You might also like

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- ASDocument58 pagesASAshutosh SinghNo ratings yet

- 13.2 AS 1 Disclosure of Accounting PoliciesDocument4 pages13.2 AS 1 Disclosure of Accounting PoliciesRohith KumarNo ratings yet

- Disclosure of Accounting Policies: ObjectivesDocument8 pagesDisclosure of Accounting Policies: ObjectivesrazorNo ratings yet

- As1 CaDocument2 pagesAs1 CaĐėvıł ĶıñgNo ratings yet

- AS1 - Disclosure of Accounting PoliciesDocument3 pagesAS1 - Disclosure of Accounting PoliciesAashutosh PatodiaNo ratings yet

- Accounting Standard 1 PDFDocument4 pagesAccounting Standard 1 PDFChristopher Jacob MurmuNo ratings yet

- As 1Document4 pagesAs 1abhishekkapse654No ratings yet

- Accounting Standard PoliciesDocument4 pagesAccounting Standard Policiesashishoraon789835No ratings yet

- Final CHP T 2Document152 pagesFinal CHP T 2Marikrishna Chandran CA100% (1)

- Accounting Standard 1Document9 pagesAccounting Standard 1ritusexyNo ratings yet

- AS-1 Disclosure of Accounting Policies: CMA S. BaskaranDocument11 pagesAS-1 Disclosure of Accounting Policies: CMA S. BaskaranS. BaskaranNo ratings yet

- Accounts Nitin SirDocument11 pagesAccounts Nitin Sirpuneet.sharma1493No ratings yet

- Other Standards: 1 IAS 8 Accounting Policies, Changes in Accounting Estimates & ErrorsDocument7 pagesOther Standards: 1 IAS 8 Accounting Policies, Changes in Accounting Estimates & Errorshafeez azizNo ratings yet

- AS 1 DISCLOSURE OF ACCOUNTING POLICIESDocument23 pagesAS 1 DISCLOSURE OF ACCOUNTING POLICIESYash ParekhNo ratings yet

- Accounting Standard 1Document7 pagesAccounting Standard 1api-3828505No ratings yet

- MFRS108 Accounting Policies, Estimates, ErrorsDocument23 pagesMFRS108 Accounting Policies, Estimates, ErrorsDont RushNo ratings yet

- Disclosure of Accounting Policies under AS-1Document9 pagesDisclosure of Accounting Policies under AS-1Dipak UgaleNo ratings yet

- 4 MFRS108Document34 pages4 MFRS108Dont RushNo ratings yet

- Accounting Policies and ErrorsDocument32 pagesAccounting Policies and ErrorsTia Li100% (1)

- IAS 8: Accounting Policies, Changes in Accounting Estimates and ErrorsDocument6 pagesIAS 8: Accounting Policies, Changes in Accounting Estimates and ErrorsmuhammadTzNo ratings yet

- Disclosure of Accounting Policies StandardDocument9 pagesDisclosure of Accounting Policies StandardAkshi BhagiaNo ratings yet

- Unit 2: Overview of Accounting Standards: After Studying This Unit, You Will Be Able ToDocument138 pagesUnit 2: Overview of Accounting Standards: After Studying This Unit, You Will Be Able Totauseefalam917100% (1)

- Accounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesDocument5 pagesAccounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesSuhasini GummeNo ratings yet

- LKAS 8 Accounting Policies (New)Document33 pagesLKAS 8 Accounting Policies (New)Kogularamanan NithiananthanNo ratings yet

- AS 1: Disclosure of Accounting Policies: IPCC Paper 1: Accounting Chapter 1 Unit 2Document31 pagesAS 1: Disclosure of Accounting Policies: IPCC Paper 1: Accounting Chapter 1 Unit 2sam hajamatNo ratings yet

- Statement of Changes in Equity, Accounting PoliciesDocument9 pagesStatement of Changes in Equity, Accounting Policiesman ibeNo ratings yet

- Accounting Standard: 1: Disclosure of Accounting PoliciesDocument6 pagesAccounting Standard: 1: Disclosure of Accounting PoliciesAbhinav AggarwalNo ratings yet

- Disclosure of Accounting PoliciesDocument7 pagesDisclosure of Accounting PoliciesgimmyjoyNo ratings yet

