You might also like

- Homework Chapter 4Document17 pagesHomework Chapter 4Trung Kiên Nguyễn100% (1)

- ABM-FABM2 12 - Q1 - W4 - Mod4Document13 pagesABM-FABM2 12 - Q1 - W4 - Mod4Jose John Vocal90% (21)

- What Every Real Estate Investor Needs to Know About Cash Flow... And 36 Other Key Financial Measures, Updated EditionFrom EverandWhat Every Real Estate Investor Needs to Know About Cash Flow... And 36 Other Key Financial Measures, Updated EditionRating: 4.5 out of 5 stars4.5/5 (15)

- Chapter 1 Review of The Accounting CycleDocument13 pagesChapter 1 Review of The Accounting CycleLouriel MartinezNo ratings yet

- Module 5 SlidesDocument34 pagesModule 5 SlidesSunena KumariNo ratings yet

- FR5 - Consolidated Is (Stud)Document15 pagesFR5 - Consolidated Is (Stud)duong duongNo ratings yet

- Three Basic Accounting Statements:: - Income StatementDocument14 pagesThree Basic Accounting Statements:: - Income Statementamedina8131No ratings yet

- Conceptual Difference Between Fundamental and Technical AnalysisDocument10 pagesConceptual Difference Between Fundamental and Technical AnalysisAdarsh NimborkarNo ratings yet

- OCI and Its Treatment in LawDocument24 pagesOCI and Its Treatment in LawCA TanishNo ratings yet

- Intermediate Accounting: Chapter 16 Appendix ADocument24 pagesIntermediate Accounting: Chapter 16 Appendix AShuo LuNo ratings yet

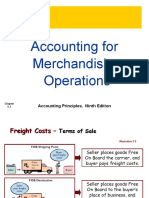

- Accounting For Merchandising Operations: Accounting Principles, Ninth EditionDocument17 pagesAccounting For Merchandising Operations: Accounting Principles, Ninth EditionMehedi HasanNo ratings yet

- Lecture 5. Capital Revenue Expenditure - Student NotesDocument6 pagesLecture 5. Capital Revenue Expenditure - Student NotesTân NguyênNo ratings yet

- Chapter 8 - Part ADocument22 pagesChapter 8 - Part AKwan Kwok AsNo ratings yet

- Hawawini Profitability - Ch5Document34 pagesHawawini Profitability - Ch5FahmyNo ratings yet

- Intercorporate Investments 2019Document14 pagesIntercorporate Investments 2019Jähäñ ShërNo ratings yet

- Group Reporting IV: Consolidation Under Ifrs 10Document84 pagesGroup Reporting IV: Consolidation Under Ifrs 10فهد التويجريNo ratings yet

- Topic 4 Basic Financial StatementsDocument25 pagesTopic 4 Basic Financial StatementsJonisNo ratings yet

- 462 Chapter 5 Notes 2019Document23 pages462 Chapter 5 Notes 2019Shajid Ul HaqueNo ratings yet

- Ch. 1-3Document29 pagesCh. 1-3UjangNo ratings yet

- 01 Accounting StatementsDocument4 pages01 Accounting StatementsTijana DoberšekNo ratings yet

- Chapter 5 Advanced AccountingDocument19 pagesChapter 5 Advanced AccountingMarife De Leon VillalonNo ratings yet

- Chapter 8 - Part ADocument22 pagesChapter 8 - Part AKwan Kwok AsNo ratings yet

- Chapter 6Document46 pagesChapter 6Phương ThảoNo ratings yet

- IFRS 9 WebinarDocument18 pagesIFRS 9 WebinarMovie MovieNo ratings yet

- (ASC) Accounting For Business CombinationDocument13 pages(ASC) Accounting For Business CombinationRENZ ALFRED ASTRERONo ratings yet

- R33 Residual Income ValuationDocument34 pagesR33 Residual Income ValuationAftab SaadNo ratings yet

- 3rd Ed v1.0 - M9A - Keyconcepts (Chapter 5)Document2 pages3rd Ed v1.0 - M9A - Keyconcepts (Chapter 5)Samuel SaravananNo ratings yet

- LBO Interviews Questions BIWSDocument5 pagesLBO Interviews Questions BIWSartemidualikNo ratings yet

- GM Roi White PaperDocument17 pagesGM Roi White PaperPablo Riquelme GonzálezNo ratings yet

- Slide CfaDocument295 pagesSlide CfaLinh HoangNo ratings yet

- Chapter 1 Cost of Capital PDFDocument58 pagesChapter 1 Cost of Capital PDFGiáng Hương VũNo ratings yet

- PSAK 65 Accounting RequirementsDocument19 pagesPSAK 65 Accounting RequirementsDikdik MegantaraNo ratings yet

- Capital Structure (I) : Professor Siyi ShenDocument18 pagesCapital Structure (I) : Professor Siyi ShenjamesNo ratings yet

- Topic Financial RatioDocument14 pagesTopic Financial RatioБота ОмароваNo ratings yet

- PFRS of SME and SE - Concept MapDocument1 pagePFRS of SME and SE - Concept MapRey OñateNo ratings yet

- Fabm2 Mod4Document11 pagesFabm2 Mod4Margaret Pagdilao MaliksiNo ratings yet

- Test Bank For Financial Accounting For Mbas 4th Edition by EastonDocument50 pagesTest Bank For Financial Accounting For Mbas 4th Edition by EastonDavidTrevinomkyji100% (23)

- Financial Instruments Student Version - Updated 190721Document56 pagesFinancial Instruments Student Version - Updated 190721Mohammad Farhan AdbiNo ratings yet

- FIN924 Lecture Topic 2Document73 pagesFIN924 Lecture Topic 2Yugiii YugeshNo ratings yet

- Master in Management: Fundamentals of Finance - Session 1Document446 pagesMaster in Management: Fundamentals of Finance - Session 1Leonardo MercuriNo ratings yet

- Consolidated Financial Statements: Intercompany TransactionsDocument23 pagesConsolidated Financial Statements: Intercompany TransactionsDr-Mohammad Nahawi-Abu AwsNo ratings yet

- Financial SlidesDocument15 pagesFinancial SlidesAnne SmithNo ratings yet

- XH-H 3e PPT Chap05Document69 pagesXH-H 3e PPT Chap05An NhiênNo ratings yet

- Financial Analysis and Reporting 1Document4 pagesFinancial Analysis and Reporting 1Anonymous ryxSr2No ratings yet

- Putting IFRS 9 Into Practice Presentation By: CPA Stephen Obock February 2018Document38 pagesPutting IFRS 9 Into Practice Presentation By: CPA Stephen Obock February 2018syed younasNo ratings yet

- Profit, Profitability and Break Even AnalysisDocument16 pagesProfit, Profitability and Break Even AnalysisDr. Meghna DangiNo ratings yet

- FANAS 7e PPT Chap16Document30 pagesFANAS 7e PPT Chap16hippop kNo ratings yet

- Financial Statement Analysis and Security Valuation: - November 9, 2022 Arnt VerriestDocument43 pagesFinancial Statement Analysis and Security Valuation: - November 9, 2022 Arnt VerriestfelipeNo ratings yet

- Finman ReviewerDocument8 pagesFinman ReviewerRafael BensigNo ratings yet

- Analyst Training: Advanced Comps & Pre-PaidsDocument18 pagesAnalyst Training: Advanced Comps & Pre-Paidswaseem1986No ratings yet

- As Levels Accounts NotesDocument19 pagesAs Levels Accounts NotesEmaan MerchantNo ratings yet

- Session 2 Chapter 3 Working With Financial StatementDocument23 pagesSession 2 Chapter 3 Working With Financial StatementOkura TsukikoNo ratings yet

- FINE4016 Lecture Slides (Financial Statement Analysis I) 20170321 - Student VersionDocument68 pagesFINE4016 Lecture Slides (Financial Statement Analysis I) 20170321 - Student Versionjack100% (2)

- 28 Financial Analysis and PlanningDocument15 pages28 Financial Analysis and Planningddrechsler9No ratings yet

- 6 Degree of LeveragesDocument5 pages6 Degree of LeveragesJennalyn DamasoNo ratings yet

- Profitability Ratio Analysis: Purpose: Return On AssetsDocument15 pagesProfitability Ratio Analysis: Purpose: Return On AssetsshawonNo ratings yet

- Financial Management 2Document33 pagesFinancial Management 2Zero OneNo ratings yet

- PowerpointPresentation Chapter 5Document25 pagesPowerpointPresentation Chapter 5Nilisha PradhanNo ratings yet

- CM 8 - Business and Consumer Loan (SCGMATH)Document19 pagesCM 8 - Business and Consumer Loan (SCGMATH)allebNo ratings yet

- 03 Financial Statement AnalysisDocument46 pages03 Financial Statement Analysissimao.lipscombNo ratings yet

