You might also like

- Project On Mutual Fund Akhilesh MishraDocument142 pagesProject On Mutual Fund Akhilesh Mishramishra.akhilesh459737983% (262)

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- FIN1000 Module06 Forecasting AssignmentDocument4 pagesFIN1000 Module06 Forecasting AssignmentfaithNo ratings yet

- Topic 6 Debt Policyv2Document65 pagesTopic 6 Debt Policyv2Бота ОмароваNo ratings yet

- Week 1 Introduction and Capital Structure in A Perfect MarketDocument12 pagesWeek 1 Introduction and Capital Structure in A Perfect MarketAndrew NguyenNo ratings yet

- Lecture 11Document51 pagesLecture 11Janice JingNo ratings yet

- Introduction To Project Valuation: Dr. Jeanine BaumertDocument79 pagesIntroduction To Project Valuation: Dr. Jeanine BaumertJosh GirnunNo ratings yet

- Capital StructureDocument44 pagesCapital Structureeliasjade2No ratings yet

- Week 5 LectureDocument48 pagesWeek 5 LectureДмитрий КолесниковNo ratings yet

- FINANCIAL LEVERAGE AND CAPITAL STRUCTUREDocument37 pagesFINANCIAL LEVERAGE AND CAPITAL STRUCTUREMALIK WASEEM JANNo ratings yet

- Cost of CapitalDocument15 pagesCost of CapitalCyrine JemaaNo ratings yet

- Optimal Capital Structure and Cost of CapitalDocument16 pagesOptimal Capital Structure and Cost of CapitalYariko ChieNo ratings yet

- M09 Gitman50803X 14 MF C09Document56 pagesM09 Gitman50803X 14 MF C09dhfbbbbbbbbbbbbbbbbbhNo ratings yet

- CF 7Document32 pagesCF 7Umair MughalNo ratings yet

- FIN 319 - Lecture 06Document30 pagesFIN 319 - Lecture 06Trà MyNo ratings yet

- Capital Structure TheoriesDocument38 pagesCapital Structure TheoriesNeha SoodNo ratings yet

- Hospital Corporation Of America Maintains A RatingDocument16 pagesHospital Corporation Of America Maintains A RatingDhruv Kalia50% (2)

- Capital Structure and Cost of CapitalDocument6 pagesCapital Structure and Cost of CapitalSam DevineNo ratings yet

- Banking Interviews Guide-2Document4 pagesBanking Interviews Guide-2SAKSHAM SINGHNo ratings yet

- Corporate Financial Policy OverviewDocument39 pagesCorporate Financial Policy OverviewVasco Laranjo100% (1)

- Chapter 17 Limits To The Use of DebtDocument25 pagesChapter 17 Limits To The Use of DebtFahmi Ahmad FarizanNo ratings yet

- FINANCIAL POLICY LECTUREDocument88 pagesFINANCIAL POLICY LECTUREYuhan KENo ratings yet

- Finance Decisions ExplainedDocument70 pagesFinance Decisions ExplainedFara HameedNo ratings yet

- Insert image: Financing overseas investment and MNC cost of capitalDocument16 pagesInsert image: Financing overseas investment and MNC cost of capitalCenith CheeNo ratings yet

- Capital Structure (I) : Professor Siyi ShenDocument18 pagesCapital Structure (I) : Professor Siyi ShenjamesNo ratings yet

- Capital Structure in Perfect MarketsDocument48 pagesCapital Structure in Perfect MarketsCecile KotzeNo ratings yet

- Limits To The Use of DebtDocument40 pagesLimits To The Use of DebtMasumNo ratings yet

- The Cost of Capital: Fourth EditionDocument39 pagesThe Cost of Capital: Fourth EditionNatasya FlorenciaNo ratings yet

- Capital Structure and Corporate StrategyDocument23 pagesCapital Structure and Corporate StrategyelyosedoNo ratings yet

- CF-II Session 3hDocument22 pagesCF-II Session 3hfew.fearlessNo ratings yet

- Financial Management: IBA, Main CampusDocument69 pagesFinancial Management: IBA, Main CampusumarNo ratings yet

- CF_Chapter 17(1)Document25 pagesCF_Chapter 17(1)huanbilly2003No ratings yet

- Chapter 9 Cost of CapitalDocument39 pagesChapter 9 Cost of CapitalPapa ZolaNo ratings yet

- Financial Distress, Managerial Incentives, and InformationDocument36 pagesFinancial Distress, Managerial Incentives, and InformationPoc TimeNo ratings yet

- Cost of Capital AnalysisDocument40 pagesCost of Capital AnalysisAbdul GhaniNo ratings yet

- Principles of Finance - Capital StructureDocument50 pagesPrinciples of Finance - Capital StructureDaniyal UsmanNo ratings yet

- Session1 2020Document47 pagesSession1 2020Nitya GuptaNo ratings yet

- Financial Management Capital StructureDocument80 pagesFinancial Management Capital StructureFarzad Touhid100% (1)

- YH - Session5 - Capital StructureDocument11 pagesYH - Session5 - Capital Structureevan.y.baiNo ratings yet

- CFM - Lecture 1 - Capital Structure TheoryDocument116 pagesCFM - Lecture 1 - Capital Structure TheoryJelien TaselaarNo ratings yet

- MFCF - Session 5Document49 pagesMFCF - Session 5Ondřej HengeričNo ratings yet

- Valuation and Capital Budgeting For The Levered Firm: Chapter OpenerDocument7 pagesValuation and Capital Budgeting For The Levered Firm: Chapter OpenerChaituNo ratings yet

- Lecture 4Document21 pagesLecture 4Jie Yi LimNo ratings yet

- 7SOGSS FM LECTURE 7 Sources of Finance 1Document60 pages7SOGSS FM LECTURE 7 Sources of Finance 1Right Karl-Maccoy HattohNo ratings yet

- Capital Structure Trade-off Theory Session IVDocument24 pagesCapital Structure Trade-off Theory Session IVAshutosh KumarNo ratings yet

- Ch16 Financial Distress, Managerial Incentives, and InformationDocument46 pagesCh16 Financial Distress, Managerial Incentives, and Informationzey9991No ratings yet

- FIN5342PS1Document3 pagesFIN5342PS1Samantha Hwey Min Ding100% (1)

- 4 Corporate Finance QuestionsDocument65 pages4 Corporate Finance QuestionsAishwarya BansalNo ratings yet

- Fin 311 Weighted Average Cost of CapitalDocument48 pagesFin 311 Weighted Average Cost of CapitalsenaNo ratings yet

- FM Ch7 Corporate FinancingDocument60 pagesFM Ch7 Corporate Financingtemesgen yohannesNo ratings yet

- MAS Handout - Risk and Returns, Cost of Capital, Capital Structure and Leverage PDFDocument5 pagesMAS Handout - Risk and Returns, Cost of Capital, Capital Structure and Leverage PDFDivine VictoriaNo ratings yet

- Session 20Document9 pagesSession 20Alba MoralesNo ratings yet

- Cost of CapitalDocument46 pagesCost of CapitalMazen SalahNo ratings yet

- Multinational Cost of Capital & Capital StructureDocument38 pagesMultinational Cost of Capital & Capital Structurenivedita_h42404No ratings yet

- Cost of CapitalDocument53 pagesCost of CapitalJaodat Mand KhanNo ratings yet

- R R D DE R E DE R R R D DE: Modigliani-Miller TheoremDocument13 pagesR R D DE R E DE R R R D DE: Modigliani-Miller TheoremPankaj Kumar BaidNo ratings yet

- Cost of Capital: © 2019 Mcgraw-Hill Education Limited. All Rights ReservedDocument43 pagesCost of Capital: © 2019 Mcgraw-Hill Education Limited. All Rights Reservedbusiness docNo ratings yet

- Amity School of Business: BBA Semister Four Financial Management-II Ashish Samarpit NoelDocument28 pagesAmity School of Business: BBA Semister Four Financial Management-II Ashish Samarpit NoelKaran MalikNo ratings yet

- MM& Agency ProbalemDocument43 pagesMM& Agency Probalemmaheswara448No ratings yet

- Fin 440 - Chapter - 16Document14 pagesFin 440 - Chapter - 16Mehedi HasanNo ratings yet

- Summary of Heather Brilliant & Elizabeth Collins's Why Moats MatterFrom EverandSummary of Heather Brilliant & Elizabeth Collins's Why Moats MatterNo ratings yet

- Ch13 Investor Behavior & Market EfficiencyDocument47 pagesCh13 Investor Behavior & Market Efficiencyzey9991No ratings yet

- Ch7 Investment Decision RulesDocument24 pagesCh7 Investment Decision Ruleszey9991No ratings yet

- Ch5 Interest RatesDocument25 pagesCh5 Interest Rateszey9991No ratings yet

- Ch9 Valuing StocksDocument65 pagesCh9 Valuing Stockszey9991No ratings yet

- Ch3 Financial Decision MakingDocument49 pagesCh3 Financial Decision Makingzey9991No ratings yet

- Ch11 Optimal Portfolio Choice & The CAPMDocument66 pagesCh11 Optimal Portfolio Choice & The CAPMzey9991No ratings yet

- Assignment 1 WorksheetDocument1 pageAssignment 1 Worksheetgolemwitch01No ratings yet

- ACT 132 Lecture 2Document69 pagesACT 132 Lecture 2Muadz D. LucmanNo ratings yet

- Case Unidentified IndustryDocument3 pagesCase Unidentified IndustryChristopher NindyoNo ratings yet

- Convertible Bonds Yield SingaporeDocument18 pagesConvertible Bonds Yield Singaporeapi-26109152No ratings yet

- Docs in A Box, Inc.Document6 pagesDocs in A Box, Inc.Leonardo D NinoNo ratings yet

- RBI urged to release 35% of deposits from Malkapur Urban Co-op BankDocument19 pagesRBI urged to release 35% of deposits from Malkapur Urban Co-op BankSamyak DahaleNo ratings yet

- Nifty 100 Quality 30Document4 pagesNifty 100 Quality 30Suhas SalehittalNo ratings yet

- CapstructDocument17 pagesCapstructPushpraj Singh BaghelNo ratings yet

- Balance SheetDocument25 pagesBalance SheetImran AhmedNo ratings yet

- Material Part IDocument64 pagesMaterial Part IKrishna AdhikariNo ratings yet

- CPAR TOA Pre-Board FinalDocument10 pagesCPAR TOA Pre-Board FinalJericho Pedragosa100% (1)

- GTU MBA 2018 3rd Semester Winter 2830201 Strategic Financial ManagementDocument4 pagesGTU MBA 2018 3rd Semester Winter 2830201 Strategic Financial ManagementAbhishek ChaturvediNo ratings yet

- Bloomberg 2014 MA Financial RankingsDocument38 pagesBloomberg 2014 MA Financial Rankingsed_nycNo ratings yet

- Free Cash Flow Introduction TrainingDocument130 pagesFree Cash Flow Introduction Trainingashrafhussein100% (5)

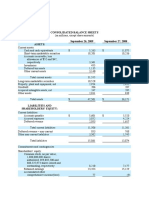

- Q12013 Consolidated Balance Sheet - Assets UKDocument1 pageQ12013 Consolidated Balance Sheet - Assets UKwellawalalasithNo ratings yet

- Data Analysis & Interpretation of Open Outcry SystemDocument41 pagesData Analysis & Interpretation of Open Outcry SystemMubeenNo ratings yet

- Valuation & Accounting of InventoryDocument21 pagesValuation & Accounting of InventoryPrasad BhanageNo ratings yet

- JFC.17C.Press Release On 2020 Audited Consolidated Finanacial Statement.04122021Document7 pagesJFC.17C.Press Release On 2020 Audited Consolidated Finanacial Statement.04122021JhenRMANo ratings yet

- ACCA F3 Financial Accounting INT Solved Past Papers 0107Document283 pagesACCA F3 Financial Accounting INT Solved Past Papers 0107Hasan Ali BokhariNo ratings yet

- Soal Week 3Document2 pagesSoal Week 3Muhammad Ananda PutraNo ratings yet

- OLABISI ONABANJO Cost Accounting Second Semester ExamDocument6 pagesOLABISI ONABANJO Cost Accounting Second Semester Examonaneye ayodejiNo ratings yet

- PAS 12 Accounting For Income TaxDocument17 pagesPAS 12 Accounting For Income TaxReynaldNo ratings yet

- CFD Tutorial Learn CFD Trading PDFDocument17 pagesCFD Tutorial Learn CFD Trading PDFZé RobertoNo ratings yet

- Negotiating The Term SheetDocument21 pagesNegotiating The Term SheetDaniel100% (6)

- Ramco WordDocument8 pagesRamco WordSomil GuptaNo ratings yet

- Financial Management - Chapter 9Document17 pagesFinancial Management - Chapter 9mechidreamNo ratings yet

- Managerial Accounting Quiz 2Document1 pageManagerial Accounting Quiz 2Raju SainiNo ratings yet

- Soal Latihan BVADocument35 pagesSoal Latihan BVAIkhsan Uiandra Putra SitorusNo ratings yet