- As-1 Disclosure of Accounting PoliciesDocument7 pagesAs-1 Disclosure of Accounting PoliciesPrakash_Tandon_583No ratings yet

- 3 Overview of Accounting StandardsDocument136 pages3 Overview of Accounting StandardsAlok Kumar100% (1)

- Smu Assanment (41 q2)Document3 pagesSmu Assanment (41 q2)shaileshNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument29 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsSheda AshrafNo ratings yet

- Accounting Standard 1Document27 pagesAccounting Standard 1Sid2875% (4)

- Accounting Standard (AS) 1: (Issued 1979)Document7 pagesAccounting Standard (AS) 1: (Issued 1979)anoop_mishra1986No ratings yet

- Advancd Acc Ca Inter cp-4Document15 pagesAdvancd Acc Ca Inter cp-4Pooja Suresh BNo ratings yet

- International Accounting Standard-8: Accounting Policies, Changes in Accounting Estimates and ErrorsDocument29 pagesInternational Accounting Standard-8: Accounting Policies, Changes in Accounting Estimates and ErrorsEric Agyenim-BoatengNo ratings yet

- SFAC No 5Document28 pagesSFAC No 5Clara Indira PurnamasariNo ratings yet

- Disclosure of Accounting PoliciesDocument8 pagesDisclosure of Accounting Policiesabdullah0331No ratings yet

- Accounting PoliciesDocument4 pagesAccounting PoliciesNaresh PalabandlaNo ratings yet

- Disclosure of Accounting PoliciesDocument7 pagesDisclosure of Accounting PoliciesSatesh Kumar KonduruNo ratings yet

- Accounting PoliciesDocument6 pagesAccounting PoliciesShalini TiwariNo ratings yet

- Section 10Document20 pagesSection 10Abata BageyuNo ratings yet

- IAS 8 Diana Maruf AnasDocument24 pagesIAS 8 Diana Maruf AnasLamis ShalabiNo ratings yet

- As1-Diclosure of Accounting PoliciesDocument6 pagesAs1-Diclosure of Accounting PoliciesDharmesh MistryNo ratings yet

- Accounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting PoliciesDocument4 pagesAccounting Standard (AS) 1 (Issued 1979) : Disclosure of Accounting Policiessaradindu123No ratings yet

- Chapter 2 Accounting Concepts - ConventionsDocument32 pagesChapter 2 Accounting Concepts - ConventionsfaaNo ratings yet

- 07. Accounting Changes and ErrorsDocument31 pages07. Accounting Changes and Errorslascona.christinerheaNo ratings yet

- AS - 1 - Disclosure - of - Accounting - Policies CH-4Document7 pagesAS - 1 - Disclosure - of - Accounting - Policies CH-4lucifersdevil68No ratings yet

- AS 1 Disclosure of Accounting PoliciesDocument3 pagesAS 1 Disclosure of Accounting PoliciesSonali PuriNo ratings yet

- 1 As Disclouser of Accounting PoliciesDocument6 pages1 As Disclouser of Accounting Policiesanisahemad1178No ratings yet

- Workbook 6 (July 2022)Document60 pagesWorkbook 6 (July 2022)Sansaar KandhroNo ratings yet

- ACC2001 Lecture 5Document50 pagesACC2001 Lecture 5michael krueseiNo ratings yet

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Master Budgeting and Forecasting for Hospitality Industry-Teaser: Financial Expertise series for hospitality, #1From EverandMaster Budgeting and Forecasting for Hospitality Industry-Teaser: Financial Expertise series for hospitality, #1No ratings yet

- Beyond Marketing: Customer Relationship Management (CRM)Document49 pagesBeyond Marketing: Customer Relationship Management (CRM)Diamond MC TaiNo ratings yet

- Pricing Issues and Post-Transaction Issues: Chapter Learning ObjectivesDocument11 pagesPricing Issues and Post-Transaction Issues: Chapter Learning ObjectivesDINEO PRUDENCE NONGNo ratings yet

- 2020 Benchmarking Look InsideDocument28 pages2020 Benchmarking Look InsideSunil GiriNo ratings yet

- Phonics Stage 1 PDFDocument50 pagesPhonics Stage 1 PDFMehwish Azmat83% (6)

