You might also like

- Assignment 1Document25 pagesAssignment 1Judy ZhangNo ratings yet

- Objection HandlingDocument3 pagesObjection HandlingNabin GaraiNo ratings yet

- Business Continuity Management (BCM) WorkshopDocument48 pagesBusiness Continuity Management (BCM) WorkshopJOSE ACOSTANo ratings yet

- XZT-Quadzilla InstallDocument2 pagesXZT-Quadzilla InstallAfzal Imam0% (1)

- Acquisition of Assets and Liabilities:: Problem IDocument17 pagesAcquisition of Assets and Liabilities:: Problem IklairvaughnNo ratings yet

- Advanced Accounting Part 2 Dayag 2015 Chapter 14Document29 pagesAdvanced Accounting Part 2 Dayag 2015 Chapter 14jayson100% (2)

- Entry Made Correct/Should Be EntryDocument15 pagesEntry Made Correct/Should Be EntryLove FreddyNo ratings yet

- Buscom Problems 2 4Document5 pagesBuscom Problems 2 4De Jesus, Tracy Marie L.No ratings yet

- Bus. Combi Probs and SolnDocument3 pagesBus. Combi Probs and SolnRyan Prado AndayaNo ratings yet

- Problem 2 1. Goodwill: Books of AcquirerDocument2 pagesProblem 2 1. Goodwill: Books of AcquirerNikki Coleen SantinNo ratings yet

- Bargain Purchase Gain/ Gain On Acquisition: Books of AcquirerDocument2 pagesBargain Purchase Gain/ Gain On Acquisition: Books of AcquirerNikki Coleen SantinNo ratings yet

- Business Combination MergerDocument108 pagesBusiness Combination Mergergojo satoruNo ratings yet

- Module 1 Comprehensive - MergerDocument5 pagesModule 1 Comprehensive - MergerGenevieve Manalo100% (6)

- 1SolMan ProblemsDocument17 pages1SolMan ProblemsBianca AcoymoNo ratings yet

- ACFrOgCXlqyBubUO 0k2 oqedP7h-nBYz6kyTwIOUtsM8YzGP85yKUDWiFtg8sxBlV4Hw82Zrv8Ha9zgsOOJOU6tLz838EivSxvzOqilLjimAlle6rnKpoa8Bur97ErTWtcl mZnrslLoC3IU KDocument2 pagesACFrOgCXlqyBubUO 0k2 oqedP7h-nBYz6kyTwIOUtsM8YzGP85yKUDWiFtg8sxBlV4Hw82Zrv8Ha9zgsOOJOU6tLz838EivSxvzOqilLjimAlle6rnKpoa8Bur97ErTWtcl mZnrslLoC3IU KStefanie Jane Royo PabalinasNo ratings yet

- Multiple Choice ProblemsDocument17 pagesMultiple Choice ProblemsDieter LudwigNo ratings yet

- Advacc Buscom Prob IVDocument2 pagesAdvacc Buscom Prob IVEdward James SantiagoNo ratings yet

- Post-Combination Balance Sheet: (Requirement 1) : Total Liabilities and Stockholder'S EquityDocument2 pagesPost-Combination Balance Sheet: (Requirement 1) : Total Liabilities and Stockholder'S Equityjayjay storageNo ratings yet

- SolutionChapter1RevFinal EditedDocument25 pagesSolutionChapter1RevFinal EditedkimberlyroseabianNo ratings yet

- Advacc Buscom Prob IIIDocument3 pagesAdvacc Buscom Prob IIIEdward James SantiagoNo ratings yet

- Solution Chapter 14Document26 pagesSolution Chapter 14grace guiuanNo ratings yet

- Chapter 1 - Multiple Choice Problem Answers AfarDocument13 pagesChapter 1 - Multiple Choice Problem Answers AfarChincel G. ANINo ratings yet

- P1-43 Comprehensive Business Combination ProblemDocument3 pagesP1-43 Comprehensive Business Combination ProblemkathNo ratings yet

- Business CombinationDocument3 pagesBusiness CombinationkathNo ratings yet

- P1-43 Comprehensive Business Combination ProblemDocument3 pagesP1-43 Comprehensive Business Combination ProblemkathNo ratings yet

- Activity 1. Partnership Formation Books of Roces: Bryle Jay P. Lape BSA-IIIDocument5 pagesActivity 1. Partnership Formation Books of Roces: Bryle Jay P. Lape BSA-IIIBryle Jay Lape40% (5)

- Accounting For Business Combi SolutionDocument4 pagesAccounting For Business Combi SolutionSophia Anne Margarette NicolasNo ratings yet

- PROBLEM 1: Goodwill and Barain Purchase Option Requirement 1Document2 pagesPROBLEM 1: Goodwill and Barain Purchase Option Requirement 1PrincessNo ratings yet

- Answer To Sample Question 2Document3 pagesAnswer To Sample Question 2Farid AbbasovNo ratings yet

- Pembahasan Genap ACT Genap 2020 19 MarDocument12 pagesPembahasan Genap ACT Genap 2020 19 MarSoca NarendraNo ratings yet

- Balance SheetDocument1 pageBalance SheetStefanie Jane Royo PabalinasNo ratings yet

- ACC203 - AssignmentDocument2 pagesACC203 - AssignmentHailsey WinterNo ratings yet

- Problem 1 San Pedro: AssetsDocument9 pagesProblem 1 San Pedro: AssetsGastelyn JacintoNo ratings yet

- Bsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyDocument7 pagesBsa Midterm Non Graded Exercises Worksheet and Financial Statements Preparation Answer KeyGarp BarrocaNo ratings yet

- Allan & WallyDocument10 pagesAllan & WallyLaura OliviaNo ratings yet

- Requirement: A New Set of Books Will Be Opened by The Partnership Roces' Books Sales' BooksDocument7 pagesRequirement: A New Set of Books Will Be Opened by The Partnership Roces' Books Sales' BooksJunzen Ralph YapNo ratings yet

- Financial StatementsDocument1 pageFinancial StatementsjaphethadadNo ratings yet

- Final Accounts Example - MBA WPDocument6 pagesFinal Accounts Example - MBA WPJIJONo ratings yet

- Acctg 601Document2 pagesAcctg 601Maria Regina Javier100% (1)

- Ans 31 To 41Document2 pagesAns 31 To 41Mallet S. GacadNo ratings yet

- CFAB Chapter12 Full GuidanceDocument74 pagesCFAB Chapter12 Full GuidanceNgân Lê Trần BảoNo ratings yet

- Sample ProblemDocument4 pagesSample ProblemENIDNo ratings yet

- ACC106 Assignment AccountDocument5 pagesACC106 Assignment AccountsyafiqahNo ratings yet

- Assignment Ans KeyDocument8 pagesAssignment Ans KeyJay Mark Marcial JosolNo ratings yet

- Transactions: Balance Sheet Income StatementDocument5 pagesTransactions: Balance Sheet Income StatementKothari InvestmentsNo ratings yet

- CHAPTER 6 - Joint VentureDocument10 pagesCHAPTER 6 - Joint VentureminmenmNo ratings yet

- Steps in Consolidation Working Papers On The Date of AcquisitionDocument3 pagesSteps in Consolidation Working Papers On The Date of AcquisitionPinky DaisiesNo ratings yet

- Activity Review StatementDocument5 pagesActivity Review Statementangel ciiiNo ratings yet

- Cfas Problem 8 1 PDFDocument3 pagesCfas Problem 8 1 PDFAzuh Shi0% (1)

- Hyper Star Traders Income Statement As of Dec 31, 2009: Net SalesDocument6 pagesHyper Star Traders Income Statement As of Dec 31, 2009: Net SalesomairpkNo ratings yet

- This Study Resource Was: Balance Sheet - ProblemsDocument3 pagesThis Study Resource Was: Balance Sheet - Problemsvenice cambryNo ratings yet

- Lecture Discussion On Worksheet Preparation To Post Closing Trial Balance November 092020Document18 pagesLecture Discussion On Worksheet Preparation To Post Closing Trial Balance November 092020Garp BarrocaNo ratings yet

- Yohannes Wibowo - Akuntansi Keuangan Lanjutan I - Akuntansi (E) - Tugas Minggu 5Document5 pagesYohannes Wibowo - Akuntansi Keuangan Lanjutan I - Akuntansi (E) - Tugas Minggu 5YOHANNES WIBOWONo ratings yet

- Problem 2.3.Document4 pagesProblem 2.3.ArtisanNo ratings yet

- ABUSCOM Lecture 14Document3 pagesABUSCOM Lecture 14Mark Lyndon YmataNo ratings yet

- Test Bank 3 - Ia 3Document25 pagesTest Bank 3 - Ia 3jessaNo ratings yet

- Consolidated Financial Statement Excercise 3-4Document2 pagesConsolidated Financial Statement Excercise 3-4Winnie TanNo ratings yet

