0% found this document useful (0 votes)

73 views3 pagesAuditing: External Confirmation Guide

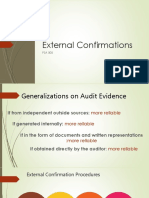

External confirmation involves obtaining verification from third parties to support audit opinions. The procedure involves determining information to confirm, selecting parties, designing requests, sending requests, and follow-ups. When management refuses confirmation, auditors must examine reasons, assess implications, and perform alternative procedures like analytical procedures, substantive testing, inquiry and observation, and documentation review.

Uploaded by

afsiya.mjCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

73 views3 pagesAuditing: External Confirmation Guide

External confirmation involves obtaining verification from third parties to support audit opinions. The procedure involves determining information to confirm, selecting parties, designing requests, sending requests, and follow-ups. When management refuses confirmation, auditors must examine reasons, assess implications, and perform alternative procedures like analytical procedures, substantive testing, inquiry and observation, and documentation review.

Uploaded by

afsiya.mjCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd