You might also like

- Supriya Lifescience Concall-Q2FY23Document14 pagesSupriya Lifescience Concall-Q2FY23Vivek RamNo ratings yet

- Outbound Hiring: How Innovative Companies are Winning the Global War for TalentFrom EverandOutbound Hiring: How Innovative Companies are Winning the Global War for TalentNo ratings yet

- Earnings Call TranscriptDocument19 pagesEarnings Call TranscriptAniket SabaleNo ratings yet

- Pnjdent: Prudent Advisory Services LTDDocument20 pagesPnjdent: Prudent Advisory Services LTDDasari PrabodhNo ratings yet

- 2023-10-18-IIFS - NS-Refinitiv StreetEven-IIFS - NS - Event Transcript of IIFL Securities LTD Conference... - 104459586Document12 pages2023-10-18-IIFS - NS-Refinitiv StreetEven-IIFS - NS - Event Transcript of IIFL Securities LTD Conference... - 104459586Vinod TPNo ratings yet

- Concall Feb 22Document23 pagesConcall Feb 22dhrivsitlani29No ratings yet

- Maharashtra SeamlessDocument19 pagesMaharashtra SeamlessmisfitmedicoNo ratings yet

- Embassy Office Parks REIT LTDDocument23 pagesEmbassy Office Parks REIT LTDSandy SandyNo ratings yet

- 41129a99-de3e-4008-a328-78db2520feb0Document25 pages41129a99-de3e-4008-a328-78db2520feb0Palash TahasildarNo ratings yet

- Ref: SK/CHN/2022-23/E29 August 11, 2022Document18 pagesRef: SK/CHN/2022-23/E29 August 11, 2022ajoy sharmaNo ratings yet

- Rupesh Laxman JadhavDocument19 pagesRupesh Laxman JadhavCOD CALL OF DUTYNo ratings yet

- Mahindra: LogisticsDocument27 pagesMahindra: Logisticspramit008No ratings yet

- Meghmani Organics LTDDocument12 pagesMeghmani Organics LTDmisfitmedicoNo ratings yet

- Consumer Behaviour in Equity MarketDocument37 pagesConsumer Behaviour in Equity MarketVivek LagooNo ratings yet

- 1db56e523a9e/transcript Embassy Reit Earnings Call q4 Fy22 PDFDocument20 pages1db56e523a9e/transcript Embassy Reit Earnings Call q4 Fy22 PDFSandy SandyNo ratings yet

- Valiant Organics ET (Q4-FY 22)Document20 pagesValiant Organics ET (Q4-FY 22)beza manojNo ratings yet

- Persistent Concall Jan 2023Document34 pagesPersistent Concall Jan 2023Parth KariaNo ratings yet

- Reymond Meet ConcallDocument11 pagesReymond Meet Concallrajesh KumarNo ratings yet

- Karvy Project Report Chetan DaiyaDocument71 pagesKarvy Project Report Chetan Daiyadheeraj panwar50% (4)

- Sub: Transcript of Q1 Earnings Conference Call - FY 2022-23Document16 pagesSub: Transcript of Q1 Earnings Conference Call - FY 2022-23Dasari PrabodhNo ratings yet

- Fa4c8e7eacb8/embassy - Reit - Earnings - Call - q1 - Fy23 - W - Qa - PDF: TH THDocument20 pagesFa4c8e7eacb8/embassy - Reit - Earnings - Call - q1 - Fy23 - W - Qa - PDF: TH THSandy SandyNo ratings yet

- Intimation Regarding Call TranscriptDocument18 pagesIntimation Regarding Call TranscriptMan Mohan KalitaNo ratings yet

- MD - Jan 27'22Document22 pagesMD - Jan 27'22Vaishnavi SomaniNo ratings yet

- Oberoi Realty Annual Report 2017-18Document208 pagesOberoi Realty Annual Report 2017-18yashneet kaurNo ratings yet

- Raymonds LTDDocument18 pagesRaymonds LTDmisfitmedicoNo ratings yet

- Apeksha Baisakhi Ya: Online Filing atDocument19 pagesApeksha Baisakhi Ya: Online Filing atAbdul SamadNo ratings yet

- HEM - Saakshi Medtech 28 Nov 2023Document18 pagesHEM - Saakshi Medtech 28 Nov 2023prima donnaNo ratings yet

- Transcript Earning Call 08-09Q2Document32 pagesTranscript Earning Call 08-09Q2shwetaforeNo ratings yet

- AB Capital ConcallDocument22 pagesAB Capital ConcallHarsimran SinghNo ratings yet

- Dacec51dd208/embassy - Reit - Earnings - Call - q2 - Fy23 - Withqa - PDF: TH THDocument20 pagesDacec51dd208/embassy - Reit - Earnings - Call - q2 - Fy23 - Withqa - PDF: TH THSandy SandyNo ratings yet

- Share Market Karvey Stock Broking Ltd. Parul SrivastavaDocument68 pagesShare Market Karvey Stock Broking Ltd. Parul SrivastavaTahir HussainNo ratings yet

- Sunil Kumar JainDocument15 pagesSunil Kumar Jainsahil.goelNo ratings yet

- Ompal: Digitally Signed by Ompal Date: 2024.02.13 18:59:44 +05'30'Document16 pagesOmpal: Digitally Signed by Ompal Date: 2024.02.13 18:59:44 +05'30'Arjun BiswasNo ratings yet

- Fineotex C: HemicalDocument210 pagesFineotex C: Hemicalarnabdeb83No ratings yet

- Dixon Technologies (India) LTD.: Sub: Transcript of The Q4 FY 2022 Earnings Conference Call Held On May 30, 2022Document15 pagesDixon Technologies (India) LTD.: Sub: Transcript of The Q4 FY 2022 Earnings Conference Call Held On May 30, 2022pratheekNo ratings yet

- IndiaMART Concall Transcript Q1FY2020 1Document17 pagesIndiaMART Concall Transcript Q1FY2020 1Harsh GandhiNo ratings yet

- Sunil Kumar JainDocument15 pagesSunil Kumar Jainsahil.goelNo ratings yet

- D Mat Trading Account ProjectDocument76 pagesD Mat Trading Account ProjectAbhimanyu mishraNo ratings yet

- Dhiraj Aroraa: WWW - Maxhealthcare.in/ Investors/investor-ResourcesDocument16 pagesDhiraj Aroraa: WWW - Maxhealthcare.in/ Investors/investor-Resourcesdipyaman patgiriNo ratings yet

- Karvy ReportDocument51 pagesKarvy ReportAbhishek rajNo ratings yet

- TRAINING REPORT FINAL FinaDocument52 pagesTRAINING REPORT FINAL FinaNeuherbs InternNo ratings yet

- ST THDocument10 pagesST THJ&J ChannelNo ratings yet

- EarningsCallTranscript Q3FY24Document38 pagesEarningsCallTranscript Q3FY24vijay4victorNo ratings yet

- Scrip Code: 543272 Symbol: EASEMYTRIP Sub: Earning Call TranscriptDocument13 pagesScrip Code: 543272 Symbol: EASEMYTRIP Sub: Earning Call TranscriptmadristasareoneNo ratings yet

- Syngene Earnings Jan25 2024Document13 pagesSyngene Earnings Jan25 2024just7No ratings yet

- Concall May 22Document20 pagesConcall May 22dhrivsitlani29No ratings yet

- Submitted To: - Submitted By: - : Jiwaji University Gwalior (MP.) Bhoopendra Pathak M.B.A. (Iii Sem)Document44 pagesSubmitted To: - Submitted By: - : Jiwaji University Gwalior (MP.) Bhoopendra Pathak M.B.A. (Iii Sem)Janani BharathiNo ratings yet