- Quiz 3 Acctg For Business Combination - EntriesDocument6 pagesQuiz 3 Acctg For Business Combination - EntriesNhicoleChoiNo ratings yet

- 17 - Accounting For Incomplete Records (Single Entry)Document7 pages17 - Accounting For Incomplete Records (Single Entry)KAMAL POKHRELNo ratings yet

- Partnership FormationDocument5 pagesPartnership FormationIce Voltaire Buban GuiangNo ratings yet

- Note 5: PPE: Acc. Dep. Book Value Acquisition CostDocument5 pagesNote 5: PPE: Acc. Dep. Book Value Acquisition CostSabel LagoNo ratings yet

- b1Document29 pagesb1misonim.eNo ratings yet

- Final Preboard Examination On Auditing Problems Suggested Answers/solutionsDocument8 pagesFinal Preboard Examination On Auditing Problems Suggested Answers/solutionsLoren Lordwell MoyaniNo ratings yet

- Tax RemediesDocument11 pagesTax Remediesmisonim.eNo ratings yet

- 2023.02.01 Lecture - Audit of Expenditure and Disbursement Cycle - AnswersDocument1 page2023.02.01 Lecture - Audit of Expenditure and Disbursement Cycle - Answersmisonim.eNo ratings yet

- 2023.05.10 Exercise - Audit of Financing Cycle 2 With Answers-1Document3 pages2023.05.10 Exercise - Audit of Financing Cycle 2 With Answers-1misonim.eNo ratings yet

- Chapter7 ReviewerDocument23 pagesChapter7 Reviewermisonim.eNo ratings yet

- Taxation On IndividualsDocument20 pagesTaxation On Individualsmisonim.eNo ratings yet

- MASDocument119 pagesMASmisonim.eNo ratings yet

- TAXDocument128 pagesTAXmisonim.eNo ratings yet

- Batas Pambansa Blg. 22-Check and Bouncing LawDocument2 pagesBatas Pambansa Blg. 22-Check and Bouncing LawRocky MarcianoNo ratings yet

- RFBTDocument206 pagesRFBTmisonim.eNo ratings yet

- Sample Working Papers-1Document11 pagesSample Working Papers-1misonim.eNo ratings yet

- Far AudDocument191 pagesFar Audmisonim.eNo ratings yet

- Taxation Notes by Angelo MonforteDocument32 pagesTaxation Notes by Angelo Monfortemisonim.eNo ratings yet

- AFAR B41 First Pre-Board Exams (Questions, Answers & Solutions) .Document24 pagesAFAR B41 First Pre-Board Exams (Questions, Answers & Solutions) .Prances ObiasNo ratings yet

- FAR ProblemDocument4 pagesFAR Problemmisonim.eNo ratings yet

- FOREX Part3Document2 pagesFOREX Part3misonim.eNo ratings yet

- FOREX Part2Document9 pagesFOREX Part2misonim.eNo ratings yet

- New Chat-MergedDocument10 pagesNew Chat-Mergedmisonim.eNo ratings yet

- FOREX Lecture-MergedDocument31 pagesFOREX Lecture-Mergedmisonim.eNo ratings yet

- SAMPLE PROBLEMS (Stock Acquisition - Subsequent To The DOA)Document14 pagesSAMPLE PROBLEMS (Stock Acquisition - Subsequent To The DOA)misonim.eNo ratings yet

- AFARDocument107 pagesAFARmisonim.eNo ratings yet

- Translation of Foreign Financial Statements (IAS 21)Document6 pagesTranslation of Foreign Financial Statements (IAS 21)misonim.eNo ratings yet

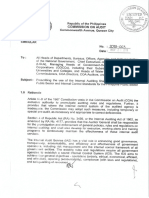

- COA - C2018 003 MergedDocument52 pagesCOA - C2018 003 Mergedmisonim.eNo ratings yet

- (Solved) Clap Off Manufacturing Uses 1,150 Switch Assemblies Per Week And... - Course HeroDocument3 pages(Solved) Clap Off Manufacturing Uses 1,150 Switch Assemblies Per Week And... - Course Heromisonim.eNo ratings yet

- (Solved) INVENTORY MODEL - ECONOMIC ORDER QUANTITY 1. Shirley Company... - Course HeroDocument5 pages(Solved) INVENTORY MODEL - ECONOMIC ORDER QUANTITY 1. Shirley Company... - Course Heromisonim.eNo ratings yet

