You might also like

- Strawberry Tea SetDocument20 pagesStrawberry Tea Settobi maniaNo ratings yet

- EVMS Gold CardDocument1 pageEVMS Gold CardHaneefa ChNo ratings yet

- Sworn Statement of Assets, Liabilities and Net WorthDocument3 pagesSworn Statement of Assets, Liabilities and Net WorthMj GarciaNo ratings yet

- Gypsum Board Installation To Wall (Drywall & Partitions)Document5 pagesGypsum Board Installation To Wall (Drywall & Partitions)xomilaaNo ratings yet

- Capital StructureDocument65 pagesCapital StructurePunitharaja Nadaraja67% (3)

- Maste Storytelling Mark-J.-Carpenter - Darrell-DDocument182 pagesMaste Storytelling Mark-J.-Carpenter - Darrell-DmauriNo ratings yet

- State Ownership, Political Ideology and Firm PerformanceDocument18 pagesState Ownership, Political Ideology and Firm PerformanceHammad HussainNo ratings yet

- The Impact of Capital Structure On Firm Performance - Evidence From VietnamDocument9 pagesThe Impact of Capital Structure On Firm Performance - Evidence From VietnamSamah Omar KhanshiriNo ratings yet

- Sheikh 2015Document9 pagesSheikh 2015Zara ShoukatNo ratings yet

- Vol - 19 3 1Document15 pagesVol - 19 3 1Shafick GabungaNo ratings yet

- Accounting and Finance Review: Chermian EforisDocument7 pagesAccounting and Finance Review: Chermian Eforisghaziya hafizaNo ratings yet

- Role of Institutions in Shaping Corporate Governance System Evidence FromDocument17 pagesRole of Institutions in Shaping Corporate Governance System Evidence Fromkin primasNo ratings yet

- SSRN Id2634879Document24 pagesSSRN Id2634879Chandrika DasNo ratings yet

- Literature ReviewDocument9 pagesLiterature ReviewreksmanotiyaNo ratings yet

- Ownership Structure and Firm Performance: Evidence From Vietnamese Listed FirmsDocument36 pagesOwnership Structure and Firm Performance: Evidence From Vietnamese Listed Firmsnsrivastav1No ratings yet

- State Ownership and Firm Innovation in China: An Integrated View of Institutional and Efficiency LogicsDocument30 pagesState Ownership and Firm Innovation in China: An Integrated View of Institutional and Efficiency LogicsAshraf KhanNo ratings yet

- State Capitalism and Performance Persistence of Business Group-Affiliated Firms: A Comparative Study of China and IndiaDocument30 pagesState Capitalism and Performance Persistence of Business Group-Affiliated Firms: A Comparative Study of China and IndiamidmlcepeajaeargieNo ratings yet

- Board Characteristics, State Ownership and FirmDocument20 pagesBoard Characteristics, State Ownership and FirmIsmanidarNo ratings yet

- Dinh ETP2021Document33 pagesDinh ETP2021Donal D MEcNo ratings yet

- Capital Structure of GLCs in MalaysiaDocument20 pagesCapital Structure of GLCs in Malaysiade_stanszaNo ratings yet

- 1 s2.0 S0264999321000730 MainDocument20 pages1 s2.0 S0264999321000730 MainAzilah AbdullahNo ratings yet

- Looking at Governance Hybridity From Different Theoretical PerspectivesDocument8 pagesLooking at Governance Hybridity From Different Theoretical PerspectivesMuhammad SetiawanNo ratings yet

- BJM-Institutional Risk ReductionDocument20 pagesBJM-Institutional Risk ReductionIrfan ur RehmanNo ratings yet

- Ownership Identity Strategy and Performa-96813252Document31 pagesOwnership Identity Strategy and Performa-96813252Sandro ManuNo ratings yet

- 9910-33101-1-SMDocument8 pages9910-33101-1-SMPhương LinhNo ratings yet

- DynamismDocument18 pagesDynamismpir bilalNo ratings yet

- Ownership Type and Company Performance: Empirical Studies in The Indonesian Stock ExchangeDocument15 pagesOwnership Type and Company Performance: Empirical Studies in The Indonesian Stock ExchangeGitha Adhi Pramana I GDNo ratings yet

- Institutions and Growth Das2016Document22 pagesInstitutions and Growth Das2016Liber Iván León OrtegaNo ratings yet

- The Value of The State-Owned Enterprises in Indonesia: A Case Study of PrivatizationDocument10 pagesThe Value of The State-Owned Enterprises in Indonesia: A Case Study of PrivatizationRecca DamayantiNo ratings yet

- 7government Ownership and The Capital Structure ofDocument15 pages7government Ownership and The Capital Structure ofMudit JhunjhunwalaNo ratings yet

- The Cross-Border Mergers and Acquisitions of Local State-Owned Enterprises: The Role of Home Country Government InvolvementDocument23 pagesThe Cross-Border Mergers and Acquisitions of Local State-Owned Enterprises: The Role of Home Country Government InvolvementNaison Shingirai PfavayiNo ratings yet

