You might also like

- Pay Slip 1Document4 pagesPay Slip 1api-3810267No ratings yet

- Order1522814 Ultra ConstructionDocument2 pagesOrder1522814 Ultra Constructionmeuh54uhNo ratings yet

- 153 Exemption Certificate 01 JUL 23 To 31 DEC 23Document2 pages153 Exemption Certificate 01 JUL 23 To 31 DEC 23athar brotherNo ratings yet

- Order 2971112Document2 pagesOrder 2971112Zeeshan KhanNo ratings yet

- Exemption Certificate of Ghandhara Industries 2021Document2 pagesExemption Certificate of Ghandhara Industries 2021Waqar RaoNo ratings yet

- 3rd Floor, Suleman Center, SC-5, (ST-17) Sector-15, Near Brooks Roundabout, KIA,, Karachi East Rasul Flour Mills (Private) LimitedDocument2 pages3rd Floor, Suleman Center, SC-5, (ST-17) Sector-15, Near Brooks Roundabout, KIA,, Karachi East Rasul Flour Mills (Private) LimitedMuhammad HamzaNo ratings yet

- Exemption Certificate Us 159 (1) 153Document2 pagesExemption Certificate Us 159 (1) 153ijazaslam.huaweiNo ratings yet

- Exemption Certificate - SalesDocument2 pagesExemption Certificate - SalesExecutive F&ADADUNo ratings yet

- Exemption 153 TY2021Document1 pageExemption 153 TY2021Usama AjazNo ratings yet

- Exemption Poly Pac Valid Up To 31.12.2020 (2) - 1Document1 pageExemption Poly Pac Valid Up To 31.12.2020 (2) - 1khawarNo ratings yet

- Order WHT Exempt, July To Dec 2022Document2 pagesOrder WHT Exempt, July To Dec 2022Roheel HashmiNo ratings yet

- Continental Print ExemptionDocument2 pagesContinental Print ExemptionkhawarNo ratings yet

- Tax Collector Correspondence3840409752263Document2 pagesTax Collector Correspondence3840409752263Muzaffar AliNo ratings yet

- With Tax Jul 22 To June 23Document2 pagesWith Tax Jul 22 To June 23Mirza Naseer AbbasNo ratings yet

- 02 - Withholding Exemption Certificate Jul-Dec 21Document3 pages02 - Withholding Exemption Certificate Jul-Dec 21Raheel AhmedNo ratings yet

- Exemption Certificate Top Link Upto Dec 2020Document1 pageExemption Certificate Top Link Upto Dec 2020khawarNo ratings yet

- Internal Corresponence2644435Document1 pageInternal Corresponence2644435Bm ShopNo ratings yet

- Exemption Certification Jpi Month of July-18 To Dec-18Document1 pageExemption Certification Jpi Month of July-18 To Dec-18syasir85No ratings yet

- Internet BillMAR2024Document1 pageInternet BillMAR2024mudhassir.aliNo ratings yet

- Exemption Certificate Tax On Profit Bannu UniversityDocument2 pagesExemption Certificate Tax On Profit Bannu UniversityHazrat AminNo ratings yet

- 114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023Document2 pages114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023BISMA RAFIQNo ratings yet

- Muhammad Asif Khan CIR Appeals DocsDocument14 pagesMuhammad Asif Khan CIR Appeals DocsSaad TahirNo ratings yet

- Order 3430212567583Document9 pagesOrder 3430212567583Saad TahirNo ratings yet

- D091963615 16928640576314369 ProposalDocument5 pagesD091963615 16928640576314369 ProposalDevanshu GoswamiNo ratings yet

- 21 - 30221463102456 NCR JhansiDocument2 pages21 - 30221463102456 NCR JhansiAbhishek DahiyaNo ratings yet

- Declaration 3520228712048Document5 pagesDeclaration 3520228712048hinamuzammil.acaNo ratings yet

- FALTA Special Economic Zone Authority - 19620231047623Document15 pagesFALTA Special Economic Zone Authority - 19620231047623shafaquesameen2001No ratings yet

- S Dps HK Sont 0520222023 AddendumDocument1 pageS Dps HK Sont 0520222023 AddendumABBA MALLANo ratings yet

