratings yet

- JP Morgan LGF-A Warner Bros Discovery Inc - Encouraged by Stabilizing TreDocument13 pagesJP Morgan LGF-A Warner Bros Discovery Inc - Encouraged by Stabilizing TreraymanNo ratings yet

- World Bank East Asia and Pacific Economic Update, Spring 2022: Risks and OpportunitiesFrom EverandWorld Bank East Asia and Pacific Economic Update, Spring 2022: Risks and OpportunitiesNo ratings yet

- 0460_s22_i2_21Document2 pages0460_s22_i2_21tawandaNo ratings yet

- S303I.sarmaDocument15 pagesS303I.sarmaapersonjust47No ratings yet

- jbms-9-2-3Document11 pagesjbms-9-2-3tawandaNo ratings yet

- Economics Assignment 1 Final DraftDocument10 pagesEconomics Assignment 1 Final DrafttawandaNo ratings yet

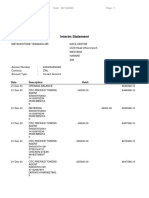

- Interim Statement: Date: 29/12/2023Document2 pagesInterim Statement: Date: 29/12/2023tawandaNo ratings yet

- ANNIE PHIRI Log BookDocument3 pagesANNIE PHIRI Log BooktawandaNo ratings yet

- BankingDocument3 pagesBankingtawandaNo ratings yet

- 0460_s22_i2_23Document2 pages0460_s22_i2_23tawandaNo ratings yet

- Praise and Worship List1Document3 pagesPraise and Worship List1tawandaNo ratings yet

- Report 1698833017896Document1 pageReport 1698833017896tawandaNo ratings yet

- Marketing Assignment 2 WordDocument6 pagesMarketing Assignment 2 WordtawandaNo ratings yet

- Why Corporate Boards Fail Due to Lack of Oversight and Monitoring (25Document1 pageWhy Corporate Boards Fail Due to Lack of Oversight and Monitoring (25tawandaNo ratings yet

- AFRISUN14Document178 pagesAFRISUN14tawandaNo ratings yet

- Measures To Restore ConfidenceDocument7 pagesMeasures To Restore ConfidencetawandaNo ratings yet

- Intermediate MacroeconomicsDocument6 pagesIntermediate MacroeconomicstawandaNo ratings yet

- International FinanceDocument6 pagesInternational FinancetawandaNo ratings yet

- AFDIS14Document52 pagesAFDIS14tawandaNo ratings yet

- Corporate Governance Government MeasuresDocument9 pagesCorporate Governance Government MeasurestawandaNo ratings yet

- Chapter 2Document15 pagesChapter 2tawandaNo ratings yet

- Corporate Governance - Non Executive DirectorsDocument7 pagesCorporate Governance - Non Executive DirectorstawandaNo ratings yet

- Course Outline BLPDocument2 pagesCourse Outline BLPtawandaNo ratings yet

- Assignment 5Document5 pagesAssignment 5tawandaNo ratings yet

- Why Some Corporate Boards Fail: Lack of Oversight and ProbityDocument9 pagesWhy Some Corporate Boards Fail: Lack of Oversight and ProbitytawandaNo ratings yet

- Individual Written AssignmentDocument2 pagesIndividual Written AssignmenttawandaNo ratings yet

- Chapter 1 Lupane State UniversityDocument8 pagesChapter 1 Lupane State UniversitytawandaNo ratings yet

- XYZ Limited ratio analysis and interest rate determinantsDocument4 pagesXYZ Limited ratio analysis and interest rate determinantstawandaNo ratings yet

- Corporate Finance 1B Study Pack CUZDocument169 pagesCorporate Finance 1B Study Pack CUZtawandaNo ratings yet

- Assignment 2 BACC205 - 2022Document3 pagesAssignment 2 BACC205 - 2022tawandaNo ratings yet

- Assignment 1Document6 pagesAssignment 1tawanda100% (2)

- Corporate FinanceDocument3 pagesCorporate FinancetawandaNo ratings yet

- Organic Food ChinaDocument36 pagesOrganic Food ChinaSoumyabuddha DebnathNo ratings yet

- Secretary's Certificate (AUB)Document1 pageSecretary's Certificate (AUB)Gerard Nelson ManaloNo ratings yet