- Laurus Concall Feb 2023Document18 pagesLaurus Concall Feb 2023Parth KariaNo ratings yet

- Seshan Uradha Chava: Sub: Letter To Shareholders For Quarter and Nine Months Ended December 31, 2022Document20 pagesSeshan Uradha Chava: Sub: Letter To Shareholders For Quarter and Nine Months Ended December 31, 2022Sree HarshaNo ratings yet

- Chitrangi Intership - RepotDocument41 pagesChitrangi Intership - RepotMonika guptaNo ratings yet

- Karvy LTDDocument52 pagesKarvy LTDvipul99solankiNo ratings yet

- Minuzee R Yazdi BamboatDocument12 pagesMinuzee R Yazdi BamboatArjun BiswasNo ratings yet

- Summer Training Report ON A Study On Commodities Future Trading AT Religare Commodities LTDDocument65 pagesSummer Training Report ON A Study On Commodities Future Trading AT Religare Commodities LTDkjrajdasNo ratings yet

- Aarti DrugsDocument45 pagesAarti Drugskrishna_buntyNo ratings yet

- Project of Entrepreneurship: Business Plan of A Start-UpDocument60 pagesProject of Entrepreneurship: Business Plan of A Start-UpMuhammad SaadNo ratings yet

- Transcript of Earnings Conference Call 01 August 2023Document24 pagesTranscript of Earnings Conference Call 01 August 2023Palash TahasildarNo ratings yet

- Comparative Analysis of Three Asset Management CompaniesDocument103 pagesComparative Analysis of Three Asset Management CompaniesNikhil Bhutada50% (4)

- Marico Transcript-1Document21 pagesMarico Transcript-1Manish PatraNo ratings yet

- Fineotex C: HemicalDocument210 pagesFineotex C: Hemicalarnabdeb83No ratings yet

- 519858Document24 pages519858arnabdeb83No ratings yet

- Steel LTD.: TubesDocument4 pagesSteel LTD.: Tubesarnabdeb83No ratings yet

- Rama Steel Tubes LTD.: Sub.: Outcome of Board Meeting Held On August 14.2023Document14 pagesRama Steel Tubes LTD.: Sub.: Outcome of Board Meeting Held On August 14.2023arnabdeb83No ratings yet

- PressreleaseQ2FY2023 Consolidated Performance OverviewDocument3 pagesPressreleaseQ2FY2023 Consolidated Performance Overviewarnabdeb83No ratings yet

- Chemicals Deep Dive 11 07 2023Document33 pagesChemicals Deep Dive 11 07 2023arnabdeb83No ratings yet

- Assertions Audit Objectives Audit Procedures: Audit of Intangible AssetsDocument12 pagesAssertions Audit Objectives Audit Procedures: Audit of Intangible AssetsUn knownNo ratings yet

- L' Pacioli Food Hub: Activity in TechnopreneurshipDocument9 pagesL' Pacioli Food Hub: Activity in Technopreneurshipfrancis dungca100% (1)

- Chapter 1 PartnershipsDocument46 pagesChapter 1 PartnershipsAkkamaNo ratings yet

- Ims-Alerts 9001 14001 OverviewDocument37 pagesIms-Alerts 9001 14001 Overviewnoyon debNo ratings yet

- What Is Project Portfolio Management? - Definition, Process & Tools - Video & Lesson TranscriptDocument4 pagesWhat Is Project Portfolio Management? - Definition, Process & Tools - Video & Lesson Transcriptshubham sharmaNo ratings yet

- Written ReportDocument2 pagesWritten ReportMary JaneNo ratings yet

- Abm 12 Marketing q1 Clas2 Relationship Marketing v1 - Rhea Ann NavillaDocument13 pagesAbm 12 Marketing q1 Clas2 Relationship Marketing v1 - Rhea Ann NavillaKim Yessamin MadarcosNo ratings yet