- Tax Exemption Certificate 2023 2024Document1 pageTax Exemption Certificate 2023 2024Rehnuma TrustNo ratings yet

- Order 3362544Document3 pagesOrder 3362544hamza awanNo ratings yet

- Eway Bill - Devangi PolymersDocument1 pageEway Bill - Devangi PolymersDeep AgrawalNo ratings yet

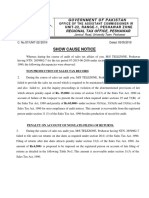

- Show Cause NoticeDocument8 pagesShow Cause NoticeinfoNo ratings yet

- 31 2023 2294 PDFDocument2 pages31 2023 2294 PDFLochan PhogatNo ratings yet

- HR45D 0007 EndosDocument1 pageHR45D 0007 Endosstjohnschool41No ratings yet

- With Tax Apr 23 To June 23Document2 pagesWith Tax Apr 23 To June 23Mirza Naseer AbbasNo ratings yet

- Ircon Technical ManpowerDocument101 pagesIrcon Technical ManpowerPriyesh Kumar CNo ratings yet

- Exemption Order 153 From Jul-Dec-18Document1 pageExemption Order 153 From Jul-Dec-18WaqasBashirNo ratings yet

- Robiul Hoque PDFDocument2 pagesRobiul Hoque PDFAMIRUL HAQUENo ratings yet

- Gccv-Public Carriers Other Than Three Wheelers Package Policy - Zone C Motor Insurance Certificate Cum Policy ScheduleDocument3 pagesGccv-Public Carriers Other Than Three Wheelers Package Policy - Zone C Motor Insurance Certificate Cum Policy Schedulefaiz.sf3033No ratings yet

- Certificate 3Document3 pagesCertificate 3Moses VilladelgadoNo ratings yet

- March InvDocument1 pageMarch Invkranthimahesh999No ratings yet

- Internal Corresponence3970701Document1 pageInternal Corresponence3970701Bm ShopNo ratings yet

- Tendernotice 1Document2 pagesTendernotice 1Soundar SNo ratings yet

- INC-24 11 04 2023 Signed PDFDocument4 pagesINC-24 11 04 2023 Signed PDFmazars advisoryNo ratings yet

- Tender For Audit of Accounts of TBB and Field DDOs - AmemdedDocument8 pagesTender For Audit of Accounts of TBB and Field DDOs - AmemdedAnimeshSahaNo ratings yet

- GC No.04-2023Document2 pagesGC No.04-2023Baljeet SinghNo ratings yet

- United India Insurance Company Limited: MR - Jiwan SinghDocument7 pagesUnited India Insurance Company Limited: MR - Jiwan Singhgunjanrawat23621No ratings yet

- Invitation To Tender (ITT)Document48 pagesInvitation To Tender (ITT)Tebogo SadikiNo ratings yet

- Karan MaliyaDocument2 pagesKaran Maliyasales.kayteeautoNo ratings yet

- SOA-Lily Restaurant-1-4-2023 TO 30-4-2023Document1 pageSOA-Lily Restaurant-1-4-2023 TO 30-4-2023Faraz KhanNo ratings yet

- 114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023Document4 pages114 (1) (Return of Income Filed Voluntarily For Complete Year) - 2023MUHAMMAD TABRAIZNo ratings yet

- United India Insurance Company LimitedDocument7 pagesUnited India Insurance Company Limitedyatishduggal4No ratings yet

- Tax Collector Correspondence3362544Document1 pageTax Collector Correspondence3362544hamza awanNo ratings yet

- LRN LetterDocument2 pagesLRN LettersubratdasbaliNo ratings yet

- Loan Sanction LetterDocument3 pagesLoan Sanction Lettergaurav sondhiNo ratings yet

- INVOICEDocument1 pageINVOICEAshok Kumar PanigrahiNo ratings yet

- Tender Document OHE T003 O1ZSDocument120 pagesTender Document OHE T003 O1ZSchaitanya bholeNo ratings yet

- Vir BahadurDocument4 pagesVir BahadurAkshat JindalNo ratings yet

- 2023 Philgeps Certfiicate WELD Construction CEBU Expire 11.29.2024 Updated 11.15..2023Document3 pages2023 Philgeps Certfiicate WELD Construction CEBU Expire 11.29.2024 Updated 11.15..2023Darvie Joy ElleviraNo ratings yet

- An Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersFrom EverandAn Overview of Compulsory Strata Management Law in NSW: Michael Pobi, Pobi LawyersNo ratings yet

- Property Tax ExemptionsDocument1 pageProperty Tax ExemptionsLexi CortesNo ratings yet

- CARELIFT - BIR Form 2550Q VAT RETURN - 4Q 2021Document1 pageCARELIFT - BIR Form 2550Q VAT RETURN - 4Q 2021Jay Mark DimaanoNo ratings yet

- State Land Investment Corporation v. Cir DigestDocument2 pagesState Land Investment Corporation v. Cir DigestAlan Gultia100% (1)

- 187 Lucky Hardware 23 24Document1 page187 Lucky Hardware 23 24REZAUL KARIMNo ratings yet

- Attention:: Not File Copy A Downloaded From This Website. The Official Printed Version of This IRS Form IsDocument6 pagesAttention:: Not File Copy A Downloaded From This Website. The Official Printed Version of This IRS Form IsBenne James50% (2)

- Acabar Payslip 2Document1 pageAcabar Payslip 2Niña Rica SembrinoNo ratings yet

- MU Syllabus Taxation-2 Transfer-TaxesDocument3 pagesMU Syllabus Taxation-2 Transfer-TaxesDJabNo ratings yet

- Answer For Payroll ProblemsDocument21 pagesAnswer For Payroll ProblemsAnonymous Lz2qH7No ratings yet

- Sales Exclusive Tax Rate &Document3 pagesSales Exclusive Tax Rate &HaripriyaNo ratings yet

- Tax Invoice: VARMORA INTERNATIONAL, Dhuva, Gujarat. State Code: 24 Details of DispatchDocument3 pagesTax Invoice: VARMORA INTERNATIONAL, Dhuva, Gujarat. State Code: 24 Details of Dispatchparvezahmad04No ratings yet

- Salaryslip June 2022Document2 pagesSalaryslip June 2022Suman KumarNo ratings yet

- Show Cause Notice: Government of PakistanDocument3 pagesShow Cause Notice: Government of PakistanFAIZ AliNo ratings yet

- Declaration Form (22-23)Document4 pagesDeclaration Form (22-23)vasavi kNo ratings yet

- 2223TPG0008835Document2 pages2223TPG0008835Huskee CokNo ratings yet

- Creation PuOd 274 133709Document1 pageCreation PuOd 274 133709emamoddin ahemadNo ratings yet

- Philamlife vs. SOFDocument1 pagePhilamlife vs. SOFMichelleNo ratings yet

- CHAPTER 15 Transfer Business TaxDocument9 pagesCHAPTER 15 Transfer Business TaxJamaica DavidNo ratings yet

- Conneqt Business Solutions Limited: 286124 Siddhant Murari SharmaDocument1 pageConneqt Business Solutions Limited: 286124 Siddhant Murari SharmaRadha SharmaNo ratings yet

- Salary September2023Document2 pagesSalary September2023depiha5135No ratings yet

- Up23t 4849Document3 pagesUp23t 4849arshadnsdl8No ratings yet

- SICOM P2 Defect64 CanadaInvoice 16mar20Document1 pageSICOM P2 Defect64 CanadaInvoice 16mar20Prem KumarNo ratings yet

- Invoice 5371888557Document2 pagesInvoice 5371888557vaibhav agrawalNo ratings yet

- University of Management and Technology Quotation Master Paints 01-08-2023Document2 pagesUniversity of Management and Technology Quotation Master Paints 01-08-2023usman khanNo ratings yet

- YdryDocument2 pagesYdryVinodhkumar Shanmugam100% (1)

- Ka 2324 3148073Document3 pagesKa 2324 3148073GAURAV CHITTORANo ratings yet

- Feb 1Document1 pageFeb 1vishnuvardhan reddyNo ratings yet

- 1604-CFDocument8 pages1604-CFmamasita25No ratings yet

- Tally SOP-3 Solution (Final Without Errors)Document3 pagesTally SOP-3 Solution (Final Without Errors)Diya -plays hereNo ratings yet

- Tax267 Ex3Document4 pagesTax267 Ex3SITI NUR DIANA SELAMATNo ratings yet