You might also like

- ACT1207 Module 1 - Review of Audit ProcessDocument11 pagesACT1207 Module 1 - Review of Audit ProcessACNo ratings yet

- Chapter-2 (2nd Part)Document12 pagesChapter-2 (2nd Part)anan wahid khanNo ratings yet

- Acca - F 8 - L2Document14 pagesAcca - F 8 - L2shazyasgharNo ratings yet

- Alan Fernandes (AUDIT EVIDENCE TO AUDIT REPORTING)Document28 pagesAlan Fernandes (AUDIT EVIDENCE TO AUDIT REPORTING)Alan FernandesNo ratings yet

- Auditing Explained in A Thousand WordsDocument4 pagesAuditing Explained in A Thousand Wordsparrenojoshua21.svcNo ratings yet

- Audit - Isa 500Document6 pagesAudit - Isa 500Imran AsgharNo ratings yet

- Explanation of Audit Report of Grameenphone LTDDocument19 pagesExplanation of Audit Report of Grameenphone LTDtaohid khanNo ratings yet

- Audit Process StepsDocument3 pagesAudit Process StepsShaira UntalanNo ratings yet

- Chapter Three: Obtaining, Evaluating and Documenting Audit Data Over Viewing Audit EvidenceDocument7 pagesChapter Three: Obtaining, Evaluating and Documenting Audit Data Over Viewing Audit EvidenceAkkamaNo ratings yet

- Audit Planning NotesDocument30 pagesAudit Planning NotesTinoManhangaNo ratings yet

- Auditng and Assurance Chapter FourDocument46 pagesAuditng and Assurance Chapter FourQais Qazi ZadaNo ratings yet

- Auditing ReportDocument47 pagesAuditing ReportNoj WerdnaNo ratings yet

- Auditing Principles and Practices IDocument7 pagesAuditing Principles and Practices IGemeda TuntunaNo ratings yet

- Chapter-6: in An Effective Manner. Planning Consists of A Number of Elements. However, They Could Be Summarized AsDocument10 pagesChapter-6: in An Effective Manner. Planning Consists of A Number of Elements. However, They Could Be Summarized AsNasir RifatNo ratings yet

- Audit Evidence MethodsDocument11 pagesAudit Evidence MethodsDeepakNo ratings yet

- Ch-3 Audit EvidenceDocument49 pagesCh-3 Audit EvidenceNuraddiin JaafarNo ratings yet

- PA503 Chapter 6 Audit EvidenceDocument6 pagesPA503 Chapter 6 Audit EvidenceAnonymous rJuerZMVNo ratings yet

- Key Definition (FAU)Document8 pagesKey Definition (FAU)BuntheaNo ratings yet

- Performing Substantive TestDocument33 pagesPerforming Substantive TestDawn Jenina Francisco100% (2)

- Chapter 4 (Salosagcol)Document4 pagesChapter 4 (Salosagcol)Lauren Obrien100% (1)

- (MIDTERM) AAP - Module 6 500-501 505 520 580Document6 pages(MIDTERM) AAP - Module 6 500-501 505 520 58025 CUNTAPAY, FRENCHIE VENICE B.No ratings yet

- Chapter 3 NotesDocument6 pagesChapter 3 NotesmatthewNo ratings yet

- Auditing Question Bank - StudentsDocument25 pagesAuditing Question Bank - StudentsAashna JainNo ratings yet

- Colegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas City 1 Semester A.Y. 2020-2021Document4 pagesColegio de La Purisima Concepcion: School of The Archdiocese of Capiz Roxas City 1 Semester A.Y. 2020-2021Jhomel Domingo GalvezNo ratings yet

- Test 8 SSDocument3 pagesTest 8 SSnaseebmasihadvNo ratings yet

- Module 9 - Evaluating The Design and Effcetiveness of Internal ControlDocument5 pagesModule 9 - Evaluating The Design and Effcetiveness of Internal ControlBhosx KimNo ratings yet

- Topic 3 Audit Planning (Slide No.2) - Materiality - Audit RiskDocument57 pagesTopic 3 Audit Planning (Slide No.2) - Materiality - Audit RiskWAN NUR SYAZANA AHMAD YARANINo ratings yet

- Activity Sheet - Module 7Document10 pagesActivity Sheet - Module 7Chris JacksonNo ratings yet

- Module 3 - AuditingDocument22 pagesModule 3 - AuditingSophia Grace NiduazaNo ratings yet

- Chapter 10 Evidence Substantive TestsDocument148 pagesChapter 10 Evidence Substantive Testsfalculan_delsie100% (2)