- Chapter 1Document47 pagesChapter 1honeyNo ratings yet

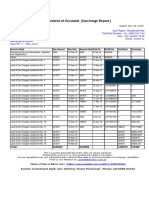

- Surcharge Report BTKSC-P05164Document1 pageSurcharge Report BTKSC-P05164Nasir Badshah AfridiNo ratings yet

- Ch15 SchedulingDocument20 pagesCh15 SchedulingFatemah Maher HegazyNo ratings yet

- Ner 65lc Nit 15sep15Document4 pagesNer 65lc Nit 15sep15vspuriNo ratings yet

- International Chamber of Commerce Non-Circumvention, Non-Disclosure & Working Agreement (Ncnda) Irrevocable Master Fee Protection Agreement (Imfpa)Document10 pagesInternational Chamber of Commerce Non-Circumvention, Non-Disclosure & Working Agreement (Ncnda) Irrevocable Master Fee Protection Agreement (Imfpa)Claudio PizzoNo ratings yet

- Tara Sanitary Wares & Tiles: QuotationDocument1 pageTara Sanitary Wares & Tiles: QuotationSyamlin LSNo ratings yet

- Rural Marketing: Assignment ofDocument8 pagesRural Marketing: Assignment ofNeha GoyalNo ratings yet

- Research Methodology and Business AnalyticsDocument27 pagesResearch Methodology and Business Analyticsamarnadh allaNo ratings yet

- What Is Maintenance?: The Objective of Plant MaintenanceDocument4 pagesWhat Is Maintenance?: The Objective of Plant MaintenanceabdullahNo ratings yet

- Control Accounts Worked ExamplesDocument2 pagesControl Accounts Worked ExamplesProto Proffesor TshumaNo ratings yet

- Research Notes and Commentaries Doing Well by Doing Good-Case Study: Fair & Lovely' Whitening CreamDocument7 pagesResearch Notes and Commentaries Doing Well by Doing Good-Case Study: Fair & Lovely' Whitening CreamMuqadas JavedNo ratings yet

- August 21 Listening 10Document2 pagesAugust 21 Listening 10Juan Andres Velez CalderónNo ratings yet

- Amul Vs Mother Diary - PDFDocument52 pagesAmul Vs Mother Diary - PDFrohit katkarNo ratings yet

- Supply C1 C4Document4 pagesSupply C1 C4shielamayavillanueva25No ratings yet

- Chapter 3Document3 pagesChapter 3Anonymous XybLZfNo ratings yet

- Coders Brain Company ProfileDocument11 pagesCoders Brain Company ProfileYoxajaNo ratings yet

- Final Esquisse Des 8 Mixed UseDocument5 pagesFinal Esquisse Des 8 Mixed Usecarlo melgarNo ratings yet

- Lot 01 Boq Utc Elgon CurrDocument445 pagesLot 01 Boq Utc Elgon CurrAnonymous qOBFvINo ratings yet

- BSBMKG555 Assessment 2Document33 pagesBSBMKG555 Assessment 2Bright Lazy100% (2)

- GlobalizationDocument4 pagesGlobalizationMark MorongeNo ratings yet

- Why Are Some Growth Poles More Successful Than OthersDocument4 pagesWhy Are Some Growth Poles More Successful Than OthersMarie POUSSEREAUNo ratings yet

- Project 요약Document36 pagesProject 요약sjcgraceNo ratings yet

- Invitational 2020 2ndDocument36 pagesInvitational 2020 2ndÁnh Thiện TriệuNo ratings yet

- Process Plant Equipment: Operation, Control, and ReliabilityFrom EverandProcess Plant Equipment: Operation, Control, and ReliabilityRating: 5 out of 5 stars5/5 (1)

- Physical and Chemical Equilibrium for Chemical EngineersFrom EverandPhysical and Chemical Equilibrium for Chemical EngineersRating: 5 out of 5 stars5/5 (1)

- The Periodic Table of Elements - Post-Transition Metals, Metalloids and Nonmetals | Children's Chemistry BookFrom EverandThe Periodic Table of Elements - Post-Transition Metals, Metalloids and Nonmetals | Children's Chemistry BookNo ratings yet

- Process Steam Systems: A Practical Guide for Operators, Maintainers, and DesignersFrom EverandProcess Steam Systems: A Practical Guide for Operators, Maintainers, and DesignersNo ratings yet

- Phase Equilibria in Chemical EngineeringFrom EverandPhase Equilibria in Chemical EngineeringRating: 4 out of 5 stars4/5 (11)

- Nuclear Energy in the 21st Century: World Nuclear University PressFrom EverandNuclear Energy in the 21st Century: World Nuclear University PressRating: 4.5 out of 5 stars4.5/5 (3)

- Gas-Liquid And Liquid-Liquid SeparatorsFrom EverandGas-Liquid And Liquid-Liquid SeparatorsRating: 3.5 out of 5 stars3.5/5 (3)

- The Periodic Table of Elements - Alkali Metals, Alkaline Earth Metals and Transition Metals | Children's Chemistry BookFrom EverandThe Periodic Table of Elements - Alkali Metals, Alkaline Earth Metals and Transition Metals | Children's Chemistry BookNo ratings yet

- Guidelines for Chemical Process Quantitative Risk AnalysisFrom EverandGuidelines for Chemical Process Quantitative Risk AnalysisRating: 5 out of 5 stars5/5 (1)

- Guidelines for the Management of Change for Process SafetyFrom EverandGuidelines for the Management of Change for Process SafetyNo ratings yet

- An Introduction to the Periodic Table of Elements : Chemistry Textbook Grade 8 | Children's Chemistry BooksFrom EverandAn Introduction to the Periodic Table of Elements : Chemistry Textbook Grade 8 | Children's Chemistry BooksRating: 5 out of 5 stars5/5 (1)

- Understanding Process Equipment for Operators and EngineersFrom EverandUnderstanding Process Equipment for Operators and EngineersRating: 4.5 out of 5 stars4.5/5 (3)

- Chemical Process Safety: Learning from Case HistoriesFrom EverandChemical Process Safety: Learning from Case HistoriesRating: 4 out of 5 stars4/5 (14)

- Piping and Pipeline Calculations Manual: Construction, Design Fabrication and ExaminationFrom EverandPiping and Pipeline Calculations Manual: Construction, Design Fabrication and ExaminationRating: 4 out of 5 stars4/5 (18)

- Pharmaceutical Blending and MixingFrom EverandPharmaceutical Blending and MixingP. J. CullenRating: 5 out of 5 stars5/5 (1)

- The HAZOP Leader's Handbook: How to Plan and Conduct Successful HAZOP StudiesFrom EverandThe HAZOP Leader's Handbook: How to Plan and Conduct Successful HAZOP StudiesNo ratings yet

- Guidelines for Engineering Design for Process SafetyFrom EverandGuidelines for Engineering Design for Process SafetyNo ratings yet

- Operational Excellence: Journey to Creating Sustainable ValueFrom EverandOperational Excellence: Journey to Creating Sustainable ValueNo ratings yet

- Well Control for Completions and InterventionsFrom EverandWell Control for Completions and InterventionsRating: 4 out of 5 stars4/5 (10)

- Functional Safety from Scratch: A Practical Guide to Process Industry ApplicationsFrom EverandFunctional Safety from Scratch: A Practical Guide to Process Industry ApplicationsNo ratings yet

- Lees' Process Safety Essentials: Hazard Identification, Assessment and ControlFrom EverandLees' Process Safety Essentials: Hazard Identification, Assessment and ControlRating: 4 out of 5 stars4/5 (4)

- Sodium Bicarbonate: Nature's Unique First Aid RemedyFrom EverandSodium Bicarbonate: Nature's Unique First Aid RemedyRating: 5 out of 5 stars5/5 (21)