- Relationship Between Capital Structure and Profitability Evidence From Four Asian TigersDocument13 pagesRelationship Between Capital Structure and Profitability Evidence From Four Asian TigersDiki Wahyu PratamaNo ratings yet

- The Impact of Family Ownership On The Capital Structure of Palestinian FirmsDocument21 pagesThe Impact of Family Ownership On The Capital Structure of Palestinian FirmsTrầnNhaGhiNo ratings yet

- The Result Shows That Capital Structures Relationship: Khush Bakht Hina, DR Muhammad AjmalDocument9 pagesThe Result Shows That Capital Structures Relationship: Khush Bakht Hina, DR Muhammad AjmalajmrdNo ratings yet

- Extension of Determinants of Capital Structure: Evidence From Pakistani Non-Financial FirmsDocument11 pagesExtension of Determinants of Capital Structure: Evidence From Pakistani Non-Financial Firmskhalid nazirNo ratings yet

- Government Business Relations 1Document56 pagesGovernment Business Relations 1Atta Ur RehmanNo ratings yet

- For Plag CheckDocument259 pagesFor Plag CheckAftab TabasamNo ratings yet

- Ownership Structure and FinancDocument11 pagesOwnership Structure and FinancFabiolaNo ratings yet

- Corporate Governance - 2009 - Singh - Business Group Affiliation Firm Governance and Firm Performance Evidence FromDocument15 pagesCorporate Governance - 2009 - Singh - Business Group Affiliation Firm Governance and Firm Performance Evidence FromHamza NaimNo ratings yet

- Journal 4Document6 pagesJournal 4Filsha NajwaNo ratings yet

- International Business Review 28 (2019) 415-427Document13 pagesInternational Business Review 28 (2019) 415-427Isabella Velasquez RodriguezNo ratings yet

- Corporate Governance-Jan2022Document58 pagesCorporate Governance-Jan2022Maganga ShimbiNo ratings yet

- Zhang 2016Document22 pagesZhang 2016MultazamMansyurAdduryNo ratings yet

- Corporate Governance Mechanism and Cost of Capital To Firm ValueDocument14 pagesCorporate Governance Mechanism and Cost of Capital To Firm ValuetanviNo ratings yet

- L, P O S L F C: Everage Rofitability and The Wnership Tructures of Isted Irms in HinaDocument28 pagesL, P O S L F C: Everage Rofitability and The Wnership Tructures of Isted Irms in HinaNgan NguyenNo ratings yet

- Ownership Structure and Innovation: An Emerging Market PerspectiveDocument24 pagesOwnership Structure and Innovation: An Emerging Market PerspectiveAshraf KhanNo ratings yet

- Corporate Performance Improvement Through Corporate Governance MechanismsDocument9 pagesCorporate Performance Improvement Through Corporate Governance MechanismsGOH CHIN FEI FMNo ratings yet

- Exploring The Determinants of Financial Structure in The Technology Industry: Panel Data Evidence From The New York Stock Exchange Listed CompaniesDocument16 pagesExploring The Determinants of Financial Structure in The Technology Industry: Panel Data Evidence From The New York Stock Exchange Listed CompaniesyebegashetNo ratings yet

- Research Proposal - MPhil Public Policy and ManagementDocument32 pagesResearch Proposal - MPhil Public Policy and ManagementFrederick AfariNo ratings yet

- Qi Kotz 2019 The Impact of State Owned Enterprises On China S Economic GrowthDocument19 pagesQi Kotz 2019 The Impact of State Owned Enterprises On China S Economic GrowthsergiolefNo ratings yet

- Impact of Ownership Structure and Corporate Governance On Capital Structure: The Case of Vietnamese FirmsDocument9 pagesImpact of Ownership Structure and Corporate Governance On Capital Structure: The Case of Vietnamese FirmsAnugrah DilaNo ratings yet

- Almadi (2015)Document11 pagesAlmadi (2015)IvankaNo ratings yet

- Factors in Uencing International Joint Venture Performance in ThailandDocument14 pagesFactors in Uencing International Joint Venture Performance in ThailandAdrian rusuNo ratings yet

- JPSP - 2022 - 479 PDFDocument11 pagesJPSP - 2022 - 479 PDFMohamed EL-MihyNo ratings yet

- Finance Research Letters: You Li, Jian ZhangDocument9 pagesFinance Research Letters: You Li, Jian ZhangSebastián PosadaNo ratings yet

- 2023 Common Institutional Ownership and Stock Price Crash RiskDocument51 pages2023 Common Institutional Ownership and Stock Price Crash RiskAhmed EldemiryNo ratings yet

- Japan and The World Economy: Márcia Zabdiele Moreira, Mário Henrique OgasavaraDocument9 pagesJapan and The World Economy: Márcia Zabdiele Moreira, Mário Henrique OgasavaraFenesia PurbaNo ratings yet