- Consideration of Internal ControlDocument4 pagesConsideration of Internal ControlFritzie Ann ZartigaNo ratings yet

- Exam by MuhammadDocument8 pagesExam by Muhammadazhar ishaqNo ratings yet

- FACULTY OF ECONOMICS AND MANAGEMENT SCIENCES DEPARTMENT OF BUSINESS STUDIES PHD ASSIGNMENT AUDITING AND INVESTIGATIONSDocument12 pagesFACULTY OF ECONOMICS AND MANAGEMENT SCIENCES DEPARTMENT OF BUSINESS STUDIES PHD ASSIGNMENT AUDITING AND INVESTIGATIONSAlex SemusuNo ratings yet

- Chapter - 4Document7 pagesChapter - 4dejen mengstieNo ratings yet

- Auditing Final RevisionDocument15 pagesAuditing Final RevisionMohamed ShaabanNo ratings yet

- Bsa Operations Auditing - CompressDocument27 pagesBsa Operations Auditing - CompressDion AtaNo ratings yet

- Audit Planning ProcessDocument7 pagesAudit Planning ProcessJun Guerzon PaneloNo ratings yet

- Practical AuditingDocument61 pagesPractical Auditinglloyd100% (1)

- AuditF8 SyDocument11 pagesAuditF8 SyZulu LoveNo ratings yet

- Activity 6Document4 pagesActivity 6Isabell CastroNo ratings yet

- Chap.3 Audit Plannng, Working Paper and Internal Control-1Document10 pagesChap.3 Audit Plannng, Working Paper and Internal Control-1Himanshu MoreNo ratings yet

- ACCO 30043 Assignment Number 5 Answer The Following Questions Briefly and ConciselyDocument3 pagesACCO 30043 Assignment Number 5 Answer The Following Questions Briefly and ConciselyYoung ManyNo ratings yet

- Uploaded in Moodle As A Guide To Complete Your Assignment Apart From Your Other Sources.)Document6 pagesUploaded in Moodle As A Guide To Complete Your Assignment Apart From Your Other Sources.)Derek GawiNo ratings yet

- Audit EvidenceDocument12 pagesAudit Evidencemuriithialex2030No ratings yet

- Principles of Auditing Lecture 5Document4 pagesPrinciples of Auditing Lecture 5Isaac PortelliNo ratings yet

- Audit Evidence and ProceduresDocument2 pagesAudit Evidence and ProceduresDhierissa LeeNo ratings yet

- ACCO 30043 Audit Evidence FactorsDocument7 pagesACCO 30043 Audit Evidence FactorsRoseanneNo ratings yet

- PBL TASK 1 GROUP 4 KUA-dikonversiDocument9 pagesPBL TASK 1 GROUP 4 KUA-dikonversiDiva GunawanNo ratings yet

- Audit and Assurance Part 2Document28 pagesAudit and Assurance Part 2ALEKSBANDANo ratings yet

- A&a L6 EditedDocument6 pagesA&a L6 EditedKimosop Isaac KipngetichNo ratings yet

- Ireneo Chapter 10 Ver 2020Document82 pagesIreneo Chapter 10 Ver 2020shanNo ratings yet

- Planning Key Activities: Objectives, Risk Assessment, Analytical ProceduresDocument3 pagesPlanning Key Activities: Objectives, Risk Assessment, Analytical ProceduresTasha MarieNo ratings yet

- Materi Webinar SA 500 Bukti Audit - Audit Berbasis ISA Studi Kasus Di Indonesia, Australia, Dan SingapuraDocument37 pagesMateri Webinar SA 500 Bukti Audit - Audit Berbasis ISA Studi Kasus Di Indonesia, Australia, Dan SingapuraIkhsan Uiandra Putra SitorusNo ratings yet

- Module 4 Introduction To The Audit ProcessDocument38 pagesModule 4 Introduction To The Audit ProcessRoyce Maenard EstanislaoNo ratings yet

- Pre-Test - Performing The EngagementDocument2 pagesPre-Test - Performing The EngagementSHARMAINE CORPUZ MIRANDANo ratings yet

- CompilationDocument95 pagesCompilationAnwar BogabongNo ratings yet

- Audit ProceduresDocument4 pagesAudit ProceduresHarley Alburque MandapatNo ratings yet

- Chapter 3 General Types of Audit - PPT 123915218Document32 pagesChapter 3 General Types of Audit - PPT 123915218Clar Aaron Bautista100% (2)

