You might also like

- Determinants of Interest Rate Spreads in Sub-Saharan African Countries A Dynamic Panel AnalysisDocument26 pagesDeterminants of Interest Rate Spreads in Sub-Saharan African Countries A Dynamic Panel AnalysisEdson AlmeidaNo ratings yet

- Credit Risk Management and The Performance of Deposit Money Banks in Nigeria: An Error Correction AnalysisDocument13 pagesCredit Risk Management and The Performance of Deposit Money Banks in Nigeria: An Error Correction AnalysisAnonymous ed8Y8fCxkSNo ratings yet

- Interest Rate Spread On Bank Profitability: The Case of Ghanaian BanksDocument12 pagesInterest Rate Spread On Bank Profitability: The Case of Ghanaian BanksKiller BrothersNo ratings yet

- Determinants of Non-Performing Loan in Nepalese Commercial BanksDocument17 pagesDeterminants of Non-Performing Loan in Nepalese Commercial Bankskripa poudelNo ratings yet

- The Effects of Interest Rate Spread On The Level of Non-Performing Assets - A Case of Commercial Banks in KenyaDocument8 pagesThe Effects of Interest Rate Spread On The Level of Non-Performing Assets - A Case of Commercial Banks in KenyaNur Arvah TamrinNo ratings yet

- Effects of Credit Risk Management on Financial Performance of Commercial BanksDocument8 pagesEffects of Credit Risk Management on Financial Performance of Commercial BanksGizachewNo ratings yet

- Determinant of Credit Growth and Banj Lending Channel in PeruDocument33 pagesDeterminant of Credit Growth and Banj Lending Channel in PeruMuhammad. RayyanNo ratings yet

- Determinants of Non-Performing Loans in Pakistan: Tanweer@s3h.nust - Edu.pkDocument15 pagesDeterminants of Non-Performing Loans in Pakistan: Tanweer@s3h.nust - Edu.pkChương Nguyễn ĐìnhNo ratings yet

- Monetary Policy On Commercial Bank LoansDocument13 pagesMonetary Policy On Commercial Bank LoansAbdulkabirNo ratings yet

- Influence of Financial Depth On Financial Performance of Commercial Banks in RwandaDocument12 pagesInfluence of Financial Depth On Financial Performance of Commercial Banks in RwandaJohn PaulNo ratings yet

- Effects of Credit Risk Management On Loan Performance in Kenyan Commercial BanksDocument13 pagesEffects of Credit Risk Management On Loan Performance in Kenyan Commercial BanksManpreet Kaur VirkNo ratings yet

- Journal of Economics and Business: Cristian Barra, Nazzareno RuggieroDocument19 pagesJournal of Economics and Business: Cristian Barra, Nazzareno RuggieroAlfonso VenturaNo ratings yet

- Risk Components and The Financial PerforDocument8 pagesRisk Components and The Financial PerforRasaq MojeedNo ratings yet

- Macroeconomic Determinants of Interest Rate Spread in Ghana: Evidence From ARDL Modelling ApproachDocument18 pagesMacroeconomic Determinants of Interest Rate Spread in Ghana: Evidence From ARDL Modelling ApproachViverNo ratings yet

- Bank Lending Rates and Spreads in EMDEs Evolution Drivers and PoliciesDocument53 pagesBank Lending Rates and Spreads in EMDEs Evolution Drivers and PoliciesLovemore TshumaNo ratings yet

- Factors Impacting Non-Performing Loans in Pakistan's Banking IndustryDocument13 pagesFactors Impacting Non-Performing Loans in Pakistan's Banking IndustryChinthaka PereraNo ratings yet

- Business and Economic Cyle, Financial MarketDocument20 pagesBusiness and Economic Cyle, Financial MarketadeNo ratings yet

- The Dynamics of Bank Competition in Kenya: Mdoe, Idi Jackson, Jacob O. Omolo, and Nelson H. W. WawireDocument45 pagesThe Dynamics of Bank Competition in Kenya: Mdoe, Idi Jackson, Jacob O. Omolo, and Nelson H. W. WawireShoaib SamNo ratings yet

- VietnamDocument49 pagesVietnamShoikot BishwasNo ratings yet

- Macroeconomic Determinants of Stock Market Development in GhanaDocument16 pagesMacroeconomic Determinants of Stock Market Development in GhanaJEAN PIERRE RIVERA HUANUCONo ratings yet