- 5 Content ServerDocument25 pages5 Content ServerMudit JhunjhunwalaNo ratings yet

- Performance in Strategic Sectors: A Comparison of Profitability and Efficiency of State-Owned Enterprises and Private CorporationsDocument14 pagesPerformance in Strategic Sectors: A Comparison of Profitability and Efficiency of State-Owned Enterprises and Private CorporationsSiti MariamNo ratings yet

- Corporate Governance and Firm PerformancDocument18 pagesCorporate Governance and Firm PerformancAfzalNo ratings yet

- 1039 3184 1 PB PDFDocument14 pages1039 3184 1 PB PDFمريمالرئيسيNo ratings yet

- Government Ownership and The Capital Structure of Firms: Analysis of An Institutional Context From ChinaDocument15 pagesGovernment Ownership and The Capital Structure of Firms: Analysis of An Institutional Context From ChinaCorolla SedanNo ratings yet

- 1 PB PDFDocument8 pages1 PB PDFsome_one372No ratings yet

- Emerging Markets Review: Dinh Hoang Bach Phan, Chwee Ming Tee, Vuong Thao Tran TDocument13 pagesEmerging Markets Review: Dinh Hoang Bach Phan, Chwee Ming Tee, Vuong Thao Tran TDessy ParamitaNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- IOM - Handte Vortex DualDocument30 pagesIOM - Handte Vortex Duallavanesh1996No ratings yet

- Lớp 6 GS - Cuối HK2Document2 pagesLớp 6 GS - Cuối HK2Ni NyNo ratings yet

- Invoice Local: Bank Bank Bri No. Va: 131064210008527Document1 pageInvoice Local: Bank Bank Bri No. Va: 131064210008527Carvahal JamesNo ratings yet

- 2.3. Elasticity - Measure of ResonsivenessDocument2 pages2.3. Elasticity - Measure of ResonsivenessgebreNo ratings yet

- ASTM E84 Rev 11 1 2017 ED 10 31 2019Document7 pagesASTM E84 Rev 11 1 2017 ED 10 31 2019Phương HoàngNo ratings yet

- CD-2048 - 2020179082654 Durg University QPDocument3 pagesCD-2048 - 2020179082654 Durg University QPManohar SumathiNo ratings yet

- Annex 1-6-Cooperative Productive Society Fowa EnglishDocument3 pagesAnnex 1-6-Cooperative Productive Society Fowa EnglishWikileaks2024No ratings yet

- Basic Full Circle Trust Diagnostic Report 20200805154233Document1 pageBasic Full Circle Trust Diagnostic Report 20200805154233Jagat SinghNo ratings yet

- Types of CollocationDocument2 pagesTypes of CollocationPhạm NgọcNo ratings yet

- 10 - ECHO Cash & Vouchers GuidelinesDocument25 pages10 - ECHO Cash & Vouchers GuidelinesAbass GblaNo ratings yet

- Market BagDocument2 pagesMarket Bagpipistrila79No ratings yet

- To, Crystal Metallurgical Services and SolutionsDocument4 pagesTo, Crystal Metallurgical Services and SolutionsP NAVEEN KUMARNo ratings yet

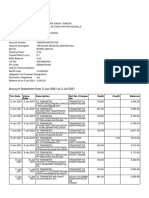

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- Channel FUSDocument1 pageChannel FUSArunKumar RajendranNo ratings yet

- What Drives GlobalisationDocument8 pagesWhat Drives GlobalisationLINDA MUTIMBIA WAMALWANo ratings yet

- HEJCL23Document10 pagesHEJCL23idilsagal2021No ratings yet

- Cheats de Pokemon Radical Red My BoyDocument14 pagesCheats de Pokemon Radical Red My BoyHyrum MamaniNo ratings yet

- Unit+1+ +Introduction+to+Agricultural+EconomicsDocument28 pagesUnit+1+ +Introduction+to+Agricultural+EconomicsDIMAKATSONo ratings yet

- Exam 2023Document3 pagesExam 2023Muhammad UsmanNo ratings yet

- Index NumbersDocument7 pagesIndex NumbersAllauddinaghaNo ratings yet

- Performance BudgetingDocument2 pagesPerformance BudgetingDr Ringco TrozanNo ratings yet

- DSC1520 Notes and Past PapersDocument168 pagesDSC1520 Notes and Past PapersMaks MahlatsiNo ratings yet

- Detailed Advertisement English Nov22Document6 pagesDetailed Advertisement English Nov22VijayNo ratings yet

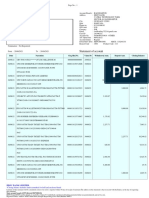

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument8 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceKartikey SharmaNo ratings yet

- The Production FunctionDocument2 pagesThe Production FunctionaiiaiaiaiaNo ratings yet