- Case Study Columbus InstrumentsDocument8 pagesCase Study Columbus Instrumentsramji100% (6)

- SALES FORECASTING TECHNIQUESDocument12 pagesSALES FORECASTING TECHNIQUESUjjwal MalhotraNo ratings yet

- Long-Term Construction Contracts & FranchiseDocument6 pagesLong-Term Construction Contracts & FranchiseBryan ReyesNo ratings yet

- Adamson University Intermediate Accounting 1 Receivable Financing - AssignmentDocument9 pagesAdamson University Intermediate Accounting 1 Receivable Financing - AssignmentKhai Supleo PabelicoNo ratings yet

- Forum Discussion - Thibasri VasuDocument2 pagesForum Discussion - Thibasri VasuLokanayaki SubramaniamNo ratings yet

- Auditing Practices and Financial Performance of SACCOs in GondarDocument4 pagesAuditing Practices and Financial Performance of SACCOs in Gondarabraham admassieNo ratings yet

- Host Manual COBAS - INTEGRA - 400 - Plus PDFDocument144 pagesHost Manual COBAS - INTEGRA - 400 - Plus PDFnestordaniel7633% (3)

- Terms of Delivery - Sauter Feinmechanik GMBHDocument7 pagesTerms of Delivery - Sauter Feinmechanik GMBHCarloncho LonchoNo ratings yet

- 2008 - APOL - APOL - Annual Report - 2008Document182 pages2008 - APOL - APOL - Annual Report - 2008Daniel ManuNo ratings yet

- Module Week 3 ACTG 1Document6 pagesModule Week 3 ACTG 1REMON HOGMONNo ratings yet

- SMB Strategy and Planning ToolkitDocument36 pagesSMB Strategy and Planning ToolkitJovany GrezNo ratings yet

- Chapter 4Document16 pagesChapter 4iwang saudjiNo ratings yet

- Strategic Management Practices of Selected State Universities and Colleges in Samar Island, PhilippinesDocument13 pagesStrategic Management Practices of Selected State Universities and Colleges in Samar Island, PhilippinesChelsie ColifloresNo ratings yet

- Graham Mayor: Word Variables, Properties and Content Controls and Bookmarks Editor Add-In For Word 2007/2010/2013Document11 pagesGraham Mayor: Word Variables, Properties and Content Controls and Bookmarks Editor Add-In For Word 2007/2010/2013Sumith VkNo ratings yet

- Performance ManagementDocument8 pagesPerformance ManagementBassam AlqadasiNo ratings yet

- Budget Cycle Both LGU and National Government AgenciesDocument41 pagesBudget Cycle Both LGU and National Government AgenciesKrizzel Sandoval100% (1)

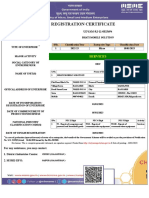

- Print - Udyam Registration CertificateDocument1 pagePrint - Udyam Registration CertificatelalitpooniaNo ratings yet

- Kuis Akun No 1Document10 pagesKuis Akun No 1Daveli NatanaelNo ratings yet

- Data Driven Facebook Ads Checklist-Fillable-1 PDFDocument29 pagesData Driven Facebook Ads Checklist-Fillable-1 PDFSergiu Alexandru VlasceanuNo ratings yet

- Organizational Change ManagementDocument235 pagesOrganizational Change ManagementtavanNo ratings yet

- HidadfrDocument55 pagesHidadfrArvind JSNo ratings yet

- ATS9900 V100R006C00 Feature List FTDocument14 pagesATS9900 V100R006C00 Feature List FTaranibarmNo ratings yet

- Scan To Scribd With CcscanDocument13 pagesScan To Scribd With CcscanclarkcclNo ratings yet

- Syslog MessagesDocument758 pagesSyslog MessagesHai Nguyen Khuong0% (1)

- 2.3 Metrobank Vs Junnel's MarketingDocument29 pages2.3 Metrobank Vs Junnel's MarketingMarion Yves MosonesNo ratings yet

- MDSAP Medical Device Single Audit Program OverviewDocument31 pagesMDSAP Medical Device Single Audit Program OverviewAditya C KNo ratings yet