- Understanding Balance SheetsDocument26 pagesUnderstanding Balance SheetsAli AhmedNo ratings yet

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)From EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)No ratings yet

- Operating and Financial Leverage: Block, Hirt, and DanielsenDocument31 pagesOperating and Financial Leverage: Block, Hirt, and DanielsenOona NiallNo ratings yet

- Acca Strategic Business Reporting (International) Mock Examination 2Document8 pagesAcca Strategic Business Reporting (International) Mock Examination 2Asad MuhammadNo ratings yet

- Inter IKEA Group Annual Report 2013 PDFDocument29 pagesInter IKEA Group Annual Report 2013 PDFDwiChen67% (3)

- Chapter 7 - Finanacial Project ApprisalDocument46 pagesChapter 7 - Finanacial Project ApprisalDomach Keak RomNo ratings yet

- Auditing - MCQDocument14 pagesAuditing - MCQProf. Subhassis PalNo ratings yet

- Constable Police Employee Payslip - IFMISDocument1 pageConstable Police Employee Payslip - IFMISpraveen kumarNo ratings yet

- 4335287Document8 pages4335287mohitgaba19No ratings yet

- Visa & Mastercard: The Pain of Paying The Psychology of MoneyDocument16 pagesVisa & Mastercard: The Pain of Paying The Psychology of Moneyferoz_bilalNo ratings yet

- NikkakkaDocument40 pagesNikkakkaGabriel LozanoNo ratings yet

- CA-Ashok-Mehta - PPT - Income TaxDocument88 pagesCA-Ashok-Mehta - PPT - Income TaxAbinash DasNo ratings yet

- Out Marriott PDFDocument35 pagesOut Marriott PDFemigdio contrerasNo ratings yet

- ACCT 201: Reporting and Analyzing InventoryDocument22 pagesACCT 201: Reporting and Analyzing InventoryDuygu YılmazNo ratings yet

- Alicorp Earnings Call Presentation 4Q21 VFDocument42 pagesAlicorp Earnings Call Presentation 4Q21 VFCesar MelgarNo ratings yet

- CABARLE Microeconomics FLADocument6 pagesCABARLE Microeconomics FLAAdrian CabarleNo ratings yet

- Deceive Cruel Definite Deliberate FirmDocument25 pagesDeceive Cruel Definite Deliberate FirmRANJAN YADAVNo ratings yet

- Topic 3 - Recording Transactions (STU)Document80 pagesTopic 3 - Recording Transactions (STU)Kim ChiNo ratings yet

- Chapter 2Document10 pagesChapter 2mengistuNo ratings yet

- Accrual and ProvisionDocument66 pagesAccrual and ProvisionVeronica Bailey100% (1)

- Effects of The Great Depression 1929-1933Document2 pagesEffects of The Great Depression 1929-1933Alexander Saliyuti75% (4)

- 2021 - 04 - 28 - 12 - 22 - 04financial Results of Inter Media and Communication S.p.A For The 9 Months Ended 31 March 2021Document37 pages2021 - 04 - 28 - 12 - 22 - 04financial Results of Inter Media and Communication S.p.A For The 9 Months Ended 31 March 2021Dhan DhanNo ratings yet

- Tle 6-He Module 1Document19 pagesTle 6-He Module 1MARILYN JAKOSALEMNo ratings yet

- Income Statement Vertical Analysis TemplateDocument2 pagesIncome Statement Vertical Analysis TemplateSope DalleyNo ratings yet

- College of Engineering and Architecture: Urdaneta City University San Vicente West, Urdaneta CityDocument5 pagesCollege of Engineering and Architecture: Urdaneta City University San Vicente West, Urdaneta CitySamuel ArzadonNo ratings yet

- NBL F21 Half Year ResultsDocument2 pagesNBL F21 Half Year ResultsLazarus Kadett NdivayeleNo ratings yet

- Topic 3 - The Recording Process (Student)Document27 pagesTopic 3 - The Recording Process (Student)leef leefNo ratings yet

- Accounting For Joint ArrangementsDocument4 pagesAccounting For Joint ArrangementsQuinn Samaon100% (1)

- Shankesh NARAYAN MANDAVAKAR 5071 Payslip DecemberDocument1 pageShankesh NARAYAN MANDAVAKAR 5071 Payslip DecemberZeenatNo ratings yet

- Chapter 1 5 Income Tax MCDocument14 pagesChapter 1 5 Income Tax MCNoella Marie BaronNo ratings yet