- (Solved) in Fiscal Year 2017 2017, Wal-Mart Stores (WMT) Had... - Course HeroDocument3 pages(Solved) in Fiscal Year 2017 2017, Wal-Mart Stores (WMT) Had... - Course Heromisonim.eNo ratings yet

- (Solved) INVENTORY MODEL - ECONOMIC ORDER QUANTITY 1. Shirley Company... - Course HeroDocument5 pages(Solved) INVENTORY MODEL - ECONOMIC ORDER QUANTITY 1. Shirley Company... - Course Heromisonim.eNo ratings yet

- Theories in Taxation MNDocument2 pagesTheories in Taxation MNGrant Kenneth FloresNo ratings yet

- Chevron OEDocument9 pagesChevron OESundar Kumar Vasantha GovindarajuluNo ratings yet

- Mba-Working Capital ManagementDocument95 pagesMba-Working Capital Managementnet6351100% (2)

- C6-Intercompany Inventory Transactions PDFDocument43 pagesC6-Intercompany Inventory Transactions PDFVico JulendiNo ratings yet

- Abolition of ManualsDocument5 pagesAbolition of ManualsJf LarongNo ratings yet

- Artiga Police Nov21 To Nov 22Document2 pagesArtiga Police Nov21 To Nov 22Hakimi StationeryNo ratings yet

- Thakur Institute of Management Studies and ResearchDocument19 pagesThakur Institute of Management Studies and ResearchKaran PanchalNo ratings yet

- Services, Training, Delivery Equipment Right To Trade NameDocument6 pagesServices, Training, Delivery Equipment Right To Trade Namecram colasitoNo ratings yet

- Lecture 18 Ee Esdm 2109 Tnb.Document19 pagesLecture 18 Ee Esdm 2109 Tnb.ayonpakistanNo ratings yet

- Cisco Case StudyDocument2 pagesCisco Case StudytanushaNo ratings yet

- History of Credit RatingDocument3 pagesHistory of Credit RatingAzhar KhanNo ratings yet

- Asset Class 150% DDB 200% DDB SL SYD Depreciation MethodDocument4 pagesAsset Class 150% DDB 200% DDB SL SYD Depreciation MethodSepto PrabowoNo ratings yet

- 2 - House Property Problems 22-23Document5 pages2 - House Property Problems 22-2320-UCO-517 AJAY KELVIN ANo ratings yet

- PRNCaseStudiesBook PDFDocument21 pagesPRNCaseStudiesBook PDFDiana Teodora ȘtefanoviciNo ratings yet

- Richa Arora: Education ExperienceDocument1 pageRicha Arora: Education Experiencekajol guptaNo ratings yet

- Corporate Finance-Lecture 10Document11 pagesCorporate Finance-Lecture 10Sadia AbidNo ratings yet

- Slide Isb 540Document14 pagesSlide Isb 540Syamil Hakim Abdul GhaniNo ratings yet

- Audit ClauseDocument3 pagesAudit ClauseSonica DhankharNo ratings yet

- HSBC Project Report DRAFT1Document94 pagesHSBC Project Report DRAFT1hikvNo ratings yet

- AFL 1 Marketing Strategy Matthew Clement 0106021910041Document4 pagesAFL 1 Marketing Strategy Matthew Clement 0106021910041Matthew ClementNo ratings yet

- 01.13 ClearingDocument38 pages01.13 Clearingmevrick_guy0% (1)

- BSBMGT803 Finance AssignmentDocument16 pagesBSBMGT803 Finance AssignmentMuhammad MubeenNo ratings yet

- Oriental Engineering Works PVTDocument20 pagesOriental Engineering Works PVTDarshan DhimanNo ratings yet

- Management Accounting Set 3 Rearranged PDFDocument12 pagesManagement Accounting Set 3 Rearranged PDFshaazNo ratings yet

- Nepal Investment Bank Limited-BackgroundDocument3 pagesNepal Investment Bank Limited-BackgroundPrabin Bikram Shahi ThakuriNo ratings yet

- EXW FCA CPT CIP: Rules Governing The Transfer of Costs and Risks Between Seller and Buyer in International TradeDocument2 pagesEXW FCA CPT CIP: Rules Governing The Transfer of Costs and Risks Between Seller and Buyer in International TradenanaNo ratings yet

- IATF 16949 Types of AuditsDocument32 pagesIATF 16949 Types of AuditsJohn OoNo ratings yet

- Small Business Loans: A Practical Guide To Business CreditDocument15 pagesSmall Business Loans: A Practical Guide To Business CreditwilllNo ratings yet