- Influence of Operational and Liquidity Risk on Financial Performance of Microfinance Banks in KenyaDocument12 pagesInfluence of Operational and Liquidity Risk on Financial Performance of Microfinance Banks in KenyaHeru ErlanggaNo ratings yet

- Bruneibankskpisandintegration Forthcoming PDFDocument30 pagesBruneibankskpisandintegration Forthcoming PDFAbcdNo ratings yet

- Determinants of Interest Rate Spread of NepaleseDocument10 pagesDeterminants of Interest Rate Spread of NepaleseRajendra LamsalNo ratings yet

- Determinants of Non-Performing Loans in NigeriaDocument8 pagesDeterminants of Non-Performing Loans in NigeriaEdlamu AlemieNo ratings yet

- Banking Stability in Nigeria-1Document33 pagesBanking Stability in Nigeria-1Seye KareemNo ratings yet

- Batten, J., & Vo, X. V. (2019) .Document13 pagesBatten, J., & Vo, X. V. (2019) .ShinyeNo ratings yet

- Role of Bank Regulation On Bank Performance: Evidence From Asia-Pacific Commercial BanksDocument25 pagesRole of Bank Regulation On Bank Performance: Evidence From Asia-Pacific Commercial BanksSayeda AlinaNo ratings yet

- Determinant of Credit Growth in LebanonDocument11 pagesDeterminant of Credit Growth in LebanonMuhammad. RayyanNo ratings yet

- What Influences Banks Lending in Sub-Saharan Africa?: Mohammed AmiduDocument42 pagesWhat Influences Banks Lending in Sub-Saharan Africa?: Mohammed Amidueconomic.rezaeiNo ratings yet

- CccrupDocument15 pagesCccrupIbrahim MuhammadibrahimNo ratings yet

- Determinants of Bank Lending Behaviour in Ghana Jonas Ladime1 Emmanuel Sarpong-Kumankoma2 Kofi A. Osei2 PDFDocument7 pagesDeterminants of Bank Lending Behaviour in Ghana Jonas Ladime1 Emmanuel Sarpong-Kumankoma2 Kofi A. Osei2 PDFDeaz Fazzaura PutriNo ratings yet

- Managing Non-Performing Assets in BankingDocument11 pagesManaging Non-Performing Assets in BankingSAMARTH TIWARINo ratings yet

- Does Monetary Policy Affect Bank Risk-Taking?: Centre For Banking and Financial Studies, Bangor UniversityDocument46 pagesDoes Monetary Policy Affect Bank Risk-Taking?: Centre For Banking and Financial Studies, Bangor Universitydungtran0989No ratings yet

- 623-Article Text-2128-2234-10-20190629Document18 pages623-Article Text-2128-2234-10-20190629CorisytNo ratings yet

- SSRN Id2938546Document16 pagesSSRN Id2938546Hesti PermatasariNo ratings yet

- BCN Working Paper FinalDocument78 pagesBCN Working Paper Finalnishant6907No ratings yet

- Relationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaDocument28 pagesRelationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaCatherine AteNo ratings yet

- CREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHDocument8 pagesCREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHdarkniightNo ratings yet

- Economic Factors Driving Pakistani Bank NPLsDocument14 pagesEconomic Factors Driving Pakistani Bank NPLsGilbert Ansah YirenkyiNo ratings yet

- Determinants of Bank Profitability in Western European Countries Evidence From System GMM EstimatesDocument13 pagesDeterminants of Bank Profitability in Western European Countries Evidence From System GMM EstimatesHbiba HabboubaNo ratings yet

- Wa0015.Document4 pagesWa0015.pandeynikhil080No ratings yet

- Assessment of The Determinants of Non-Performing Loans and Their Effects On Performance of Commercial Banks in KenyaDocument23 pagesAssessment of The Determinants of Non-Performing Loans and Their Effects On Performance of Commercial Banks in KenyaOIRCNo ratings yet

- Kinshuk Sir - ReferenceDocument16 pagesKinshuk Sir - ReferenceBhaskargrNo ratings yet

- Fane Kelvin Work3Document11 pagesFane Kelvin Work3ekojamichaelNo ratings yet

- Literature ReviewDocument3 pagesLiterature ReviewNgọc Dương Thị BảoNo ratings yet