- Google Search Based Sentiment Indexes - 2020 - IIMB Management ReviewDocument11 pagesGoogle Search Based Sentiment Indexes - 2020 - IIMB Management ReviewYG DENo ratings yet

- Nestlé's Use of Internet and Software SolutionsDocument3 pagesNestlé's Use of Internet and Software SolutionsAleena AmirNo ratings yet

- 04.may 2022Document138 pages04.may 2022Dream creatorsNo ratings yet

- HSC CTD Apr 6th, 2023Document17 pagesHSC CTD Apr 6th, 2023Đức Anh NguyễnNo ratings yet

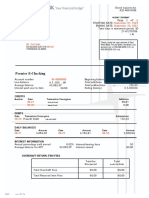

- East West Bank StatementDocument1 pageEast West Bank StatementHalon GlenNo ratings yet

- Chapter 1 Economic Growth and DevelopmentDocument14 pagesChapter 1 Economic Growth and DevelopmentHyuna KimNo ratings yet

- STEP 1: Setting Up Your UCC Contract Trust Account: (FIRST Package To Treasury)Document2 pagesSTEP 1: Setting Up Your UCC Contract Trust Account: (FIRST Package To Treasury)Jahe El97% (58)

- Case 1 Phuket Beach HotelDocument7 pagesCase 1 Phuket Beach HotelYana Dela CernaNo ratings yet

- IndustrialDocument18 pagesIndustrialKarthickrajaNo ratings yet

- Building A Network To Share and Discuss: Dialogue On TaxDocument156 pagesBuilding A Network To Share and Discuss: Dialogue On TaxcadrjainNo ratings yet

- ACREV 426 - AP 02 ReceivablesDocument5 pagesACREV 426 - AP 02 ReceivablesEve Jennie Rose MagnificoNo ratings yet

- Salary Slip NewDocument1 pageSalary Slip Newfakiv83032No ratings yet

- Chapter-5-Accounting for Partnerships in EthiopiaDocument17 pagesChapter-5-Accounting for Partnerships in EthiopiaYasinNo ratings yet

- Multiple Choice Questions On TreasuryDocument8 pagesMultiple Choice Questions On Treasuryparthasarathi_in100% (1)

- Competitive EnvironmentDocument19 pagesCompetitive EnvironmentMd. Musfiqur RahmanNo ratings yet

- Comparative Advantage Time ProductionDocument1 pageComparative Advantage Time ProductionPhung NhaNo ratings yet

- (Q1) Conceptual Analysis: AntunesDocument4 pages(Q1) Conceptual Analysis: AntuneskucaantunesNo ratings yet

- SFM FT M-2 PDFDocument31 pagesSFM FT M-2 PDFveenamadhurimeduriNo ratings yet

- Strategic Plan 2021/22-2026: Ethiopian Skylight HotelDocument47 pagesStrategic Plan 2021/22-2026: Ethiopian Skylight HotelLamesginew Mersha100% (4)

- Policy recommendations to mitigate COVID-19 supply shocks for Indian MSMEsDocument8 pagesPolicy recommendations to mitigate COVID-19 supply shocks for Indian MSMEsHashmita MistriNo ratings yet

- Reorder PointDocument2 pagesReorder Pointpankaj1230No ratings yet

- IAS 7 - Statement of Cash FlowsDocument4 pagesIAS 7 - Statement of Cash FlowsSky WalkerNo ratings yet

- SCM Coordination and ContractsDocument64 pagesSCM Coordination and ContractsdurgaNo ratings yet

- Globalization and EducationDocument7 pagesGlobalization and Educationbambi rose espanola50% (2)

- Eaton Brass Products Master CatalogDocument168 pagesEaton Brass Products Master CatalogankitNo ratings yet

- Strictly no erasures allowedDocument12 pagesStrictly no erasures allowedErwin Labayog MedinaNo ratings yet

- Astro Electronics Corp. v. Phil. Export (Digest)Document2 pagesAstro Electronics Corp. v. Phil. Export (Digest)Dany Abuel100% (1)

- Chapter - 1: A Study On Inventory Management at Precot Meridian LTD HindupurDocument76 pagesChapter - 1: A Study On Inventory Management at Precot Meridian LTD HindupurSudeep SNo ratings yet