- BSPH2106 Accounting in Pharmacy MerchandizingDocument2 pagesBSPH2106 Accounting in Pharmacy MerchandizingWijdan Saleem EdwanNo ratings yet

- Principles of Auditing - Chapter - 4Document34 pagesPrinciples of Auditing - Chapter - 4Wijdan Saleem EdwanNo ratings yet

- Principles of Auditing - Chapter - 3Document31 pagesPrinciples of Auditing - Chapter - 3Wijdan Saleem EdwanNo ratings yet

- 2021 Book TheFourthIndustrialRevolutionI PDFDocument473 pages2021 Book TheFourthIndustrialRevolutionI PDFWijdan Saleem EdwanNo ratings yet

- Principles of Auditing - Chapter - 1Document36 pagesPrinciples of Auditing - Chapter - 1Wijdan Saleem EdwanNo ratings yet

- Gender Disparities in The Duration of Unemployment Spells in SloveniaDocument131 pagesGender Disparities in The Duration of Unemployment Spells in SloveniaWijdan Saleem EdwanNo ratings yet

- Chapter 5 APM 2022-2023Document18 pagesChapter 5 APM 2022-2023Wijdan Saleem EdwanNo ratings yet

- Chapter 3 APM 2022-2023Document33 pagesChapter 3 APM 2022-2023Wijdan Saleem EdwanNo ratings yet

- Accounting Application by Computer (TallyPrime) - BAAC 2205 - HandoutDocument77 pagesAccounting Application by Computer (TallyPrime) - BAAC 2205 - HandoutWijdan Saleem EdwanNo ratings yet

- Chapter 3 Vertical & Horizontal AnalysisDocument21 pagesChapter 3 Vertical & Horizontal AnalysisWijdan Saleem EdwanNo ratings yet

- Hedging Effectiveness in Greek Stock Index Futures Market, 1999-2001Document12 pagesHedging Effectiveness in Greek Stock Index Futures Market, 1999-2001Wijdan Saleem EdwanNo ratings yet

- Hedge Ratio Estimation and Hedging Effectiveness: The Case of The S&P 500 Stock Index Futures ContractDocument25 pagesHedge Ratio Estimation and Hedging Effectiveness: The Case of The S&P 500 Stock Index Futures ContractWijdan Saleem EdwanNo ratings yet

- Hedging Effectiveness and Minimum Risk Hedge Ratios in The Presence of Autocorrelation: Foreign Currency FuturesDocument14 pagesHedging Effectiveness and Minimum Risk Hedge Ratios in The Presence of Autocorrelation: Foreign Currency FuturesWijdan Saleem EdwanNo ratings yet

- Regceba GoogleformDocument1 pageRegceba GoogleformWijdan Saleem EdwanNo ratings yet

- ورقة ثالثة محاسبة 2013-2012-2011-2009Document51 pagesورقة ثالثة محاسبة 2013-2012-2011-2009Wijdan Saleem EdwanNo ratings yet

- Conceptual Framework for Financial ReportingDocument35 pagesConceptual Framework for Financial ReportingWijdan Saleem EdwanNo ratings yet

- Final SettlementDocument1 pageFinal SettlementWijdan Saleem EdwanNo ratings yet

- Introduction To Entrepreneurship StrategyDocument6 pagesIntroduction To Entrepreneurship StrategyWijdan Saleem EdwanNo ratings yet

- Financial analysis toolsDocument21 pagesFinancial analysis toolsWijdan Saleem EdwanNo ratings yet

- BAAC4206 CH 3 Income Tax UKDocument35 pagesBAAC4206 CH 3 Income Tax UKWijdan Saleem EdwanNo ratings yet

- BAAC4204 CH 1 - Accounting Concepts and ConventionsDocument25 pagesBAAC4204 CH 1 - Accounting Concepts and ConventionsWijdan Saleem EdwanNo ratings yet

- Conceptual Framework - Chapter 2Document42 pagesConceptual Framework - Chapter 2Wijdan Saleem EdwanNo ratings yet

- Direct Tax Law and Practice Book 04102019 PDFDocument610 pagesDirect Tax Law and Practice Book 04102019 PDFkilop omarNo ratings yet

- BAAC4206 CH 4 Employement IncomeDocument43 pagesBAAC4206 CH 4 Employement IncomeWijdan Saleem EdwanNo ratings yet

- Data Analytics For Decision MakingDocument15 pagesData Analytics For Decision MakingWijdan Saleem EdwanNo ratings yet

- BAAC4206 CH 1 Introduction To TaxationDocument30 pagesBAAC4206 CH 1 Introduction To TaxationWijdan Saleem EdwanNo ratings yet

- Data-Analytics-Using-Excel Certificate of Achievement PDFDocument2 pagesData-Analytics-Using-Excel Certificate of Achievement PDFWijdan Saleem EdwanNo ratings yet

- BAMA 1101, CH1, Ratio and ProportionDocument31 pagesBAMA 1101, CH1, Ratio and ProportionWijdan Saleem EdwanNo ratings yet

- BAMA 1101, CH1, Ratio and ProportionDocument31 pagesBAMA 1101, CH1, Ratio and ProportionWijdan Saleem EdwanNo ratings yet

- SEC Form 20-Is Definitive - 2015 - 0Document263 pagesSEC Form 20-Is Definitive - 2015 - 0Aeron Paul AntonioNo ratings yet

- ExercisesDocument3 pagesExercisesrhumblineNo ratings yet

- Ans: AnsDocument7 pagesAns: AnsRomelie M. NopreNo ratings yet

- Cfas Midterms q1Document3 pagesCfas Midterms q1Rommel Royce CadapanNo ratings yet

- Detailed Bank Statement SummaryDocument2 pagesDetailed Bank Statement SummaryAjay Chowdary Ajay ChowdaryNo ratings yet

- Working Capital of Coca ColaDocument3 pagesWorking Capital of Coca ColaSagor Aftermath0% (1)

- Condonation or RemissionDocument6 pagesCondonation or RemissionRhon Mhiel RomanoNo ratings yet

- JhunjhunwalaDocument12 pagesJhunjhunwalapercysearchNo ratings yet

- Assignment#2Document10 pagesAssignment#2hae1234No ratings yet

- Profile of DirectorsDocument5 pagesProfile of DirectorsSho NaNo ratings yet

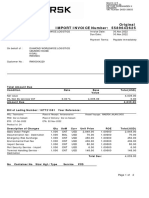

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- Bibf Course Catalogue 2012 PDFDocument370 pagesBibf Course Catalogue 2012 PDFImad Mkanna100% (1)

- Cost Dynamics - Elements and ClassificationDocument4 pagesCost Dynamics - Elements and ClassificationBrian OmbatiNo ratings yet

- Priyank ST03Document2 pagesPriyank ST03pkNo ratings yet

- Feasibility Analysis Offtake CANDI From The UMBULAN Drinking Water Supply SystemDocument7 pagesFeasibility Analysis Offtake CANDI From The UMBULAN Drinking Water Supply SystemInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Nationalisation of Banks in IndiaDocument5 pagesNationalisation of Banks in IndiaPravish Lionel DcostaNo ratings yet

- Unit 1 Portfolio Activity Review of Key Financial StatementsDocument4 pagesUnit 1 Portfolio Activity Review of Key Financial StatementsSimran PannuNo ratings yet

- Case Solution - A New Financial Policy at Swedish Match - ANIDocument20 pagesCase Solution - A New Financial Policy at Swedish Match - ANIAnisha Goyal33% (3)

- LatinFocus Consensus Forecast - February 2020Document142 pagesLatinFocus Consensus Forecast - February 2020Felipe OrnellesNo ratings yet

- Summer Training Project Report Derivatives in The Stock MarketDocument42 pagesSummer Training Project Report Derivatives in The Stock Marketprashant purohitNo ratings yet

- Faculty of Commerace: I YearDocument23 pagesFaculty of Commerace: I YearKaran Veer SinghNo ratings yet

- DocxDocument5 pagesDocxLorraine Mae Robrido100% (2)

- O.P.C.F 16 Suspension of CoverageDocument1 pageO.P.C.F 16 Suspension of CoverageGarry sharmaNo ratings yet

- Remote Deposit CaptureDocument60 pagesRemote Deposit Capture4701sandNo ratings yet

- Fees 2018 - The HillsDocument1 pageFees 2018 - The Hillsvelaphi_nhlapo2936No ratings yet

- Judicial study examines English mortgage systemDocument22 pagesJudicial study examines English mortgage systemSiddhant makhlogaNo ratings yet

- STMNT 112013 9773Document3 pagesSTMNT 112013 9773redbird77100% (1)

- Chapter 1 Solutions 1Document9 pagesChapter 1 Solutions 1yebegashetNo ratings yet

- Customer Satisfaction towards RTGS & NEFTDocument70 pagesCustomer Satisfaction towards RTGS & NEFTRajibKumar100% (1)