- KantengwaDocument30 pagesKantengwaMana Uri NzizaNo ratings yet

- Al MagharemDocument15 pagesAl MagharemPham NamNo ratings yet

- DocumentDocument13 pagesDocumentdhahri nourhenNo ratings yet

- The Effect of Credit and Market Risk On Bank Performance - Evidence From Turkey (#352457) - 363360Document8 pagesThe Effect of Credit and Market Risk On Bank Performance - Evidence From Turkey (#352457) - 363360ZinebNo ratings yet

- NPL LocalperceptionDocument21 pagesNPL Localperceptionkripa poudelNo ratings yet

- Impact of Non-Performing Loans On Bank's Profitability: Empirical Evidence From Commercial Banks in TanzaniaDocument9 pagesImpact of Non-Performing Loans On Bank's Profitability: Empirical Evidence From Commercial Banks in TanzaniaChương Nguyễn ĐìnhNo ratings yet

- 4 Importnt - DETERMINANTSOFBANKPROFITABILITY1.JordanDocument12 pages4 Importnt - DETERMINANTSOFBANKPROFITABILITY1.JordanFarooq KhanNo ratings yet

- African Vol4 Article2Document22 pagesAfrican Vol4 Article2Rani AliNo ratings yet

- Impact of Diversification, Competition and Regulation On Banks Risk Taking: Evidence From Asian Emerging EconomiesDocument61 pagesImpact of Diversification, Competition and Regulation On Banks Risk Taking: Evidence From Asian Emerging EconomiesAfsheenNo ratings yet

- Competition and Commercial Banks Risk Taking Evidence From Sub Saharan Africa RegionDocument15 pagesCompetition and Commercial Banks Risk Taking Evidence From Sub Saharan Africa RegionJesus castroNo ratings yet

- Chapter One by Group 9-1Document8 pagesChapter One by Group 9-1Mohamed B SannohNo ratings yet

- Determinants of The Exchange Rate, Its VolaDocument48 pagesDeterminants of The Exchange Rate, Its VolaMichael OdiemboNo ratings yet

- The Determinants of Bank Profitability: Dynamic Panel Evidence From South Asian CountriesDocument21 pagesThe Determinants of Bank Profitability: Dynamic Panel Evidence From South Asian Countriessunil lamichhaneNo ratings yet

- EIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataFrom EverandEIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataNo ratings yet

- LAC Semiannual Report, October 2013: Latin America’s Deceleration and the Exchange Rate BufferFrom EverandLAC Semiannual Report, October 2013: Latin America’s Deceleration and the Exchange Rate BufferNo ratings yet

- Ijfe 2370Document23 pagesIjfe 2370ViverNo ratings yet

- RP 106Document52 pagesRP 106ViverNo ratings yet

- Best ScenarioDocument4 pagesBest ScenarioViverNo ratings yet

- Ecaf 12233Document9 pagesEcaf 12233ViverNo ratings yet

- Best ScenarioDocument3 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument3 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument3 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument4 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument3 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument4 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument4 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument3 pagesBest ScenarioViverNo ratings yet

- The Other ScenarioDocument5 pagesThe Other ScenarioViverNo ratings yet

- Best ScenarioDocument4 pagesBest ScenarioViverNo ratings yet

- The Other ScenarioDocument7 pagesThe Other ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- Best ScenarioDocument2 pagesBest ScenarioViverNo ratings yet

- The Other ScenarioDocument14 pagesThe Other ScenarioViverNo ratings yet

- The Other ScenarioDocument4 pagesThe Other ScenarioViverNo ratings yet

- The Other ScenarioDocument7 pagesThe Other ScenarioViverNo ratings yet

- The Other ScenarioDocument17 pagesThe Other ScenarioViverNo ratings yet

- Dalal Street Investment Journal PDFDocument26 pagesDalal Street Investment Journal PDFShailesh KhodkeNo ratings yet

- GeneralMathematics (SHS) Q2 Mod9 DifferentMarketsForStocksAndBonds V1Document24 pagesGeneralMathematics (SHS) Q2 Mod9 DifferentMarketsForStocksAndBonds V1Rachael Ortiz86% (7)

- Sales and Marketing ManagementDocument5 pagesSales and Marketing Managementapi-78558323No ratings yet

- Analyze Engineering Economy ProblemsDocument4 pagesAnalyze Engineering Economy ProblemsRenellejay PHNo ratings yet

- Types of Financial MarketsDocument12 pagesTypes of Financial MarketsunicornsarecoolasiceNo ratings yet

- DornbuschDocument13 pagesDornbuschdivyajain2888No ratings yet

- @ieltsbank Idea - Bank - BusinessDocument53 pages@ieltsbank Idea - Bank - Businesslindazykov43719No ratings yet

- Axis Bank: Asset Quality Normalization From 3QFY22 OnwardsDocument10 pagesAxis Bank: Asset Quality Normalization From 3QFY22 OnwardsLizzy McquireNo ratings yet

- Responses of People in %: Q1. On Which Bank You Depend For Your Regular Transaction?Document12 pagesResponses of People in %: Q1. On Which Bank You Depend For Your Regular Transaction?Shobhit GoswamiNo ratings yet

- FINDocument26 pagesFINJadeNo ratings yet

- Factors: How Time and Interest Affect Money: Engineering EconomyDocument33 pagesFactors: How Time and Interest Affect Money: Engineering Economymudassir ahmadNo ratings yet

- Finance HSC Business NotesDocument32 pagesFinance HSC Business NoteschloeNo ratings yet

- Financial Services Environment Chapter 1Document26 pagesFinancial Services Environment Chapter 1Joelene Chew100% (1)

- Assignment On Financial Resource ManagementDocument16 pagesAssignment On Financial Resource ManagementZubayer HussainNo ratings yet

- Credit Transactions ReviewerDocument18 pagesCredit Transactions ReviewerMonique AcostaNo ratings yet

- Why You Just Can't Withdraw A Bounce Back Loan From Company?Document2 pagesWhy You Just Can't Withdraw A Bounce Back Loan From Company?kainat fatimaNo ratings yet

- Maths - QuestionsDocument18 pagesMaths - QuestionsraghavNo ratings yet

- Financial Terms GlossaryDocument11 pagesFinancial Terms GlossarysubhasishmajumdarNo ratings yet

- Littlefield Game 2 OverviewDocument3 pagesLittlefield Game 2 OverviewRichard Joshua SNo ratings yet

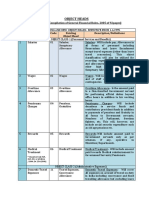

- Object Heads ListingDocument6 pagesObject Heads ListingLal ZahawmaNo ratings yet

- Introduction to Malaysia's Financial System and Bank Negara MalaysiaDocument47 pagesIntroduction to Malaysia's Financial System and Bank Negara MalaysiaHyun爱纶星No ratings yet

- Jam, Jelly, Murabba Manufacturing Project ProfileDocument2 pagesJam, Jelly, Murabba Manufacturing Project ProfilecasagarteliNo ratings yet

- B.inggris N Kel.2Document34 pagesB.inggris N Kel.2Putra RakhmadaniNo ratings yet

- Liquidity Preference Theory of Rate of InterestDocument13 pagesLiquidity Preference Theory of Rate of InterestNishchay SaxenaNo ratings yet

- IIFL - Embassy REIT - Initiating Coverage - 20200127Document39 pagesIIFL - Embassy REIT - Initiating Coverage - 20200127Saatvik ShettyNo ratings yet

- Midterm 2 SolutionDocument11 pagesMidterm 2 SolutiondavidNo ratings yet

- Financial Markets Assignment 1Document2 pagesFinancial Markets Assignment 1Mary Joy SameonNo ratings yet

- What Moves Housing Markets - A Variance Decomposition of The Rent-Price RatioDocument13 pagesWhat Moves Housing Markets - A Variance Decomposition of The Rent-Price RatioEdivaldo PaciênciaNo ratings yet

- Understanding Culture, Society, and PoliticsDocument12 pagesUnderstanding Culture, Society, and PoliticsrobertNo ratings yet

- International Parity Conditions: Dr. Ch. Venkata Krishna Reddy Associate ProfessorDocument34 pagesInternational Parity Conditions: Dr. Ch. Venkata Krishna Reddy Associate Professorkrishna reddyNo ratings yet